Students can get federal loans for private universities. However, federal student loans usually have lower interest rates than private student loans, so it is recommended that students first exhaust their federal loan options before turning to private lenders. To apply for federal student loans, students need to complete the Free Application for Federal Student Aid (FAFSA). This application also determines eligibility for other federal student aid, such as grants and work-study programs. Private student loans are provided by banks, credit unions, and other financial institutions, and they typically offer more flexibility in terms of repayment options and interest rates.

| Characteristics | Values |

|---|---|

| Who provides federal student loans? | The government |

| Who provides private student loans? | Banks, credit unions, and other financial institutions |

| What should you do first when applying for federal student loans? | Complete the Free Application for Federal Student Aid (FAFSA) |

| What determines your eligibility for federal student aid? | Your FAFSA application |

| What does the FAFSA determine your eligibility for besides federal student loans? | Other federal student aid like grants and work-study |

| What is the key difference between federal and private loans? | Interest rates—federal loans typically have lower interest rates |

| What else differs between federal and private loans? | Repayment options and other features |

| What is another difference between federal and private loans? | Private student loans usually offer the choice of a fixed or variable interest rate |

| What is a fixed interest rate? | Predictable monthly payments that stay the same |

| What is a variable interest rate? | Payments that may go up or down due to an increase or decrease in the loan's index |

| What are some other repayment plan differences? | Some private student loans allow you to make interest-only or fixed payments while you're in school, and some allow you to track your credit health for free with quarterly FICO Credit Scores |

| What is another difference between federal and private loans? | Private student loans offer more flexibility, as they can be taken out by a student (often with a cosigner), parent, or creditworthy individual |

| What is a disadvantage of private loans? | Private student loan rates are generally higher than federal loan rates |

| What is a Parent PLUS Loan? | A loan issued to a student's parents |

| What is a Direct PLUS Loan? | There are two types: Grad PLUS Loans for graduate and professional students, and Parent PLUS Loans |

Explore related products

What You'll Learn

- Federal student loans are provided by the government

- Private student loans are provided by banks and other financial institutions

- Federal loans usually have lower interest rates than private loans

- Private student loans offer more flexibility in repayment options

- Federal student loans require the completion of the FAFSA

![]()

Federal student loans are provided by the government

There are several key differences between federal and private student loans. Firstly, federal loans are provided by the government, while private loans come from banks, credit unions, and other financial institutions. Secondly, federal loans usually offer lower interest rates, which can result in significant savings over the life of the loan. However, it's important to note that interest rates for both types of loans can vary based on the economic climate.

Federal student loans also tend to provide more flexible repayment options. For example, some federal loans offer a grace period after graduation, allowing borrowers to postpone their payments until they have completed their studies. In contrast, private student loans often require borrowers to make interest payments while they are still in school. Nevertheless, private student loans can offer benefits such as the ability to track your credit health with quarterly FICO Credit Scores.

When considering federal student loans, it's essential to understand the eligibility criteria, application process, and terms and conditions. Federal loans may have specific requirements that differ from those of private loans. Additionally, federal loans may have different repayment plans and forgiveness programs that could impact your financial planning. It is always advisable to evaluate your anticipated monthly loan payments and expected future earnings before committing to any loan.

In summary, federal student loans provided by the government can be a valuable option for students attending private universities. They typically offer lower interest rates and more flexible repayment options compared to private loans. By completing the FAFSA, students can access federal financial aid and make informed decisions about their loan options. It is important to carefully review the terms and conditions of any loan agreement and seek guidance from a school counselor or lender if needed.

Transferring to University of Michigan: What You Need to Know

You may want to see also

Explore related products

![]()

Private student loans are provided by banks and other financial institutions

Private student loans depend on your credit score, and you may need a cosigner if your credit isn't strong. The interest rates and fees are based on your credit history or score, and having a cosigner with a better credit score could result in a lower interest rate and lower fees. Private student loan funds are usually sent directly to the school's financial aid office, and you must pay back the money you borrow, plus interest, whether you graduate or not.

There are a variety of private student loan options, and it is important to research which option is best for you. Some key information to understand includes the annual and cumulative loan limits, interest rates, fees, and loan terms. Private student loans may have variable interest rates, meaning the interest rate may change over time.

It is generally recommended to use federal student loans, if available, before resorting to private loans. Federal loans typically have lower interest rates and offer protections that private loans may not, such as fixed interest rates.

Syracuse University: OPT Student Hiring

You may want to see also

Explore related products

$6.99 $12.99

![]()

Federal loans usually have lower interest rates than private loans

When it comes to paying for college, specifically at a private university, there are a few options available to students and their families. Firstly, it's important to understand the difference between federal and private student loans. Federal loans are provided by the government, while private loans come from banks, credit unions, or other financial institutions. Both types of loans must be repaid with interest, but federal loans typically offer lower interest rates than private loans. This makes them a more attractive option for those seeking to minimise their overall loan cost.

