The topic of student loan forgiveness has been a contentious issue in recent years, with many borrowers eagerly awaiting relief from their financial burdens. However, the question of whether student loan forgiveness can be overturned has emerged as a critical concern, particularly in light of ongoing legal challenges and political debates. As the federal government considers various proposals to alleviate the student debt crisis, opponents argue that such measures could be subject to reversal, leaving borrowers in a state of uncertainty. This uncertainty stems from potential legal challenges, changes in administration, or shifts in legislative priorities, all of which could jeopardize the long-term viability of student loan forgiveness programs. As a result, understanding the potential for overturning student loan forgiveness is essential for borrowers, policymakers, and advocates alike, as it underscores the need for robust, durable solutions to address the growing student debt burden.

| Characteristics | Values |

|---|---|

| Legal Challenges | Student loan forgiveness programs can be challenged in court, particularly if they are deemed unconstitutional or exceed executive authority. |

| Congressional Action | Congress can pass legislation to overturn or modify student loan forgiveness programs. |

| Executive Order Limitations | Forgiveness through executive orders can be reversed by future administrations. |

| Judicial Review | Courts can rule on the legality of forgiveness programs, potentially overturning them if found unlawful. |

| Political Climate | Changes in political leadership can lead to shifts in policy, potentially reversing forgiveness programs. |

| Program Design | Forgiveness programs with clear statutory authority are less likely to be overturned. |

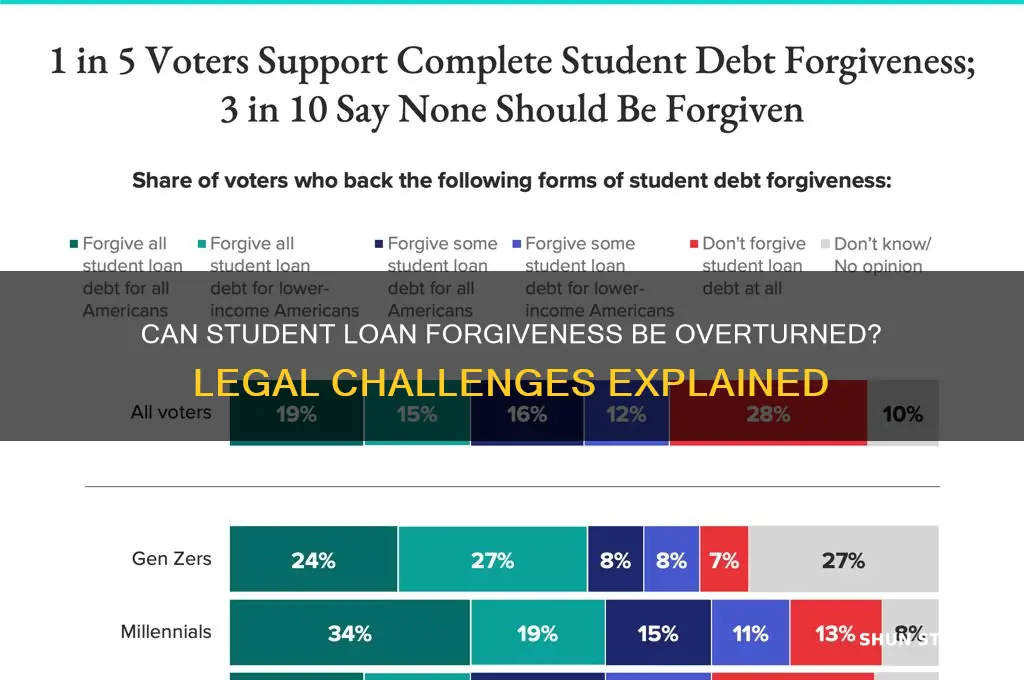

| Public Opinion | Strong public opposition or support can influence the likelihood of a program being overturned. |

| Economic Impact | Economic factors may influence decisions to maintain or overturn forgiveness programs. |

| Legal Precedents | Past court rulings on similar programs can set precedents affecting current forgiveness initiatives. |

| Implementation Status | Programs already implemented and benefiting borrowers are harder to overturn than those in planning stages. |

Explore related products

What You'll Learn

![]()

Legal Challenges to Loan Forgiveness

Legal challenges to student loan forgiveness have emerged as a significant obstacle to widespread debt relief, particularly in the United States. One of the most prominent examples is the legal battle surrounding the Biden administration’s 2022 student loan forgiveness plan, which aimed to cancel up to $20,000 in debt for eligible borrowers. This initiative was swiftly challenged in court by several Republican-led states and conservative groups, who argued that the administration overstepped its authority under the Higher Education Relief Opportunities for Students (HEROES) Act. The Supreme Court’s eventual ruling in *Biden v. Nebraska* (2023) struck down the plan, citing a lack of clear congressional authorization for such broad debt cancellation. This case underscores how legal challenges can effectively halt or overturn loan forgiveness efforts, even when they are designed to address systemic financial burdens.

