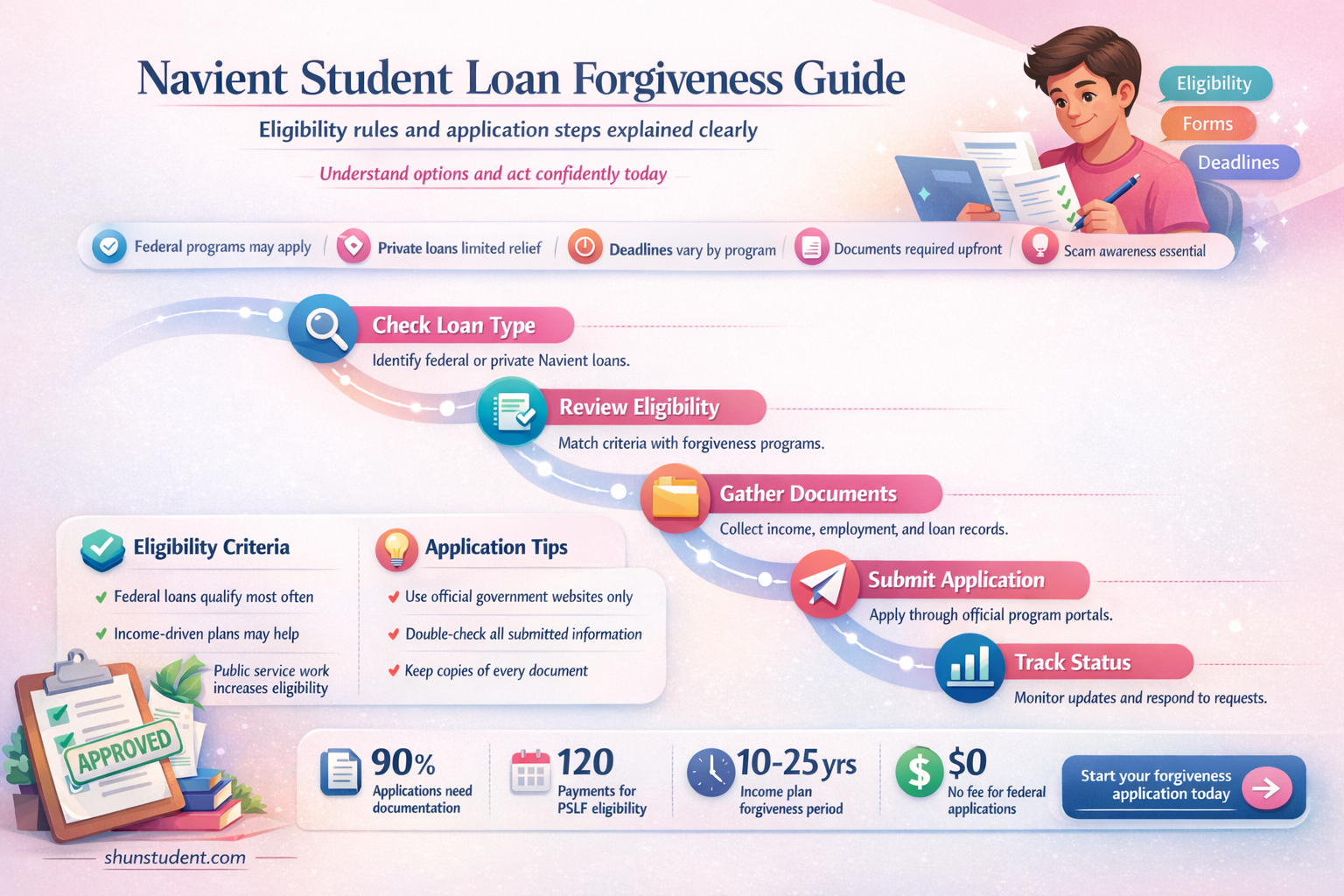

If you're wondering whether you're eligible for Navient student loan forgiveness, it's important to understand the various programs and options available. Navient, one of the largest student loan servicers, has been involved in several settlements and lawsuits, leading to potential loan forgiveness opportunities for certain borrowers. Eligibility often depends on factors such as the type of loans you have (federal or private), your repayment history, and whether you qualify for programs like Public Service Loan Forgiveness (PSLF), Borrower Defense to Repayment, or settlements related to Navient's past practices. To determine your eligibility, review your loan details, check for any updates from Navient or the Department of Education, and consider consulting with a student loan advisor or attorney specializing in student debt relief.

