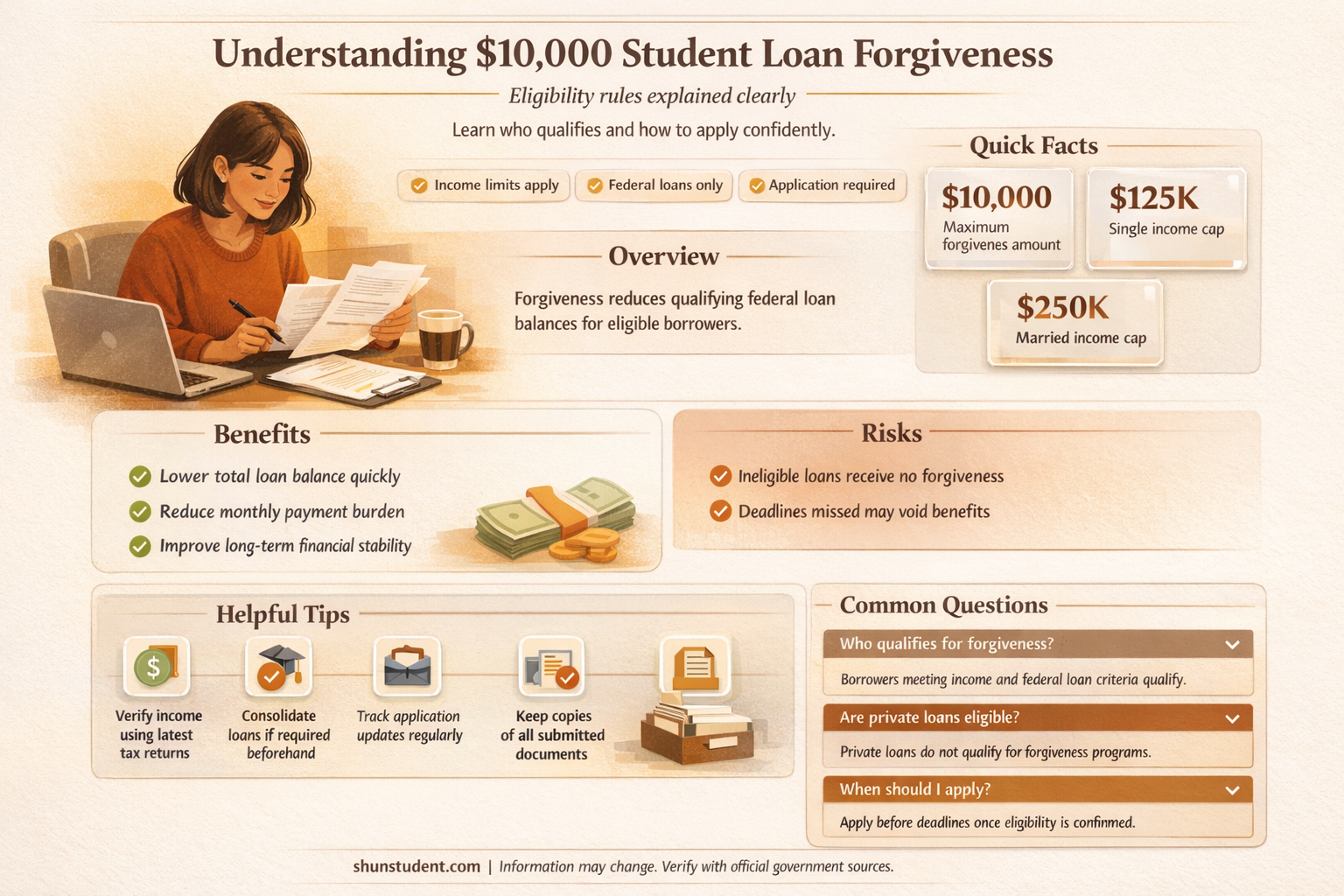

If you're wondering whether you're eligible for the $10,000 student loan forgiveness program, it's essential to understand the specific criteria set by the government. This program, often referred to as the federal student loan forgiveness initiative, is designed to provide relief to borrowers who meet certain requirements, such as having federal student loans and an income below a specified threshold. Eligibility typically depends on factors like the type of loans you have, your repayment plan, and your employment status, particularly if you work in public service or for a qualifying non-profit organization. Additionally, the recent updates to the program may have expanded eligibility, so it’s crucial to review the latest guidelines from the Department of Education to determine if you qualify for this significant financial relief.

