The question of whether the president can forgive student loans has become a central issue in American political and economic discourse, particularly as student debt continues to burden millions of Americans. Advocates argue that executive action to cancel student loans could provide significant financial relief, stimulate the economy, and address systemic inequalities in education financing. Critics, however, contend that such a move could be legally questionable, fiscally irresponsible, and unfair to those who have already paid off their debts. The debate hinges on interpretations of the Higher Education Act and the president’s authority under existing laws, with potential implications for both individual borrowers and the broader financial landscape. As policymakers, legal experts, and the public weigh in, the issue remains a contentious and pivotal aspect of the national conversation on education and economic opportunity.

| Characteristics | Values |

|---|---|

| Legal Authority | The President's authority to forgive student loans is limited. Under the Higher Education Act, the Secretary of Education has the power to "compromise, waive, or release" student loans, but this is typically done on a case-by-case basis for specific circumstances (e.g., death, disability, school closure). |

| Executive Action | The President can issue executive orders or direct the Department of Education to implement loan forgiveness programs. However, broad-scale forgiveness without congressional approval is legally contentious and has faced legal challenges. |

| Existing Programs | The President can expand existing programs like Public Service Loan Forgiveness (PSLF), income-driven repayment (IDR) plans, or temporary relief measures (e.g., COVID-19 payment pauses). |

| Congressional Role | Large-scale student loan forgiveness typically requires congressional legislation. The President cannot unilaterally forgive all student loans without legal or legislative backing. |

| Recent Actions | As of October 2023, President Biden has implemented targeted forgiveness programs, such as $10,000 to $20,000 in relief for eligible borrowers under the HEROES Act, but this has been blocked by the Supreme Court in June 2023. |

| Legal Challenges | Broad forgiveness initiatives have faced lawsuits, with courts questioning the President's authority to act without explicit congressional approval. |

| Political Feasibility | Forgiveness is a politically divisive issue, with support and opposition across party lines, affecting the likelihood of implementation. |

| Cost Implications | Large-scale forgiveness would have significant budgetary impacts, requiring funding or offset measures, which complicates its feasibility. |

| Eligibility Criteria | Any forgiveness program would likely include income limits, loan type restrictions, or other eligibility requirements to target specific borrowers. |

| Long-Term Impact | Forgiveness could reduce borrower debt burden but may raise concerns about moral hazard, inflation, and fairness to those who have already paid off loans. |

Explore related products

What You'll Learn

![]()

Legal Authority of the President

The President's legal authority to forgive student loans hinges on a delicate balance between executive power and congressional oversight. While the Higher Education Act of 1965 grants the Secretary of Education broad authority to "enforce, pay, compromise, waive, or release any right, title, claim, lien, or demand" related to federal student loans, this power is not explicitly delegated to the President. This distinction is crucial, as it underscores the constitutional principle of separation of powers, where Congress holds the purse strings and the President executes the law.

To navigate this legal landscape, consider the following steps: First, examine the specific language of the Higher Education Act, particularly Section 432(a), which outlines the Secretary's authority. Second, review relevant case law, such as the Supreme Court's decision in *Biden v. Nebraska* (2023), which struck down the President's attempt to forgive $400 billion in student loans through executive action. This case highlights the importance of statutory interpretation and the limits of executive authority. Third, analyze the role of the Department of Education, which serves as the primary agency responsible for administering federal student aid programs.

A comparative analysis of executive actions reveals a pattern of limited presidential authority in this area. For instance, President Obama's expansion of income-driven repayment plans and President Trump's temporary pause on student loan payments during the COVID-19 pandemic were both implemented through the Department of Education, not direct presidential action. These examples illustrate the President's reliance on existing statutory authority and administrative procedures, rather than unilateral executive power.