Explore related products

What You'll Learn

![]()

Income-Driven Repayment Plans

Income-driven repayment (IDR) plans are a lifeline for borrowers struggling to manage their Navient student loans. These plans adjust your monthly payments based on your income and family size, often reducing them to a more manageable amount. For instance, if you earn $40,000 annually and have a family of three, your payment under an IDR plan could drop from $500 to as low as $100 per month. This flexibility can prevent default and keep your loans in good standing, a critical factor for eligibility in forgiveness programs like Public Service Loan Forgiveness (PSLF).

To qualify for an IDR plan, you must demonstrate partial financial hardship, which is calculated by comparing your adjusted gross income (AGI) to the federal poverty guideline for your family size. For example, in 2023, the poverty guideline for a family of four is $30,000. If your AGI is $45,000, you’re likely eligible for reduced payments. Navient offers four IDR plans: Income-Based Repayment (IBR), Pay As You Earn (PAYE), Revised Pay As You Earn (REPAYE), and Income-Contingent Repayment (ICR). Each plan has unique eligibility criteria and payment caps, so it’s essential to choose the one that aligns with your financial situation and long-term goals.

One of the most compelling aspects of IDR plans is their pathway to loan forgiveness. After 20–25 years of qualifying payments, any remaining balance is forgiven, though you may owe taxes on the forgiven amount. For example, if you owe $60,000 and make consistent payments under REPAYE for 24 years, the remaining balance could be forgiven. However, this timeline can be shortened to 10 years if you work in public service and qualify for PSLF. Pairing an IDR plan with PSLF is a strategic move for borrowers in government or nonprofit roles, as it minimizes payments while maximizing forgiveness potential.

While IDR plans offer significant benefits, they’re not without drawbacks. Lower monthly payments extend the loan term, meaning you’ll pay more in interest over time. Additionally, if your income increases, so will your payments. To navigate these challenges, consider recertifying your income annually to ensure your payments remain affordable. Tools like the Federal Student Aid Repayment Estimator can help you project payments under different plans. Finally, stay vigilant about documentation—errors in income reporting or missed recertifications can disqualify you from IDR and forgiveness programs.

In summary, income-driven repayment plans are a powerful tool for managing Navient student loans and qualifying for forgiveness. By understanding eligibility criteria, choosing the right plan, and staying proactive with recertifications, you can leverage IDR to achieve financial stability and, ultimately, debt relief. Whether you’re aiming for 10-year PSLF forgiveness or 25-year balance discharge, IDR plans provide a structured path to navigate your student loan journey.

Biden's Student Debt Forgiveness Plan: What You Need to Know

You may want to see also

Explore related products

![]()

Public Service Loan Forgiveness (PSLF)

To qualify for PSLF, borrowers must meet specific criteria. First, your loans must be federal Direct Loans; other types, like FFEL or Perkins Loans, require consolidation into a Direct Consolidation Loan. Second, you must work full-time for a qualifying employer, such as a government organization, 501(c)(3) nonprofit, or certain other entities providing public services. Part-time workers can combine hours from multiple qualifying employers to meet the full-time requirement, typically 30 hours per week or the employer’s definition of full-time. Lastly, you must make 120 qualifying payments under an income-driven repayment plan, such as Income-Based Repayment (IBR) or Pay As You Earn (PAYE), while employed in a qualifying role.

One common pitfall borrowers face is assuming their payments automatically count toward PSLF. In reality, each payment must meet strict criteria: it must be made on time, for the full amount due, and while employed in a qualifying role. To ensure progress, submit an Employment Certification Form (ECF) annually or whenever you change employers. This form verifies your eligibility and helps track your payments, reducing the risk of errors later. Additionally, switching repayment plans or consolidating loans can reset your payment count, so proceed with caution and consult the PSLF Help Tool for guidance.

