Being a university student does not make you ineligible for Obamacare. In fact, Obamacare, or the Affordable Care Act (ACA), has improved health insurance options for students. Before the ACA, student health coverage was inconsistent, and eligibility to remain on a parent's health plan was often contingent on being enrolled in school full-time. Now, young adults can remain on their parents' health plans until the age of 26, regardless of their enrollment status or tax dependency. Additionally, the ACA expanded Medicaid, making it a viable option for students with low incomes. While most university health plans are now regulated by the ACA, students also have the option to purchase ACA-compliant insurance through the Marketplace. International students, however, are generally exempt from the ACA and must purchase private insurance that meets their university's requirements.

| Characteristics | Values |

|---|---|

| Student health insurance plans | Many universities offer student health insurance plans, which are regulated by the ACA and cover the ten essential health benefits. |

| ACA eligibility for students | Students can remain on their parents' ACA plans until age 26, regardless of their enrolment status, tax dependency, or employer-provided coverage. |

| Student health plan considerations | Students should consider their parents' insurance coverage network, especially if their school is far from their parents' home, as out-of-state coverage may be limited to emergency services. |

| International students | International students on F1 or J1 visas are not subject to ACA compliance and are not eligible for ACA plans. They can purchase private insurance or ACA-compliant university plans. |

| Cost assistance | Students may qualify for cost assistance through Marketplace tax credits or Medicaid, depending on their income level and tax filing status. |

Explore related products

$82.51 $92.95

$81.51 $92.95

What You'll Learn

![]()

University students can remain on their parents' health insurance plans

Before the Affordable Care Act (ACA), also known as Obamacare, health coverage for college students was often dependent on their enrolment status and age. Many students relied on their parents' health insurance plans, which was often contingent on being enrolled full-time, with a cut-off age of 22 or 26.

However, the ACA has made significant changes, allowing young adults to remain on their parents' health insurance plans until they turn 26, regardless of their enrolment status, tax dependency, or offers of coverage from employers. This provision ensures that students can maintain health coverage under their parents' plans, even if they graduate or are no longer full-time students.

It's important to note that this rule applies to all individual market plans and employer-sponsored plans. Additionally, students can still benefit from cost assistance and coverage under the ACA. They can explore options like the Marketplace, Medicaid, school health plans, or catastrophic plans.

While most university health plans are now regulated by the ACA, providing essential health benefits, students should be aware that not all plans marketed to students are considered "student health plans" under the law. For example, short-term policies or self-insured plans offered by universities may not be ACA-compliant.

International students studying in the US on visas are generally exempt from ACA requirements and can purchase private insurance or university-compliant plans.

Full Sail University's Undergrad Student Population

You may want to see also

Explore related products

$117.19 $245.95

![]()

Students can purchase their own health insurance through Obamacare

University health plans are now typically regulated by the ACA, covering the ten essential health benefits with no annual or lifetime benefit maximums. However, not all plans marketed to students are considered "student health plans" under the ACA. For example, short-term policies or self-insured plans offered by universities may not be ACA-compliant. Therefore, students should carefully review their university's health plan to ensure it meets their needs.

Students who wish to purchase their own health insurance can explore the Obamacare exchanges, which offer a range of plans with different coverage options and costs. Obamacare provides guaranteed-issue coverage, meaning individuals cannot be denied coverage or charged more due to pre-existing medical conditions. Additionally, Obamacare offers subsidies and tax credits for eligible individuals to make premiums more affordable, especially for low and middle-income enrollees.

When considering purchasing their own health insurance, students should evaluate their specific needs and budget. They should also be mindful of open enrollment periods to ensure they can apply for cost assistance, change plans, or enrol in a new plan. While students can remain on their parents' health plans until the age of 26, they may find that their parents' insurance network does not adequately cover medical services while they are away at school, especially if they attend university in a different state.

It is important to note that international students on specific visas are generally not required to comply with the ACA and may need to purchase private insurance that meets their university's requirements. Overall, students have the option to purchase their own health insurance through Obamacare, allowing them to access affordable and comprehensive healthcare during their time at university.

