Many borrowers wonder whether Federal Family Education Loan (FFEL) Program loans qualify for student loan forgiveness. FFEL loans, which were issued by private lenders but guaranteed by the federal government, are eligible for certain forgiveness programs, but their eligibility depends on the specific program and the borrower’s circumstances. For instance, FFEL loans can be consolidated into Direct Loans to qualify for Public Service Loan Forgiveness (PSLF) or income-driven repayment (IDR) forgiveness. However, they are not automatically eligible for programs like the one-time student loan forgiveness initiative announced in 2022, which primarily applies to Direct Loans. Borrowers with FFEL loans must carefully review program requirements and consider consolidation options to maximize their chances of qualifying for forgiveness.

| Characteristics | Values |

|---|---|

| Eligibility for Forgiveness | FFEL loans do not automatically qualify for federal forgiveness programs like Public Service Loan Forgiveness (PSLF) or income-driven repayment (IDR) forgiveness unless consolidated into a Direct Loan. |

| Consolidation Requirement | FFEL loans must be consolidated into a Direct Consolidation Loan to become eligible for federal forgiveness programs. |

| Public Service Loan Forgiveness (PSLF) | FFEL loans are ineligible for PSLF unless consolidated into a Direct Loan and meet PSLF requirements. |

| Income-Driven Repayment (IDR) Forgiveness | FFEL loans are ineligible for IDR forgiveness unless consolidated into a Direct Loan and enrolled in an IDR plan. |

| Teacher Loan Forgiveness | FFEL loans may qualify for Teacher Loan Forgiveness if the borrower meets eligibility criteria (e.g., teaching in a low-income school). |

| Total and Permanent Disability (TPD) Discharge | FFEL loans may qualify for TPD discharge, but the process differs from Direct Loans. |

| Closed School Discharge | FFEL loans may qualify for discharge if the school closed while the borrower was enrolled or shortly after withdrawal. |

| Death Discharge | FFEL loans are discharged upon the borrower's death, similar to Direct Loans. |

| Bankruptcy Discharge | FFEL loans may be discharged in bankruptcy, but it is rare and requires proving undue hardship. |

| State-Specific Forgiveness Programs | Some states offer forgiveness programs that may include FFEL loans, depending on the program's criteria. |

| Servicer | FFEL loans are serviced by private companies, not the federal government, which affects forgiveness options. |

| Current Policy (as of 2023) | No direct federal forgiveness for FFEL loans unless consolidated into Direct Loans. |

Explore related products

What You'll Learn

![]()

FFEL Loan Types Eligible

Federal Family Education Loan (FFEL) program loans, though no longer issued since 2010, remain a significant portion of outstanding student debt. Borrowers often wonder if these loans qualify for forgiveness programs. The answer hinges on the specific FFEL loan type and the forgiveness program in question. Not all FFEL loans are created equal in the eyes of forgiveness eligibility.

Understanding which FFEL loan types are eligible for forgiveness is crucial for borrowers seeking debt relief.

Stafford Loans: These are the most common FFEL loans and generally qualify for income-driven repayment (IDR) plans, which can lead to forgiveness after 20-25 years of qualifying payments. Additionally, Stafford loans may be eligible for Public Service Loan Forgiveness (PSLF) if the borrower meets the program's stringent requirements, including 10 years of qualifying payments while working full-time for a qualifying employer.

PLUS Loans: FFEL PLUS loans, taken out by parents on behalf of dependent students, are also eligible for IDR plans, but forgiveness options are more limited. They do not qualify for PSLF unless consolidated into a Direct Consolidation Loan.

Consolidation Considerations: Consolidating FFEL loans into a Direct Consolidation Loan can open up additional forgiveness possibilities. This is particularly beneficial for FFEL PLUS loans seeking PSLF eligibility. However, consolidating resets the clock on IDR forgiveness timelines.

Important Caveats: FFEL loans held by commercial lenders are not eligible for most federal forgiveness programs unless consolidated into Direct Loans. Additionally, private student loans, even if they were used to pay for education, are never eligible for federal forgiveness programs.

Action Steps: Borrowers with FFEL loans should carefully review their loan types and explore consolidation options if seeking PSLF. Consulting with a student loan counselor can provide personalized guidance on navigating forgiveness programs and maximizing debt relief opportunities.

