International students in the US are required to file a tax return each year they are in the country, even if they do not have US-sourced income. This is a federal requirement, and some students may also need to file a state tax return. International students with F-1 visas are required to file tax returns even if they do not work during their studies. Students with M-1 visas do not pay taxes because they are in the US only to learn and do not earn income, while J-1 visa holders pay taxes like US citizens. International students who are nonresident aliens are exempt from Social Security and Medicare taxes on wages for services performed within the US.

| Characteristics | Values |

|---|---|

| Who needs to file taxes? | All international students and scholars in the US, even if they did not earn an income. |

| What forms do they need to fill? | Form 8843, Form 1040NR, Form 1040NR-EZ, Form 843, Form 8316, and state tax forms. |

| When is the deadline? | April 15 (or the following Monday if it falls on a weekend) |

| What if I paid too much tax? | You are eligible for a refund. |

| Are there any exemptions? | Students on M-1 visas do not pay taxes. F-1 visa holders pay federal and state income taxes, while J-1 visa holders pay taxes like US citizens. Students from countries with tax treaties with the US may be exempt or pay reduced rates. |

| What if I have taxable income from another country? | You must declare it on your US tax return. |

| What if I have income from an internship or CPT position? | You must declare this on your tax return. |

| Do I need an SSN or ITIN? | If you worked and received compensation, you need an SSN or ITIN. If you didn't receive any income, you don't need either. |

| What if I have a complicated tax situation? | Consult the IRS or a qualified tax accountant. |

| Are there any software tools to help? | Yes, Sprintax is a tax preparation software provided by some universities. |

| What are the consequences of not filing? | You may face problems with your visa or become ineligible for a green card. |

Explore related products

What You'll Learn

![]()

International students and tax treaties

International students in the USA are required to file a tax return. This is true even if they have no income to report, in which case they must file Form 8843. International students who did receive income must file Form 1040NR or 1040NR-EZ. If an international student worked in the USA and received taxable employment compensation, they must use a Social Security Number (SSN) or an Individual Taxpayer Identification Number (ITIN) on their tax forms.

Some countries have tax treaties with the USA, and international students from those countries may be exempt from some US taxes or have a reduced rate. For example, French citizens in the US for study, training, or research are exempt from US tax on income earned from gifts from abroad for the purpose of maintenance, education, study, research, or training. Similarly, Korean international students in the US for study, training, or research are exempt from tax on any grant, allowance, award, or income ($2,000 or less) from personal services performed. Canadian citizens can be exempt for up to $10,000 in personal services if their total income is under or equal to $10,000.

To claim a tax treaty benefit on a non-compensatory scholarship or grant, international students must fill out a W-8BEN form. To fill out Form W-8BEN, students will need to know their personal information, such as name, TIN, and address in their country of residence. They will also need to know the exact treaty on which they are basing their claim for tax exemption and details of their US visa type. To claim a tax treaty benefit on income from personal services, compensatory scholarships, or grants received, students will need to complete a Form 8233 and submit it to their university.

In addition to federal taxes, some international students must also pay state and/or local taxes. However, some countries have tax treaty agreements with the US in which certain types of income may be exempted from federal (but not state) taxes.

Working in Japan: Opportunities for International Students

You may want to see also

Explore related products

![]()

Social Security and Medicare taxes

International students on F-1, J-1, M-1, or Q-1 visas are usually exempt from Social Security and Medicare taxes (also known as FICA taxes) on wages paid to them for services performed in the United States, as long as they are non-residents for income tax purposes. This exemption typically applies for the first five calendar years of their physical presence in the country. After this period, international students are generally classified as residents for tax purposes and become subject to FICA tax withholding. However, if they remain enrolled as students for at least half-time, they may still be eligible for the FICA exemption.

To qualify for the exemption, the services performed by the non-resident international students must be allowed by the United States Citizenship and Immigration Services (USCIS) for their specific non-immigrant statuses. Additionally, such services must be performed to carry out the purposes for which their visas were issued. It is important to note that the exemption does not apply to off-campus employment or work for employers other than the school, college, or university where the student is enrolled.

International students on STEM OPT extensions are generally not subject to FICA taxes or Social Security and Medicare contributions during the first five calendar years of holding their F-1 nonimmigrant status. However, this exemption may not apply if the student has already accrued a substantial physical presence in the country before participating in STEM OPT.