Georgetown University's Competitive Application Numbers

You may want to see also

Explore related products

![Life and Health Insurance Study Cards: Life Health Insurance License Exam Prep with Practice Test Questions [Full Color]](https://m.media-amazon.com/images/I/51Pox87Z5lL._AC_UY218_.jpg)

![]()

Student health insurance plans are regulated by the ACA

Before the Affordable Care Act (ACA), health coverage for college students was inconsistent. Many universities now offer student health insurance plans, and in almost all cases, these plans are regulated by the ACA. This means they cover the ten essential health benefits, including preventive care, hospitalization, prescription drugs, mental health, and maternity, with no annual or lifetime benefit maximums.

However, there are some important distinctions to be made. Firstly, not all plans marketed to students are considered "student health plans" by the law. For example, a short-term policy advertised as "perfect for students" would not have to comply with ACA regulations. Secondly, when a school self-insures its student health plan, it is not subject to HHS regulation. In 2012, the HHS confirmed that around 200,000 students were covered under self-insured health plans offered by approximately 30 colleges and universities.

Student health plans are technically considered individual-market coverage but function more like group health plans, with slight variations in regulation. Self-insured student health plans are not subject to ACA regulations unless the school requests HHS certification. If an insurer offers student health plans in a given state and also offers regular individual market coverage in that state, the plans are not combined for rate-setting. University-sponsored student health plans were initially given some leeway in terms of early compliance with the ACA, with lower annual benefit limits and a later deadline to meet MLR requirements.

International students studying in the US on a student visa, such as F1 or J1, are not subject to ACA rules and are therefore not eligible for ACA plans or state insurance marketplace plans. However, after five years of stay in the US, students may become subject to ACA compliance depending on their visa status and the duration of their stay. Some universities may require international students to have US health insurance that complies with ACA standards or their own criteria.

Explore Student Organizations at Chapman University

You may want to see also

Explore related products

$18.23 $29.98

![]()

International students are not eligible for ACA plans

International students are not required to purchase an Affordable Care Act (ACA)-compliant plan, but it is highly recommended that they still purchase health insurance. The ACA is a healthcare reform law that aims to make health insurance more accessible and affordable for US citizens and residents. However, it does not apply to international students studying in the US on a student visa (e.g. F1 or J1 visas). Therefore, international students are not eligible for ACA plans or plans available on each state's insurance marketplace.

International students are considered “non-resident aliens” for tax purposes for the first five years of their stay in the US and are exempt from the ACA mandate. After this initial period, students may be subject to ACA compliance depending on their visa status and the number of years they have lived in the US. During this time, they may need to purchase an ACA-compliant plan or a plan that meets the minimum requirements set by their school or university.

Some of the benefits of an ACA-compliant plan include essential health benefits such as preventive care, hospitalization, prescription drugs, mental health, and maternity care. These plans also have no annual or lifetime limits on coverage and do not deny coverage or charge more based on pre-existing conditions or gender. While ACA-compliant plans offer enhanced coverage, they also come with the drawback of increased costs.

International students can purchase their own student health insurance from private insurance companies that cater specifically to students. These plans are often cheaper than ACA-compliant plans and university health plans while still offering similar coverage. Additionally, some universities may require US health insurance for international students that is compliant with ACA standards or their own criteria. It is important for international students to carefully review the health insurance requirements of their chosen university before enrolling.

Texas University's Student Population: A Comprehensive Overview

You may want to see also

Explore related products

![]()

Students may be eligible for Medicaid

Being a university student does not make you ineligible for Obamacare. In fact, the Affordable Care Act (ACA), also known as Obamacare, has improved health insurance options for students. Firstly, young adults can remain on their parents' health insurance plans until the age of 26, regardless of their student status, dependency status, or whether they have an offer of coverage from their employer.