| Characteristics | Values |

|---|---|

| Loan Type | Federal student loans (Direct Loans, FFELP Loans, Perkins Loans) |

| Income Eligibility | Not applicable (no income limits for $10,000 forgiveness) |

| Forgiveness Amount | Up to $10,000 |

| Additional Forgiveness for Pell Grants | Up to $20,000 for borrowers with Pell Grants |

| Application Requirement | Automatic for most borrowers; manual application for some (e.g., FFELP) |

| Eligibility Period | Borrowers with loans disbursed before July 1, 2022 |

| Income-Driven Repayment (IDR) Adjustment | Fixes IDR payment counts retroactively (separate from $10,000 forgiveness) |

| Tax Implications | Tax-free under the American Rescue Plan Act |

| Deadline to Apply | December 31, 2023 (for manual applications) |

| Current Status | Application paused due to legal challenges (as of November 2023) |

| Eligibility for Private Loans | Not eligible (only federal loans qualify) |

| Employment Requirements | No specific employment requirements |

| Loan Status | Eligible regardless of repayment status (e.g., in default, forbearance) |

| Citizenship Requirement | U.S. citizens, permanent residents, or eligible non-citizens |

| Debt Limit | No cap on total debt amount for eligibility |

Explore related products

What You'll Learn

![]()

Income-Driven Repayment Plan Requirements

To qualify for the $10,000 student loan forgiveness under income-driven repayment (IDR) plans, understanding the specific requirements is crucial. These plans adjust your monthly payments based on your income and family size, potentially leading to forgiveness after 20–25 years of qualifying payments. However, not all borrowers meet the criteria, and the rules can be complex. Here’s a breakdown to help you navigate the process.

First, eligibility hinges on the type of federal student loans you hold. Direct Loans, including subsidized and unsubsidized Stafford Loans, PLUS Loans, and Consolidation Loans, are eligible for IDR plans. Federal Family Education Loans (FFEL) and Perkins Loans are generally ineligible unless consolidated into a Direct Loan. If your loans fall outside these categories, consolidation might be your first step. For instance, consolidating FFEL loans into a Direct Consolidation Loan can open the door to IDR plans and, subsequently, forgiveness opportunities.

Next, your income and family size play a pivotal role in determining your monthly payment. IDR plans calculate payments as a percentage of your discretionary income, typically 10–20%, depending on the plan. For example, the Revised Pay As You Earn (REPAYE) Plan caps payments at 10% of discretionary income for all borrowers. To qualify, your income must fall below a certain threshold relative to your federal poverty guideline. A single borrower earning $30,000 annually with no dependents might pay significantly less than someone earning $60,000 under the same plan. Use the Federal Student Aid website’s Loan Simulator to estimate your payments and forgiveness timeline.

Maintaining eligibility requires annual recertification of your income and family size. Failure to recertify on time can result in a switch to the standard repayment plan, which often has higher monthly payments. Set reminders to submit your updated information each year to avoid disruptions. Additionally, keep detailed records of your payments, as administrative errors can delay forgiveness. For example, payments made under certain plans, like Income-Based Repayment (IBR), must be documented to count toward the 20–25-year forgiveness threshold.

Finally, consider the tax implications of loan forgiveness. While the $10,000 forgiveness under recent initiatives may be tax-free, forgiveness after 20–25 years of IDR payments is typically treated as taxable income. Plan ahead by consulting a tax professional or setting aside funds to cover potential tax liabilities. For instance, if $50,000 is forgiven after 25 years, you might owe taxes on that amount, depending on current tax laws.

In summary, income-driven repayment plans offer a pathway to student loan forgiveness, but eligibility depends on loan type, income, and consistent recertification. By understanding these requirements and taking proactive steps, you can maximize your chances of qualifying for forgiveness while minimizing financial surprises.

Illinois Tax Rules: Does Student Loan Forgiveness Count as Income?

You may want to see also

Explore related products

![]()

Public Service Loan Forgiveness Criteria

The Public Service Loan Forgiveness (PSLF) program offers a pathway to debt relief for those committed to a career in public service. However, eligibility hinges on a strict set of criteria that borrowers must meticulously navigate. Understanding these requirements is crucial for anyone seeking to leverage this program.

First, employment is the cornerstone of PSLF eligibility. Borrowers must be employed full-time by a qualifying employer, which includes government organizations at any level (federal, state, local), non-profit organizations that are tax-exempt under Section 501(c)(3) of the Internal Revenue Code, and some other types of non-profits that provide certain public services. Part-time work can also qualify if it meets the employer’s definition of full-time or involves at least 30 hours per week.