From a persuasive standpoint, advocates for broad presidential authority often cite the necessity of swift action in times of crisis. However, this argument must be weighed against the risk of overreaching executive power, which could undermine the rule of law and congressional authority. A more prudent approach would be to encourage legislative solutions, such as targeted loan forgiveness programs or reforms to the bankruptcy code, which would provide a more durable and legally sound framework for addressing student debt.

In practical terms, individuals seeking student loan relief should focus on existing programs, such as Public Service Loan Forgiveness (PSLF) or income-driven repayment plans. These options, while not as comprehensive as broad-scale forgiveness, offer tangible benefits and are firmly grounded in statutory authority. By understanding the legal boundaries of presidential power, borrowers can make informed decisions and advocate for sustainable policy changes that address the underlying issues driving student debt.

Student Loan Forgiveness Dates: What Borrowers Need to Know

You may want to see also

Explore related products

![]()

Impact on National Debt

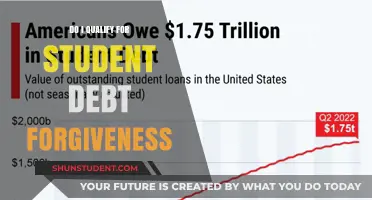

Student loan forgiveness, while a relief for millions of borrowers, would immediately add to the national debt. The Congressional Budget Office (CBO) estimates that canceling $10,000 per borrower would cost approximately $377 billion, while $50,000 per borrower could reach $1.4 trillion. These figures represent direct additions to the federal deficit, as the government would absorb the forgiven debt without a corresponding offset in revenue. Such a move would exacerbate an already precarious fiscal situation, with the national debt currently exceeding $30 trillion.

Critics argue that this approach shifts the burden from individual borrowers to taxpayers, many of whom did not attend college or have already paid off their loans. Proponents counter that the economic benefits—such as increased consumer spending and reduced defaults—could partially offset the cost. However, quantifying these benefits is complex, and they may not materialize quickly enough to mitigate the immediate impact on the debt. For instance, while forgiven loans could free up disposable income, the long-term effects on economic growth remain uncertain.

Another consideration is the potential for moral hazard. Broad forgiveness could incentivize future borrowers to take on larger loans under the assumption that they, too, might be forgiven. This behavior could inflate tuition costs further, as institutions raise prices in response to increased borrowing limits. Over time, this cycle could lead to even greater debt burdens for both individuals and the government, creating a self-perpetuating problem.

To minimize the impact on national debt, policymakers could explore targeted forgiveness programs rather than blanket cancellation. For example, forgiving loans for low-income borrowers or those in public service roles could provide relief without the staggering price tag of universal forgiveness. Additionally, pairing forgiveness with reforms to the higher education funding model—such as increased accountability for institutions with high default rates—could address root causes and prevent future crises.

Ultimately, the decision to forgive student loans requires balancing immediate relief with long-term fiscal sustainability. While the humanitarian and economic arguments for forgiveness are compelling, the direct and indirect costs to the national debt cannot be ignored. Without careful planning and complementary reforms, such a policy could alleviate one crisis while sowing the seeds for another.

Unlocking Student Loan Forgiveness: Weekly Work Hours Explained

You may want to see also

Explore related products

![]()

Eligibility Criteria for Forgiveness

The eligibility criteria for student loan forgiveness are a complex web of requirements, often leaving borrowers confused and frustrated. To navigate this maze, one must understand the specific conditions set by various forgiveness programs. For instance, the Public Service Loan Forgiveness (PSLF) program requires borrowers to make 120 qualifying payments while working full-time for a qualifying employer, such as a government or non-profit organization. This equates to approximately 10 years of consistent payments, a significant commitment that demands careful planning and documentation.

Consider the case of income-driven repayment (IDR) plans, which offer forgiveness after 20-25 years of qualifying payments. These plans adjust monthly payments based on income and family size, making them an attractive option for borrowers with lower incomes. However, to qualify for IDR forgiveness, borrowers must recertify their income and family size annually, ensuring their payments remain aligned with their financial situation. Failure to recertify can result in a reset of the forgiveness clock, emphasizing the need for vigilance and attention to detail.