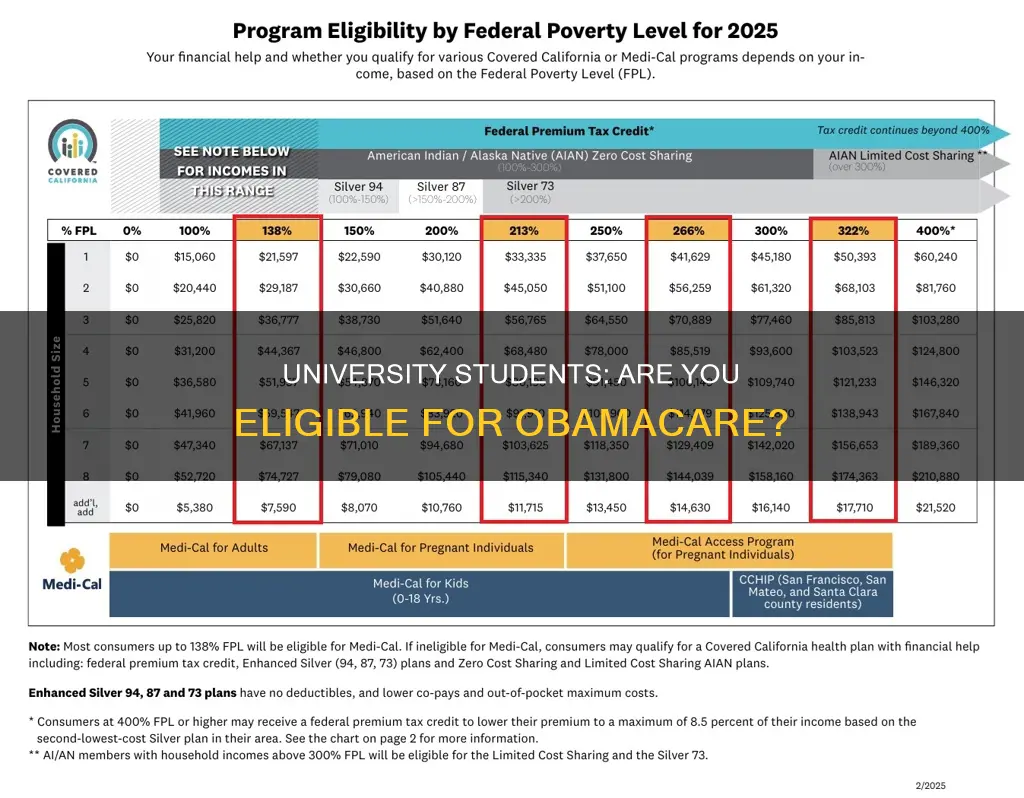

Secondly, the ACA has expanded Medicaid coverage to include more low-income adults. As a college student, it is likely that you meet the income requirements for Medicaid, unless you have a full-time job with a high salary. However, there are a few important things to keep in mind:

- Your parents cannot claim you as a dependent on their tax return if you want to be eligible for Medicaid. Therefore, you must file income taxes on your own in order to qualify.

- You must be a resident of the state where you are receiving Medicaid. If you move to another state for university, this could complicate the application process.

- Only 40 states and the District of Columbia have expanded Medicaid coverage to adults with incomes up to 138% of the poverty level. This is equal to $29,435 for a family of three or $17,609 for an individual as of 2020. Therefore, you should check with your specific state agency to determine your eligibility.

- If your university offers a student health plan, enrolling in it can be an easy and affordable way to get basic insurance coverage. However, it is important to note that not all plans marketed to students are considered "student health plans" under the law, and some may not be ACA-compliant.

Student Status: Institutional Affiliation Explained

You may want to see also

Frequently asked questions

No, being a university student does not make you ineligible for Obamacare. In fact, university students have a number of health plan options, including Obamacare.

University students can choose from a variety of health plans, including:

- The Marketplace

- Medicaid

- School health plans

- Catastrophic plans

- Their parents' plan

Obamacare offers a range of benefits for university students, such as:

- No annual or lifetime limits on coverage.

- Coverage for essential health benefits, such as preventive care, hospitalization, prescription drugs, mental health, and maternity.

- Subsidies or tax credits to help with the cost of premiums.

- The ability to remain on their parents' health insurance plan until the age of 26, regardless of their enrolment status or tax dependency.