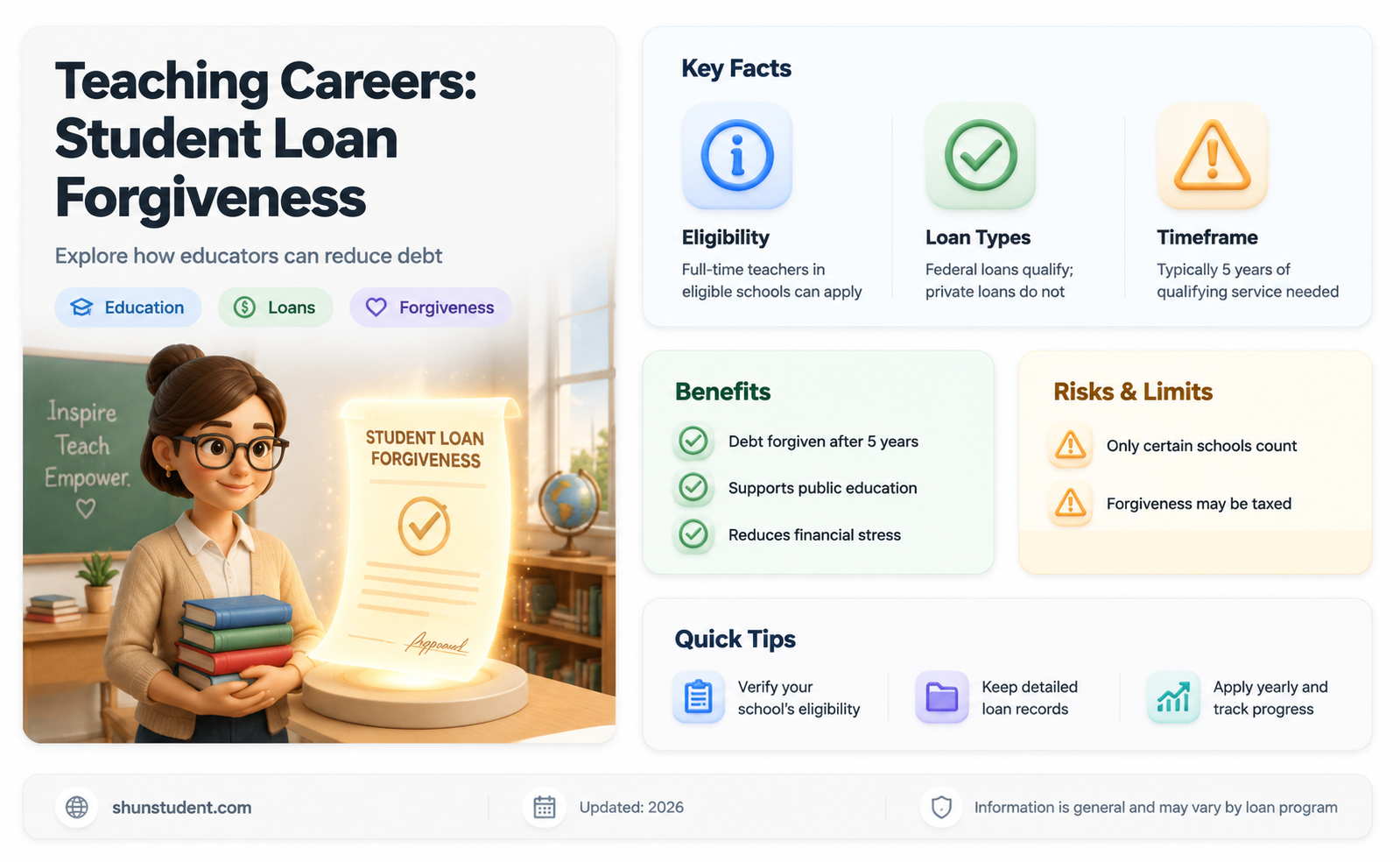

Many aspiring educators wonder if student loans can be forgiven if they pursue a career in teaching, and the answer is often yes, but with specific conditions. Programs like the Teacher Loan Forgiveness Program and Public Service Loan Forgiveness (PSLF) offer opportunities for teachers to have a portion of their federal student loans forgiven after meeting certain requirements, such as teaching full-time in low-income schools for a designated period. While these programs can significantly reduce financial burden, eligibility depends on factors like loan type, employment status, and the school’s designation. Understanding these programs and their criteria is essential for teachers seeking relief from student debt.

