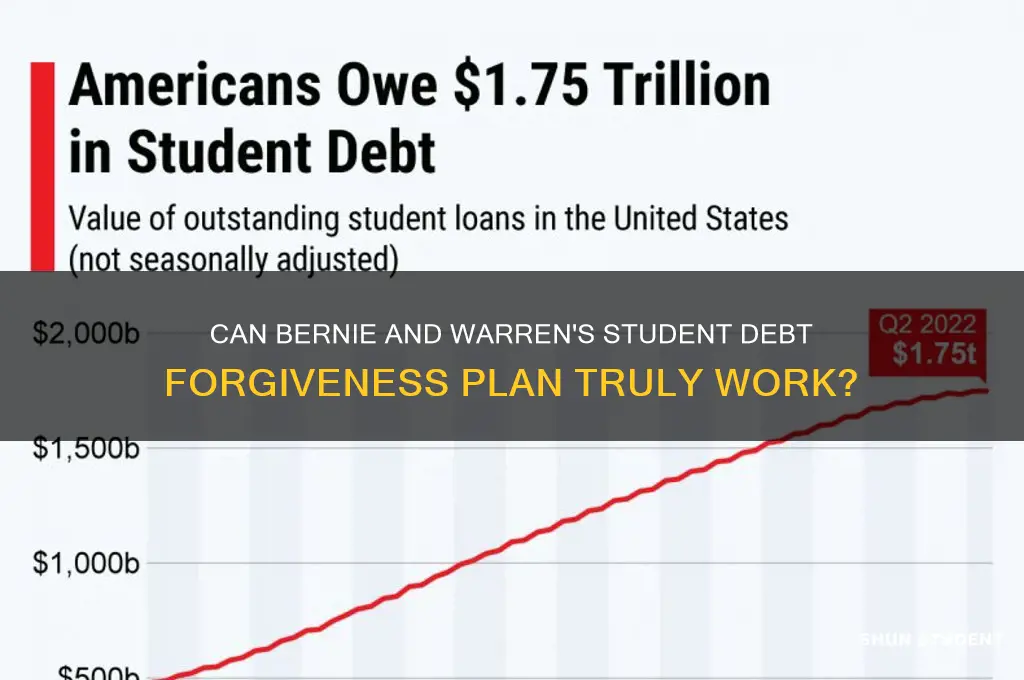

The idea of forgiving student loan debt has been a contentious topic in American politics, with Senators Bernie Sanders and Elizabeth Warren emerging as prominent advocates for this policy. Both have proposed ambitious plans to cancel a significant portion of student debt, arguing that it would alleviate the financial burden on millions of Americans and stimulate economic growth. Sanders has called for the elimination of all $1.6 trillion in outstanding student loan debt, while Warren has proposed canceling up to $50,000 per borrower, with a focus on targeting relief to those most in need. As the issue gains traction, the question remains: could Bernie and Warren's proposals really become a reality, and what would be the implications for borrowers, taxpayers, and the broader economy?

| Characteristics | Values |

|---|---|

| Proposed Policy | Cancellation of up to $50,000 in student loan debt per borrower. |

| Eligibility Criteria | Household income below $100,000 (phased out for incomes up to $250,000). |

| Estimated Cost | Approximately $1.6 trillion (as of latest estimates). |

| Funding Mechanism | Ultra-Millionaire Tax (2% annual tax on wealth above $50 million). |

| Impact on Borrowers | Over 44 million borrowers could benefit, with 75% debt-free immediately. |

| Economic Justification | Stimulate economy by increasing consumer spending and reducing defaults. |

| Political Feasibility | Faces opposition from Republicans and moderate Democrats; unlikely without legislative or executive action. |

| Legal Challenges | Potential lawsuits questioning executive authority to cancel debt. |

| Public Opinion | Majority support (58% in recent polls) but polarized along party lines. |

| Long-Term Implications | Could reshape higher education financing and reduce wealth inequality. |

| Criticisms | Concerns about moral hazard, fairness to non-borrowers, and inflationary risks. |

| Current Status | No federal action taken; limited to targeted relief (e.g., Public Service Loan Forgiveness). |

Explore related products

What You'll Learn

![]()

Economic Impact of Debt Forgiveness

Student debt forgiveness, a cornerstone of Bernie Sanders and Elizabeth Warren’s policy platforms, promises relief for millions but raises critical questions about its economic ripple effects. Proponents argue that canceling student debt would inject billions into the economy as borrowers redirect funds from loan payments to consumer spending. A 2021 study by the Roosevelt Institute estimated that canceling $1.4 trillion in student debt could boost GDP by $86 billion to $108 billion annually over the next decade. This increased spending could stimulate industries like retail, housing, and healthcare, creating a multiplier effect that benefits the broader economy. However, this optimistic outlook hinges on the assumption that freed-up income will be spent rather than saved, a behavior that varies widely among demographics.

