Forgiving student debt has been a contentious issue, with proponents arguing it would alleviate financial burdens and stimulate the economy. However, opponents contend that widespread debt forgiveness is unfair to those who have already repaid their loans or chose not to pursue higher education, effectively shifting the financial burden onto taxpayers. Additionally, it could incentivize future borrowers to take on excessive debt under the assumption that it might be forgiven later, potentially exacerbating the very problem it aims to solve. Critics also argue that addressing the root causes of skyrocketing tuition costs and improving access to affordable education would be a more sustainable and equitable solution than blanket debt forgiveness.

| Characteristics | Values |

|---|---|

| Economic Impact | Forgiving student debt could increase inflation and burden taxpayers. |

| Moral Hazard | May incentivize future borrowers to take on excessive debt recklessly. |

| Fairness Concerns | Critics argue it unfairly benefits higher-income individuals who can afford repayment. |

| Cost to Taxpayers | Estimates suggest forgiving all student debt could cost trillions of dollars. |

| Targeted vs. Universal Relief | Opponents prefer targeted relief for low-income borrowers instead of blanket forgiveness. |

| Impact on Higher Education | Could lead to unchecked tuition increases by colleges and universities. |

| Work Ethic and Responsibility | Emphasizes personal responsibility for repaying debts incurred voluntarily. |

| Alternative Solutions | Advocates for income-driven repayment plans, refinancing options, or tuition reform. |

| Political Divide | Primarily supported by conservative and libertarian viewpoints. |

| Long-Term Financial Behavior | Concerns that forgiveness may discourage prudent financial decision-making. |

Explore related products

What You'll Learn

- Economic Impact: Canceling debt may inflate taxes, burdening non-student-debtors and straining federal budgets

- Moral Hazard: Forgiveness could discourage personal responsibility and future prudent financial decision-making

- Inequality Concerns: Benefits higher-income graduates more, widening wealth gaps instead of aiding the poorest

- Alternative Solutions: Investing in affordable education or income-driven repayment plans may be fairer

- Political Backlash: Debt forgiveness risks alienating taxpayers, sparking divisive political and social reactions

![]()

Economic Impact: Canceling debt may inflate taxes, burdening non-student-debtors and straining federal budgets

