Consolidation can significantly impact the eligibility and process of student loan forgiveness, making it a critical consideration for borrowers seeking debt relief. When federal student loans are consolidated, they are combined into a single Direct Consolidation Loan, which simplifies repayment but may reset the clock on forgiveness programs like Public Service Loan Forgiveness (PSLF) or income-driven repayment plans. For instance, consolidating loans can disqualify previously made qualifying payments toward forgiveness, requiring borrowers to start anew. Additionally, certain loan types, such as Perkins Loans, may lose their unique forgiveness benefits when consolidated. While consolidation can offer lower monthly payments or access to additional repayment plans, borrowers must carefully weigh these advantages against potential setbacks in their path to loan forgiveness. Understanding these nuances is essential for making informed decisions that align with long-term financial goals.

| Characteristics | Values |

|---|---|

| Impact on Eligibility for Forgiveness | Consolidation does not inherently disqualify loans from forgiveness programs like PSLF or IDR forgiveness. |

| PSLF (Public Service Loan Forgiveness) | Consolidation resets the payment count toward PSLF, requiring borrowers to start over. |

| Income-Driven Repayment (IDR) Forgiveness | Consolidation resets the qualifying payment count for IDR forgiveness plans. |

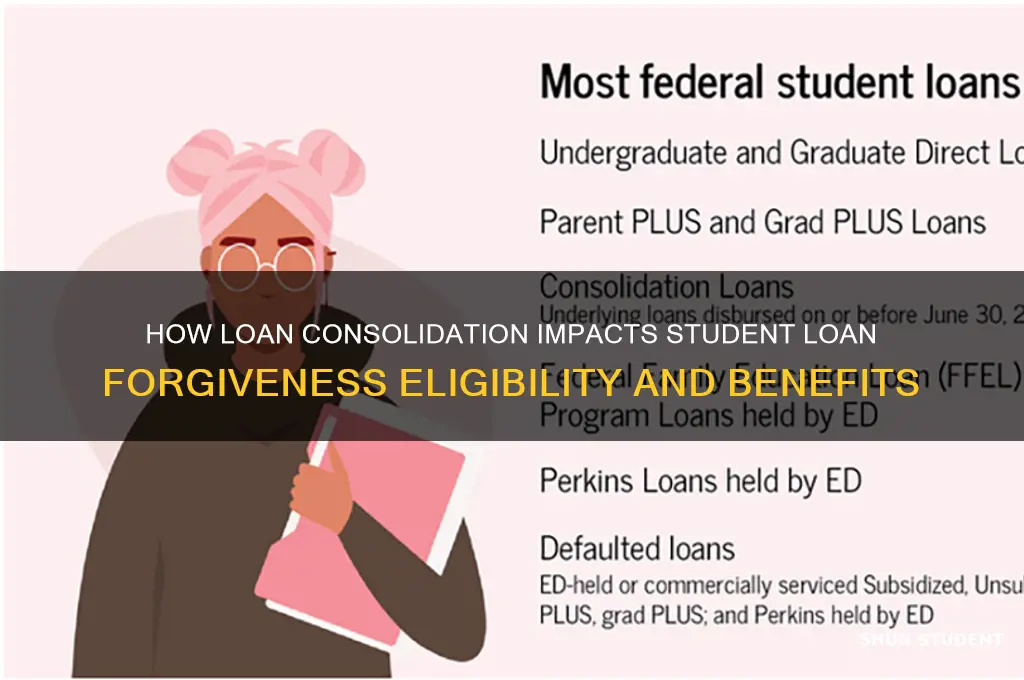

| Federal Loan Types | Only federal loans can be consolidated; private loans are ineligible. |

| Interest Rates | Consolidated loans have a fixed rate based on the weighted average of the original loans, rounded up. |

| Repayment Terms | Consolidation can extend the repayment term, potentially increasing total interest paid. |

| Defaulted Loans | Consolidation can help borrowers exit default and regain eligibility for forgiveness programs. |

| Perkins Loan Cancellation | Consolidating Perkins Loans eliminates eligibility for Perkins Loan cancellation benefits. |

| Parent PLUS Loans | Parent PLUS loans can be consolidated, but only eligible for IDR forgiveness if consolidated under the borrower’s name. |

| Timeframe for Forgiveness | Consolidation may delay forgiveness by resetting payment counts for PSLF or IDR plans. |

| Loan Servicer | Consolidation often changes the loan servicer, which may affect payment processing and forgiveness tracking. |

| Credit Score Impact | Consolidation may temporarily lower credit scores due to a new credit inquiry and account changes. |

| Prepayment Penalties | No prepayment penalties for consolidated federal loans. |

| Eligibility for Other Programs | Consolidated loans remain eligible for programs like deferment, forbearance, and rehabilitation. |

| Application Process | Borrowers must apply through the Federal Student Aid website to consolidate loans. |

| Cost | No application fee for federal loan consolidation. |

Explore related products

What You'll Learn

![]()