Critics counter that debt forgiveness could exacerbate inflation by increasing demand without a corresponding rise in supply. If borrowers spend their newfound savings on goods and services in high demand, prices could rise, particularly in sectors like housing and education. For instance, if forgiven debt enables more individuals to purchase homes, housing prices might surge, offsetting some of the intended benefits. Additionally, the Federal Reserve’s monetary policy could tighten in response to inflationary pressures, potentially raising interest rates and slowing economic growth. This delicate balance underscores the need for complementary policies, such as investments in affordable housing and education, to mitigate unintended consequences.

Another economic consideration is the distributional impact of debt forgiveness. While it would benefit millions of borrowers, the policy is regressive in nature, as higher-income individuals—who hold a disproportionate share of student debt—would receive larger benefits. For example, a doctor with $200,000 in debt would gain more than a teacher with $30,000. To address this, policymakers could cap forgiveness at a certain income level or debt amount, ensuring that relief targets those most in need. Alternatively, pairing forgiveness with reforms like tuition-free college or income-driven repayment plans could create a more equitable system that prevents future debt accumulation.

Finally, the long-term economic impact of debt forgiveness depends on how it is funded. If financed through deficit spending, it could contribute to rising national debt, potentially leading to higher taxes or reduced government spending in other areas. However, if funded through progressive taxation—such as a wealth tax or increased taxes on high earners—it could reduce economic inequality while generating revenue. For instance, Warren’s proposed Ultra-Millionaire Tax of 2% on wealth above $50 million could raise an estimated $3.75 trillion over a decade, more than enough to cover the cost of canceling student debt. Such a funding mechanism would not only make the policy fiscally sustainable but also align with broader goals of economic justice.

In conclusion, the economic impact of student debt forgiveness is multifaceted, offering both opportunities and challenges. While it has the potential to stimulate growth and reduce financial burdens, its success hinges on careful design and implementation. Policymakers must weigh the short-term benefits against long-term risks, ensuring that relief is targeted, equitable, and sustainably funded. By addressing these complexities, debt forgiveness could serve as a transformative tool for economic empowerment rather than a source of unintended economic strain.

Unlocking Freedom: Strategies for Student Loan Debt Forgiveness Explained

You may want to see also

Explore related products

![]()

Political Feasibility of Large-Scale Relief

The political feasibility of large-scale student debt relief hinges on navigating a complex web of legislative, economic, and public opinion challenges. While Senators Bernie Sanders and Elizabeth Warren have championed debt forgiveness as a cornerstone of their progressive agendas, the path to implementation is fraught with obstacles. The sheer scale of the proposal—estimated to cost over $1 trillion—immediately raises questions about funding sources and budgetary priorities. Without a clear, politically palatable plan to offset such a massive expenditure, even sympathetic lawmakers may balk at the prospect of adding to the national debt.

Consider the legislative process itself, which demands a delicate balance of coalition-building and compromise. In a deeply polarized Congress, securing the necessary votes for such a transformative policy requires more than ideological alignment. It necessitates strategic concessions, such as targeting relief to specific demographics (e.g., low-income borrowers) or phasing in forgiveness over time. For instance, a means-tested approach could alleviate concerns about subsidizing high-earning professionals while focusing resources on those most burdened by debt. However, even these compromises risk alienating parts of the progressive base, who view universal forgiveness as a non-negotiable principle.

Public opinion, though increasingly supportive of debt relief, remains a double-edged sword. Polls show that a majority of Americans favor some form of student debt cancellation, particularly among younger voters. Yet, this support is not monolithic. Critics argue that broad forgiveness unfairly benefits college graduates at the expense of those who never attended college or already paid off their loans. To counter this narrative, proponents must frame relief as part of a broader investment in economic mobility, emphasizing its potential to stimulate consumer spending and reduce racial wealth gaps. Messaging matters: highlighting success stories from countries like Germany, where tuition-free education has bolstered social equity, could shift the debate from cost to value.

Finally, the executive branch offers a potential workaround to congressional gridlock, but its authority is limited. President Biden’s use of executive action to cancel $42 billion in debt for defrauded students and public service workers demonstrates the power of administrative measures. However, legal challenges and political backlash underscore the risks of overreaching. A more sustainable strategy might involve pairing executive actions with legislative efforts, such as expanding income-driven repayment plans or increasing funding for Pell Grants. This dual approach could create a sense of progress while laying the groundwork for more comprehensive reform.

