Student loans are a common way to fund a college education, and they are available from both federal and private lenders. Federal loans are often needs-based and offer lower interest rates and flexible repayment plans, while private loans are similar to other bank loans and usually require a credit check. Students can use loan funds to pay for tuition, housing, food, and other expenses. However, it is important to understand that student loans should be primarily used for education-related purposes and not for unnecessary spending. Before taking out student loans, individuals should explore scholarships, grants, and federal loans, as these options may provide sufficient funding without incurring the same level of debt as private loans.

| Characteristics | Values |

|---|---|

| Who offers student loans? | Private lenders (banks, credit unions) and federal lenders |

| Who can apply for a student loan? | Students, parents or other creditworthy individuals |

| What are the types of student loans? | Direct subsidized loans, direct unsubsidized loans, Direct PLUS Loans |

| What are the requirements? | For federal loans, fill out the Free Application for Federal Student Aid (FAFSA); for private loans, submit an application to a bank or other private lender |

| What can student loans be used for? | Tuition, rent, utilities, groceries, and other living expenses |

| What should student loans not be used for? | Shopping sprees, expensive meals or drinks, vehicles |

| What are the repayment terms? | Federal loans offer income-driven repayment plans and flexible options; private loans offer fixed or variable interest rates and different repayment plans |

| What are the interest rates? | Federal loans typically have lower fixed interest rates; private loans often have variable rates |

Explore related products

What You'll Learn

![]()

Federal vs. private loans

When it comes to student loans, there are two main categories: federal loans and private loans. Both types of loans have their own unique features, eligibility criteria, application processes, and terms and conditions. Here is a detailed comparison between federal and private student loans:

Federal Student Loans

Federal student loans are provided by the government, specifically the US Department of Education, to cover higher education expenses. One of the key advantages of federal loans is their low eligibility requirements, making them accessible to a wide range of borrowers. Federal loans do not consider your credit score, and their interest rates are fixed for all borrowers in a given school year. These rates tend to be lower than most private student loans, especially for borrowers without a cosigner. Additionally, federal loans offer income-driven repayment plans, allowing borrowers to pay a percentage of their discretionary income. This flexibility ensures that borrowers can manage their loan repayments based on their financial situation. Federal loans also provide the option for partial loan forgiveness under certain circumstances, such as the Teacher Loan Forgiveness program. However, federal loans have borrowing limits, particularly for undergraduate students, and borrowers must pay an origination fee when taking out the loan.

Private Student Loans

Private student loans are issued by banks, credit unions, or other financial institutions. These loans are a good option for students who have reached the federal borrowing limit or do not qualify for federal loans. Private loans typically offer a choice between fixed and variable interest rates. With a fixed rate, your monthly payments remain predictable, while variable rates can fluctuate based on the loan's index. Private loans also provide various repayment plans, including the option to make interest-only or fixed payments while still in school, which can lower your total loan cost. Private loans usually require a creditworthy cosigner, such as a parent, and often involve a credit check.

In summary, federal student loans are generally the more favourable option due to their low eligibility requirements, flexible repayment plans, and lower interest rates. Private student loans can be useful if federal loans do not cover the full cost of tuition or if you have strong credit. It is recommended to explore federal loans, scholarships, and grants before considering private student loans.

Public University Students: Studying Abroad in Turkey

You may want to see also

Explore related products

![]()

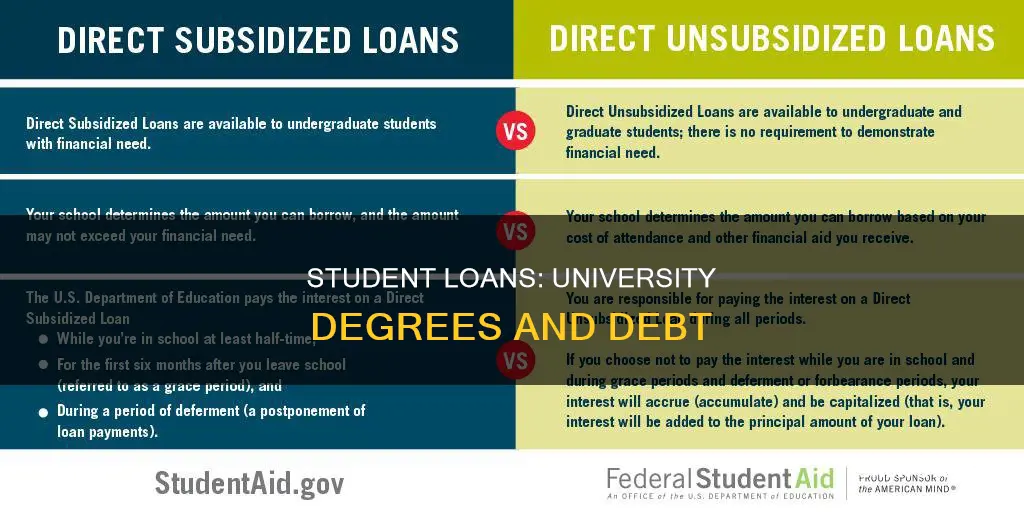

Direct subsidized loans

Federal Direct Subsidized Loans are need-based loans for undergraduate students. Eligibility is determined by your cost of attendance, expected family contribution, and other financial aid (such as grants or scholarships). The maximum amount you can borrow each academic year depends on your grade level and dependency status. Direct Subsidized Loans do not accrue interest while you are in school at least half-time or during deferment periods.