PSLF is particularly advantageous for borrowers with high debt-to-income ratios, such as those in social work, education, or healthcare. For example, a teacher with $100,000 in loans earning $45,000 annually could see monthly payments as low as $200 under IBR, with the remaining balance forgiven after 10 years of service. Compare this to standard repayment, where payments would exceed $1,000 monthly, and the value of PSLF becomes clear. However, this program requires long-term commitment; borrowers must carefully plan their careers and finances to maximize benefits.

In conclusion, PSLF is a powerful tool for those dedicated to public service, offering a clear path to debt freedom. By understanding eligibility requirements, avoiding common mistakes, and strategically managing payments, borrowers can leverage this program to achieve financial stability. While the process demands diligence, the reward—tax-free loan forgiveness—is well worth the effort for those who qualify.

Does the CARE Act Offer Student Loan Forgiveness? What You Need to Know

You may want to see also

Explore related products

$32.98 $44.99

![]()

Teacher Loan Forgiveness Eligibility

Teachers seeking Navient student loan forgiveness through the Teacher Loan Forgiveness Program must meet specific criteria to qualify for up to $17,500 in debt relief. First, eligibility hinges on employment: you must teach full-time for five consecutive academic years in a low-income school or educational service agency. The Federal Student Aid office maintains a directory of eligible schools, so verify your institution’s status before applying. Second, loan type matters—only Federal Direct Loans and Federal Stafford Loans qualify; Perkins Loans and private loans are excluded. Third, timing is critical: your teaching service must begin after October 1, 1998, and you must have taken out the loans before the end of your five-year teaching period.

Analyzing the eligibility requirements reveals a clear emphasis on commitment to underserved communities. The $17,500 maximum forgiveness is reserved for secondary school math and science teachers, as well as special education teachers; others may receive up to $5,000. This tiered structure incentivizes high-need specialties, reflecting policy priorities. Notably, the program does not require proof of financial hardship, focusing instead on service in low-income schools. However, partial years of teaching do not count toward the five-year requirement, so consistency is key.

To navigate this process effectively, start by confirming your school’s eligibility and loan type. Next, maintain detailed records of your teaching years, including contracts and certifications. Once you complete five years, submit the Teacher Loan Forgiveness Application to your loan servicer, ensuring all fields are accurate. Be cautious of scams promising expedited forgiveness—the official process is free and handled through your servicer. Finally, consider pairing this program with Public Service Loan Forgiveness (PSLF) if you continue in public service, as the two can complement each other for maximum debt relief.

Comparing Teacher Loan Forgiveness to other Navient forgiveness options highlights its accessibility for educators. Unlike PSLF, which requires 10 years of service, this program offers relief in half the time. However, it’s more restrictive in terms of eligible loans and schools. For teachers in high-need fields, the higher forgiveness cap makes it a compelling choice. By understanding these nuances, educators can strategically plan their loan repayment and maximize available benefits.

Can Federal Student Loans Be Forgiven? Exploring Loan Forgiveness Options

You may want to see also

Explore related products

![]()

Total and Permanent Disability Discharge

If you’re unable to work due to a severe disability, the Total and Permanent Disability (TPD) Discharge program offers a pathway to eliminate your Navient student loans. This federal initiative recognizes that individuals facing long-term disabilities should not be burdened by insurmountable debt. To qualify, you must provide documented proof of your disability, which can come from the U.S. Department of Veterans Affairs, the Social Security Administration, or a physician’s certification. The process is rigorous but designed to ensure fairness and support for those in genuine need.

Steps to Apply for TPD Discharge

Begin by obtaining the TPD discharge application from the U.S. Department of Education’s website. You’ll need to complete the form and submit it along with the required disability documentation. If you’re a veteran, a VA determination of unemployability suffices. For Social Security Disability Insurance (SSDI) recipients, ensure you’ve received a benefit notice within the past three years. Alternatively, a physician’s certification form, available on the Federal Student Aid website, must be filled out by a licensed doctor verifying your permanent disability. Once submitted, your loans will be placed in a monitoring period, during which you must not earn above the poverty guideline or receive a new federal loan.

Cautions and Common Pitfalls

While TPD discharge can be life-changing, it’s not without potential drawbacks. Approved discharges may be considered taxable income, depending on the year of approval, so consult a tax professional to plan accordingly. Additionally, the monitoring period requires vigilance; failing to meet its conditions could result in loan reinstatement. Be wary of scams promising expedited TPD approval—the process is free and should only be handled through official channels. Lastly, if your disability status changes during the monitoring period, report it immediately to avoid complications.

