Student loan forgiveness has been a hot topic in recent years, offering potential relief to millions of borrowers burdened by educational debt. However, a critical question arises for those in financial distress: does student loan forgiveness apply to defaulted loans? Defaulted loans, which occur when borrowers fail to make payments for an extended period, often carry severe consequences, including damaged credit scores and wage garnishments. Understanding whether these loans qualify for forgiveness programs, such as Public Service Loan Forgiveness (PSLF) or income-driven repayment plans, is essential for borrowers seeking a path to financial recovery. While some forgiveness options may be available, eligibility criteria and specific conditions often dictate whether defaulted loans can be included, making it crucial for borrowers to explore their options carefully.

| Characteristics | Values |

|---|---|

| Eligibility for Defaulted Loans | Generally, defaulted loans may qualify for forgiveness under specific programs. |

| Programs Applicable | Public Service Loan Forgiveness (PSLF), Income-Driven Repayment (IDR) Forgiveness, and Total and Permanent Disability (TPD) Discharge. |

| Conditions for PSLF | Must consolidate defaulted loans into a Direct Consolidation Loan and make qualifying payments while in default. |

| Conditions for IDR Forgiveness | Must rehabilitate defaulted loans first, then enroll in an IDR plan and complete the required payment period (20–25 years). |

| TPD Discharge Eligibility | Defaulted loans can be discharged if the borrower qualifies for TPD discharge. |

| Loan Rehabilitation | Required for defaulted loans to regain eligibility for forgiveness programs. Involves making 9 out of 10 consecutive monthly payments. |

| Fresh Start Initiative (2023) | Temporarily allows defaulted borrowers to bring loans back to good standing without full rehabilitation, making them eligible for forgiveness. |

| Tax Implications | Forgiveness of defaulted loans may be taxable depending on the program and circumstances. |

| Private Loans | Defaulted private student loans are generally not eligible for federal forgiveness programs. |

| Timeframe for Forgiveness | Varies by program; PSLF requires 120 qualifying payments, IDR takes 20–25 years, and TPD is immediate upon approval. |

| Impact on Credit Score | Forgiveness may improve credit score after default is removed, but rehabilitation is required first. |

Explore related products

What You'll Learn

![]()

Eligibility for defaulted loans under forgiveness programs

Defaulted student loans complicate eligibility for forgiveness programs, but pathways exist to regain access. The first step is rehabilitation, a process where borrowers make nine on-time, voluntary payments within 10 months. This not only removes the default status but also clears adverse credit reports, making the loan eligible for forgiveness programs like Public Service Loan Forgiveness (PSLF) or income-driven repayment (IDR) plans. Rehabilitation is a one-time opportunity per loan, so borrowers must commit to the process fully.

Another option is consolidation, which combines defaulted loans into a new Direct Consolidation Loan. This immediately lifts the default status, provided borrowers agree to an IDR plan or make three consecutive, on-time payments before consolidation. Consolidated loans become eligible for PSLF and IDR forgiveness, but prior payments toward forgiveness are reset. Borrowers must weigh the trade-off between restarting the forgiveness clock and regaining eligibility.

For those in default, proactive communication with loan servicers is critical. Servicers can guide borrowers through rehabilitation or consolidation and discuss temporary solutions like forbearance or deferment. However, these options pause payments without addressing default, so they’re best used sparingly while pursuing rehabilitation or consolidation. Ignoring defaulted loans only worsens consequences, including wage garnishment and tax refund interception.

Lastly, borrowers should explore forgiveness programs tailored to their circumstances. For example, PSLF requires 120 qualifying payments while working full-time for a government or nonprofit employer. IDR plans like Revised Pay As You Earn (REPAYE) forgive remaining balances after 20–25 years of payments, depending on the plan. Defaulted loans must be rehabilitated or consolidated before these programs apply, but the effort can lead to significant debt relief.

In summary, defaulted loans aren’t automatically disqualified from forgiveness, but borrowers must take specific steps to restore eligibility. Rehabilitation and consolidation are the primary tools, each with unique requirements and implications. By understanding these options and acting decisively, borrowers can navigate default and pursue forgiveness, ultimately regaining financial stability.