To understand the mechanics of these challenges, consider the legal arguments typically employed. Opponents often claim that loan forgiveness programs violate the Administrative Procedure Act (APA) by bypassing required notice-and-comment rulemaking processes. They also argue that such programs exceed the executive branch’s authority, infringing on Congress’s constitutional power to control spending. For instance, in the *Biden v. Nebraska* case, the Court ruled 6-3 that the HEROES Act did not grant the Department of Education the authority to cancel student debt on such a massive scale. This decision highlights the importance of legislative clarity in crafting loan forgiveness programs that can withstand judicial scrutiny. Borrowers and advocates must therefore push for explicit congressional action to ensure the legality of future relief efforts.

Another critical aspect of legal challenges is their strategic timing and funding. Conservative legal organizations, such as the Job Creators Network Foundation, have been instrumental in filing lawsuits against loan forgiveness programs. These groups often receive backing from wealthy donors and corporations with a vested interest in maintaining the status quo. For example, the lawsuit in *Biden v. Nebraska* was funded by a coalition of plaintiffs who argued that debt cancellation would harm taxpayers and private loan servicers. Borrowers and advocates must be aware of these tactics and prepare counterarguments that emphasize the public interest in alleviating student debt, such as its economic benefits and the moral imperative to address educational inequities.

Practical steps can be taken to mitigate the impact of legal challenges on loan forgiveness. First, policymakers should draft legislation with explicit language granting the executive branch authority to implement debt relief programs. Second, borrowers should stay informed about ongoing legal battles and participate in advocacy efforts to support forgiveness initiatives. Third, alternative relief measures, such as income-driven repayment plans or targeted forgiveness for public service workers, may be less vulnerable to legal challenges due to their narrower scope. By adopting a multi-pronged strategy, stakeholders can increase the likelihood of successful loan forgiveness while navigating the complex legal landscape.

In conclusion, legal challenges to student loan forgiveness are a formidable barrier, but they are not insurmountable. The *Biden v. Nebraska* case serves as a cautionary tale about the limits of executive action and the need for robust legislative support. Borrowers, advocates, and policymakers must work together to craft legally sound programs, anticipate opposition tactics, and build public support for debt relief. Only through strategic planning and persistence can the goal of widespread student loan forgiveness be achieved in the face of ongoing legal obstacles.

Sanford Brown Closure: Steps to Qualify for Student Loan Forgiveness

You may want to see also

Explore related products

![]()

Congressional Authority Over Forgiveness Programs

The authority to overturn or modify student loan forgiveness programs ultimately rests with Congress, as it holds the power of the purse and legislative oversight. While the executive branch, particularly the Department of Education, administers these programs, their existence and scope are rooted in statutory law. This means that any significant changes, including the overturning of forgiveness initiatives, would require congressional action. For instance, the Higher Education Act of 1965, which governs federal student aid programs, grants Congress the ability to amend or repeal provisions related to loan forgiveness. Thus, understanding congressional authority is crucial for predicting the fate of such programs.

Consider the process by which Congress could overturn a forgiveness program. First, a bill must be introduced in either the House or Senate, proposing to amend or repeal the relevant section of law. This bill would then need to navigate the committee system, where it could face scrutiny or modification. If it advances, it would require a majority vote in both chambers. However, the process doesn’t end there. The bill would need to be signed into law by the President, or Congress would need to override a presidential veto with a two-thirds majority in both houses. This multi-step process highlights the deliberate nature of congressional action and the checks and balances inherent in the system.

A key factor in congressional decision-making is political will, which often hinges on public opinion and economic conditions. For example, during periods of economic hardship, there may be greater support for maintaining or expanding forgiveness programs to alleviate financial strain on borrowers. Conversely, in times of fiscal austerity, there could be pressure to reduce government spending by curtailing such initiatives. Historical examples, such as the 2007 Public Service Loan Forgiveness Program, illustrate how congressional priorities can shape the longevity and effectiveness of these programs. Advocates and opponents alike must therefore engage in strategic lobbying and public outreach to influence legislative outcomes.