Student Loan Forgiveness: What Borrowers Need to Know Now

You may want to see also

Explore related products

![]()

Consolidation Requirements for Forgiveness

Federal Family Education Loan (FFEL) borrowers seeking forgiveness often encounter a critical hurdle: consolidation. Unlike Direct Loans, FFEL loans aren’t eligible for programs like Public Service Loan Forgiveness (PSLF) unless they’re first consolidated into a Direct Consolidation Loan. This process effectively converts FFEL loans into Direct Loans, unlocking access to forgiveness programs. However, consolidation isn’t automatic—borrowers must apply through the Federal Student Aid website and choose the correct servicer to ensure their loans remain on track for forgiveness.

Consolidation comes with caveats. For instance, any payments made toward forgiveness before consolidation are reset. If a borrower had already made 5 years of qualifying payments under an FFEL loan, those payments won’t count toward PSLF after consolidation. This reset can delay forgiveness timelines, so borrowers must weigh the trade-offs carefully. Additionally, consolidating FFEL loans into a Direct Loan may change interest rates, as the new rate is a weighted average of the previous loans, rounded to the nearest eighth of a percent.

Another critical requirement is timing. Borrowers must consolidate their FFEL loans *before* applying for forgiveness. For example, a teacher pursuing Teacher Loan Forgiveness must consolidate FFEL loans into a Direct Consolidation Loan to qualify. Failure to consolidate first can disqualify the borrower from forgiveness programs. It’s also essential to ensure the new Direct Consolidation Loan is placed with a servicer that handles forgiveness applications, such as MOHELA for PSLF.

Practical tips can streamline the process. First, gather all FFEL loan information, including account numbers and servicer details, before starting the consolidation application. Second, select the income-driven repayment plan that aligns with forgiveness goals during the consolidation process. Third, keep detailed records of all payments and correspondence, as documentation is crucial for forgiveness applications. Finally, monitor the consolidation status closely—errors or delays can derail forgiveness eligibility.

In summary, consolidation is a non-negotiable step for FFEL borrowers pursuing forgiveness. While it opens the door to programs like PSLF, it resets payment counts and alters interest rates, requiring careful consideration. By understanding the requirements, timing, and potential pitfalls, borrowers can navigate consolidation effectively and stay on course for loan forgiveness.

Biden's Student Debt Forgiveness Plan: What You Need to Know

You may want to see also

Explore related products

![]()

Income-Driven Repayment Plans

Income-driven repayment (IDR) plans can be a lifeline for borrowers with Federal Family Education Loan (FFEL) Program loans seeking forgiveness, but navigating eligibility requires precision. Unlike Direct Loans, FFEL loans aren’t automatically eligible for Public Service Loan Forgiveness (PSLF) or IDR forgiveness. However, consolidating FFEL loans into a Direct Consolidation Loan opens the door to these programs. Once consolidated, borrowers can enroll in an IDR plan, which caps monthly payments at a percentage of discretionary income (typically 10-20%) and offers forgiveness after 20-25 years of qualifying payments. This strategic move transforms FFEL loans from forgiveness-ineligible to forgiveness-eligible, making consolidation a critical first step.

Choosing the right IDR plan is crucial for maximizing forgiveness potential. For FFEL borrowers post-consolidation, Revised Pay As You Earn (REPAYE) is often the most advantageous, as it offers the lowest payment cap (10% of discretionary income) and forgiveness after 20 years for undergraduate loans. However, if you’re married and file taxes jointly, Income-Based Repayment (IBR) may be preferable, as it excludes spousal income from calculations in certain cases. Pay As You Earn (PAYE) and Income-Contingent Repayment (ICR) are also options, but their higher payment caps (10-20%) and longer forgiveness timelines (20-25 years) make them less ideal for most. Analyzing your income, family size, and tax filing status is essential to selecting the plan that minimizes payments and accelerates forgiveness.

A common pitfall for FFEL borrowers is failing to consolidate before enrolling in an IDR plan. Payments made on FFEL loans prior to consolidation do not count toward IDR forgiveness, even if they were made under an IDR-like plan. For example, if a borrower made 10 years of payments on an FFEL loan under a standard repayment plan, those payments are essentially reset to zero after consolidation. To avoid this, consolidate immediately and begin making qualifying payments under the new Direct Loan. Additionally, ensure your income documentation is accurate and up-to-date, as errors can lead to overpayment or disqualification from the program.