To be eligible for a federal student loan, you must submit the Free Application for Federal Student Aid (FAFSA). It's important to submit the FAFSA as early as possible, as some grant money is awarded on a first-come, first-served basis. You must submit a new FAFSA every year you need money for college.

Federal student loans offer income-driven repayment plans, where the rate of repayment is based on the borrower's salary after college. Borrowers don't need a credit check to be considered (except for PLUS Loans for parents and graduate students). You can change your repayment plan even after taking out the loan.

Direct Unsubsidized Loans, on the other hand, are not based on financial need. Your school will determine how much you can borrow, based on the cost of attendance and other financial aid. Interest is charged during in-school, deferment, and grace periods, and you are responsible for this interest from the time the loan is disbursed until it's paid in full.

Unlocking Student Success: The Role of Colleges and Universities

You may want to see also

Explore related products

![]()

Direct unsubsidized loans

To answer the question, "Do I need to be a university student to take out student loans?"—yes, you do. Student loans are specifically for students who are enrolled in an academic program.

Now, here's detailed information about Direct Unsubsidized Loans:

To apply for a Direct Unsubsidized Loan, you must complete the Free Application for Federal Student Aid (FAFSA) or the Renewal FAFSA for returning students. This application is available at StudentAid.gov. It's important to note that there is no cost to submit the FAFSA, and it must be completed each year you need financial aid for college. The earlier you submit the FAFSA after October 1, the better, as some grant money is awarded on a first-come, first-served basis.

Once you've submitted the FAFSA, you'll receive a financial aid award letter from your school's financial aid office. This letter will summarize your available financial aid, including any Direct Subsidized Loans (if eligible) and Direct Unsubsidized Loans. To accept the financial aid package, including any student loans, you'll need to contact your financial aid office and sign any necessary paperwork, such as the Master Promissory Note (MPN).

It's worth mentioning that Direct Unsubsidized Loans have a six-month grace period once the student drops below half-time enrollment or completes their program. However, unlike subsidized loans, you are required to cover all the interest that accrues on these loans until they are completely repaid. The interest rates for Direct Unsubsidized Loans are fixed and do not change over the life of the loan. For the 2024-2025 academic year, the fixed interest rate for undergraduate students is 6.53%, while the rate for graduate and professional students is 8.08%.

Understanding University Student Loans: A Guide for Beginners

You may want to see also

Explore related products

$16.53 $22.99

![]()

Parent loans

Parents who want to help their children pay for college can choose from both federal and private student loan options. Comparing your options is crucial because there may be trade-offs to each loan type.

Federal Parent PLUS Loans

Federal PLUS loans are credit-based, unsubsidized federal loans for parents and graduate/professional students. They have higher interest rates than other federal loans and high origination fees, but they also provide generous repayment terms. Parent PLUS loan borrowers must not have any adverse credit history to qualify. Borrowers with adverse credit history can still receive a parent PLUS loan by enlisting a co-signer without adverse credit history or documenting extenuating circumstances for their credit history. Federal PLUS loans are available to parents of undergraduates as well as graduate students. They are best for parents who may need the safety net they offer, like income-contingent repayment after consolidation.

Private Parent Loans

Private parent student loans may offer lower fees and potentially lower interest rates for the most creditworthy borrowers, but feature fewer flexible repayment options. Private student loans usually offer the choice of a fixed or variable interest rate. Fixed rates stay the same, giving you predictable monthly payments. Variable rates may go up or down due to an increase or decrease in the loan's index.

Exploring Student Organizations at Emporia State University

You may want to see also

Explore related products

$8.34 $17.99

![]()

What can student loans be spent on?

Student loans are intended to pay for college, but education costs can include more than just tuition fees. Student loans can also be used for living expenses, such as meals, on-campus housing, off-campus rent, utilities, groceries, transportation, and basic living necessities. They can also be used to purchase books and supplies, including textbooks, pens, notebooks, and backpacks. Additionally, equipment that is needed for classes, such as laptops, software, or cameras, can be covered by student loans. Dependent care expenses, such as childcare or adult care while attending classes, may also be covered, but it is important to check the loan agreement for approved uses.

It is important to note that student loans should not be spent on non-essential items or entertainment, such as concert tickets, streaming services, high-end clothing, or vacations. Lenders require that student loan money be used for education costs and basic living expenses, and spending it on non-approved expenses can result in serious consequences, including loan termination and ineligibility for future borrowing. While there may not be direct tracking of how student loan money is spent, lenders can take action if they discover misuse of funds.

Beckett Student Population: How Many Are There?

You may want to see also

Frequently asked questions

Yes, you need to be enrolled in university to take out a student loan. The financial aid office at your university will determine how much aid to make available to you based on your FAFSA application.

FAFSA stands for Free Application for Federal Student Aid. It is a form that must be filled out and submitted when applying for federal student loans. The FAFSA is used by financial aid offices at colleges to determine how much aid to offer a student.

Student loans are meant to be used for education purposes. They can be used to pay for tuition, fees, room and board, and other expenses such as housing, food, a new laptop, and bus tickets.