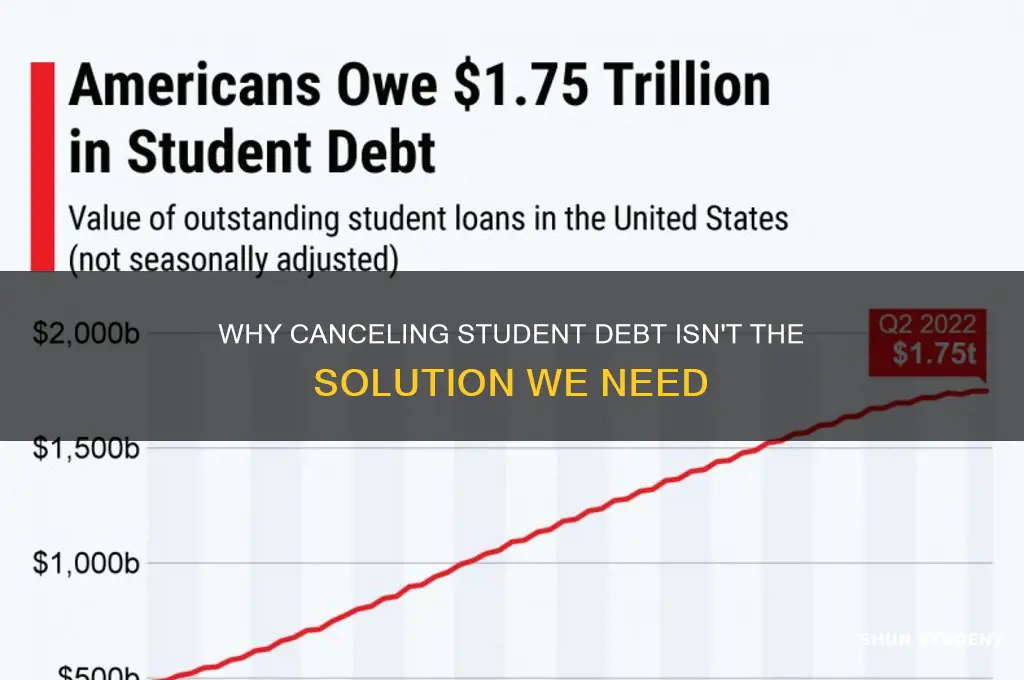

Canceling student debt, while appealing to those burdened by loans, shifts the financial weight onto taxpayers, many of whom never attended college or have already paid off their debts. This redistribution of costs raises ethical questions about fairness. For instance, a 45-year-old tradesman who skipped higher education to enter the workforce early could see his federal tax rate increase by 2-3% to fund debt forgiveness. Similarly, retirees living on fixed incomes might face reduced Social Security benefits as federal budgets tighten. This scenario underscores how debt cancellation, though targeted, creates a ripple effect that penalizes those who made different life choices or sacrificed to avoid debt.

Consider the mechanics of funding such a policy. A one-time cancellation of $1 trillion in student debt would require reallocating funds from existing federal programs or increasing taxes. For perspective, the IRS estimates that closing the tax gap (unpaid taxes) could generate $400 billion annually, but even this falls short. To cover the shortfall, the government might slash infrastructure spending, delay healthcare reforms, or raise income taxes across the board. A family earning $75,000 annually could see their tax liability rise by $1,200 per year—a regressive outcome that disproportionately affects middle-income households. Such trade-offs highlight the hidden costs of what appears to be a benevolent policy.

Proponents argue that debt cancellation stimulates the economy by freeing up disposable income for spending. However, this overlooks the crowding-out effect on federal budgets. Every dollar allocated to debt forgiveness is a dollar diverted from other economic priorities. For example, reducing student debt might boost consumer spending by $100 billion annually, but this pales in comparison to the $1.2 trillion infrastructure bill, which creates jobs and improves long-term productivity. By prioritizing debt cancellation, policymakers risk sacrificing investments in education, renewable energy, and public health—sectors that yield higher economic returns over time.

Finally, the inflationary pressure of debt cancellation cannot be ignored. Injecting trillions into the economy without corresponding productivity gains risks devaluing the currency. Historical precedents, such as the 2008 bank bailouts, show that large-scale debt forgiveness often leads to temporary economic relief followed by prolonged stagnation. To mitigate this, policymakers could explore targeted solutions, such as income-driven repayment plans or refinancing options, which address affordability without straining federal budgets. Such measures would balance relief for borrowers with fiscal responsibility, ensuring that the economic burden is shared equitably.

Forgiving Student Loans: Economic Impact and Inflationary Pressures Explained

You may want to see also

Explore related products

![]()

Moral Hazard: Forgiveness could discourage personal responsibility and future prudent financial decision-making

Student loan forgiveness, while seemingly compassionate, risks creating a moral hazard by undermining personal accountability. When individuals anticipate that their debts might be erased, they may make riskier financial decisions, assuming a safety net exists. For instance, a prospective student might choose a more expensive private university over a more affordable public one, reasoning that future forgiveness could absolve them of the burden. This behavior not only shifts the cost to taxpayers but also distorts the incentive to weigh costs and benefits carefully before committing to substantial loans.

Consider the analogy of car insurance: if drivers knew their premiums would cover reckless behavior without consequence, they might drive more dangerously. Similarly, blanket student debt forgiveness could signal that financial irresponsibility carries no long-term repercussions. This could encourage future borrowers to overextend themselves, assuming society will bail them out. For example, a borrower might pursue a low-paying degree in a field with limited job prospects, knowing that forgiveness could later alleviate their debt. Such decisions, while individually rational, collectively strain public resources and devalue the principle of financial prudence.

To mitigate this moral hazard, policymakers could implement targeted relief rather than broad forgiveness. For instance, income-driven repayment plans or loan forgiveness tied to public service ensure that relief is directed toward those who genuinely need it, rather than rewarding indiscriminate borrowing. Additionally, financial literacy programs in high schools and colleges could empower students to make informed decisions about loans, emphasizing the long-term consequences of debt. By combining targeted relief with education, society can address hardship without fostering dependency.

Ultimately, the moral hazard of student debt forgiveness lies in its potential to erode the connection between choices and consequences. While alleviating the burden for those in dire straits is justifiable, indiscriminate forgiveness risks normalizing the idea that debts are optional obligations. This could lead to a cycle where future generations borrow without restraint, expecting society to foot the bill. Striking a balance between compassion and accountability is essential to preserving both individual responsibility and the sustainability of financial systems.