Practical Tips for a Smooth Process

To streamline your application, gather all necessary documents before starting. Keep copies of everything submitted for your records. If using a physician’s certification, ensure your doctor understands the criteria and completes the form accurately. For SSDI recipients, verify your benefit status via the Social Security Administration’s online portal. Stay proactive during the monitoring period by tracking your income and loan activity. Finally, consider setting up alerts for important deadlines or updates from your loan servicer.

Long-Term Impact and Takeaway

TPD discharge not only eliminates your student loan debt but also provides financial breathing room to focus on your health and well-being. While the process demands attention to detail, the relief it offers is invaluable for those facing permanent disabilities. By understanding the requirements and staying organized, you can navigate this program successfully and secure a more stable financial future. Remember, this isn’t just about loan forgiveness—it’s about reclaiming your peace of mind.

Unlocking Debt-Free Future: Guide to Federal Student Loan Forgiveness

You may want to see also

Explore related products

![]()

Borrower Defense to Repayment Rules

Borrower Defense to Repayment (BDR) is a federal provision that allows borrowers to seek student loan forgiveness if their school engaged in misconduct or violated certain laws. For those with Navient-serviced loans, understanding BDR rules is crucial, as it could be a pathway to relief. This provision is rooted in the idea that borrowers should not be held accountable for debts incurred due to a school’s deceptive practices. To qualify, you must prove that your school misled you or violated state laws directly related to your enrollment or educational services.

The process begins with filing a BDR claim through the Federal Student Aid website. Your application must include detailed evidence of the school’s misconduct, such as false job placement rates, accreditation issues, or violations of state consumer protection laws. For example, if your school claimed a 90% employment rate for graduates but later investigations revealed it was closer to 30%, this could form the basis of a strong claim. Navient’s role as a loan servicer does not directly impact your eligibility, but the loan itself must be federally owned.

One critical aspect of BDR is its retrospective nature. It does not automatically forgive loans but instead evaluates each claim individually. Approval can lead to full or partial loan discharge, and in some cases, refunds for amounts already paid. However, the process can be lengthy, often taking months or even years. During this time, your loans may be placed in forbearance, temporarily pausing payments but accruing interest unless you qualify for a waiver.

A common misconception is that BDR applies to dissatisfaction with education quality. This is not the case. The misconduct must be specific, such as fraudulent advertising or illegal practices. For instance, a school falsely claiming accreditation for a program that never received it would qualify. Borrowers should gather all relevant documentation, including enrollment agreements, marketing materials, and correspondence with the school, to strengthen their case.

Finally, it’s essential to stay informed about policy changes. The Biden administration has expanded BDR approvals, particularly for borrowers who attended schools like Corinthian Colleges and ITT Tech. If your school has been the subject of widespread complaints or legal action, your chances of approval may be higher. Regularly check the Department of Education’s website for updates and consider consulting with a student loan attorney to navigate the complexities of your claim.

Bernie's Plan to Forgive Student Loans: A Comprehensive Guide

You may want to see also

Frequently asked questions

Navient student loan forgiveness refers to programs that may discharge or reduce Navient-serviced student loans. Eligibility depends on factors like loan type, repayment plan, employment, and participation in programs like Public Service Loan Forgiveness (PSLF) or Borrower Defense to Repayment.

A: No, Navient student loan forgiveness programs typically apply only to federal student loans serviced by Navient. Private loans are not eligible for federal forgiveness programs.

A: If you have federal Direct Loans serviced by Navient and work full-time for a qualifying public service employer, you may be eligible for PSLF after 120 qualifying payments. Navient is the servicer, but the program is administered by the federal government.

A: Borrower Defense to Repayment is a federal program that forgives loans if your school misled you. If Navient services your federal loans and you qualify, you can apply, but the decision is made by the U.S. Department of Education, not Navient.

A: Yes, if you enroll in an income-driven repayment (IDR) plan through Navient for your federal loans, you may qualify for loan forgiveness after 20–25 years of qualifying payments, depending on the plan.