Practical implications of congressional authority extend to borrowers and institutions alike. For individuals, uncertainty about the future of forgiveness programs can affect financial planning and career choices, particularly in sectors like public service or education that often rely on such incentives. Institutions, including universities and employers, may also adjust their policies in response to perceived risks of program overturn. For instance, some employers might reconsider offering student loan repayment benefits if federal programs appear unstable. Borrowers can mitigate risk by staying informed about legislative developments and exploring alternative repayment options, such as income-driven plans, which are less susceptible to abrupt changes.

In conclusion, while the executive branch plays a significant role in implementing student loan forgiveness programs, Congress holds the ultimate authority to overturn or modify them. This power is exercised through a structured legislative process that reflects broader political and economic considerations. For stakeholders, understanding this dynamic is essential for navigating the complexities of student loan policy. By staying informed and proactive, borrowers and advocates can better position themselves to respond to potential changes in the landscape of loan forgiveness.

Buying a House? Here’s How to Get Student Loans Forgiven

You may want to see also

Explore related products

![]()

Supreme Court Precedents and Impact

The Supreme Court's role in shaping student loan forgiveness policies is pivotal, as its precedents can either solidify or dismantle executive actions. In *Biden v. Nebraska* (2023), the Court struck down the Biden administration’s $400 billion student loan forgiveness plan, citing the Higher Education Relief Opportunities for Students (HEROES) Act as an insufficient basis for such broad debt cancellation. This decision hinged on the "major questions doctrine," which requires explicit congressional authorization for actions of significant economic or political consequence. The ruling underscores the Court’s willingness to limit executive power in areas traditionally governed by legislative action, setting a precedent that future forgiveness initiatives must navigate.

Analyzing the Court’s reasoning reveals a cautious approach to executive overreach. The majority opinion emphasized that the HEROES Act, designed to provide targeted relief during national emergencies, did not grant the Department of Education authority to waive trillions in debt. This interpretation narrows the scope of what agencies can achieve without explicit congressional approval, effectively raising the bar for future student loan forgiveness efforts. Advocates for debt cancellation must now focus on legislative solutions, as judicial precedent suggests executive actions alone are insufficient.

Practically, this precedent impacts borrowers by delaying relief and shifting the battleground to Congress. For instance, borrowers with federal loans under the Public Service Loan Forgiveness (PSLF) program remain unaffected, as this initiative is rooted in existing legislation. However, broader forgiveness plans, like those proposed during the pandemic, face significant legal hurdles. Borrowers should monitor legislative developments, such as the proposed *Student Loan Forgiveness for Public Servants Act*, which seeks to codify forgiveness into law, thereby bypassing judicial challenges.

Comparatively, the Court’s stance contrasts with its treatment of other executive actions, such as immigration policies under *DACA*. While *DACA* survived legal challenges due to its narrower scope and reliance on prosecutorial discretion, student loan forgiveness was deemed too expansive. This distinction highlights the Court’s sensitivity to the scale and economic impact of executive actions. Policymakers and advocates must therefore craft initiatives that align with existing statutes and avoid triggering the "major questions doctrine."

In conclusion, the Supreme Court’s precedents on student loan forgiveness prioritize legislative authority over executive action, creating a roadmap for future challenges. Borrowers and advocates must pivot toward legislative solutions, while policymakers should ensure proposals are grounded in clear statutory authority. The Court’s rulings serve as both a cautionary tale and a guide, shaping the contours of what is legally achievable in addressing the student debt crisis.

Can Signature Student Loans Be Forgiven? Exploring Options for Relief

You may want to see also

Explore related products

![]()

Administrative Procedure Act Compliance

The Administrative Procedure Act (APA) serves as a critical framework for ensuring federal agencies follow transparent and fair processes when creating or modifying regulations. When considering whether student loan forgiveness can be overturned, APA compliance becomes a pivotal factor. Any attempt to reverse such policies must adhere to the APA’s requirements, including notice-and-comment rulemaking, which mandates public input and a reasoned explanation for the agency’s decision. Failure to comply can render the action arbitrary and capricious, opening it to legal challenges.

To overturn student loan forgiveness, an agency would need to initiate a new rulemaking process under the APA. This involves publishing a proposed rule in the Federal Register, providing a minimum 30-day comment period, and carefully considering public feedback before issuing a final rule. For example, if the Department of Education sought to rescind forgiveness, it would need to justify the reversal with data, legal authority, and a clear rationale. Omitting these steps could lead to court intervention, as seen in cases like *Department of Homeland Security v. Regents of the University of California*, where the Supreme Court emphasized the importance of reasoned decision-making.

