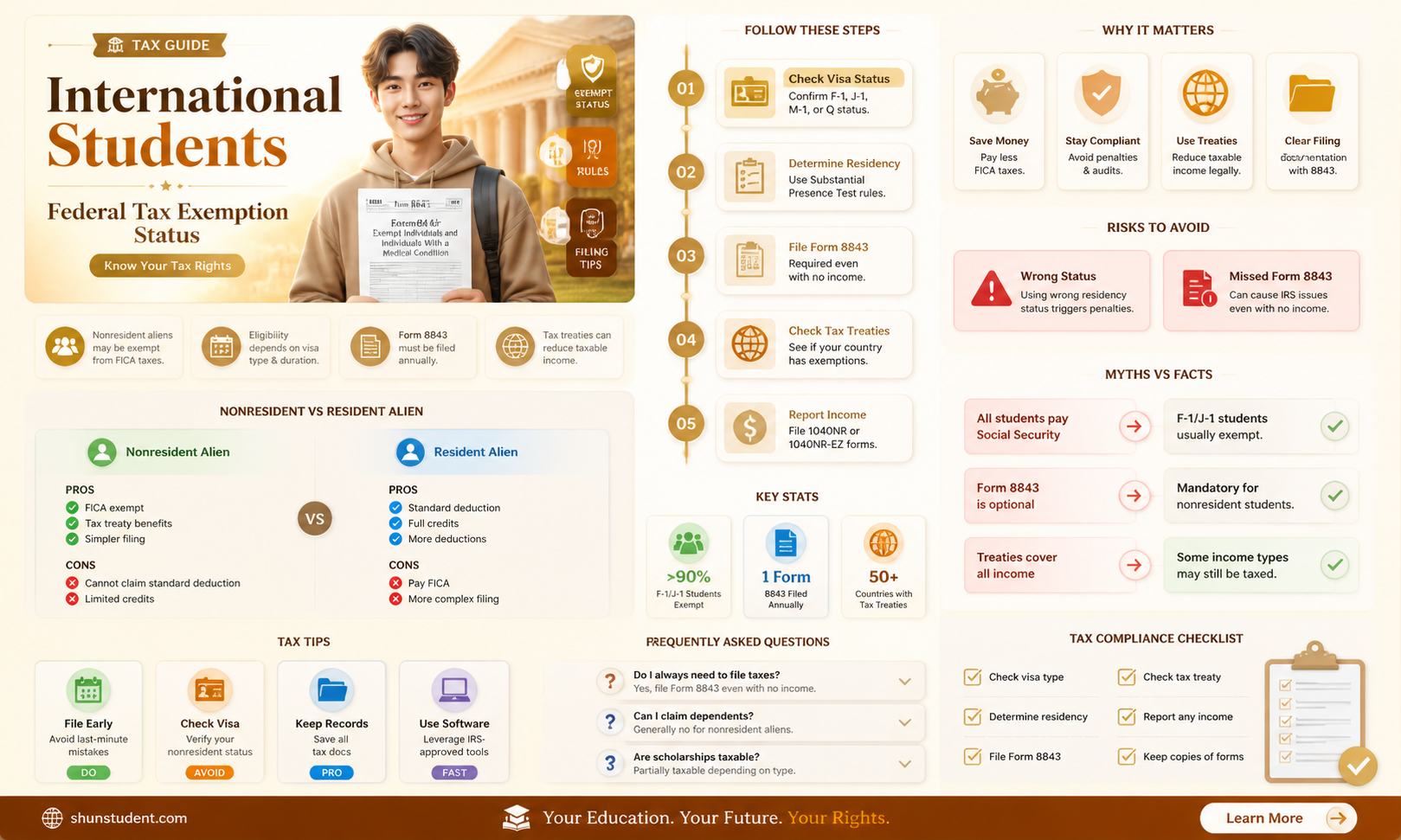

International students in the US are required to file a tax return, and most F-1 visa holders are considered nonresident aliens for tax purposes. However, some international students can be considered 'residents' or 'resident aliens' for tax filing purposes, depending on whether they pass the substantial presence test. While international students are generally exempt from Social Security and Medicare taxes, they may still be required to pay federal, state, and local taxes. The tax rates and deductions will differ for each state, and the amount paid will depend on the student's location and income.

Explore related products

What You'll Learn

![]()

International students on F-1 visas

It is important to note that F-1 students are exempt from the substantial presence test for the first five years they are in the US. This test is used to determine an individual's tax residency status. Even if an F-1 student passes this test within the first five years, they may still be considered a nonresident for tax purposes if they qualify for the Closer Connection Exception.

Furthermore, international students from countries with tax treaties with the US may be exempt from paying US income tax or may be taxed at a reduced rate. To claim this exemption, students must complete Form 8233 and a country-specific statement detailing the terms of the treaty. These forms must be submitted annually and reviewed by the IRS.

Overall, while international students on F-1 visas may be exempt from certain taxes, they are still required to comply with Federal tax filing requirements and may be liable for Federal and State taxes on any income earned in the US. It is recommended that international students on F-1 visas seek guidance from a tax professional or accountant to ensure they are fulfilling their tax obligations accurately.

International Students: File Your Tax Returns Promptly

You may want to see also

Explore related products

$45 $151

$32.62 $283.95

![]()

International students with US-based income

International students on F-1 visas are considered non-residents for tax purposes for the first five years they are in the US and are exempt from the Substantial Presence Test during this time. If they pass the Substantial Presence Test, they may still be considered non-residents if they qualify for the Closer Connection Exception.

International students must file Form 8843, even if they did not earn any income in the US. If they did earn income, they must also file Form 1040NR or 1040NR-EZ, depending on their residency status. Non-resident alien students must complete Form W-4 and may need to fill out additional forms if their country has a tax treaty with the US. These forms include Form 8233 and a country-specific statement, which must be submitted annually.