In certain cases, international students may find themselves liable for Social Security and Medicare taxes. If an international student violates their non-immigrant status and earns self-employment income in the United States, their income will be subject to U.S. income tax and, if they become a resident alien, self-employment tax as well. Additionally, if an international student becomes a resident alien and meets certain criteria, they may be subject to Social Security and Medicare taxes on wages earned from employment within the United States.

Working in Russia: Opportunities for International Students

You may want to see also

Explore related products

![LLC Beginner's Guide [All-in-1]: Everything on How to Start, Run, and Grow Your First Company Without Prior Experience. Includes Essential Tax Hacks, Critical Legal Strategies, and Expert Insights](https://m.media-amazon.com/images/I/61SXdyvdqKL._AC_UY218_.jpg)

![]()

Tax forms for international students

International students in the US are required to file a tax return each year. The deadline for filing is usually April 15, or the following Monday if April 15 falls on a weekend.

The Internal Revenue Service (IRS) is the US government agency that collects taxes. The IRS website has dedicated information on tax information for foreign students and scholars.

Tax Forms

International students must file at least one tax form—Form 8843. This form must be mailed in a separate envelope for each dependent (including spouses and children of all ages) to the IRS. This form is not an income tax form, but it is required by the IRS for tax purposes.

If you have received income in the US, you will need to fill out additional tax forms. If you are considered a nonresident for tax purposes, you will need to use Form 1040NR. You can electronically file (or e-file) this form on the IRS website. If you are considered a resident for tax purposes, you will need to use Form 1040. You may also need to file a state tax return using Form 540NR.

Tax Identification Numbers

If you worked in the US and received taxable employment compensation, you will need a Social Security Number (SSN). If you are not eligible for an SSN, you must apply for an Individual Taxpayer Identification Number (ITIN) from the IRS to use on tax forms.

Tax Treaties

Some countries have a tax treaty with the US, and international students from those countries may be exempt from taxes or have a reduced rate.

Social Security and Medicare Taxes

In general, aliens performing services in the US as employees are liable for Social Security and Medicare taxes. However, certain classes of alien employees are exempt, including students. Under Section 3121(b)(10) of the Internal Revenue Code, students are exempt from Social Security and Medicare taxes on employment income if they are enrolled at least half-time and the employment is on-campus and incidental to their course of study.

Tax Preparation

Many people in the US use tax preparation software or pay a tax preparation company to prepare and file tax forms. There are also online resources with tax information for foreign students and scholars, such as Sprintax.

Passport Rules for International Students on Domestic Flights

You may want to see also

Explore related products

![[OLD VERSION] TurboTax Deluxe 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71UbHaUeeUL._AC_UL320_.jpg)

![]()

Tax filing status

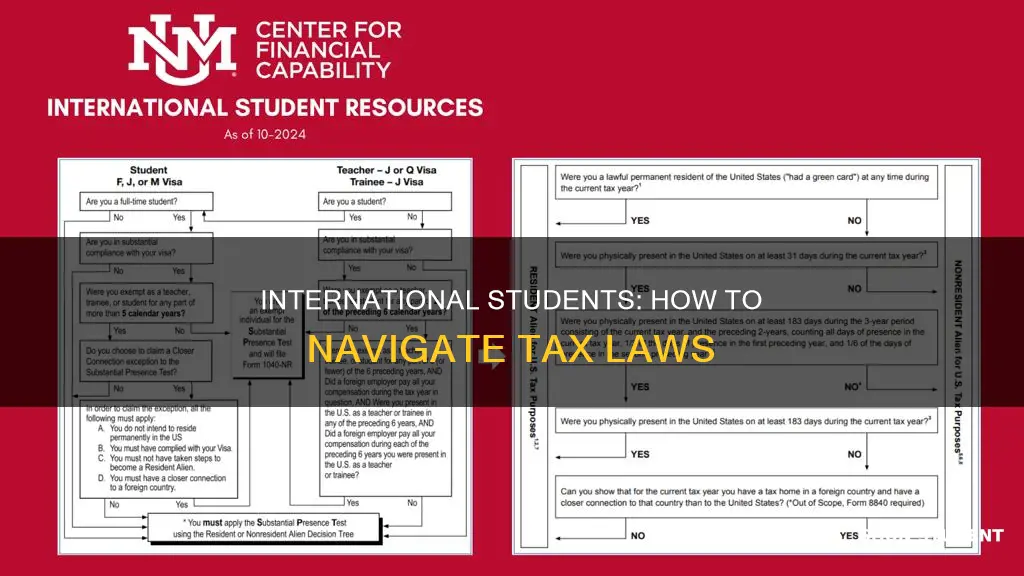

International students in the US on F-1 visas are generally considered nonresident aliens for tax purposes for the first five calendar years of their stay. However, some can be classified as 'residents' or 'resident aliens' for tax purposes, which does not equate to resident status for immigration or other purposes. This status change typically occurs after being present in the US for five calendar years.

