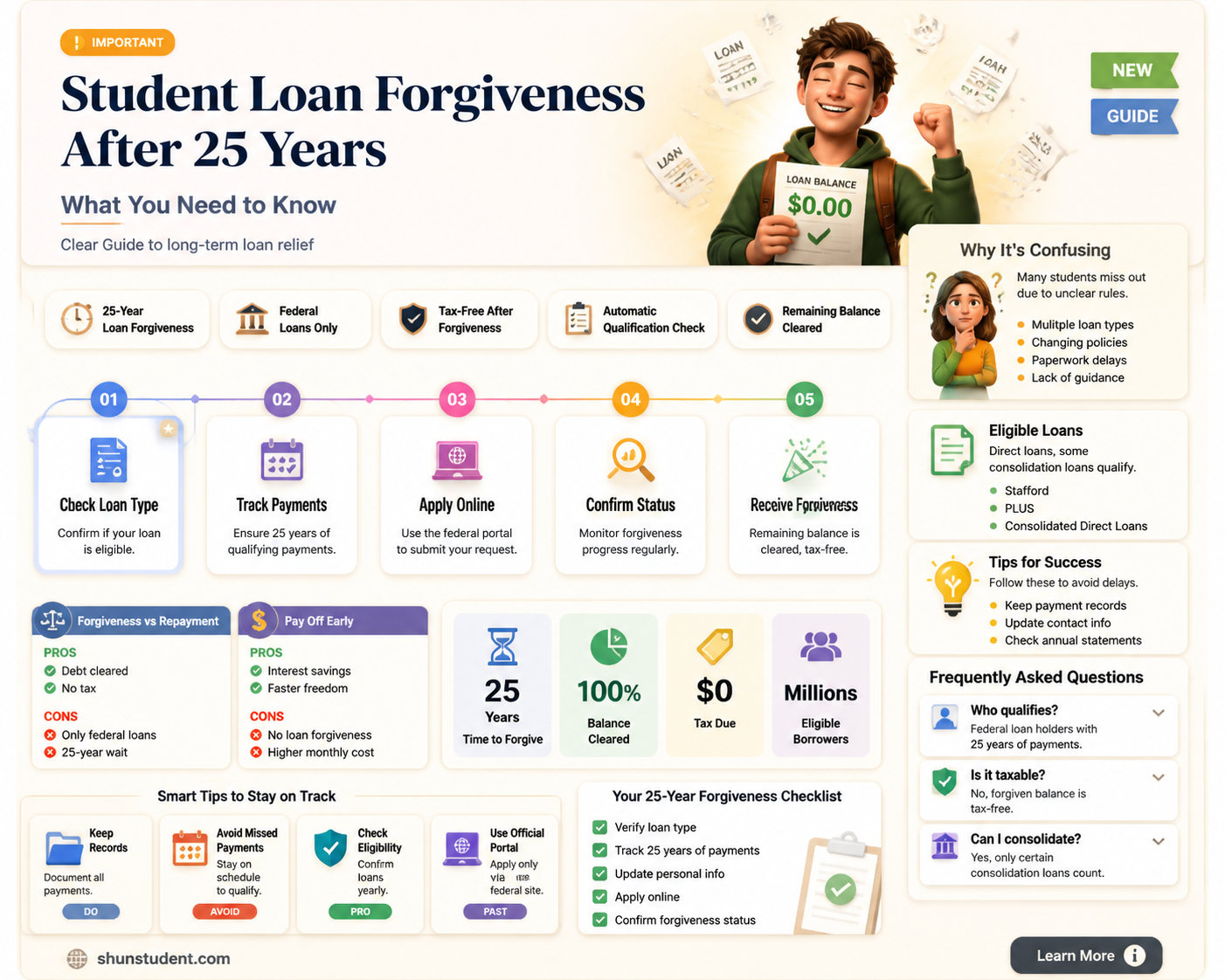

The question of whether student loans are forgiven after 25 years is a critical concern for many borrowers, particularly those enrolled in income-driven repayment (IDR) plans. Under these federal programs, such as Income-Based Repayment (IBR) or Pay As You Earn (PAYE), borrowers make payments based on their income and family size, with the remaining balance potentially eligible for forgiveness after 20 to 25 years of consistent payments. However, the specifics depend on the type of loan and repayment plan chosen. For instance, Public Service Loan Forgiveness (PSLF) offers forgiveness after 10 years for those working in qualifying public service jobs. Understanding the eligibility criteria, documentation requirements, and potential tax implications is essential for borrowers navigating this complex process.

