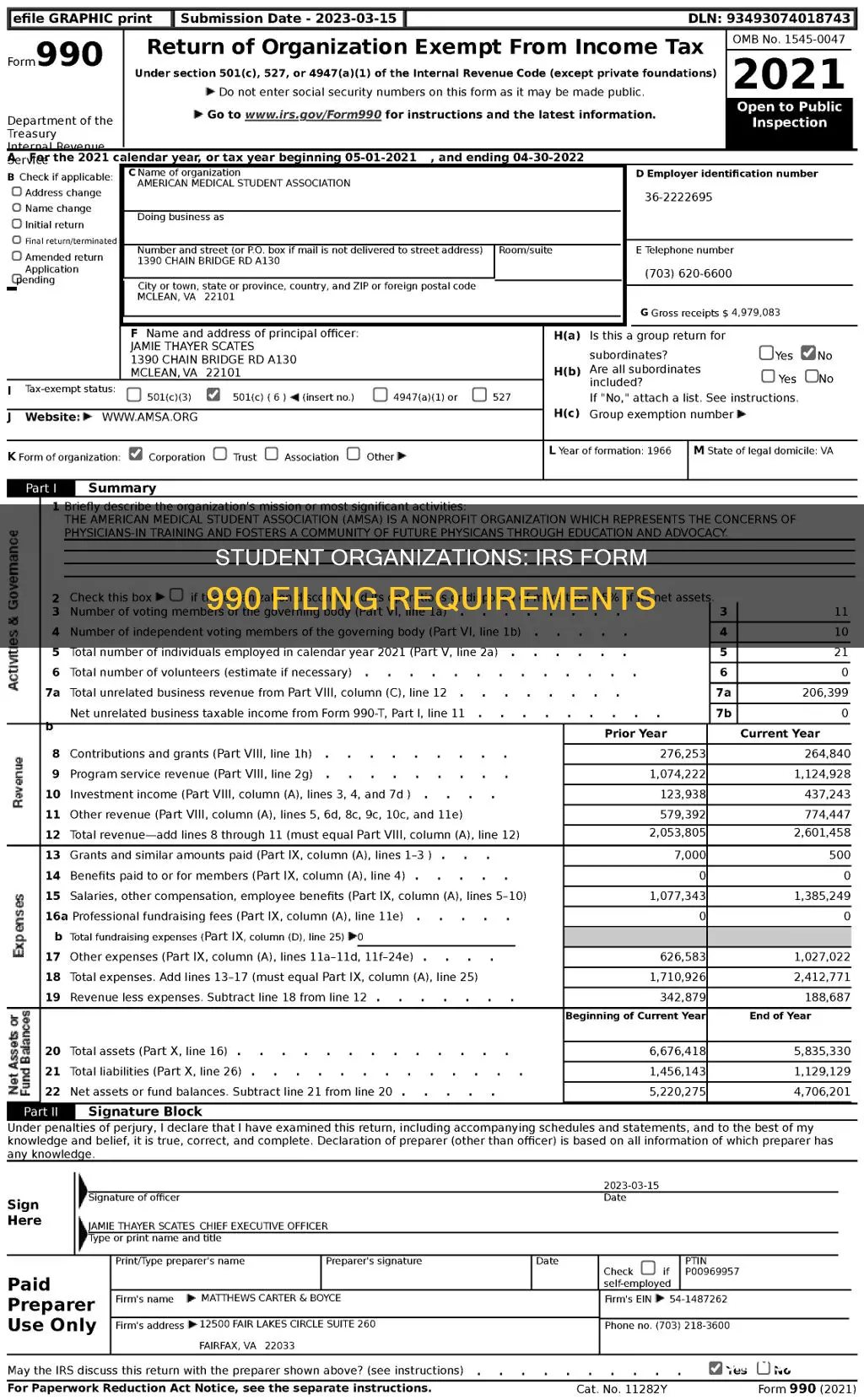

Form 990 is a document that tax-exempt organizations must submit to the IRS. It provides an overview of the organization's activities, including program information, financial activities, and compensation to key executives. While Form 990 is typically associated with tax-exempt colleges and universities, it is not exclusively for educational institutions. State institutions are exempt from filing Form 990. However, it is unclear whether state university student organizations are classified as state institutions in this context. Therefore, it is important to refer to the specific guidelines provided by the IRS to determine if state university student organizations are required to file Form 990 or if they fall under any exemptions.

| Characteristics | Values |

|---|---|

| Who has to file Form 990? | All tax-exempt higher education institutions |

| What is the purpose of the form? | Enable the IRS and the public to evaluate whether tax-exempt colleges and universities are complying with the requirements to maintain their exempt status |

| What does the form contain? | Program information, financial activities, compensation to key executives, and qualifications as a tax-exempt school |

| When is the deadline for filing? | The 15th day of the 5th month after the tax period ends |

| What is Form 990-N? | An electronic notice for small tax-exempt organizations with gross receipts of $50,000 or less |

| Are there any exceptions to filing Form 990? | Yes, churches, state institutions, and subsidiary organizations covered under a group return |

Explore related products

What You'll Learn

![]()

Student organisations as tax-exempt organisations

Student organizations are an integral part of university life, offering students opportunities for personal growth, leadership, and community building. These organizations often engage in a variety of activities, from academic pursuits to social events and charitable initiatives. As they are often involved in financial transactions and may receive donations or generate income, it is important to understand their tax obligations and exemptions.