For borrowers nearing retirement, IDR plans offer a unique advantage: forgiveness after 20-25 years, regardless of the remaining balance. This means that older FFEL borrowers who consolidate and enroll in an IDR plan can strategically time their payments to align with retirement, potentially eliminating debt without significant financial strain. For instance, a 50-year-old borrower consolidating FFEL loans into REPAYE could make 20 years of income-driven payments, reaching forgiveness by age 70. While forgiven amounts may be taxed as income, careful planning with a financial advisor can mitigate this burden.

In conclusion, FFEL loans can qualify for student loan forgiveness through IDR plans, but only after consolidation into a Direct Loan. By selecting the optimal IDR plan, avoiding common pitfalls, and strategically timing payments, borrowers can transform their FFEL debt into a manageable, forgivable obligation. This approach requires proactive steps and careful planning but offers a clear path to financial relief for those burdened by long-standing student loans.

Can SCOTUS Block Student Loan Forgiveness? Legal Battle Explained

You may want to see also

Explore related products

![]()

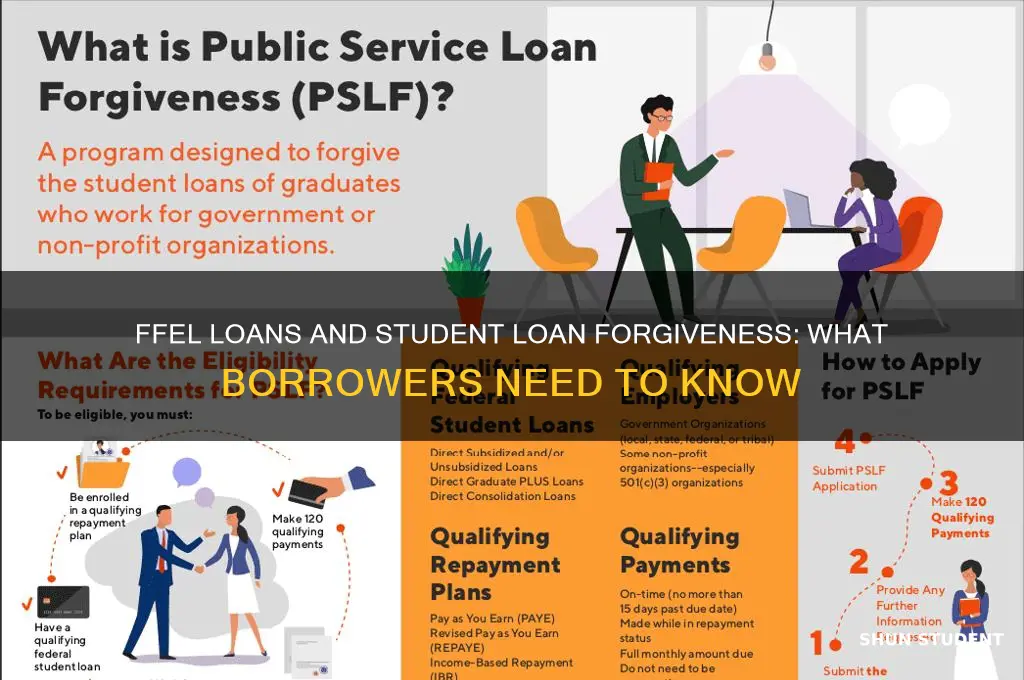

Public Service Loan Forgiveness (PSLF) Rules

Federal Family Education Loan (FFEL) program loans, once a cornerstone of student financing, present a unique challenge for borrowers seeking Public Service Loan Forgiveness (PSLF). The PSLF program, designed to incentivize careers in public service, offers debt relief after 120 qualifying payments. However, FFEL loans, originated by private lenders and guaranteed by the government, are not directly eligible for PSLF. This ineligibility stems from the program's requirement that loans be held by the Department of Education, which is not the case for FFEL loans.

Borrowers with FFEL loans have two primary strategies to pursue PSLF. The first involves consolidating FFEL loans into a Direct Consolidation Loan, effectively transferring the debt to the Department of Education. This consolidation process, while straightforward, requires careful consideration. Borrowers must ensure that their consolidation does not reset the clock on their qualifying payments, as only payments made after consolidation count toward PSLF. The second strategy, though more complex, involves the Temporary Expanded Public Service Loan Forgiveness (TEPSLF) initiative. This program, introduced in 2018, provides a pathway for borrowers with FFEL loans who have made payments under a non-qualifying repayment plan. By submitting a TEPSLF application, borrowers can have their payments retroactively counted toward PSLF, provided they meet specific criteria, including employment certification and payment history.