| Characteristics | Values |

|---|---|

| Eligibility | Applies to federal student loans under income-driven repayment (IDR) plans. |

| Timeframe | 20-25 years, depending on the specific IDR plan and loan type. |

| Loan Types Covered | Direct Loans, FFEL Program loans (if consolidated into Direct Loans). |

| Non-Eligible Loans | Private student loans, Perkins Loans, and Parent PLUS Loans (unless consolidated). |

| Repayment Plans | Income-Based Repayment (IBR), Pay As You Earn (PAYE), Revised Pay As You Earn (REPAYE), Income-Contingent Repayment (ICR). |

| Tax Implications | Forgiven amount may be taxable as income (exceptions under the American Rescue Plan Act of 2021 until 2025). |

| Remaining Balance | Any remaining balance after 20-25 years is forgiven. |

| Payment Requirement | Must make qualifying payments for the entire 20-25 year period. |

| Public Service Loan Forgiveness (PSLF) | Separate program with 10-year forgiveness for public service workers. |

| Recent Updates | Temporary changes under IDR Account Adjustment (2023) may count past periods toward forgiveness. |

| Application Process | Automatic forgiveness upon meeting the 20-25 year requirement. |

| Impact on Credit Score | Forgiveness does not negatively impact credit score. |

Explore related products

What You'll Learn

- Income-Driven Repayment Plans: Explains how IDR plans can lead to loan forgiveness after 25 years of payments

- Public Service Loan Forgiveness: Details PSLF eligibility and its 10-year forgiveness vs. 25-year IDR

- Tax Implications: Discusses potential tax liabilities on forgiven amounts after 25 years

- Eligibility Requirements: Outlines criteria for qualifying for 25-year loan forgiveness under IDR plans

- Private vs. Federal Loans: Clarifies that only federal loans qualify for 25-year forgiveness

![]()

Income-Driven Repayment Plans: Explains how IDR plans can lead to loan forgiveness after 25 years of payments

For borrowers grappling with federal student loan debt, Income-Driven Repayment (IDR) plans offer a lifeline by capping monthly payments at a percentage of discretionary income. What many don’t realize is that these plans also provide a pathway to loan forgiveness after 25 years of qualifying payments. This isn’t a loophole—it’s a built-in feature designed to prevent lifelong debt servitude for those with modest incomes. However, the clock doesn’t start ticking automatically; borrowers must actively enroll in an IDR plan and maintain eligibility through annual recertification of their income and family size.

Consider this scenario: A recent graduate with $50,000 in federal loans and an annual income of $40,000 might qualify for payments as low as $150 per month under the Revised Pay As You Earn (REPAYE) plan. Over 25 years, they’d pay approximately $45,000—far less than the original principal plus interest. The remaining balance? Forgiven. But there’s a catch: the forgiven amount may be treated as taxable income, though current laws (like the American Rescue Plan Act) temporarily waive this tax liability through 2025. Borrowers should consult a tax professional to plan ahead.

Not all IDR plans are created equal. For instance, the Income-Based Repayment (IBR) plan forgives loans after 25 years, while the Pay As You Earn (PAYE) and REPAYE plans reduce the forgiveness timeline to 20 years for undergraduate loans. Public Service Loan Forgiveness (PSLF) offers forgiveness after 10 years for eligible borrowers, but it’s a separate program. The key is to choose the IDR plan that aligns with your income, loan type, and long-term goals. For example, if you expect your income to rise significantly, REPAYE might be less advantageous due to its higher payment cap compared to IBR.

To maximize the benefits of IDR plans, borrowers should stay organized. Recertify income and family size annually—missing this step can kick loans back into a standard repayment plan, halting progress toward forgiveness. Keep detailed records of payments, as administrative errors are common. Finally, monitor policy changes; the Biden administration has proposed reforms to streamline IDR forgiveness and reduce red tape. For now, IDR remains a viable strategy for those seeking relief from student debt, but it requires patience, diligence, and a clear understanding of the rules.

Do Students Embrace Grade Forgiveness in College? Insights and Opinions

You may want to see also

Explore related products

![]()

Public Service Loan Forgiveness: Details PSLF eligibility and its 10-year forgiveness vs. 25-year IDR

Student loan forgiveness after 25 years is a reality, but it’s not automatic or universal. The key lies in understanding Income-Driven Repayment (IDR) plans, which cap monthly payments based on income and family size. After 240 to 300 qualifying payments (20 to 25 years), the remaining balance is forgiven, though the forgiven amount may be taxed as income. However, for borrowers in public service, the Public Service Loan Forgiveness (PSLF) program offers a faster path to forgiveness in just 10 years. This raises the question: which option is better—10 years of PSLF or 25 years of IDR?