Unlock DeVry Student Loan Forgiveness: A Step-by-Step Application Guide

You may want to see also

Explore related products

$9.99 $29.99

![]()

Steps to rehabilitate defaulted loans for forgiveness

Defaulted student loans cast a long shadow, threatening credit scores, wage garnishment, and even Social Security benefits. Yet, rehabilitation offers a path back to financial stability and, crucially, eligibility for loan forgiveness programs. This process, while demanding, is a lifeline for borrowers drowning in debt.

Think of rehabilitation as a structured repayment plan designed to demonstrate your commitment to resolving your debt. It's not a quick fix, but a deliberate journey towards restoring your financial standing.

Step 1: Acknowledge the Problem and Contact Your Loan Holder

The first step is acknowledging the default and taking proactive measures. Contact your loan holder immediately. This could be the Department of Education, a guaranty agency, or a collection agency. Be prepared to discuss your financial situation honestly and explore available options. They will guide you through the rehabilitation process, outlining specific requirements and timelines.

Remember, transparency is key. Hiding from the problem only exacerbates it.

Step 2: Negotiate Affordable Payments

Rehabilitation doesn't mean resuming your original, potentially unsustainable payments. You'll negotiate a new, affordable monthly payment based on your income and expenses. This payment must be made for nine consecutive months to qualify for rehabilitation.

Consider using income-driven repayment calculators to estimate a realistic payment amount. Remember, the goal is to demonstrate consistent, good-faith efforts to repay your debt.

Step 3: Make Timely Payments Religiously

Consistency is paramount. Missing even one payment during the nine-month period can derail the rehabilitation process. Set up automatic payments if possible to ensure timeliness. Treat these payments as non-negotiable, prioritizing them above discretionary spending.

Think of each on-time payment as a brick in the foundation of your financial recovery.

Step 4: Reap the Rewards of Rehabilitation

Successfully completing rehabilitation removes the default from your credit report, significantly improving your credit score. More importantly, it restores your eligibility for loan forgiveness programs like Public Service Loan Forgiveness (PSLF) and income-driven repayment forgiveness.

Rehabilitation is a challenging but transformative process. It requires discipline, honesty, and a commitment to rebuilding your financial future. By taking these steps, you can break free from the shackles of default and pave the way for a brighter financial tomorrow.

Consolidate Student Loans Strategically for Faster Forgiveness: A Guide

You may want to see also

Explore related products

![]()