Federal student loans are often the first choice for students seeking financial aid. To apply for federal loans, students need to complete the Free Application for Federal Student Aid (FAFSA). The FAFSA also determines eligibility for other types of federal student aid, such as grants and work-study programs. It is recommended to submit the FAFSA first, even if you plan to borrow both federal and private loans, as it provides a comprehensive view of your financial aid options.

Private student loans usually come into play when there is still a financial gap after receiving a federal loan or other financial aid. These loans offer flexibility, as they can be taken out by students, often with a cosigner, or by a creditworthy individual. Private loans typically provide a choice between fixed or variable interest rates. Fixed rates offer stability with predictable monthly payments, while variable rates can fluctuate, potentially leading to higher or lower monthly payments over time.

While federal loans generally have lower interest rates, it's important to note that the interest rates for both federal and private loans can vary based on the economic climate. Additionally, borrowers with bad credit may encounter higher interest rates, loan fees, and lower loan limits. To make informed borrowing decisions, students can utilise tools like Finaid's Loan Payment Calculator to estimate their repayment amounts after graduation.

In conclusion, when considering federal and private student loans, it is advisable to prioritise federal loans due to their typically lower interest rates. Private loans should be explored only after federal loan options have been exhausted or if unique features of private loans, such as flexible repayment plans or in-school payment options, align with your financial strategy. Ultimately, understanding the terms and conditions of each loan type and seeking guidance from the financial aid office at your chosen university can help you make the most suitable borrowing decisions for your educational journey.

International Students Thriving at Alfred University

You may want to see also

Explore related products

![]()

Private student loans offer more flexibility in repayment options

Federal student loans are available for students attending private universities. Typically, federal student loans total $5500 per year for middle-class or lower-income undergrads. However, the high cost of tuition fees at private universities means that students often need to take out additional loans or find other sources of funding.

Private student loans can offer more flexibility in repayment options. While federal student loans generally don't require payments during school, private student loans can offer both in-school and deferred repayment options. This means that borrowers can choose to make no payments while they're in school and during their separation or grace period, or they can opt to pay a fixed amount or only pay the interest each month. After this period, borrowers will be required to make principal and interest payments, and there may be programs available for budget flexibility, such as the Graduated Repayment Period.

Some private lenders also offer deferments on private student loans, allowing borrowers to reduce or postpone payments if they return to school or take on an internship, law clerkship, fellowship, or residency. Additionally, private loan borrowers may be eligible for loan modification, which lowers monthly payments by reducing the interest rate and possibly extending the loan term.

It's important to note that the specific repayment options available to private student loan borrowers can differ depending on the lender, and borrowers should carefully review the terms and conditions of their loan before making a decision. Seeking advice from a financial aid office or a professional is always recommended.

International Students at Cornell: Admissions Insights

You may want to see also

Explore related products

![]()

Federal student loans require the completion of the FAFSA

Federal student loans are provided by the government, while private student loans are provided by banks, credit unions, and other financial institutions. Each type of loan has its own eligibility criteria, application process, terms, and conditions. Federal student loans typically have lower interest rates compared to private student loans, and it is recommended to consider federal loans before opting for private loans.

To apply for federal student loans, individuals must complete the Free Application for Federal Student Aid (FAFSA). The FAFSA is crucial as it not only determines eligibility for federal student loans but also assesses an individual's suitability for other forms of federal student aid, including grants and work-study programs. By submitting the FAFSA, students can access the financial support they need to pursue their educational goals.

The FAFSA serves as a gateway to crucial financial assistance for students aiming to attend college or university. It is recommended that students submit their FAFSA applications first before considering private student loans. This ensures that they have explored all possibilities for federal aid, which often comes with more favourable terms and conditions.

Completing the FAFSA is a straightforward process, and resources are available to guide applicants through the questions. It is important to answer the questions accurately to maximise the chances of receiving financial aid. The FAFSA takes into account various factors to determine an individual's eligibility for federal student loans and other forms of aid.

The bottom line is that federal student loans require the completion of the FAFSA, which is a vital step in securing financial assistance for higher education. Students should be diligent in their research and understand the terms and conditions associated with federal and private student loans before making any decisions. Seeking guidance from a school counsellor or lender can help ensure that students make informed choices about their educational financing.

Teaching Careers: Liberty University Student Guide

You may want to see also

Frequently asked questions

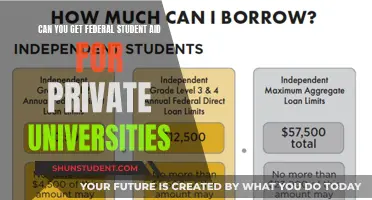

Yes, you can get federal student loans for private universities.

To apply for federal student loans, you need to complete the Free Application for Federal Student Aid (FAFSA®).

Federal loans are provided by the government, and private loans are provided by banks, credit unions, and other financial institutions. Federal loans typically have lower interest rates than private loans, and there are differences in repayment options and other features.

You should consider taking out a private student loan after you have exhausted your federal loan options and still have a funding gap.

It is important to understand the terms and conditions of your loan, including the interest rate, repayment plan, and loan limits. Student loans are legal agreements, so be sure to read and understand the contract before signing.