Consolidation vs. Refinancing Impact

Consolidation and refinancing are two strategies borrowers use to manage student loan debt, but they have distinct implications for loan forgiveness programs. Consolidation, specifically through a Direct Consolidation Loan, combines multiple federal loans into one, often simplifying repayment. However, it resets the clock on forgiveness timelines for income-driven repayment (IDR) plans, potentially delaying eligibility for Public Service Loan Forgiveness (PSLF) or IDR forgiveness. For example, if a borrower has made 5 years of qualifying payments toward PSLF and consolidates, those payments no longer count toward the 10-year requirement, effectively restarting the forgiveness process.

Refinancing, on the other hand, involves taking out a new private loan to pay off existing federal or private loans, often at a lower interest rate. While refinancing can reduce monthly payments and total interest costs, it disqualifies federal loans from all forgiveness programs, including PSLF and IDR forgiveness. This trade-off is critical for borrowers in public service or those relying on forgiveness as a long-term strategy. For instance, a teacher with $50,000 in federal loans might save $5,000 in interest by refinancing but would forfeit the potential for $30,000 in PSLF after 10 years of service.

To illustrate the impact, consider a borrower with $70,000 in federal loans, split between unsubsidized Stafford and Grad PLUS loans. Consolidating these loans would streamline repayment but reset the PSLF or IDR forgiveness timeline. Refinancing might lower the interest rate from 7% to 5%, saving $7,000 over 10 years, but it would eliminate access to forgiveness programs entirely. The decision hinges on the borrower’s career path, financial stability, and likelihood of qualifying for forgiveness.

Practical tips for navigating this decision include evaluating your eligibility for forgiveness programs before consolidating or refinancing. If pursuing PSLF, avoid refinancing federal loans and consider consolidating only if it simplifies repayment without restarting the forgiveness clock. For those prioritizing lower payments and not relying on forgiveness, refinancing might be advantageous, especially if private loans are included. Always use loan simulators (e.g., the Department of Education’s Loan Simulator) to model outcomes and consult a financial advisor or loan specialist to weigh the long-term consequences.

In summary, consolidation and refinancing serve different purposes and carry unique risks for borrowers seeking loan forgiveness. Consolidation preserves federal benefits but resets forgiveness timelines, while refinancing offers immediate financial relief at the cost of losing access to forgiveness programs. The choice depends on individual circumstances, career goals, and the value of potential forgiveness versus short-term savings. Careful analysis and strategic planning are essential to avoid unintended consequences.

Burger King Student Loan Forgiveness: Step-by-Step Registration Guide

You may want to see also

Explore related products

![]()

Eligibility for Forgiveness Programs

Consolidating student loans can significantly impact eligibility for forgiveness programs, often in ways borrowers might not anticipate. For instance, consolidating Federal Family Education Loans (FFEL) into a Direct Consolidation Loan can make them eligible for Public Service Loan Forgiveness (PSLF), a program originally restricted to Direct Loans. However, this move resets the forgiveness clock, meaning previous qualifying payments no longer count toward the 120 required for PSLF. Borrowers must weigh the trade-off between gaining access to PSLF and losing progress already made.

Income-driven repayment (IDR) forgiveness programs, such as those under the Revised Pay As You Earn (REPAYE) plan, also interact uniquely with consolidation. Consolidating loans can simplify repayment by combining multiple loans into one, but it can disqualify borrowers from IDR forgiveness if the consolidation includes loans that were previously ineligible. For example, Parent PLUS Loans, when consolidated with other Direct Loans, can lose their eligibility for IDR plans unless the borrower consolidates them separately. Understanding these nuances is critical to avoiding unintended consequences.

Another critical factor is the treatment of Perkins Loans in consolidation. Perkins Loans come with their own forgiveness options, including cancellation for teachers, nurses, and other public service roles. Consolidating Perkins Loans into a Direct Consolidation Loan eliminates access to these Perkins-specific forgiveness benefits. Borrowers must decide whether the administrative convenience of consolidation outweighs the loss of these targeted forgiveness opportunities.