International students can apply for an Individual Taxpayer Identification Number (ITIN) if they are not eligible for a Social Security Number (SSN). They should consult with a tax professional or a certified public accountant (CPA) to ensure they are completing the correct forms and meeting their tax obligations.

Germany's Free Education: International Students' Dream

You may want to see also

Explore related products

![]()

International students and Social Security

International students on F-1 visas are generally considered nonresident aliens for tax purposes for the first five calendar years of their stay in the US. They are exempt from Social Security and Medicare taxes on wages paid to them for services performed within the United States during this period. However, they may still need to obtain a Social Security Number (SSN) for various reasons, including employment and non-wage income such as scholarships and grants.

Obtaining a Social Security Number as an International Student

To obtain an SSN, international students must typically provide proof of their age, identity, and work-authorized immigration status. Their record in the Student and Exchange Visitor Information System (SEVIS) must be in Active status for at least two days before applying. It is recommended that students wait at least ten days after arriving in the US before applying to allow their arrival information to update across government systems.

International students can apply for an SSN at any Social Security Card Center or local Social Security office. They may also need to submit a Social Security Letter Request and provide evidence of employment or employment authorization, depending on the type of employment. For instance, J-1 students must show evidence of employment and be in valid J-1 status, registered for a full course of study.

International Students and Taxes

While international students on F-1 visas are generally exempt from Social Security and Medicare taxes during their first five years in the US, they may still have tax obligations. They may need to file a federal tax return (Form 1040-NR) to assess their federal income and taxes, even if they didn't earn any money during their stay. Additionally, they may be required to file a state tax return and pay state income tax, depending on the state they reside in.

The Uncertain Future of International Students in America

You may want to see also

Explore related products

![The Administration of Gasoline Tax Refunds and Exemptions [microform]](https://m.media-amazon.com/images/I/61DrX+VgknL._AC_UY218_.jpg)

![]()

International students and state taxes

International students on F-1 visas are considered nonresident aliens for tax purposes for the first five calendar years of their stay in the US. After this period, they may be considered resident aliens for tax purposes, depending on their circumstances.

International students are liable for federal and state taxes, but not for Social Security (FICA) taxes, unless they are considered 'residents for tax purposes' by the IRS. This usually applies if they have lived in the US for five calendar years or more.

The US has income tax treaties with many different countries, and residents of these countries may be taxed at a reduced rate or be exempt from US income tax withholding on specific kinds of US-source income. Treaties vary among countries, and the type of income covered by the treaty. If the treaty does not cover a particular kind of income, or if there is no treaty between the US and the student's country, the student must pay tax on the income at the same rate as a US resident.

International students may need to file a state tax return, depending on the state they are in. They will need to send their tax return to the Department of the Treasury Internal Revenue Service in whichever state they are in. It is important to comply with the tax requirements, as missing the deadline may lead to fines and penalties, and could jeopardize future visa applications.

Canada Welcomes International Students: What's the Reality?

You may want to see also

Explore related products

![]()

International students and tax treaties

International students on F-1 visas are exempt from the substantial presence test for five years, and even if they pass the test, they may still be considered non-residents for tax purposes. The US has income tax treaties with several countries, and residents of these countries may be taxed at reduced rates or be exempt from US income tax withholding on certain types of US-source income. These treaties vary among countries.

If a student's country of residence has a tax treaty with the US, and the criteria in columns B and C are met, their wages qualify for a tax exemption, and they must complete Form 8233: Exemption from Withholding on Compensation for Independent (and Certain Dependent) Personal Services of a Nonresident Alien Individual. This form must be submitted to their university. If a student's country of residence does not have a tax treaty with the US, Form 8233 does not need to be completed.

To claim a tax treaty benefit on a non-compensatory scholarship or grant, a W-8BEN form must be completed. To fill out Form W-8BEN, you will need to provide your name, TIN, and address in your country of residence. Additionally, you must describe the services provided and the total amount of income earned, and provide details of your US visa type, including the date of your entry into the US and the date your current non-immigrant status expires.

Some examples of tax treaties include:

- Korean international students are exempt from tax on any grant, allowance, award, or income ($2,000 or less) from personal services performed.

- French citizens are not subject to US tax on any income earned from gifts from abroad for the purpose of maintenance, education, study, research, or training, as well as income ($5,000 or less) from personal services performed.

- Canadian citizens can be exempt for up to $10,000 in personal services (OPT, teaching, and research are considered personal services) if their total income is under or equal to $10,000.

- Chinese students with wages of $6,000 will only have $1,000 subject to federal taxation, as the tax treaty exempts up to $5,000.

International Students: Get Your TLSAE in Easy Steps

You may want to see also

Frequently asked questions

Most international students on F and J visas are considered nonresidents for tax purposes for their first five calendar years in the US. However, they may be considered 'residents' or 'resident aliens' for tax filing purposes.

International students are required to file a federal tax return. However, nonresident alien students are exempt from Social Security Tax and Medicare Tax on wages paid to them for services performed within the United States.

International students who did not earn any income in the US and only need to file Form 8843 do not need a Social Security Number (SSN) or Individual Taxpayer Identification Number (ITIN). If you received income from a US-based university, business, or individual, you will need to fill out Form 1040-NR or 1040NR-EZ.

The deadline to file taxes is usually April 15 (or the following Monday if it falls on a weekend).

Yes, if you are eligible for tax reduction, credit, or exemption under tax treaty regulations, you will need to fill out Form W8-BEN, Certificate of Foreign Status of Beneficial Owner for United States Tax Withholding and Reporting.