In the United States, the Internal Revenue Service (IRS) requires most tax-exempt organizations to file Form 990 annually to maintain their tax-exempt status. This form is a comprehensive disclosure that provides an overview of the organization's activities, financial transactions, and compliance with tax-exempt requirements. While student organizations are not specifically mentioned, understanding their tax obligations is crucial.

Firstly, it is important to note that the IRS defines "school" as an educational organization that maintains a regular facility and curriculum and regularly enrolls students. This definition likely includes universities and colleges, which are considered higher education institutions. Therefore, the IRS's requirements for schools and higher education institutions may apply to student organizations operating under the umbrella of these institutions.

Now, let's discuss the tax-exempt status of student organizations and their potential requirements for filing Form 990. Most tax-exempt organizations, including those under Section 501(c)(3), are required to file Form 990, 990-EZ, or 990-N annually. Section 501(c)(3) organizations are considered charitable organizations and are typically eligible for tax-exempt status. This could include student organizations engaged in charitable activities, such as providing scholarships, disaster relief, or other community services. However, to obtain and maintain this tax-exempt status, these student organizations must comply with specific requirements.

Student organizations operating as tax-exempt organizations under the umbrella of a university or college should consult with their institution's financial or legal advisors to determine their specific obligations. They should also stay informed about any updates or changes to IRS requirements, as non-compliance could result in penalties or loss of tax-exempt status. Additionally, while Form 990 is a critical disclosure for tax-exempt organizations, it can also raise complex issues regarding executive compensation, conflicts of interest, and financial activities. Therefore, student organizations should carefully review and prepare their Form 990 to address any potential concerns proactively.

Chicago Scholarships: International Students' Opportunities

You may want to see also

Explore related products

![]()

State university student organisations and donor information

State university student organizations and donor information are important aspects of a university's operations and finances. Universities and colleges are under constant public scrutiny, and maintaining transparency is essential. Form 990, an IRS form for tax-exempt organizations, is a critical tool in this regard. While it is dense and time-consuming to review, it offers valuable insights into the institution's activities, financial dealings, and compliance with tax-exemption requirements.

State universities, as tax-exempt institutions, are generally required to file Form 990 annually to maintain their tax-exempt status. This form provides an overview of their activities, including program information, financial activities, and compensation to key executives. However, it's important to note that state institutions are exempt from filing Form 990. Instead, they may fall under the category of "state institutions" which are not required to file this form.

The donor information in Form 990 is particularly sensitive. While the donors' names and addresses listed on the form are usually redacted before being made public, certain donors to private foundations and Section 527 political organizations are publicly disclosed. This can include donors to student organizations, depending on their tax status and structure. Student organizations that are set up as private foundations or political organizations under Section 527 would disclose donor information, while those structured differently may not.

Additionally, universities should be mindful of the optics surrounding executive compensation. Deferred compensation, bonuses, and incentives can sometimes create a perception of excessive compensation, even if that is not the case. Therefore, it is crucial for universities to be transparent and provide clear explanations for such compensation packages.

In conclusion, state university student organizations may not be required to file Form 990, depending on their specific structure and tax status. However, if they are set up as private foundations or political organizations, they will need to disclose donor information. Universities should also be aware of the public perception of their financial activities and executive compensation practices, as Form 990 is accessible to prospective and current students, alumni, staff, and the media.

Applying to Oxford: A Guide for US Students

You may want to see also

Explore related products

![]()

Student organisations and executive compensation

Student organizations that are considered tax-exempt are required to file Form 990 annually to maintain compliance with IRS requirements. This includes state university student organizations that meet the requirements of IRS section 501(c)(3), which defines charitable organizations. These organizations must report their annual activities, including program information, financial activities, and compensation to key executives.

Schedule J of Form 990 specifically addresses executive compensation. It requires the disclosure of compensation paid to certain individuals, such as officers, directors, trustees, key employees, and the highest-compensated employees. This includes compensation paid by related organizations and deferred compensation, which can create a perception of higher compensation if not properly presented.

Student organizations should carefully review Schedule J and other sensitive sections of Form 990, as the information is accessible to the public and media. This can help them avoid surprises and address any issues that may arise. The form also covers bonuses and incentive compensation, which are used by educational institutions to attract top talent.

The deadline for filing Form 990 is the 15th day of the 5th month after the tax period ends, and extensions are available for Form 990 and 990-EZ filers. However, state institutions are exempt from filing Form 990, and smaller organizations with gross receipts of $50,000 or less may file Form 990-N instead.