A comparative analysis of forgiveness programs reveals distinct eligibility criteria for different professions. For example, the Teacher Loan Forgiveness program offers up to $17,500 in forgiveness for eligible teachers who work in low-income schools for five consecutive years. In contrast, the Nurse Corps Loan Repayment Program provides up to 85% of unpaid nursing education debt for licensed nurses who work in critical shortage facilities for two years. These profession-specific programs highlight the importance of researching and understanding the unique requirements tailored to one's career path.

To maximize the chances of qualifying for forgiveness, borrowers should adopt a strategic approach. This includes selecting the right repayment plan, consolidating loans if necessary, and maintaining accurate records of payments and employment. For instance, borrowers pursuing PSLF should submit an Employment Certification Form annually to ensure their payments and employment qualify. Additionally, staying informed about policy changes and updates is crucial, as demonstrated by the recent expansion of PSLF eligibility under the limited waiver period in 2021-2022. By proactively managing their loans and meeting the specific eligibility criteria, borrowers can increase their likelihood of achieving student loan forgiveness.

Ultimately, the key to unlocking student loan forgiveness lies in understanding the intricate eligibility criteria and taking a proactive, informed approach. Borrowers must carefully assess their financial situation, career path, and long-term goals to determine the most suitable forgiveness program. By doing so, they can navigate the complex landscape of student loan forgiveness, minimize their debt burden, and achieve financial stability. As the debate surrounding presidential authority to forgive student loans continues, individual borrowers must focus on the tangible steps they can take to qualify for existing forgiveness programs, ensuring a more secure financial future.

FBI and Student Loan Forgiveness: Separating Fact from Fiction

You may want to see also

Explore related products

$14.95 $14.95

![]()

Political and Public Opinion

The question of whether the president can forgive student loans has become a lightning rod for political and public debate, with opinions sharply divided along partisan lines. Democrats, particularly progressives, argue that executive action on student debt relief is both a moral imperative and a strategic move to address economic inequality. They point to the president’s authority under the Higher Education Act to modify or cancel federal student loans in times of national emergency, a power invoked during the COVID-19 pandemic to pause loan payments. Republicans, however, counter that such action oversteps executive authority, bypasses congressional oversight, and unfairly burdens taxpayers who did not attend college. This partisan split is evident in polling: a 2022 Pew Research survey found that 85% of Democrats supported widespread student loan forgiveness, compared to just 20% of Republicans.

Public opinion, while leaning in favor of some form of relief, is far from unanimous. A 2023 Morning Consult poll revealed that 55% of Americans support targeted student loan forgiveness for low-income borrowers, but only 37% back broad cancellation for all borrowers. This nuance highlights a critical divide: while many acknowledge the crushing weight of student debt, there is skepticism about blanket solutions. Independents, often the swing voters in elections, are particularly wary of large-scale forgiveness, with 42% opposing it due to concerns about fairness and fiscal responsibility. This middle ground suggests that public opinion is more pragmatic than ideological, favoring policies that balance relief with accountability.

The political calculus of student loan forgiveness is further complicated by its potential impact on voter turnout, especially among young adults. For Democrats, pushing for debt relief could energize a key demographic—voters aged 18–29, who hold a disproportionate share of student debt. However, this strategy risks alienating older voters who may view it as an unearned handout. Republicans, meanwhile, have framed the issue as a matter of fiscal discipline, appealing to their base’s concerns about government overreach. This tug-of-war underscores the challenge of crafting a policy that satisfies both political expediency and public sentiment.

To navigate this landscape, policymakers must consider a hybrid approach: targeted relief paired with systemic reforms. For instance, canceling up to $10,000 in debt for borrowers earning below $75,000 annually could address the most acute cases of financial hardship without triggering widespread backlash. Simultaneously, expanding income-driven repayment plans and capping interest rates would prevent future debt crises. Such a strategy aligns with public preferences for fairness and practicality, while also acknowledging the political realities of divided government. By focusing on incremental solutions, leaders can bridge the gap between ideological extremes and deliver meaningful change.