As a nonresident alien, you will need to file Form 1040-NR (federal tax return) to assess your federal income and taxes. Even if you did not earn any money during your time in the US, you must file Form 8843 with the IRS by the deadline. Additionally, you may be required to file a state tax return, depending on the state.

If you are an F-1 visa holder and intend to reside in the US for longer than a year, you are subject to a 30% taxation rate on your capital gains during any tax year in which you are present in the US for 183 days or more. This rate may be reduced under a tax treaty.

F-1 students can file joint returns if their spouse is a US citizen or resident. If both F-1 visa holders are nonresidents for tax purposes, their filing status should be 'Married Filing Separate'.

To accurately determine your federal tax filing status, you can refer to the IRS website or Sprintax's blog. Sprintax will ask a series of questions based on the substantial presence test to determine your residence status for federal tax filing purposes.

It is important to note that your tax filing status may change over time, so reviewing the guidelines each time you complete your taxes is essential.

Bringing Spouses: International Students' Rights

You may want to see also

Explore related products

![[OLD VERSION] TurboTax Home & Business 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71b5aAzdXOL._AC_UL320_.jpg)

![H&R Block Tax Software Deluxe + State 2024 with Refund Bonus Offer (Amazon Exclusive) Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51+fonAXhPL._AC_UL320_.jpg)

![]()

Tax exemptions

International students in the USA are required to file a tax return. However, there are some exemptions from certain taxes for international students.

International students on F, J, M, or Q visas are considered "exempt individuals", meaning they are excused from the Substantial Presence Test for the first five years they are in the US. After this period, they will be subject to the Substantial Presence Test, which is used to determine if someone was in the US long enough to be considered a resident.

International students with F-1, J-1, or M-1 nonimmigrant status who have been in the US for more than five calendar years become resident aliens for US tax purposes if they meet the Substantial Presence Test. However, they may be exempt from FICA (Social Security and Medicare) taxes under the "student FICA exemption".

Section 3121(b)(10) of the Internal Revenue Code provides an exemption from FICA (Social Security and Medicare) taxes for all students, regardless of their US tax residency status. Under this exception, Social Security and Medicare taxes do not apply to services performed by students employed by a school, college, or university where the student is enrolled at least half-time. The student's on-campus employment must be incidental to and for the purpose of pursuing a course of study.

Nonresident aliens are generally liable for Social Security and Medicare taxes on wages for services performed in the US. However, foreign students temporarily present in the US on F-1, J-1, or M-1 visas for less than five calendar years are exempt from these taxes. To qualify for this exemption, the services performed must be allowed by USCIS for these nonimmigrant statuses, and such services must be performed to carry out the purposes for which such visas were issued.

Additionally, some countries have a tax treaty with the USA, and international students from those countries may be exempt from certain taxes or have a reduced rate. For example, J-1 visa holders pay taxes just like US citizens, while F-1 visa holders pay federal and state income taxes.

It is important to note that even if income is not taxable due to a tax treaty, it must still be reported on a US income tax return.

International Student Investing: Is It Possible?

You may want to see also

Frequently asked questions

Yes, international students in the US are required to file a federal tax return each year they are in the country, even if they did not earn any income.

If you worked in the US and received taxable employment compensation, you must apply for an SSN. If you are not eligible for an SSN, you must apply for an Individual Taxpayer Identification Number (ITIN) from the IRS.

Yes, there are some exceptions. Students on M-1 visas do not pay taxes because they are in the US solely to study and do not earn any income. Additionally, some countries have tax treaties with the US that may reduce or eliminate federal income taxes for their citizens.

![[OLD VERSION] TurboTax Premier 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71yj6wGqynL._AC_UL320_.jpg)

![H&R Block Tax Software Premium 2024 Win/Mac with Refund Bonus Offer (Amazon Exclusive) [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51tob7UDgCL._AC_UL320_.jpg)

![[OLD VERSION] TurboTax Business 2024 Tax Software, Federal Tax Return [PC Download]](https://m.media-amazon.com/images/I/71NKT0cDwnL._AC_UL320_.jpg)