Overall, while student organizations at state universities may not need to file Form 990, those that are tax-exempt must comply with IRS requirements by disclosing executive compensation and other financial information to maintain their tax-exempt status and transparency with students, alumni, and the public.

Michigan's University Student Population: A Comprehensive Overview

You may want to see also

Explore related products

![]()

Student organisations and conflicts of interest

Student organizations at state universities do not have to file Form 990 with the IRS as they are considered state institutions and are therefore exempt from this requirement. Form 990 is an annual information return that must be filed by tax-exempt organizations, including charitable organizations and private foundations. However, state institutions, churches, and most faith-based organizations are exempt from filing this form.

While student organizations at state universities are exempt from filing Form 990, it is important for them to be mindful of potential conflicts of interest that may arise in their financial activities. Conflicts of interest in student organizations can occur when the personal or financial interests of individuals or entities involved in the organization are at odds with the best interests of the group as a whole. To maintain the integrity of the student organization and ensure that decisions are made in the best interest of all members, it is crucial to identify and address these conflicts effectively.

One common area where conflicts of interest may arise is in fundraising activities. Student organizations often rely on donations and sponsorships to support their initiatives and events. When seeking financial support, it is important for the organization to ensure that the sources of funding do not compromise the group's values, mission, or independence. For example, accepting donations from a company that conflicts with the organization's values or objectives could create a conflict of interest. To mitigate this, student organizations should have clear guidelines for accepting donations, including criteria for evaluating potential donors and ensuring transparency in the decision-making process.

Another area of potential conflict is when members of the student organization have personal financial interests that may influence their decisions or actions within the group. For instance, if a member of the organization's executive board owns a business that could benefit from a contract the organization is awarding, this creates a conflict of interest. In such cases, the member should disclose their financial interest and recuse themselves from any discussions or votes related to that particular decision. Establishing a code of conduct that outlines expectations for disclosing and managing personal financial interests can help prevent such conflicts from compromising the integrity of the student organization.

Additionally, conflicts of interest can arise when student organizations collaborate with external partners or seek sponsorship for events. In these situations, it is important for the student organization to ensure that the partnership or sponsorship does not compromise the group's independence or mission. Student organizations should carefully evaluate potential partners to ensure that their values and objectives are aligned. Clear guidelines for vetting and selecting partners, as well as transparent reporting of any financial benefits received from sponsorships, can help maintain the trust of the student body and the university community.

To effectively manage conflicts of interest, student organizations should establish clear policies and procedures. This includes regular disclosure of any potential conflicts, both financial and non-financial, by all members. Additionally, the organization should have a process for reviewing and resolving these disclosures, such as an ethics committee or an independent advisor. By proactively addressing conflicts of interest, student organizations can maintain their integrity, transparency, and accountability, ensuring that their decisions and activities align with the best interests of the entire group.

Kutztown University Students: Accessing Office 365

You may want to see also

Explore related products

$17

![]()

Student organisations and tax-exemption status

Student organizations in state universities do not need to file Form 990 as they are considered state institutions. However, if a student organization wishes to apply for tax-exempt status, it must meet the requirements of the IRS's charitable organizations definition under section 501(c)(3). This includes operating with a racially nondiscriminatory policy and maintaining a regular facility, curriculum, and enrolled students.

Once an organization has obtained tax-exempt status, it must file Form 990 annually to maintain its status. This form is due by the 15th day of the 5th month after the tax period ends and can be filed with the help of an IRS-authorized e-file provider. Form 990 requires organizations to disclose detailed information, including program information, financial activities, and compensation to key executives.

It is important to note that Form 990 is accessible to the public and the media, which can create scrutiny for the organization. As such, it is crucial to carefully review the form before submission and be prepared to address any issues that may arise.

For smaller organizations with gross receipts of $50,000 or less, Form 990-N, also known as the e-Postcard, is a simpler alternative. This form is an electronic return that covers eight questions and does not require extensions. However, for organizations with larger gross receipts, Form 990 or Form 990-EZ must be filed, and extensions of up to 90 days are available.

In summary, while student organizations in state universities are not required to file Form 990, those seeking tax-exempt status must meet specific IRS criteria and file the necessary forms to obtain and maintain their exempt status.

Foreign Students Thriving at Oxford University

You may want to see also

Frequently asked questions

State universities are exempt from filing Form 990. However, tax-exempt higher education institutions are required to file Form 990 to maintain their tax-exempt status.

Form 990 is a document that tax-exempt organizations must file with the IRS. It provides an overview of the organization's activities, including program information, financial activities, and compensation to key executives.

There is no single deadline for filing Form 990. The due date is the 15th day of the 5th month after the tax period ends. Organizations can also receive extensions of up to 90 days for filing.

Form 990 contains a lot of detailed information. Some important sections to focus on include Schedule J (executive compensation), Schedule L (conflicts of interest), and the presentation of financial information.