Secondly, the type of loan and repayment plan are pivotal. Only Direct Loans are eligible for PSLF. Borrowers with other federal loans, such as Federal Family Education Loan (FFEL) Program loans or Perkins Loans, must consolidate them into a Direct Consolidation Loan to qualify. Additionally, borrowers must be enrolled in an income-driven repayment (IDR) plan, which ties monthly payments to income and family size. These plans include Income-Based Repayment (IBR), Pay As You Earn (PAYE), Revised Pay As You Earn (REPAYE), and Income-Contingent Repayment (ICR).

Finally, the forgiveness process requires consistent documentation and application. Borrowers should submit the Employment Certification Form (ECF) annually or when changing employers to ensure their employment qualifies and to track their progress toward the required 120 qualifying payments. After making these payments, borrowers must submit the PSLF application to receive forgiveness.

In summary, while PSLF offers significant relief, it demands careful planning and adherence to specific criteria. Borrowers must verify their employment, loan type, and repayment plan, and maintain diligent record-keeping to maximize their chances of success.

Biden Student Loan Forgiveness: Step-by-Step Application Guide for Borrowers

You may want to see also

Explore related products

![]()

Federal Student Loan Eligibility

Determining eligibility for federal student loan forgiveness requires understanding the specific criteria tied to different programs. The most widely discussed is the Public Service Loan Forgiveness (PSLF) program, which forgives remaining loan balances after 120 qualifying payments for borrowers working full-time in eligible public service jobs. To qualify, your loans must be federal Direct Loans, and payments must be made under an income-driven repayment plan. Notably, this program is not a one-time $10,000 forgiveness but a pathway to full loan discharge after meeting stringent requirements.

Another critical factor is the type of federal loans you hold. Only Direct Loans are eligible for PSLF and other forgiveness programs like Teacher Loan Forgiveness or Income-Driven Repayment (IDR) forgiveness. Federal Family Education Loans (FFEL) and Perkins Loans, unless consolidated into a Direct Loan, do not qualify. Consolidation can be a strategic step to make ineligible loans eligible, but it resets the payment counter for PSLF, so timing is crucial.

Income-driven repayment plans play a pivotal role in federal loan forgiveness eligibility. Plans like REPAYE, PAYE, IBR, and ICR cap monthly payments at a percentage of your discretionary income and offer forgiveness after 20–25 years of payments, depending on the plan. For example, REPAYE forgives remaining balances after 20 years for undergraduate loans and 25 years for graduate loans. However, the forgiven amount may be taxed as income, so planning for this potential liability is essential.

Employment status and sector significantly impact eligibility. Borrowers in public service roles, such as government, non-profit, or certain healthcare positions, have a clear path to PSLF. Teachers in low-income schools may qualify for up to $17,500 in forgiveness through the Teacher Loan Forgiveness program. Conversely, private-sector employees typically rely on IDR forgiveness, which takes longer and requires consistent enrollment in an eligible repayment plan.

Finally, stay vigilant about program updates and temporary waivers. For instance, the limited PSLF waiver in 2022 allowed past payments on ineligible loans to count toward forgiveness, benefiting many borrowers. Such waivers are rare but underscore the importance of monitoring federal announcements and consulting resources like the Federal Student Aid website. Eligibility for $10,000 in forgiveness often refers to targeted relief initiatives, such as those tied to economic stimulus or executive actions, which have distinct criteria and application processes. Always verify your loan type, repayment plan, and employment status to maximize your chances of qualifying.

Discover Student Loan Forgiveness Programs: A Comprehensive Guide for Borrowers

You may want to see also

Explore related products

![]()

Loan Type and Consolidation Rules

Not all student loans qualify for the $10,000 forgiveness program. Eligibility hinges on loan type and consolidation status. Federal Direct Loans, including subsidized, unsubsidized, and PLUS loans borrowed directly from the Department of Education, are generally eligible. Federal Family Education Loans (FFEL) and Perkins Loans held by the government also qualify, but privately held FFEL loans do not. Consolidating FFEL loans into a Direct Consolidation Loan can make them eligible, but timing matters: consolidation must occur before applying for forgiveness to ensure the new loan retains eligibility.