Can States Tax Student Loan Forgiveness? What Borrowers Need to Know

You may want to see also

Explore related products

![]()

Inequality Concerns: Benefits higher-income graduates more, widening wealth gaps instead of aiding the poorest

Student debt forgiveness, while seemingly equitable, often disproportionately benefits higher-income graduates, exacerbating existing wealth inequalities. Consider this: graduates from elite institutions, who typically earn higher salaries, carry larger debt loads due to costlier tuition. Forgiveness programs, which often cap relief at a fixed amount, provide these individuals with a larger absolute benefit compared to lower-income graduates from less expensive schools. For instance, a graduate with $100,000 in debt from a private university stands to gain more from a $50,000 forgiveness program than a community college graduate with $20,000 in debt. This dynamic effectively subsidizes the wealthier segment of borrowers, widening the wealth gap rather than closing it.

To illustrate, let’s break down the numbers. A higher-income graduate earning $80,000 annually with $80,000 in debt might see their monthly payments reduced by $400 through forgiveness. In contrast, a lower-income graduate earning $30,000 annually with $15,000 in debt might only save $100 monthly. Over time, the wealthier graduate accumulates significantly more disposable income, which can be invested in assets like homes or stocks, further accelerating their financial advantage. Meanwhile, the lower-income graduate, despite receiving some relief, remains financially constrained, with limited opportunities to build wealth.

A persuasive argument against blanket forgiveness lies in its failure to address the root causes of inequality. Instead of aiding the poorest, such policies often overlook systemic issues like underfunded public education and wage stagnation. For example, a low-income student who avoids debt by forgoing college altogether is left entirely unsupported by debt forgiveness programs. These individuals, who might benefit most from targeted investments in job training or affordable education, are effectively bypassed in favor of a policy that rewards those who have already accessed higher education.

Comparatively, alternative solutions like income-driven repayment plans or expanded Pell Grants offer more equitable outcomes. Income-driven plans adjust payments based on earnings, ensuring that lower-income graduates pay less regardless of debt amount. Pell Grants, on the other hand, provide upfront financial aid to the neediest students, reducing their reliance on loans. These approaches directly target financial disparities, unlike blanket forgiveness, which inadvertently favors those who are already better off.

In conclusion, while the intent behind student debt forgiveness is commendable, its execution often perpetuates inequality. By disproportionately benefiting higher-income graduates, such policies fail to address the systemic barriers faced by the poorest individuals. To truly bridge the wealth gap, policymakers must prioritize targeted, equitable solutions that support those most in need, rather than reinforcing existing financial advantages.

Can UoFP Students Get Loan Forgiveness? Eligibility Explained

You may want to see also

Explore related products

$4.99 $15.95

![]()

Alternative Solutions: Investing in affordable education or income-driven repayment plans may be fairer

Student debt forgiveness, while appealing to some, raises concerns about fairness and long-term economic impact. Instead of broad cancellations, consider this: investing in affordable education and expanding income-driven repayment plans could address the root causes of the crisis while promoting personal responsibility.

Step 1: Cap Tuition and Increase Public Funding

Universities often raise tuition unchecked, knowing students will borrow to cover costs. Governments can intervene by capping tuition increases at public institutions and tying them to inflation. Simultaneously, increasing state and federal funding for higher education reduces reliance on student loans. For example, Germany and Norway offer tuition-free public education, demonstrating that affordability is achievable with proper investment.

Step 2: Expand Income-Driven Repayment Plans

Income-driven repayment (IDR) plans adjust monthly payments based on earnings, capping them at a percentage of discretionary income (typically 10-20%). These plans already exist but are underutilized due to complexity and lack of awareness. Simplifying enrollment processes and automatically enrolling eligible borrowers could ensure more graduates benefit. For instance, a borrower earning $40,000 annually might pay $300/month, while someone earning $25,000 could pay $0 until their income rises.

Caution: Avoid Moral Hazard

While affordability and IDR plans address systemic issues, they must be paired with incentives for responsible borrowing. Requiring financial literacy courses for loan recipients and limiting borrowing to a percentage of expected post-graduation income can prevent over-borrowing. For example, a student pursuing a degree in early childhood education, with an average starting salary of $35,000, should not be able to borrow $100,000 without additional scrutiny.

Forgiving student debt without addressing underlying issues risks perpetuating the cycle of debt. By investing in affordable education and expanding income-driven repayment plans, policymakers can create a fairer system that rewards personal responsibility while ensuring access to higher education. This approach not only alleviates financial strain on graduates but also fosters a more sustainable economic future.