Impact of default on forgiveness application process

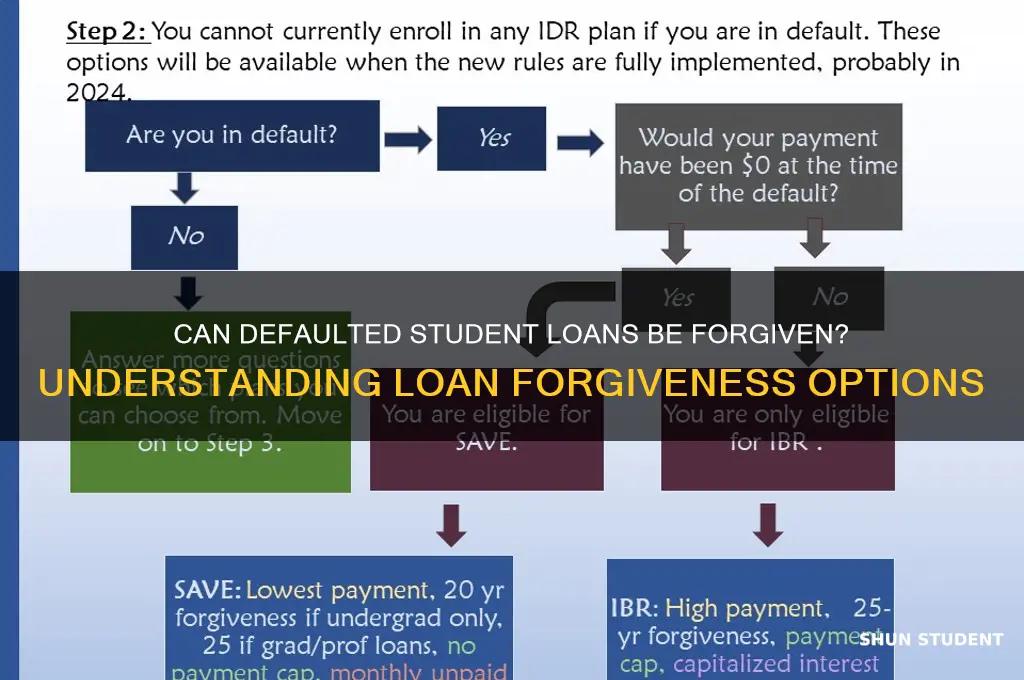

Defaulting on a student loan complicates the forgiveness application process significantly. When a loan is in default, the borrower is no longer in good standing with the lender, which is a fundamental requirement for most forgiveness programs. For instance, Public Service Loan Forgiveness (PSLF) and income-driven repayment (IDR) plans typically mandate that loans be in an active repayment status to qualify. Defaulted loans are ineligible for these programs until they are rehabilitated or consolidated, a process that can take months and requires specific actions from the borrower.

Rehabilitating a defaulted loan is a critical step to regain eligibility for forgiveness programs. This involves making nine out of ten consecutive, on-time monthly payments, as agreed upon with the loan holder. For example, if a borrower’s monthly payment is $200, they must pay this amount consistently for nine months. Once rehabilitated, the default status is removed from the borrower’s credit report, and they can apply for forgiveness programs. However, rehabilitation can only be done once per loan, making it a one-time opportunity to correct the default.

Consolidation is another pathway to resolve default and pursue forgiveness. By consolidating defaulted loans into a Direct Consolidation Loan, borrowers can choose an income-driven repayment plan and restart their journey toward forgiveness. For example, a borrower with $50,000 in defaulted loans could consolidate them, enroll in the Revised Pay As You Earn (REPAYE) plan, and begin making payments as low as 10% of their discretionary income. After 20–25 years of qualifying payments, the remaining balance may be forgiven. However, consolidation resets the clock on forgiveness timelines, which can delay relief.

Defaulted loans also expose borrowers to additional hurdles during the forgiveness application process. Collection agencies may garnish wages, offset tax refunds, or place liens on property, creating financial strain that makes it harder to meet repayment requirements. For instance, if a borrower’s wages are garnished at 15% of their disposable income, they may struggle to afford the rehabilitation payments needed to restore eligibility for forgiveness. This underscores the importance of addressing default promptly to minimize long-term consequences.

In summary, defaulting on a student loan creates significant barriers to accessing forgiveness programs. Borrowers must take proactive steps, such as rehabilitating or consolidating their loans, to restore eligibility. While these processes are time-consuming and require careful planning, they are essential for regaining access to forgiveness opportunities. Understanding these pathways and acting swiftly can help borrowers navigate the complexities of default and work toward financial relief.

Who Qualifies for Student Loan Forgiveness? Eligibility Explained

You may want to see also

Explore related products

![]()

Types of forgiveness available for defaulted loans

Defaulted student loans can feel like a financial anchor, but forgiveness programs offer a lifeline. While not all forgiveness options are created equal, several pathways exist for borrowers in default. Understanding these programs is crucial for navigating the complexities of loan rehabilitation.

Let's delve into the specific types of forgiveness available, examining their eligibility criteria, application processes, and potential benefits.

Public Service Loan Forgiveness (PSLF) stands out as a beacon of hope for defaulted borrowers in public service careers. This program forgives the remaining balance on Direct Loans after 120 qualifying payments while working full-time for a qualifying employer. Crucially, defaulted loans can be consolidated into a Direct Consolidation Loan, making them eligible for PSLF. However, borrowers must first rehabilitate their loans by making nine on-time, voluntary payments within ten months. This rehabilitation period not only opens the door to PSLF but also removes the default status from the borrower's credit report.

Notably, PSLF requires meticulous documentation of employment and payments, making organization and record-keeping paramount.

Income-Driven Repayment (IDR) plans offer another avenue for defaulted loan forgiveness, albeit with a longer timeline. These plans cap monthly payments at a percentage of the borrower's discretionary income, with forgiveness of the remaining balance after 20-25 years of qualifying payments. Defaulted loans can be rehabilitated and enrolled in an IDR plan, allowing borrowers to make affordable payments based on their financial situation. While the forgiveness timeline is longer than PSLF, IDR plans provide immediate relief from unmanageable payments and the potential for eventual debt cancellation. It's important to note that forgiven amounts under IDR may be considered taxable income, requiring careful financial planning.