Consolidation can be a double-edged sword in this context. While it can simplify repayment by combining multiple loans into one, it resets the clock on forgiveness programs tied to payment counts, such as Public Service Loan Forgiveness (PSLF). For the $10,000 forgiveness, consolidation primarily affects eligibility based on loan type. Borrowers with a mix of eligible and ineligible loans should carefully consider whether consolidation aligns with their forgiveness goals. For instance, consolidating a private FFEL loan into a Direct Loan opens the door to forgiveness but may not be worth the potential loss of benefits tied to the original loan.

Borrowers must also navigate the rules around consolidation timing. Applying for forgiveness before consolidating ineligible loans can result in disqualification. Conversely, consolidating too late might exclude the new Direct Consolidation Loan from forgiveness if the application window has closed. A strategic approach involves reviewing loan types, checking eligibility, and consolidating only if necessary to maximize forgiveness potential. Tools like the National Student Loan Data System (NSLDS) can help identify loan types and holders, ensuring informed decisions.

Practical steps include first verifying loan types through the NSLDS or loan servicer. If ineligible loans are identified, research consolidation options and their implications. Borrowers should also monitor program updates, as rules can change. For example, temporary waivers or extensions might allow FFEL borrowers to consolidate without losing eligibility for other programs. Consulting a financial advisor or student loan specialist can provide tailored guidance, especially for complex loan portfolios. Proactive management of loan type and consolidation rules is key to securing the $10,000 forgiveness.

Understanding Student Loan Forgiveness: Payments and Eligibility Explained

You may want to see also

Explore related products

![]()

Application Process and Deadlines

The application process for the $10,000 student loan forgiveness program is straightforward but requires attention to detail. Borrowers must complete an online form provided by the U.S. Department of Education, which typically asks for personal information, loan details, and income verification. This form is designed to be user-friendly, but applicants should gather all necessary documents beforehand, such as tax returns and loan account numbers, to streamline the process. Submitting accurate information is critical, as errors can delay approval or result in disqualification.

Deadlines for the $10,000 student loan forgiveness program vary depending on the type of loan and the borrower’s circumstances. For federal student loan borrowers, the application window often aligns with broader relief initiatives, such as the Public Service Loan Forgiveness (PSLF) or income-driven repayment plans. For example, borrowers pursuing PSLF must submit their forgiveness application after making 120 qualifying payments, while those seeking forgiveness under income-driven plans may have a different timeline. It’s essential to monitor official announcements from the Department of Education to ensure compliance with specific deadlines.

One common misconception is that the application process is automatic. In reality, borrowers must actively apply for forgiveness, even if they believe they meet all eligibility criteria. This proactive step is often overlooked, leading to missed opportunities. Additionally, borrowers should be aware of potential scams. Legitimate applications are always free and can only be submitted through official government channels. Any service offering to expedite the process for a fee is likely fraudulent.

For borrowers with multiple loans, prioritizing which loans to apply for forgiveness can be strategic. Direct Loans, for instance, are typically eligible for the $10,000 forgiveness, while FFEL or Perkins Loans may require consolidation into the Direct Loan program first. This consolidation process can take several weeks, so starting early is advisable. Borrowers should also consider their long-term financial goals, as forgiveness may impact credit scores or tax liabilities, though the $10,000 forgiveness is generally tax-free under current law.

Finally, staying informed about updates to the program is crucial. The Department of Education frequently releases guidance and FAQs to clarify eligibility and application procedures. Subscribing to official newsletters or following trusted financial advisors can help borrowers navigate changes effectively. While the process may seem daunting, careful preparation and adherence to deadlines can significantly increase the chances of successfully securing the $10,000 student loan forgiveness.

Obama Loan Forgiveness: Did Students Receive Reimbursement?

You may want to see also

Frequently asked questions

Eligibility for the $10,000 student loan forgiveness typically applies to borrowers with federal student loans who meet income requirements, such as individuals earning less than $125,000 annually or married couples filing jointly earning less than $250,000.

No, the $10,000 student loan forgiveness program only applies to federal student loans, such as Direct Loans, FFEL Loans, and Perkins Loans. Private loans are not eligible.

Borrowers typically need to submit an application through the U.S. Department of Education’s website or their loan servicer. Details and application processes may vary depending on the specific forgiveness program.

Yes, borrowers who have already made payments on their federal student loans may still be eligible for the $10,000 forgiveness, provided they meet the income and loan type requirements.

The $10,000 student loan forgiveness is generally tax-free at the federal level, thanks to the American Rescue Plan Act. However, state tax treatment may vary, so check your state’s tax laws.