In sum, the political feasibility of large-scale student debt relief demands a multi-pronged strategy that addresses fiscal, legislative, and public relations challenges. By combining targeted policy design, strategic messaging, and incremental action, proponents can increase the likelihood of success. The stakes are high, but so is the potential to reshape the economic futures of millions.

Will Biden Deliver on Student Loan Forgiveness? What We Know

You may want to see also

Explore related products

![]()

Moral Hazard Concerns in Policy

The proposal to forgive student loan debt, championed by figures like Bernie Sanders and Elizabeth Warren, raises significant moral hazard concerns. At its core, moral hazard refers to the risk that individuals or institutions will alter their behavior in undesirable ways when insulated from the consequences of their actions. In the context of student debt forgiveness, critics argue that such a policy could incentivize future borrowers to take on excessive debt, assuming it will eventually be absolved. This behavioral shift could perpetuate a cycle of rising tuition costs and irresponsible borrowing, undermining the very problem the policy aims to solve.

Consider the analogy of car insurance: if drivers knew their insurer would cover all damages regardless of fault, they might drive more recklessly. Similarly, blanket student debt forgiveness could signal to prospective students that financial prudence is optional. For instance, a student might choose a more expensive private university over an affordable public option, reasoning that the debt burden will later be lifted. This dynamic could exacerbate the already inflated cost of higher education, as institutions face less pressure to keep tuition rates competitive. Policymakers must weigh the immediate relief of debt forgiveness against the long-term behavioral incentives it creates.

To mitigate moral hazard, any debt forgiveness policy should incorporate targeted safeguards. One approach is means-testing, ensuring relief is directed toward those most in need rather than providing a windfall to high-earning graduates. Another strategy is to cap the amount of debt eligible for forgiveness, discouraging excessive borrowing. For example, forgiving up to $50,000 in debt per borrower could balance relief with accountability. Additionally, pairing forgiveness with reforms such as income-driven repayment plans or increased funding for public universities could address systemic issues without fostering dependency.

A comparative analysis of existing policies offers further insight. Countries like Germany and Norway, which offer tuition-free higher education, avoid moral hazard by eliminating the need for student loans altogether. In contrast, the U.S. system, which relies heavily on debt financing, creates conditions ripe for moral hazard. By studying these models, policymakers can design solutions that provide relief without inadvertently encouraging risky behavior. For instance, investing in affordable public education could reduce reliance on loans, while targeted forgiveness addresses existing debt burdens.

Ultimately, addressing moral hazard requires a nuanced approach that balances compassion with accountability. While forgiving student debt could provide immediate relief to millions, it must be part of a broader strategy to reform the higher education financing system. Without such reforms, the policy risks becoming a temporary fix that perpetuates deeper problems. By carefully structuring forgiveness programs and addressing root causes, policymakers can alleviate the burden of student debt while minimizing unintended consequences. The challenge lies in crafting a policy that rewards responsibility rather than rewarding recklessness.

Unlocking Student Loan Forgiveness: Your Guide to $10,000 Relief

You may want to see also

Explore related products

![]()

Long-Term Effects on Education Costs

Student debt forgiveness, as proposed by figures like Bernie Sanders and Elizabeth Warren, could reshape the financial landscape of higher education, but its long-term effects on education costs are complex and multifaceted. One immediate consequence might be a surge in tuition prices as institutions, anticipating government intervention, raise fees under the assumption that students will have greater access to funds. This phenomenon, known as the "Bennett Hypothesis," suggests that increased federal aid often leads to higher tuition, effectively canceling out the intended benefits for students. For instance, if a public university currently charges $10,000 annually, it might increase tuition to $12,000 post-forgiveness, exploiting the newfound financial flexibility of students.

To mitigate this risk, policymakers could implement tuition caps or tie federal funding to affordability metrics. For example, institutions receiving federal aid could be required to limit annual tuition increases to the rate of inflation, ensuring that costs remain manageable for future students. Additionally, incentivizing colleges to reduce administrative bloat—such as excessive spending on non-academic staff or luxury amenities—could redirect resources toward lowering tuition. A case study from Germany, where public universities are tuition-free, demonstrates that government investment in higher education can coexist with cost control when paired with strict regulatory oversight.

Another long-term effect could be a shift in student behavior, potentially leading to over-enrollment in higher education programs. With the burden of debt removed, more individuals might pursue degrees, even in fields with limited job prospects. This could devalue certain credentials and exacerbate labor market mismatches. For example, a 20% increase in humanities enrollments without a corresponding rise in related job opportunities could leave graduates underemployed. To address this, debt forgiveness could be paired with career counseling and workforce development programs, ensuring students make informed decisions about their academic paths.