Finally, timing plays a pivotal role in consolidation decisions. For borrowers pursuing PSLF, consolidating before submitting the PSLF application can ensure all loans are eligible. However, consolidating after making progress toward PSLF can reset the payment counter, delaying forgiveness. Similarly, borrowers nearing the end of their IDR repayment term should avoid consolidation, as it restarts the clock and extends the time until forgiveness. Strategic timing, coupled with a clear understanding of program rules, can maximize forgiveness potential while minimizing setbacks.

Beware: How Student Loan Forgiveness Scams Target and Exploit Borrowers

You may want to see also

Explore related products

![]()

Payment Count Reset Risks

Consolidating student loans can reset the payment count toward forgiveness, a critical risk borrowers must navigate carefully. For instance, under the Public Service Loan Forgiveness (PSLF) program, borrowers must make 120 qualifying payments. Consolidation restarts this counter, potentially delaying forgiveness by years. Similarly, income-driven repayment (IDR) plans require 240 to 300 payments, and consolidation can nullify progress, especially if prior payments were non-qualifying. This reset is not merely procedural—it directly impacts the timeline and financial burden of achieving forgiveness.

Consider a borrower with 72 PSLF-qualifying payments who consolidates to access a lower interest rate. Post-consolidation, their payment count resets to zero, forcing them to restart the 120-payment journey. This scenario underscores the importance of weighing consolidation benefits against the cost of lost progress. For IDR plans, the reset can be equally detrimental, particularly for borrowers nearing the 20- or 25-year forgiveness mark. A single consolidation decision could add years to their repayment term, increasing total interest paid.

To mitigate reset risks, borrowers should first assess their current payment count and eligibility for forgiveness programs. Tools like the Federal Student Aid website provide payment trackers for PSLF and IDR plans. If consolidation is unavoidable, timing is crucial. For example, consolidating after reaching a significant milestone, such as 10 years of PSLF-qualifying payments, minimizes the impact of a reset. Alternatively, borrowers can explore alternatives like refinancing private loans separately or adjusting repayment plans without consolidation.

A comparative analysis reveals that while consolidation simplifies loan management by combining multiple loans into one, it often sacrifices progress toward forgiveness. For instance, a borrower with both Direct Loans and FFEL Loans might consolidate to qualify for PSLF, but this resets their payment count. In contrast, keeping loans separate and applying for employer certification annually could preserve their progress. This trade-off highlights the need for strategic planning, emphasizing long-term forgiveness goals over short-term convenience.

In conclusion, payment count reset risks are a significant consideration when deciding to consolidate student loans. Borrowers must balance the benefits of consolidation, such as lower monthly payments or access to forgiveness programs, against the potential setback of restarting their payment count. Practical steps include reviewing payment histories, consulting loan servicers, and exploring non-consolidation alternatives. By approaching consolidation with caution and foresight, borrowers can protect their progress toward loan forgiveness and avoid unnecessary delays.

Biden's Student Loan Forgiveness Plan: How It Works and Who Qualifies

You may want to see also

Explore related products

![]()

Income-Driven Repayment Plans

Income-driven repayment (IDR) plans can be a lifeline for borrowers juggling federal student loans, but consolidation often complicates their path to forgiveness. These plans, which cap monthly payments at a percentage of discretionary income (typically 10-20%), offer a structured route to loan forgiveness after 20-25 years of qualifying payments. However, consolidating loans under the Federal Direct Consolidation Loan program resets the payment counter on IDR plans. For instance, if a borrower has already made 5 years of qualifying payments under an IDR plan and then consolidates, their progress toward forgiveness restarts from zero. This reset can delay forgiveness by years, making consolidation a double-edged sword for those prioritizing loan discharge.

Before consolidating, borrowers must weigh the immediate benefits against long-term forgiveness goals. Consolidation can simplify repayment by combining multiple loans into one, potentially lowering monthly payments if paired with an IDR plan. However, this convenience comes at a cost. For example, any unpaid interest on subsidized loans may capitalize upon consolidation, increasing the principal balance. Additionally, consolidating Parent PLUS Loans with other federal loans can make the entire consolidated loan ineligible for certain IDR plans, such as Pay As You Earn (PAYE) or Revised Pay As You Earn (REPAYE). Borrowers should use tools like the Loan Simulator on StudentAid.gov to model outcomes before deciding.

A strategic exception exists for borrowers pursuing Public Service Loan Forgiveness (PSLF). Consolidation can be advantageous if it converts ineligible Federal Family Education Loan (FFEL) or Perkins Loans into Direct Loans, the only type eligible for PSLF. In this case, consolidating early in the repayment process minimizes the impact of resetting the IDR payment counter, as PSLF requires only 120 qualifying payments (10 years) regardless of the repayment plan. However, borrowers must ensure they remain in an IDR plan post-consolidation to maintain eligibility for both PSLF and eventual IDR forgiveness if PSLF is not achieved.