| Characteristics | Values |

|---|---|

| Loan Forgiveness Program | Teacher Loan Forgiveness (TLF) under the William D. Ford Federal Direct Loan Program |

| Eligibility Requirements | Must be a highly qualified teacher, work full-time for 5 consecutive academic years in a low-income school or educational service agency, and have Federal Direct Loans (Subsidized/Unsubsidized or Consolidation) |

| Forgiveness Amount | Up to $17,500 for secondary math/science, special education teachers; up to $5,000 for other eligible teachers |

| Loan Types Covered | Federal Direct Subsidized, Unsubsidized, and Consolidation Loans; does not apply to Perkins Loans, FFEL, or private loans |

| Application Process | Submit the Teacher Loan Forgiveness Application to the loan servicer after completing the 5-year teaching requirement |

| Additional Programs | Public Service Loan Forgiveness (PSLF) offers full forgiveness after 10 years of qualifying payments while working full-time for a government or nonprofit organization (including teaching roles) |

| State-Specific Programs | Some states offer additional loan forgiveness or repayment assistance for teachers (e.g., California's Assumption Program of Loans for Education (APLE)) |

| Tax Implications | Loan forgiveness under TLF is tax-free; PSLF forgiveness is also tax-free |

| Renewal/Recertification | No renewal required for TLF; PSLF requires annual recertification and final application after 120 qualifying payments |

| Impact on Credit Score | Forgiveness does not negatively impact credit score; loans are removed from the balance after forgiveness is granted |

| Latest Updates (as of 2023) | Temporary PSLF waiver expired Oct. 31, 2022; TLF criteria remain unchanged |

| Private Loan Eligibility | Private student loans are not eligible for federal forgiveness programs; teachers must explore state or employer-based programs |

| Part-Time Teaching | Part-time teaching does not qualify for TLF but may count toward PSLF if other criteria are met |

| School Eligibility | Schools must be listed in the Annual Directory of Designated Low-Income Schools for TLF eligibility |

Explore related products

What You'll Learn

![]()

Federal loan forgiveness programs for teachers

Teachers in the United States burdened by federal student loan debt have access to targeted forgiveness programs designed to incentivize service in high-need areas. The Teacher Loan Forgiveness Program offers up to $17,500 in forgiveness for direct or FFEL loans after five consecutive years of teaching full-time in a low-income school or educational service agency. Eligibility hinges on teaching math, science, special education, or serving as a reading specialist in a Title I school. For those with higher debt, the Public Service Loan Forgiveness (PSLF) program forgives the remaining balance of direct loans after 120 qualifying payments while employed full-time by a government or non-profit organization, including public schools.

Mastering Email: Essential Tips for Teaching Students Effective Communication

You may want to see also

Explore related products

![]()

State-specific teacher loan forgiveness options

In the realm of student loan forgiveness for teachers, state-specific programs often fly under the radar, yet they can be a lifeline for educators burdened by debt. Unlike federal programs, which have broad eligibility criteria, state initiatives are tailored to local needs, offering targeted relief to teachers in high-demand subjects or underserved areas. For instance, the Texas Teacher Loan Forgiveness Program provides up to $2,000 annually for full-time teachers in low-income schools, with a cap of $10,000 over five years. This example underscores how state programs can complement federal options, providing additional avenues for debt relief.

Consider the Mississippi Teacher Loan Repayment Program, which takes a unique approach by focusing on critical shortage areas like special education and secondary math. Eligible teachers can receive up to $3,000 annually for four years, totaling $12,000. To qualify, educators must commit to teaching in a designated shortage area for the entire period. This program not only alleviates financial stress but also strategically addresses staffing gaps in Mississippi’s education system. Such state-specific initiatives highlight the importance of researching local opportunities, as they often align with regional educational priorities.

For those in California, the California Teacher Loan Forgiveness Program offers a different model. Teachers working in low-income schools or subjects with teacher shortages, such as STEM or bilingual education, can receive up to $20,000 in loan forgiveness after five consecutive years of service. This program stands out for its higher forgiveness cap compared to many state initiatives, making it particularly attractive for long-term educators. However, applicants must navigate a competitive selection process, emphasizing the need to prepare a strong application that demonstrates commitment to the field.

While state programs offer promising opportunities, they come with caveats. Eligibility often hinges on teaching in specific subjects or geographic areas, and some require a multi-year commitment. For example, the Illinois Student Loan Repayment Program mandates that teachers work in a designated high-need district for at least four years to receive up to $5,000 annually. Prospective applicants should carefully review program requirements and consider how they align with their career goals. Additionally, combining state and federal programs, such as the Public Service Loan Forgiveness (PSLF) program, can maximize debt relief, but careful planning is essential to avoid overlapping eligibility issues.