Student Loan Forgiveness: Impact on Credit Scores and Financial Health

You may want to see also

Explore related products

![]()

Political Backlash: Debt forgiveness risks alienating taxpayers, sparking divisive political and social reactions

Student debt forgiveness, while appealing to borrowers, carries a political risk that cannot be ignored: alienating taxpayers who perceive the policy as an unfair redistribution of wealth. Consider the 2022 Biden administration’s proposal to cancel up to $20,000 in student debt, which faced immediate backlash from critics arguing it unfairly burdened those who paid their debts or chose not to attend college. Polls revealed a stark divide: while 59% of Democrats supported the plan, only 17% of Republicans did, highlighting how such policies can deepen partisan fractures. This reaction underscores a broader concern—taxpayers, particularly those without college degrees, may view debt forgiveness as a subsidy for individuals who made different life choices, fostering resentment rather than solidarity.

To mitigate this backlash, policymakers must address the perceived inequity head-on. One strategy is to frame debt forgiveness as a targeted intervention rather than a blanket giveaway. For instance, limiting eligibility to borrowers earning below a certain income threshold or those in public service roles could reduce the impression of indiscriminate favoritism. Additionally, pairing forgiveness with broader reforms, such as lowering college costs or expanding vocational training, could shift the narrative from individual relief to systemic improvement. Without such nuance, the policy risks becoming a political lightning rod, amplifying divisions rather than resolving them.

The social implications of debt forgiveness further complicate its political viability. For many, student debt is a symbol of personal responsibility, and forgiving it can be seen as undermining this value. Take the case of a 45-year-old taxpayer who worked multiple jobs to pay off their loans—they might view forgiveness as a reward for those who deferred responsibility. This perception can fuel narratives of generational or class conflict, pitting younger borrowers against older taxpayers or blue-collar workers against college graduates. Such divisions are not merely rhetorical; they can manifest in protests, legal challenges, and electoral consequences, as seen in the lawsuits that halted Biden’s debt relief plan in 2022.

A comparative analysis of similar policies abroad offers cautionary lessons. In the UK, the introduction of tuition fees in the 1990s led to widespread student debt, but proposals for forgiveness have been met with skepticism due to concerns about fairness and fiscal sustainability. Germany, by contrast, has avoided such backlash by offering tuition-free education, eliminating the need for debt forgiveness altogether. These examples suggest that addressing the root causes of debt—high tuition costs and limited funding—may be more politically sustainable than forgiving existing debt. For U.S. policymakers, this implies that investing in affordable education could preempt the need for forgiveness while avoiding its divisive aftermath.

Ultimately, the political backlash against student debt forgiveness is not just about economics—it’s about values and identity. To navigate this minefield, policymakers must balance empathy for borrowers with respect for taxpayers’ concerns. Practical steps include transparent communication about the policy’s goals, phased implementation to gauge public reaction, and complementary measures to address broader educational inequities. Without such care, debt forgiveness risks becoming a wedge issue, exacerbating social divisions rather than alleviating financial burdens. The challenge lies in crafting a solution that acknowledges shared sacrifices while fostering a sense of collective progress.

Do Nelnet Loans Qualify for Student Loan Forgiveness? What You Need to Know

You may want to see also

Frequently asked questions

Forgiving student debt could create moral hazard, discouraging future borrowers from responsibly managing their loans, and unfairly burden taxpayers who did not attend college or have already paid off their debts.

While debt forgiveness might provide temporary relief, it does not address the root causes of rising tuition costs or ensure long-term economic stability. Targeted investments in education affordability and wage growth may be more effective.

Debt forgiveness benefits all borrowers, including high-income earners, and may not effectively target those most in need. Alternative solutions like income-driven repayment plans or Pell grant expansions could better support low-income students.

While it may alleviate stress for some, it does not solve systemic issues in higher education funding. It could also lead to resentment from those who sacrificed to pay off their loans or chose not to pursue college due to cost concerns.

![Unforgiven / Outlaw Josey Wales [Blu-ray]](https://m.media-amazon.com/images/I/81O9IZmvu3L._AC_UY218_.jpg)

![LE SSERAFIM - 1st Studio Album UNFORGIVEN [COMPACT ver.] (HONG EUNCHAE ver.)](https://m.media-amazon.com/images/I/51uMxk08pGL._AC_UY218_.jpg)