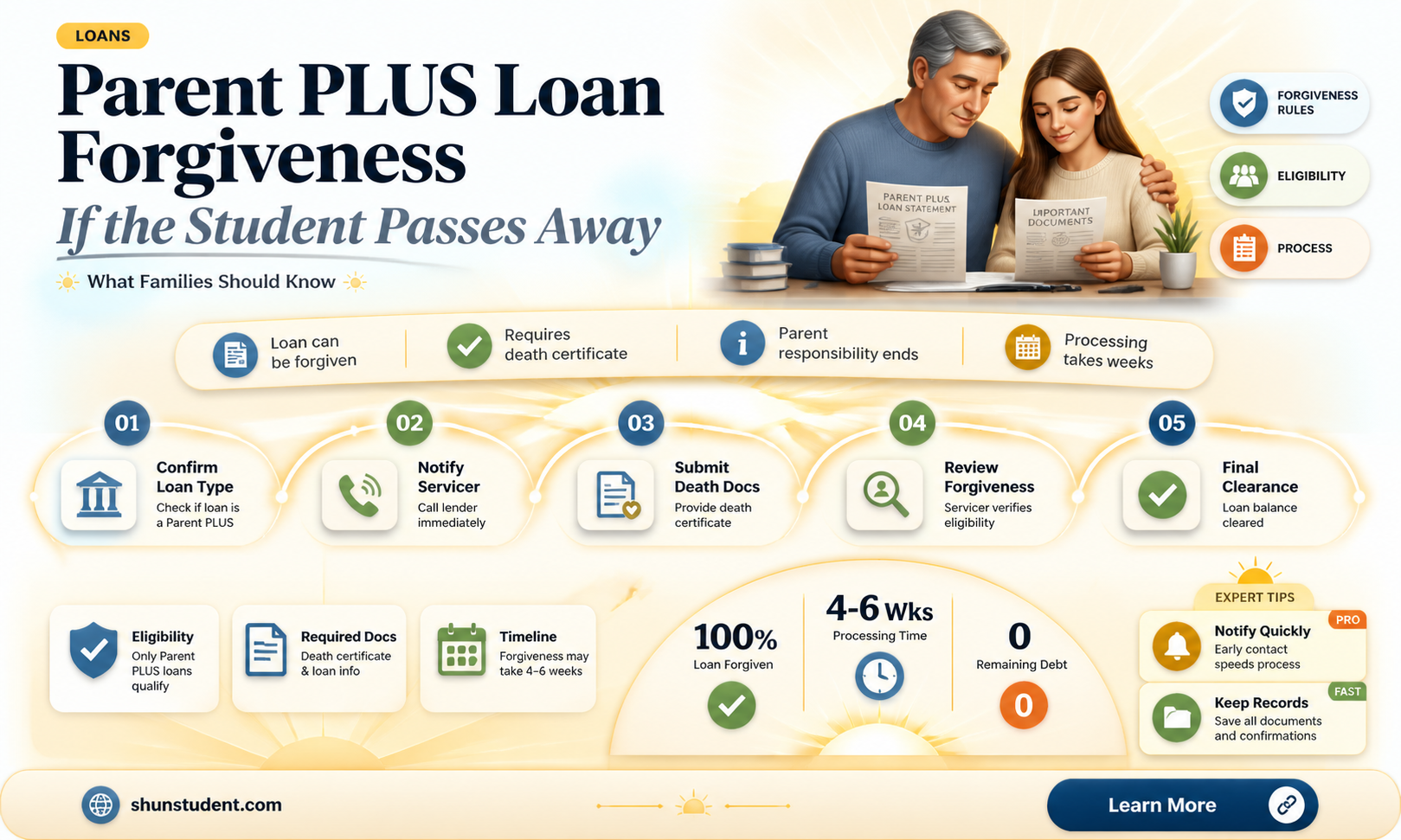

Parent PLUS loans are a federal student loan option that allows parents to borrow funds to cover their child’s educational expenses. A common concern among borrowers is whether these loans are forgiven in the event of the student’s death. According to federal guidelines, Parent PLUS loans are eligible for discharge if the student borrower passes away, relieving the parent borrower from the obligation to repay the debt. This provision ensures financial protection for families during a time of loss, though it’s important to note that the forgiveness applies specifically to the student’s death, not the parent borrower’s. Parents should familiarize themselves with the process for applying for loan discharge in such circumstances to ensure they receive the appropriate relief.