In conclusion, state-specific teacher loan forgiveness programs are a valuable yet underutilized resource for educators seeking to manage student debt. By targeting local needs, these initiatives not only provide financial relief but also contribute to strengthening educational systems. Teachers should proactively explore programs in their state, assess eligibility criteria, and strategize how to combine state and federal options for optimal results. With thorough research and planning, these programs can turn the dream of debt-free teaching into a reality.

Can I, May I Use a Pencil? Student-Teacher Etiquette Explained

You may want to see also

Explore related products

![]()

Eligibility requirements for teacher loan forgiveness

Teachers seeking student loan forgiveness must navigate a complex web of eligibility requirements, each designed to ensure that relief is targeted to those serving in high-need areas or low-income schools. The Teacher Loan Forgiveness Program offers up to $17,500 in forgiveness for direct or FFEL loans after five consecutive years of full-time teaching in a low-income school or educational service agency. However, not all teaching positions qualify. Secondary school teachers in math, science, or special education are eligible for the maximum amount, while other teachers can receive up to $5,000. This distinction highlights the program’s emphasis on addressing critical teacher shortages in specific subjects and grade levels.

To qualify, teachers must meet stringent criteria, starting with the type of school they serve. The school must be listed in the Annual Directory of Designated Low-Income Schools for Teacher Cancellation Benefits, updated annually by the Department of Education. This directory ensures that forgiveness is directed to schools with a high percentage of students from low-income families, as determined by the number of students eligible for the National School Lunch Program. Teachers must also be *highly qualified*, a term defined by the No Child Left Behind Act, which requires state certification, a bachelor’s degree, and subject-matter competency. Failure to meet these standards can disqualify applicants, even if they teach in an eligible school.

The timeline for eligibility is equally critical. Teachers must complete five *consecutive* academic years, with no gaps in service exceeding one year. Part-time teaching or service in non-classroom roles does not count toward this requirement. Additionally, the loans being forgiven must have been disbursed before the end of the fifth year of qualifying teaching. For example, if a teacher’s fifth year of service ends in June 2024, any loans taken out after that date would not qualify for forgiveness under this program. This rule underscores the importance of strategic loan management for teachers pursuing forgiveness.

Beyond federal requirements, teachers should be aware of potential state-specific programs that may offer additional benefits. For instance, the Public Service Loan Forgiveness (PSLF) program can forgive remaining loan balances after 10 years of qualifying payments for teachers working in public schools or government organizations. While PSLF has broader eligibility, it requires a different application process and adherence to income-driven repayment plans. Teachers should also consider the *tax implications* of loan forgiveness, as some programs treat forgiven amounts as taxable income, though the Teacher Loan Forgiveness Program is currently tax-free.

In practice, teachers must meticulously document their eligibility. This includes maintaining records of employment, school eligibility, and loan disbursement dates. Submitting the Teacher Loan Forgiveness Application after completing the five-year requirement is the final step, but preparation begins on day one. By understanding these requirements and planning accordingly, teachers can maximize their chances of successfully obtaining loan forgiveness, easing the financial burden of their education while serving in high-need communities.

Effective Strategies for Teaching Fractions to Special Education Students

You may want to see also

Explore related products

![]()

Public vs. private school teaching impact

Teaching in public versus private schools can significantly alter your eligibility and strategy for student loan forgiveness, particularly under programs like the Public Service Loan Forgiveness (PSLF) or Teacher Loan Forgiveness (TLF). Public school teachers often have a clearer path to forgiveness due to the sector’s alignment with government-backed programs. For instance, PSLF requires 120 qualifying payments while working full-time for a government or non-profit employer—a criterion public schools automatically meet. In contrast, private school teachers face a steeper climb unless their institution is a 501(c)(3) non-profit, which is rare. Even then, private school teachers must meticulously document their employment status and payments to qualify for PSLF, as misclassification can derail forgiveness.

Consider the Teacher Loan Forgiveness program, which offers up to $17,500 in forgiveness for five consecutive years of teaching in a low-income public school. Private school teachers are ineligible unless their school serves low-income students under specific federal guidelines, a condition few private institutions meet. This disparity highlights how public school teaching not only broadens forgiveness opportunities but also simplifies the process. For example, a math teacher in a Title I public school in Texas could qualify for both TLF and PSLF simultaneously, maximizing debt relief. Private school teachers, however, often rely on income-driven repayment plans, which offer forgiveness after 20–25 years but result in taxable income on the forgiven amount.