To qualify for PSLF, borrowers must work full-time for a qualifying employer, such as a government organization or nonprofit, and make 120 eligible payments under an IDR plan. Unlike IDR forgiveness, PSLF is tax-free, making it a more attractive option for those eligible. However, the requirements are strict: payments must be on time and in full, and employment certification is recommended annually to ensure compliance. For example, a teacher working in a low-income school district could have their loans forgiven after 10 years, saving potentially tens of thousands of dollars compared to waiting 25 years under IDR.

The choice between PSLF and IDR depends on career trajectory and financial goals. If you’re committed to a public service career, PSLF is the clear winner, offering faster forgiveness without tax penalties. However, if your career path is uncertain or you don’t qualify for PSLF, IDR provides a safety net, though it requires patience and long-term planning. For instance, a borrower earning $50,000 annually with $100,000 in loans might pay around $200 monthly under an IDR plan, but the remaining balance after 25 years could be substantial, especially if income grows over time.

Practical tips for maximizing forgiveness include consolidating FFEL or Perkins Loans into a Direct Consolidation Loan to qualify for PSLF, submitting the Employment Certification Form annually, and choosing the lowest-cost IDR plan (e.g., Revised Pay As You Earn, or REPAYE). Borrowers should also monitor their payment counts and ensure their employer qualifies for PSLF. While 25-year IDR forgiveness is a fallback, PSLF’s 10-year timeline and tax-free benefit make it the superior option for eligible borrowers. Ultimately, understanding these programs empowers borrowers to make informed decisions about their financial future.

Biden's Student Debt Forgiveness Plan: What You Need to Know

You may want to see also

Explore related products

![]()

Tax Implications: Discusses potential tax liabilities on forgiven amounts after 25 years

Forgiven student loan amounts after 25 years can trigger unexpected tax liabilities, turning what seems like a financial relief into a taxable event. Under current U.S. tax law, the IRS treats forgiven debt as taxable income unless it falls under specific exceptions. For borrowers on income-driven repayment plans, the remaining balance forgiven after 25 years of qualifying payments is generally considered taxable income in the year of forgiveness. This means you could face a substantial tax bill, depending on the forgiven amount and your tax bracket. For example, if $50,000 is forgiven and you’re in the 22% tax bracket, you could owe $11,000 in taxes.

However, there’s a critical exception to this rule: the Tax Cuts and Jobs Act (TCJA) of 2017 temporarily excludes forgiven student loan debt from taxable income for borrowers who receive forgiveness through 2025. This provision applies to both Public Service Loan Forgiveness (PSLF) and income-driven repayment plans. While this exclusion provides significant relief, it’s set to expire after 2025, leaving future borrowers uncertain about their tax obligations. If you’re planning to rely on 25-year forgiveness, monitor legislative updates to prepare for potential tax changes.

To mitigate tax liabilities, consider timing your income and deductions strategically in the year of forgiveness. For instance, if you anticipate a large forgiven amount, deferring income or maximizing deductions (e.g., charitable contributions or retirement account contributions) could lower your taxable income. Additionally, consult a tax professional to explore options like installment agreements with the IRS if the tax bill is unmanageable. Proactive planning can turn a daunting tax liability into a manageable financial event.

Comparatively, borrowers pursuing Public Service Loan Forgiveness (PSLF) after 10 years of qualifying payments benefit from tax-free forgiveness, making it a more tax-efficient option than 25-year forgiveness. If you’re eligible for PSLF, prioritizing this path could save you from future tax complications. However, if 25-year forgiveness is your only option, weigh the long-term benefits of debt elimination against the potential tax burden.

In conclusion, while 25-year student loan forgiveness offers a path to debt relief, it’s not without tax implications. Understanding the current tax landscape, planning ahead, and exploring alternative forgiveness programs can help you navigate this financial crossroads effectively. Stay informed, act strategically, and consult experts to minimize surprises come tax season.