| Characteristics | Values |

|---|---|

| Loan Type | Parent PLUS Loans |

| Forgiveness Upon Student's Death | Yes, Parent PLUS Loans are discharged if the student borrower dies. |

| Documentation Required | Proof of the student's death (e.g., death certificate) must be submitted. |

| Impact on Parent Borrower | The parent borrower is no longer responsible for repaying the loan. |

| Tax Implications | As of recent updates, forgiven loans due to death are tax-free. |

| Effect on Credit Score | No negative impact on the parent borrower's credit score. |

| Application Process | Contact the loan servicer to initiate the discharge process. |

| Eligibility for Other Forgiveness Programs | Does not qualify for other forgiveness programs like PSLF or income-driven forgiveness. |

| Recent Policy Changes | Tax-free forgiveness was solidified under the Tax Cuts and Jobs Act of 2017. |

Explore related products

What You'll Learn

![]()

Parent PLUS Loan Discharge Criteria

Parent PLUS loans, a federal education financing option for parents of dependent undergraduate students, carry unique discharge criteria that differ significantly from those for student borrowers. One critical scenario where discharge may apply is the death of the student. According to federal regulations, if the student for whom the Parent PLUS loan was taken out passes away, the loan is eligible for discharge. This provision ensures that parents are not burdened with repayment obligations in the tragic event of their child’s death. The process requires documentation, such as a death certificate, to be submitted to the loan servicer, after which the remaining balance is forgiven without tax implications for the parent borrower.

While the death of the student triggers discharge, it’s essential to understand that the death of the parent borrower does not automatically discharge the loan. This distinction highlights the loan’s structure, where the parent, not the student, is the primary borrower. However, if the parent borrower passes away, the loan may be discharged if the student for whom the loan was taken out is no longer enrolled in school. This secondary criterion underscores the importance of understanding the loan’s terms and conditions to avoid confusion or unexpected financial liabilities.

Another lesser-known discharge criterion for Parent PLUS loans is total and permanent disability (TPD) of the parent borrower. Unlike student loans, which may also consider the student’s disability, Parent PLUS loans focus solely on the borrower’s condition. To qualify, the parent must provide documentation from a physician certifying the disability or submit proof of Social Security Disability Insurance (SSDI) benefits. This pathway offers relief for parents facing long-term health challenges that impede their ability to repay the loan.

Practical steps for pursuing Parent PLUS loan discharge include contacting the loan servicer immediately upon the occurrence of a qualifying event. For instance, in the case of a student’s death, parents should request the discharge application and submit the required documentation promptly. Delays can prolong the process and cause unnecessary stress. Additionally, parents should keep detailed records of all communications and submissions to ensure a smooth discharge process. Understanding these criteria and taking proactive steps can alleviate financial burdens during difficult times.

Comparatively, Parent PLUS loans offer fewer discharge options than traditional student loans, which may include pathways like borrower defense to repayment or public service loan forgiveness. This limitation emphasizes the need for parents to carefully consider the long-term implications of taking on such debt. For example, parents nearing retirement age should weigh the risks of carrying educational debt into their later years, as repayment obligations can impact retirement planning. Exploring alternatives, such as scholarships or work-study programs for the student, may reduce reliance on Parent PLUS loans and mitigate future financial risks.

In conclusion, Parent PLUS loan discharge criteria are narrowly defined but provide crucial relief in specific circumstances, such as the death of the student or the parent borrower’s disability. By familiarizing themselves with these provisions and taking timely action, parents can navigate the complexities of these loans more effectively. While the criteria are limited, understanding them ensures that borrowers can access available relief when needed, offering a measure of financial security during challenging times.

Understanding Student Loan Forgiveness Timeline for Income-Based Repayment Plans

You may want to see also

Explore related products

![]()

Documentation Required for Forgiveness

In the event of a student's death, parents seeking forgiveness of Parent PLUS loans must navigate a specific documentation process. This isn't a simple phone call or online form; it requires meticulous gathering and submission of proof. The U.S. Department of Education demands concrete evidence to verify the borrower's claim, ensuring the integrity of the loan discharge program.