Borrower Defense to Repayment (BDR) presents a unique forgiveness option for borrowers who were misled or defrauded by their school. If a borrower can demonstrate that their school violated applicable laws or engaged in deceptive practices, they may be eligible for full or partial loan discharge. This option is particularly relevant for borrowers who attended predatory for-profit institutions. The BDR process involves submitting a detailed application and supporting evidence to the Department of Education. While BDR offers the possibility of complete forgiveness, the application process can be lengthy and complex, requiring persistence and thorough documentation.

Total and Permanent Disability (TPD) discharge provides relief for borrowers facing significant physical or mental impairments. Borrowers who are unable to engage in substantial gainful activity due to a disability may qualify for TPD discharge, resulting in the cancellation of their federal student loans. Defaulted loans are eligible for TPD discharge, offering a crucial safety net for borrowers facing long-term disability. The application process involves submitting medical documentation and undergoing a review by the Department of Education. TPD discharge not only eliminates the debt burden but also provides financial stability for borrowers facing challenging circumstances.

Navigating the landscape of defaulted loan forgiveness requires careful consideration of individual circumstances and eligibility criteria. While the process can be complex, understanding the available options empowers borrowers to take control of their financial future. By exploring programs like PSLF, IDR, BDR, and TPD discharge, defaulted borrowers can find a path towards financial freedom and a fresh start.

Leidos Employees: Are You Eligible for Student Loan Forgiveness?

You may want to see also

Explore related products

![]()

Consequences of remaining defaulted during forgiveness review

Remaining in default while your student loan forgiveness application is under review can trigger a cascade of financial and legal repercussions. For instance, defaulted loans are subject to wage garnishment, where up to 15% of your disposable income can be withheld directly from your paycheck. This reduction in take-home pay can severely disrupt your budget, making it harder to cover essential expenses like rent, utilities, and groceries. Additionally, the government can offset your tax refunds and Social Security benefits to collect on the debt, further straining your financial stability. These actions continue unabated until the default is resolved, even if you’re awaiting forgiveness approval.

Another critical consequence is the damage to your credit score. Defaulted loans are reported to credit bureaus, often dropping your score by 100 points or more. This blemish can linger for up to seven years, limiting your ability to secure credit cards, auto loans, or mortgages during that period. Lenders view defaulted borrowers as high-risk, which may result in higher interest rates or outright denials for future financing. Even if your loans are eventually forgiven, the credit damage may already be done, affecting your financial opportunities long-term.

From a legal standpoint, remaining in default exposes you to potential lawsuits by loan holders or collection agencies. Once sued, you could face court judgments that allow creditors to seize assets, such as bank accounts or property, to satisfy the debt. Legal fees and court costs add to the financial burden, compounding the original loan amount. While forgiveness programs aim to alleviate debt, they do not automatically protect you from legal action during the review process. Proactive steps, like consolidating defaulted loans into a new direct loan, can halt collections and lawsuits, but inaction leaves you vulnerable.

Finally, staying in default during the forgiveness review period can delay or even jeopardize your eligibility for relief. Some forgiveness programs, like Public Service Loan Forgiveness (PSLF), require loans to be in good standing. Defaulted loans must first be rehabilitated—a process that involves making nine on-time payments within ten months—before they qualify for forgiveness. Failing to address the default promptly could reset the clock on forgiveness timelines or disqualify you from certain programs altogether. Taking immediate action to resolve default is not just advisable; it’s essential for maximizing your chances of successful loan forgiveness.

Is Interest Forgiven on Student Loans? Understanding Loan Forgiveness Programs

You may want to see also

Frequently asked questions

Yes, certain student loan forgiveness programs, such as Public Service Loan Forgiveness (PSLF) and income-driven repayment (IDR) forgiveness, may apply to defaulted loans after they are rehabilitated or consolidated.

Yes, defaulted loans can qualify for PSLF after they are rehabilitated or consolidated into a Direct Consolidation Loan, and the borrower makes qualifying payments.

The Fresh Start initiative does not forgive defaulted loans but provides a temporary opportunity to rehabilitate them, remove default status, and regain access to forgiveness programs.

Private student loans are not eligible for federal forgiveness programs, even if they are in default. Borrowers may need to negotiate with the lender or explore settlement options.