Veterans and Student Loan Forgiveness: Exploring Options for Debt Relief

You may want to see also

Explore related products

![]()

Eligibility Requirements: Outlines criteria for qualifying for 25-year loan forgiveness under IDR plans

Qualifying for 25-year loan forgiveness under Income-Driven Repayment (IDR) plans isn’t automatic—it requires meeting specific eligibility criteria. First, your loans must be federal, as private loans are ineligible for this program. Direct Loans, Federal Family Education Loans (FFEL) Program loans, and Perkins Loans may qualify, but consolidation might be necessary to streamline eligibility. Second, you must enroll in an IDR plan, such as Income-Based Repayment (IBR), Pay As You Earn (PAYE), or Revised Pay As You Earn (REPAYE). These plans cap monthly payments at a percentage of your discretionary income, typically 10-20%, making them manageable for lower earners.

The clock on your 25-year forgiveness timeline starts ticking once you’ve made 300 qualifying payments under an IDR plan. These payments don’t need to be consecutive but must meet specific criteria: they must be on-time, full payments, and made while enrolled in an IDR plan. Partial or late payments don’t count, so consistency is key. Additionally, periods of deferment, forbearance, or economic hardship typically don’t qualify, though exceptions exist for certain types of forbearance, such as those related to military service or cancer treatment.

Income plays a critical role in eligibility, as IDR plans are designed for borrowers with lower earnings relative to their debt. Your annual income must fall below a threshold determined by your family size and the federal poverty guideline. For example, a single borrower earning less than $20,000 annually in a state with a poverty guideline of $13,590 would likely qualify for reduced payments. However, if your income increases significantly, your payments will adjust accordingly, potentially delaying forgiveness.

Finally, tax implications are a practical consideration. Any forgiven amount after 25 years is treated as taxable income, which could result in a substantial bill. Planning ahead by setting aside funds or exploring tax exemptions, such as the Public Service Loan Forgiveness (PSLF) program if applicable, can mitigate this financial burden. Understanding these eligibility requirements ensures you’re on track to maximize the benefits of 25-year loan forgiveness under IDR plans.

Do Government Employees Qualify for Student Loan Forgiveness?

You may want to see also

Explore related products

![]()

Private vs. Federal Loans: Clarifies that only federal loans qualify for 25-year forgiveness

The 25-year forgiveness clock is a lifeline for many borrowers, but it’s not a universal safety net. Only federal student loans qualify for this benefit, leaving private loan borrowers in a vastly different landscape. This distinction is critical, as private loans often carry higher interest rates and fewer repayment options, making long-term debt management significantly more challenging. Understanding this difference is the first step in strategizing your repayment plan effectively.

Private lenders operate under no obligation to offer forgiveness programs, and their terms are typically rigid. For instance, a borrower with $50,000 in private loans at 8% interest could end up paying over $90,000 over 25 years, with no guarantee of forgiveness. In contrast, federal loans under income-driven repayment plans cap monthly payments at a percentage of discretionary income, and any remaining balance after 25 years of consistent payments is forgiven. This federal benefit is a game-changer for low-income earners or those in public service roles.

To illustrate, consider two borrowers with identical $70,000 debts. Borrower A has federal loans and enrolls in an income-driven plan, paying 10% of their discretionary income monthly. After 25 years, the remaining $40,000 is forgiven. Borrower B, with private loans, pays the same amount monthly but accrues interest faster, ending up with a $65,000 balance after 25 years—with no forgiveness in sight. This example underscores the importance of loan type in long-term financial planning.

If you’re unsure whether your loans are federal or private, log into the National Student Loan Data System (NSLDS) for federal loans or check your credit report for private ones. For those with a mix of both, prioritize paying off private loans first while maintaining minimum payments on federal loans. Refinancing private loans to lower interest rates can also ease the burden, though it won’t provide forgiveness. Ultimately, knowing the rules of your loan type is key to avoiding decades of unnecessary debt.

Unlocking Student Loan Forgiveness for Radiologic Technologists: A Comprehensive Guide

You may want to see also

Frequently asked questions

No, only federal student loans under income-driven repayment (IDR) plans are eligible for forgiveness after 25 years of qualifying payments. Private loans and certain federal loans not on IDR plans do not qualify.

No, the 25 years (300 months) of payments do not need to be consecutive. However, each payment must qualify under an income-driven repayment plan.

It depends. Under current law, forgiven amounts under IDR plans are taxable as income, but the American Rescue Act of 2021 temporarily exempts forgiveness through 2025. Future tax laws may change.

Yes, you can switch between income-driven repayment plans, but only payments made under an IDR plan count toward the 25-year forgiveness timeline.

Yes, Parent PLUS loans can qualify for 25-year forgiveness if they are consolidated into a Direct Consolidation Loan and repaid under an income-driven plan.