Essential Documents:

The cornerstone of your application is a certified copy of the student's death certificate. This official document, issued by the relevant government agency, serves as irrefutable proof of the borrower's eligibility for loan forgiveness. Alongside this, you'll need to provide documentation confirming your relationship to the deceased student. This could be a birth certificate listing you as the parent or legal guardian, or other court-issued documents establishing guardianship.

Submission and Follow-Up:

Once you've assembled the necessary documents, submit them to the loan servicer handling your Parent PLUS loan. It's crucial to keep copies of everything you send for your records. Don't hesitate to follow up with the servicer to confirm receipt and inquire about the status of your forgiveness application. The process can take time, so patience is key.

Potential Hurdles and Tips:

While the documentation requirements seem straightforward, complications can arise. Ensure the death certificate is a certified copy, not a photocopy or online printout. If the student's name or other details on the certificate differ from those on the loan documents, be prepared to provide additional proof of identity. Contacting the loan servicer beforehand to clarify any potential issues can save time and frustration.

Navigating the documentation process for Parent PLUS loan forgiveness after a student's death can be emotionally taxing. By understanding the required documents, submitting them accurately, and being proactive in follow-up, you can streamline the process and secure the financial relief you're entitled to during this difficult time.

SCOTUS Decision on Student Loan Forgiveness: What’s at Stake?

You may want to see also

Explore related products

![]()

Impact on Parent’s Credit Score

The death of a student with a Parent PLUS loan triggers a discharge of the debt, but this process doesn’t automatically shield parents from credit score repercussions. Lenders report loan discharges to credit bureaus, and while the loan balance drops to zero, the notation "paid by death discharge" appears on the credit report. This entry, though not inherently negative, can confuse algorithms and potential creditors, who may misinterpret it as a delinquency or settlement. Parents should monitor their credit reports post-discharge to ensure accuracy and address any discrepancies promptly.

Analyzing the credit score impact reveals a nuanced scenario. Initially, the discharge removes a significant liability, which might improve a credit utilization ratio—a factor accounting for 30% of a FICO score. However, the "death discharge" notation lacks standardized treatment across scoring models. Some algorithms may flag it as a non-traditional payoff, potentially lowering the score by 10–20 points temporarily. Parents with otherwise pristine credit histories are less likely to experience severe drops, but those with marginal scores may face challenges in securing new credit immediately.

To mitigate risks, parents should proactively communicate with credit bureaus. Requesting a goodwill adjustment or providing documentation of the discharge can expedite the removal of any misleading notations. Additionally, maintaining low balances on existing accounts and avoiding new credit inquiries for six months post-discharge can stabilize the score. Tools like Credit Karma or annualcreditreport.com offer free monitoring to track changes and ensure accuracy.

Comparatively, Parent PLUS loan discharges differ from traditional debt forgiveness programs, which often carry explicit credit penalties. For instance, income-driven repayment forgiveness after 25 years may report as "settled for less than owed," severely damaging scores. In contrast, death discharges are more neutral but require vigilance. Parents should treat this event as a credit management opportunity, using it to reassess financial strategies and strengthen their profiles through disciplined spending and timely payments.

Practically, parents can take three steps to safeguard their credit: first, obtain a death certificate and notify the loan servicer immediately to initiate discharge. Second, request updated credit reports from all three bureaus 60 days post-discharge to verify accuracy. Third, if discrepancies arise, file disputes with evidence of the discharge. By acting swiftly and strategically, parents can minimize the credit score impact and maintain financial stability during a challenging time.

Can County Government Jobs Erase Your Student Loan Debt?

You may want to see also

Explore related products

![]()

Tax Implications of Loan Discharge

The discharge of a Parent PLUS loan due to a student's death can provide financial relief, but it also triggers tax implications that borrowers must navigate carefully. Under current IRS guidelines, discharged debt is generally considered taxable income unless it falls under specific exceptions. For Parent PLUS loans, the discharge upon the student’s death is treated as cancellation of debt, which may be taxable unless the borrower qualifies for insolvency or bankruptcy exclusions. This means the forgiven amount could increase the borrower’s taxable income for the year, potentially pushing them into a higher tax bracket or increasing their tax liability.