A key challenge in APA compliance is the "arbitrary and capricious" standard, which courts use to review agency actions. If an agency fails to provide a satisfactory explanation for reversing a policy—such as student loan forgiveness—courts may invalidate the decision. For instance, abruptly rescinding forgiveness without addressing reliance interests or providing a coherent justification could violate this standard. Agencies must also avoid procedural shortcuts, such as using interim final rules without a compelling reason, as this can undermine public trust and legal validity.

Practical tips for ensuring APA compliance in this context include conducting a thorough cost-benefit analysis, documenting the rationale for policy changes, and engaging stakeholders early in the process. Agencies should also be mindful of timing; rushing the rulemaking process increases the risk of errors and legal vulnerabilities. For borrowers, understanding the APA’s role in policy reversals can empower them to participate in the comment process and challenge non-compliant actions through litigation. Ultimately, strict adherence to the APA is not just a legal requirement but a safeguard against arbitrary governance.

Biden's Student Loan Forgiveness: Step-by-Step Application Guide

You may want to see also

Explore related products

![]()

Political and Legislative Reversal Risks

Student loan forgiveness programs, while offering relief to millions, are inherently vulnerable to political and legislative reversals. This fragility stems from their reliance on executive actions, congressional legislation, or regulatory changes, all of which can shift dramatically with changes in administration or party control. For instance, the Biden administration’s 2022 student loan forgiveness plan, which aimed to cancel up to $20,000 in debt for eligible borrowers, was immediately challenged in court and ultimately struck down by the Supreme Court in 2023. This example underscores how even well-intentioned policies can be overturned when they lack bipartisan support or a solid legal foundation.

To mitigate reversal risks, policymakers must prioritize legislative permanence over temporary fixes. Executive actions, such as those taken under the Higher Education Act’s authority, are particularly susceptible to reversal because they depend on the discretion of the sitting president. In contrast, laws passed by Congress carry more weight and are less likely to be overturned without a significant shift in political consensus. For example, the Public Service Loan Forgiveness (PSLF) program, established by Congress in 2007, has endured multiple administrations because it is enshrined in statute. Advocates for student loan forgiveness should push for similar legislative solutions rather than relying on executive orders or regulatory changes.

Another critical factor is the role of judicial interpretation in determining the fate of forgiveness programs. Courts, particularly the Supreme Court, have become increasingly influential in deciding the legality of executive actions. In the case of *Biden v. Nebraska* (2023), the Court ruled that the administration overstepped its authority under the HEROES Act, effectively invalidating the forgiveness plan. This highlights the importance of crafting policies with a clear legal basis and anticipating potential legal challenges. Policymakers should consult legal experts early in the process to ensure their actions are defensible in court.

Public opinion and political mobilization also play a pivotal role in safeguarding forgiveness programs. Policies that enjoy broad public support are less likely to be targeted for reversal, as politicians risk backlash from constituents. For instance, the widespread outcry following the Supreme Court’s decision to block Biden’s forgiveness plan demonstrated the strength of public sentiment on this issue. Advocacy groups and borrowers must continue to mobilize, using grassroots campaigns, social media, and lobbying efforts to maintain pressure on lawmakers. Practical steps include organizing town halls, contacting representatives, and sharing personal stories to humanize the impact of student debt.

Finally, policymakers should consider incremental approaches to forgiveness rather than sweeping, one-time initiatives. Smaller, targeted programs—such as expanding income-driven repayment plans or forgiving debt for specific professions—may face less opposition and are easier to defend legally. For example, the PSLF program, which forgives debt for public servants after 10 years of payments, has been more resilient than broader forgiveness proposals. By focusing on incremental changes, advocates can build a foundation of support that is harder to dismantle, even in the face of political shifts.

Budget Cuts Threaten Student Loan Forgiveness: What Borrowers Need to Know

You may want to see also

Frequently asked questions

Yes, student loan forgiveness implemented through executive action or regulations could be overturned by a future administration or Congress, as it is not permanently codified into law.

Yes, student loan forgiveness programs, especially those implemented through executive action, can be challenged in court and potentially overturned if found to exceed legal authority or violate constitutional principles.

Once student loan forgiveness is granted and processed, it is unlikely to be revoked unless there is evidence of fraud or a legal challenge invalidates the entire program.

Yes, Congress has the authority to pass legislation that could overturn or limit student loan forgiveness, even if it has already been granted, though such action would face political and legal challenges.