To navigate these differences, private school teachers should prioritize verifying their employer’s non-profit status and consult the IRS’s EO Select Check tool. If ineligible for PSLF, focus on refinancing options or state-specific forgiveness programs, such as the Maryland’s Edward Byrne Memorial Justice Assistance Grant Program, which supports teachers in private schools serving at-risk students. Public school teachers, meanwhile, should ensure their loan type (Direct Loans) and repayment plan (income-driven) align with PSLF requirements. Both groups should track employment certification forms annually to avoid disqualifying errors.

The financial implications of these choices are profound. A public school teacher earning $50,000 annually with $60,000 in loans could see full forgiveness after 10 years under PSLF, while a private school counterpart might pay $40,000 over 20 years under an income-driven plan, plus taxes on $20,000 in forgiven debt. This underscores the need for private school teachers to weigh their passion for the role against long-term financial trade-offs. Public school teaching, despite lower average salaries, often yields greater net savings through forgiveness programs.

Ultimately, the decision between public and private school teaching should factor in not just loan forgiveness but also career fulfillment, school culture, and student demographics. For those prioritizing debt relief, public schools offer a more direct route, but private school teachers can still strategize with careful planning. Use tools like the PSLF Help Tool or consult a financial advisor to map your path. Remember, forgiveness programs reward commitment to underserved communities—whether in a public classroom or a qualifying private institution—so align your choice with both your values and your wallet.

Tailoring Instruction: Effective Strategies for Engaging Gifted Learners in Classrooms

You may want to see also

Explore related products

![]()

Loan forgiveness for special education teachers

Special education teachers play a critical role in shaping the lives of students with disabilities, yet they often face significant financial burdens from student loans. Fortunately, several loan forgiveness programs specifically target these educators, recognizing their invaluable contributions. The Teacher Loan Forgiveness Program offers up to $17,500 in forgiveness for special education teachers who work full-time for five consecutive years in a low-income school or educational service agency. To qualify, teachers must hold at least a bachelor’s degree and state certification. This program is particularly beneficial for those specializing in high-need areas like special education, where teacher shortages are common.

Beyond federal programs, state-specific initiatives often provide additional relief. For instance, the Texas Loan Repayment Program for Teachers offers up to $2,000 annually for special education teachers working in designated shortage areas. Similarly, California’s Teacher Loan Assumption Program provides up to $19,000 for educators in special education, contingent on a four-year commitment. These state programs complement federal options, creating a layered approach to debt relief. Special education teachers should research their state’s offerings to maximize benefits, as eligibility criteria and award amounts vary widely.

One of the most comprehensive options is the Public Service Loan Forgiveness (PSLF) program, which applies to special education teachers working in public schools or qualifying non-profit organizations. After making 120 eligible payments (approximately 10 years), the remaining loan balance is forgiven tax-free. To qualify, teachers must enroll in an income-driven repayment plan and submit employment certification forms annually. While PSLF requires a longer commitment, it offers complete forgiveness, making it ideal for long-term educators. Combining PSLF with the Teacher Loan Forgiveness Program can further accelerate debt relief.

Despite these opportunities, navigating loan forgiveness programs can be complex. Special education teachers should take proactive steps to ensure eligibility. First, verify that your employer qualifies under program guidelines—most public schools and many charter schools meet the criteria. Second, maintain meticulous records of employment and payments, as documentation is critical for approval. Finally, consult with a financial advisor or loan servicer to create a tailored strategy. By leveraging these programs strategically, special education teachers can alleviate financial stress and focus on what matters most: supporting their students.

Effective Strategies for Teaching Letter Sounds to Students with Language Delays

You may want to see also

Frequently asked questions

No, not all student loans are forgiven for teachers. Only specific federal student loans may qualify for forgiveness through programs like the Teacher Loan Forgiveness Program or Public Service Loan Forgiveness (PSLF).

Teachers may receive up to $17,500 in loan forgiveness through the Teacher Loan Forgiveness Program if they teach for five consecutive years in a low-income school. For PSLF, teachers can have their remaining balance forgiven after 10 years of qualifying payments.

Yes, for the Teacher Loan Forgiveness Program, you must teach full-time for five consecutive years in a low-income elementary or secondary school designated by the federal government.

No, private student loans do not qualify for federal loan forgiveness programs. Only federal Direct Loans are eligible for teacher loan forgiveness programs.

You must submit an application for the Teacher Loan Forgiveness Program after completing your five years of teaching. For PSLF, you must make 120 qualifying payments and submit a PSLF application after completing the program requirements.