Student Loan Forgiveness: What’s in the New Stimulus Bill?

You may want to see also

Explore related products

![]()

Long-Term Economic Effects

Student loan forgiveness, while offering immediate relief to borrowers, triggers a cascade of long-term economic effects that ripple through the economy. One of the most direct impacts is on consumer spending. With reduced debt burdens, individuals have more disposable income, which can stimulate economic growth as they spend on goods, services, and investments. For instance, a borrower saving $200 monthly from loan forgiveness might allocate $100 to savings, $50 to dining out, and $50 to retail purchases. Over time, this increased spending could boost sectors like housing, automotive, and leisure, creating jobs and driving GDP growth. However, this effect is contingent on borrowers not redirecting savings into other debts or long-term investments, which could dampen immediate economic stimulation.

From a macroeconomic perspective, widespread student loan forgiveness could alter labor market dynamics. With less financial pressure, individuals might feel more empowered to pursue careers aligned with their passions rather than high-paying jobs solely for debt repayment. This shift could lead to increased innovation and productivity in creative and public service sectors. For example, a forgiven borrower might transition from a corporate job to teaching or starting a small business, contributing to societal well-being and economic diversity. However, this trend could also reduce the talent pool in high-demand fields like engineering or healthcare, potentially slowing growth in critical industries unless accompanied by targeted incentives or workforce development programs.

The long-term fiscal implications of student loan forgiveness are equally significant. While forgiving loans reduces government revenue from interest payments, it also shifts the burden of repayment to taxpayers. Estimates suggest forgiving $10,000 per borrower could cost the federal government over $300 billion, with broader forgiveness plans reaching trillions. This expenditure could necessitate budget reallocations or tax increases, potentially slowing economic growth if not managed carefully. Moreover, the perception of future forgiveness might discourage responsible borrowing, creating a moral hazard that could inflate tuition costs further, as institutions anticipate government bailouts.

Finally, the intergenerational impact of student loan forgiveness cannot be overlooked. Younger generations, burdened by rising tuition costs and stagnant wages, stand to benefit most from debt relief. However, older generations, who may have already paid off their loans or never borrowed, could perceive this as an unfair redistribution of resources. This tension could influence political and economic policies, shaping future debates on education funding and social welfare. For instance, a policy that caps annual loan forgiveness at $50,000 might balance relief with equity, ensuring benefits are targeted without exacerbating generational divides.

In conclusion, while student loan forgiveness offers immediate benefits, its long-term economic effects are complex and multifaceted. Policymakers must weigh the potential for increased consumer spending and labor market flexibility against fiscal risks and intergenerational equity concerns. By designing targeted, sustainable solutions, such as income-driven repayment plans or public service loan forgiveness expansions, the economic benefits can be maximized while mitigating unintended consequences.

Oregon's Student Loan Forgiveness Program: What You Need to Know

You may want to see also

Frequently asked questions

The president’s authority to forgive student loans unilaterally is a matter of legal debate. While the Higher Education Act grants the Secretary of Education the power to modify or waive certain federal student loans, large-scale debt cancellation without congressional action is controversial and has faced legal challenges.

Yes, presidents have used executive actions to forgive student loans in specific circumstances, such as through targeted programs like Public Service Loan Forgiveness (PSLF) or relief for defrauded borrowers under the Borrower Defense to Repayment rule. However, broad, one-time forgiveness for all borrowers has not been implemented.

Forgiving student loans could stimulate the economy by freeing up disposable income for borrowers, potentially boosting consumer spending and reducing defaults. However, critics argue it could increase the national debt, lead to inflation, and create fairness concerns for those who have already paid off their loans or chose not to attend college.