To mitigate this, borrowers should first assess their financial situation to determine if they qualify for insolvency relief. Insolvency occurs when the borrower’s total debts exceed their total assets. If this is the case, the forgiven debt may not be taxable. Borrowers must file IRS Form 982 to claim this exclusion, providing detailed calculations of their assets and liabilities. It’s crucial to consult a tax professional to ensure accurate reporting and avoid penalties. Additionally, staying informed about legislative changes is essential, as tax laws regarding debt forgiveness can evolve.

Another practical step is to plan for potential tax liabilities in advance. If insolvency doesn’t apply, borrowers should estimate the tax impact of the forgiven debt and set aside funds to cover the obligation. For example, if $50,000 in debt is discharged, and the borrower’s marginal tax rate is 24%, they could owe $12,000 in taxes. Proactive planning can prevent financial strain when tax season arrives. Borrowers can also explore payment plans with the IRS if immediate payment is unfeasible.

Comparatively, the tax treatment of Parent PLUS loan discharge differs from other loan forgiveness programs, such as Public Service Loan Forgiveness (PSLF), which is tax-free. This disparity highlights the importance of understanding the specific rules governing each type of loan discharge. While the emotional and financial relief of loan discharge upon a student’s death is significant, borrowers must remain vigilant about the tax consequences to avoid unexpected financial burdens.

In conclusion, while the discharge of a Parent PLUS loan due to a student’s death offers financial relief, it requires careful attention to tax implications. Borrowers should assess their eligibility for insolvency exclusions, plan for potential tax liabilities, and seek professional guidance to navigate this complex area. By taking these steps, they can manage the tax consequences effectively and focus on other important matters during a difficult time.

Nurse Loan Forgiveness: A Comprehensive Guide to Debt-Free Nursing

You may want to see also

![]()

Alternative Repayment Options for Parents

Parent PLUS loans, unlike federal student loans held by the student, do not offer automatic discharge upon the borrower's death. This leaves parents financially vulnerable if their child passes away before the loan is repaid. However, this doesn't mean parents are left without recourse. Several alternative repayment options exist, offering a lifeline to grieving families facing this unexpected burden.

Income-Contingent Repayment (ICR): This plan adjusts monthly payments based on the parent's income and family size. Payments are capped at 20% of discretionary income, making them more manageable for those facing financial hardship after a loss. While ICR doesn't forgive the debt, it can significantly reduce monthly obligations, providing breathing room during a difficult time.

Loan Consolidation: Consolidating multiple Parent PLUS loans into a Direct Consolidation Loan can simplify repayment and potentially lower monthly payments. This is especially beneficial if the parent has other federal student loans, as consolidation allows for access to income-driven repayment plans like ICR.

Loan Rehabilitation: If a parent has defaulted on their Parent PLUS loan, rehabilitation offers a path to regaining good standing. This involves making nine on-time, voluntary payments within ten months. While rehabilitation doesn't directly address the financial impact of a child's death, it can prevent further financial hardship by stopping collection efforts and wage garnishment.

Negotiation with the Servicer: While not guaranteed, some loan servicers may be willing to negotiate alternative repayment terms or even partial forgiveness in cases of extreme hardship. This requires proactive communication and documentation of the circumstances surrounding the student's death.

It's crucial for parents to explore these options promptly after their child's passing. Delaying action can lead to accruing interest, late fees, and potential default. By understanding these alternative repayment options, parents can navigate the financial aftermath of a devastating loss with greater clarity and potentially find a path towards financial stability.

Kamala Harris' Stance on Student Loan Forgiveness: What We Know

You may want to see also

Frequently asked questions

Yes, Parent PLUS loans are eligible for loan forgiveness if the student borrower passes away.

You will need to provide an original or certified copy of the student’s death certificate to the loan servicer.

No, the forgiveness of a Parent PLUS loan due to the student’s death does not negatively impact the parent’s credit score.

No, Parent PLUS loans are not forgiven if the parent borrower dies; forgiveness only applies if the student borrower passes away.

There is no specific time limit, but it’s recommended to contact the loan servicer as soon as possible to initiate the forgiveness process.