Finally, the psychological and societal impacts of debt forgiveness could indirectly influence education costs. By alleviating financial stress, students might be more likely to invest in additional resources like study abroad programs, internships, or advanced certifications, which could drive up the overall cost of education. However, this increased investment could also yield higher returns in terms of employability and earnings, potentially offsetting the initial expense. For instance, a student pursuing a semester abroad might incur an additional $5,000 in costs but gain valuable skills that lead to a $10,000 salary increase post-graduation.

In conclusion, while student debt forgiveness holds promise for reducing individual financial burdens, its long-term effects on education costs require careful consideration and proactive policy measures. By addressing potential tuition increases, enrollment shifts, and behavioral changes, policymakers can ensure that the benefits of debt forgiveness are sustainable and equitable for future generations.

Navient Student Loan Forgiveness: Strategies to Erase Your Debt

You may want to see also

Explore related products

![]()

Public Opinion on Taxpayer Burden

The idea of forgiving student loan debt, as proposed by figures like Bernie Sanders and Elizabeth Warren, sparks intense debate over who bears the cost. Critics often frame this as a taxpayer burden, arguing that debt cancellation shifts the financial responsibility from individual borrowers to the broader public. This perspective raises questions about fairness: Why should taxpayers, many of whom did not attend college or have already paid off their loans, subsidize the education of others? Surveys show that while a majority of Americans support some form of student debt relief, opposition hardens when the conversation turns to the potential impact on federal spending and taxes. For instance, a 2022 Pew Research poll found that 58% of U.S. adults favored reducing student debt, but support dropped significantly when respondents were informed of the estimated $1.6 trillion price tag.

To understand the taxpayer burden argument, consider the mechanics of funding debt forgiveness. The federal government would need to allocate a substantial portion of its budget to cover the canceled debt, potentially diverting resources from other priorities like infrastructure, healthcare, or social services. Critics argue that this reallocation could exacerbate existing fiscal challenges, such as the national debt, which stood at over $31 trillion in 2023. Proponents counter that the economic benefits of debt forgiveness—such as increased consumer spending and reduced defaults—could offset these costs over time. However, quantifying these benefits remains contentious, leaving taxpayers uncertain about the net impact on their financial well-being.

A comparative analysis of taxpayer burden reveals disparities in public opinion based on demographic factors. Younger Americans, who are more likely to hold student debt, tend to view forgiveness as a necessary investment in their future. In contrast, older generations, many of whom paid their way through college or benefited from lower tuition costs, often express skepticism. For example, a 2021 survey by the University of Chicago found that 63% of respondents aged 18–29 supported debt cancellation, compared to just 37% of those over 65. This generational divide underscores the challenge of crafting a policy that balances the interests of borrowers and non-borrowers alike.

Practical considerations further complicate the taxpayer burden debate. If debt forgiveness were implemented, policymakers would need to decide whether to impose new taxes or cut existing programs to cover the cost. One proposal suggests a wealth tax on high-income earners, but this approach faces political and logistical hurdles. Alternatively, some argue for means-tested forgiveness, targeting relief to low- and middle-income borrowers, which could reduce the overall cost but may alienate higher-earning borrowers who still struggle with debt. Without a clear funding mechanism, the taxpayer burden argument remains a potent obstacle to widespread debt cancellation.

Ultimately, the taxpayer burden debate hinges on a fundamental question: Is student debt forgiveness a collective responsibility or an individual one? Framing the issue in these terms can help policymakers and the public weigh the moral and economic implications. For taxpayers, the key takeaway is that while debt cancellation could provide relief to millions of borrowers, it is not a cost-free solution. Engaging in informed discussions, considering alternative funding models, and advocating for transparency in policy design can help mitigate concerns and foster a more equitable approach to addressing the student debt crisis.

FAU Students' Perspective: Embracing Grade Forgiveness in College Academics

You may want to see also

Frequently asked questions

Both Bernie Sanders and Elizabeth Warren have proposed plans to cancel a significant portion of student loan debt. Sanders has advocated for canceling all $1.6 trillion in student debt, while Warren proposed canceling up to $50,000 per borrower for 95% of loan holders. However, the feasibility of these plans depends on legislative and political support, as well as potential legal challenges.

Sanders proposed funding his plan through a tax on Wall Street transactions, while Warren suggested a wealth tax on the richest Americans. Both plans aim to redistribute wealth to address economic inequality, but critics argue these measures could face opposition and have broader economic implications.

This is a common concern. Proponents argue that debt forgiveness would stimulate the economy and reduce racial and economic disparities. However, opponents believe it could be perceived as unfair to those who sacrificed to pay off their debt or pursued alternative paths. Policymakers would need to address these equity concerns in any implementation.