The consolidation route demands meticulous planning. Borrowers should gather all necessary documentation, including employment certification forms, before initiating the process. It's crucial to understand that consolidation may not be the best option for everyone, especially those close to the 120-payment threshold. In such cases, the TEPSLF initiative might be more advantageous. This program, while temporary, offers a lifeline to borrowers who have diligently served in public service but found themselves ineligible due to loan type or repayment plan.

A comparative analysis reveals the nuances between these strategies. Consolidation provides a clear path to PSLF eligibility but may delay forgiveness for those with significant payment histories. TEPSLF, on the other hand, offers a faster route to forgiveness for eligible borrowers but requires a detailed application process and a thorough review of payment history. The choice between these options hinges on individual circumstances, including the number of qualifying payments already made, the borrower's current repayment plan, and their long-term financial goals.

In conclusion, while FFEL loans are not directly eligible for PSLF, borrowers are not without options. By strategically consolidating their loans or applying for TEPSLF, they can navigate the complexities of the program and work toward debt relief. Each approach has its advantages and considerations, underscoring the importance of informed decision-making in the pursuit of student loan forgiveness.

Student Debt Forgiveness Reimbursement: Who Received Financial Relief?

You may want to see also

Explore related products

![]()

Loan Forgiveness Programs and FFEL Loans

FFEL loans, part of the Federal Family Education Loan Program, present a unique challenge for borrowers seeking student loan forgiveness. Unlike Direct Loans, which are eligible for programs like Public Service Loan Forgiveness (PSLF) and income-driven repayment (IDR) forgiveness, FFEL loans are not automatically eligible for these programs. This distinction stems from their origination through private lenders, even though they are federally guaranteed. Borrowers with FFEL loans must take specific steps to qualify for forgiveness, often involving consolidation into a Direct Consolidation Loan.

Consolidating FFEL loans into the Direct Loan program is a critical step for accessing forgiveness programs. Once consolidated, borrowers can pursue PSLF by working full-time for a qualifying employer, such as a government or nonprofit organization, and making 120 eligible payments. Similarly, consolidating FFEL loans allows borrowers to enroll in income-driven repayment plans, which can lead to forgiveness after 20–25 years of payments, depending on the plan. However, consolidating resets the payment count, so borrowers should carefully consider the timing to avoid losing progress toward forgiveness.

One lesser-known option for FFEL loan forgiveness is the Teacher Loan Forgiveness Program. Teachers with FFEL loans who work in low-income schools for five consecutive years may qualify for up to $17,500 in forgiveness. This program does not require consolidation into Direct Loans, making it a viable option for FFEL borrowers in the education sector. However, eligibility is limited to specific teaching roles and schools, so borrowers should verify their qualifications before applying.

Borrowers with FFEL loans should also be aware of temporary relief measures, such as those introduced during the COVID-19 pandemic. While FFEL loans were initially excluded from payment pauses and interest waivers, the U.S. Department of Education later allowed commercially held FFEL loans to qualify if the lender agreed to participate. These measures highlight the evolving nature of student loan policies and the importance of staying informed about changes that could benefit FFEL borrowers.

In conclusion, FFEL loans require strategic action to qualify for forgiveness programs. Consolidation into Direct Loans is often the key to accessing PSLF and IDR forgiveness, but borrowers must weigh the trade-offs, such as resetting payment counts. Alternatively, programs like Teacher Loan Forgiveness offer targeted relief without consolidation. By understanding these options and staying updated on policy changes, FFEL borrowers can navigate the complexities of loan forgiveness and work toward financial freedom.

Student Loan Forgiveness After Death: What Happens to Your Debt?

You may want to see also

Frequently asked questions

FFEL loans do not directly qualify for PSLF, but they can become eligible if consolidated into a Direct Consolidation Loan. Once consolidated, the loans are treated as Direct Loans and can qualify for PSLF if all other program requirements are met.

FFEL loans held by the Department of Education were initially eligible for the one-time forgiveness program, but the program is currently on hold due to legal challenges. Privately held FFEL loans were not eligible unless they were consolidated into Direct Loans before the application deadline.

FFEL loans can qualify for IDR forgiveness after 20–25 years of qualifying payments, but they must first be consolidated into a Direct Consolidation Loan. Payments made under an IDR plan before consolidation do not count toward the forgiveness period unless the loans are consolidated.