For those not pursuing PSLF, avoiding consolidation until closer to the forgiveness timeline can preserve years of progress under an IDR plan. For example, a borrower with 15 years of qualifying payments on a 20-year forgiveness track could consolidate without losing much ground. Alternatively, borrowers can strategically time consolidation to align with a switch to a more favorable IDR plan, such as moving from Income-Based Repayment (IBR) to REPAYE to take advantage of lower monthly payments or better spousal income treatment. Careful planning and consultation with a loan servicer or financial advisor are essential to navigate these complexities.

Ultimately, consolidation’s impact on IDR forgiveness hinges on individual circumstances and goals. Borrowers must balance the need for immediate payment relief against the long-term pursuit of loan discharge. For some, consolidation may streamline repayment and reduce monthly burdens, while for others, it could derail progress toward forgiveness. Understanding the mechanics of IDR plans, the implications of consolidation, and the interplay with programs like PSLF empowers borrowers to make informed decisions that align with their financial priorities.

Teacher Loan Forgiveness: Can Educators Erase Their Student Debt?

You may want to see also

Explore related products

![]()

Federal vs. Private Loan Rules

Consolidating student loans can significantly impact eligibility for loan forgiveness programs, but the rules diverge sharply between federal and private loans. Federal loans, when consolidated through the government’s Direct Consolidation Loan program, retain access to income-driven repayment (IDR) plans and Public Service Loan Forgiveness (PSLF). For example, if you’ve made 10 years of qualifying payments under an IDR plan, consolidating can reset your payment counter, but it doesn’t disqualify you from eventual forgiveness. Private loans, however, cannot be consolidated into a federal Direct Consolidation Loan, meaning they remain ineligible for federal forgiveness programs. Private consolidation (refinancing) often offers lower interest rates but permanently forfeits access to federal benefits, including forgiveness.

Consider this scenario: A borrower with $30,000 in federal loans under an IDR plan and $20,000 in private loans might be tempted to consolidate all debt for simplicity. Consolidating the federal loans alone preserves forgiveness eligibility, but adding private loans to a private refinance would strip the federal loans of their benefits. The takeaway? Federal consolidation is a strategic tool for managing multiple federal loans, while private consolidation is a trade-off between lower rates and lost forgiveness opportunities.

For borrowers pursuing PSLF, federal consolidation is often necessary to qualify. Only Direct Loans are eligible for PSLF, so consolidating Federal Family Education Loans (FFEL) or Perkins Loans into a Direct Consolidation Loan is a critical step. However, this resets the PSLF payment counter, requiring another 10 years of qualifying payments. Private loans cannot be included in this process, leaving them outside the PSLF framework entirely. This distinction underscores the importance of separating federal and private debt management strategies.

If you’re unsure whether to consolidate, assess your long-term goals. For federal loan holders aiming for forgiveness, consolidation can streamline repayment but requires careful timing to minimize counter resets. For private loan holders, refinancing might reduce monthly payments but eliminates any hope of federal forgiveness. Practical tip: Use the Federal Student Aid website to simulate consolidation outcomes and consult a loan specialist to weigh the pros and cons of each option.

Ultimately, the federal vs. private loan rules in consolidation hinge on preserving or sacrificing access to forgiveness. Federal consolidation is a tactical move within the forgiveness ecosystem, while private consolidation is a financial recalibration outside it. Borrowers must align their consolidation strategy with their forgiveness goals, recognizing that the wrong choice could cost years of progress or thousands in forgivable debt.

Student Loan Forgiveness Canceled: What Borrowers Need to Know Now

You may want to see also

Frequently asked questions

Consolidation can affect eligibility for loan forgiveness programs. For example, consolidating Federal Family Education Loans (FFEL) into a Direct Consolidation Loan may make you eligible for Public Service Loan Forgiveness (PSLF), but it resets your qualifying payment count.

Yes, consolidating your loans typically resets the clock on forgiveness programs like PSLF or income-driven repayment plans, as it combines multiple loans into one new loan with a new repayment term.

Yes, you can qualify for IDR forgiveness after consolidation, but the process restarts. Any payments made before consolidation do not count toward the required 20–25 years for IDR forgiveness.

Private student loans do not qualify for federal forgiveness programs, and consolidating them does not change this. However, refinancing private loans might offer better repayment terms but is separate from consolidation.

If you have FFEL or Perkins Loans, consolidating them into a Direct Consolidation Loan is necessary to qualify for PSLF. However, if you already have Direct Loans, consolidation may not be beneficial, as it resets your payment count.