The Public Service Loan Forgiveness (PSLF) program has been a beacon of hope for many borrowers seeking relief from their student loan debt. Since its inception in 2007, the program has promised to forgive the remaining balance of eligible federal student loans after 120 qualifying payments for those working full-time in public service jobs. However, the question on many minds is: *Has anyone actually had their student loans forgiven through PSLF?* The answer is yes, but the journey to forgiveness has been fraught with challenges, including stringent eligibility requirements, administrative hurdles, and initial low approval rates. Over the years, reforms and improvements have led to more success stories, with thousands of borrowers finally achieving loan forgiveness. Yet, the process remains complex, leaving many to wonder about their own chances of qualifying and the steps needed to ensure their loans are forgiven.

| Characteristics | Values |

|---|---|

| Program Name | Public Service Loan Forgiveness (PSLF) |

| Eligibility Criteria | Must work full-time for a qualifying employer (government or non-profit) |

| Qualifying Payments | 120 qualifying payments (10 years) under an income-driven repayment plan |

| Loan Types Eligible | Direct Loans (other federal loans must be consolidated into Direct Loans) |

| Forgiveness Amount | Remaining loan balance forgiven tax-free |

| Number of Borrowers Approved (2023) | Over 762,000 borrowers have received forgiveness as of October 2023 |

| Total Amount Forgiven (2023) | Over $46 billion in student loan debt forgiven |

| Common Challenges | Incorrect payment counts, ineligible employers, wrong repayment plans |

| Temporary Waivers (Ended Oct 2022) | Allowed past payments on ineligible loans to count toward forgiveness |

| Current Status | Active program with ongoing approvals |

| Notable Success Stories | Teachers, nurses, and government workers among top beneficiaries |

| Average Forgiveness Amount | Approximately $60,000 per borrower (varies widely) |

| Processing Time | Typically 2-3 months after application submission |

| Application Method | Submit PSLF form through Federal Student Aid (FSA) website |

| Recent Updates (2023) | Improved processing times and clearer guidance for borrowers |

Explore related products

What You'll Learn

![]()

PSLF Eligibility Requirements

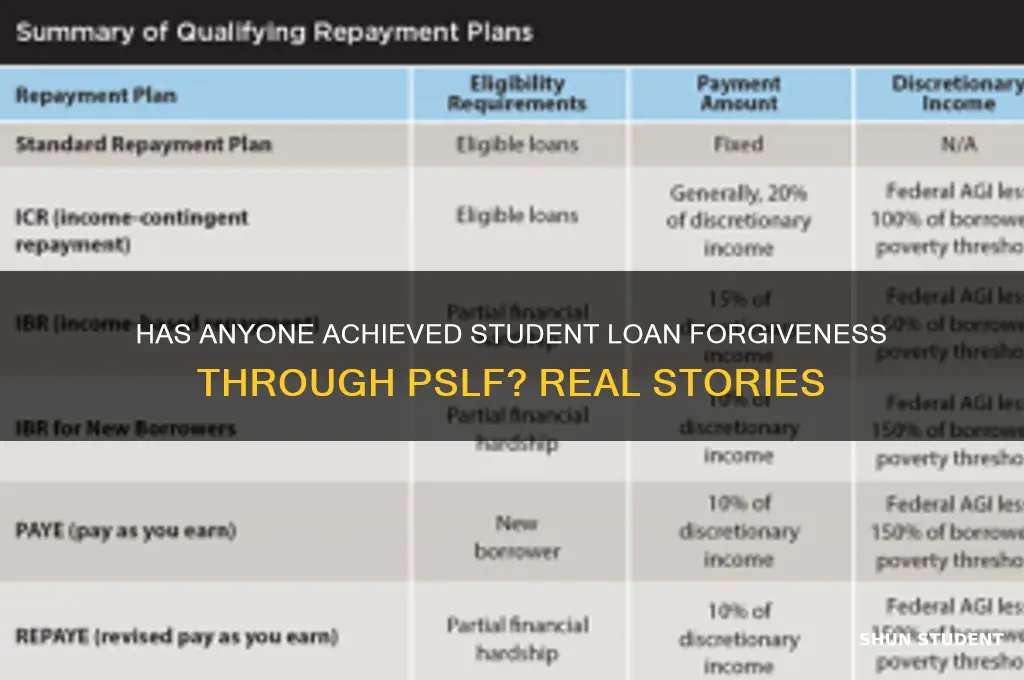

The Public Service Loan Forgiveness (PSLF) program has been a lifeline for many borrowers, but its eligibility requirements are often misunderstood. To qualify, you must make 120 qualifying payments while working full-time for a qualifying employer. These payments must be made under an income-driven repayment plan, which adjusts your monthly payment based on your income and family size. For example, if you earn $40,000 annually and have a family of three, your payment under the Revised Pay As You Earn (REPAYE) plan could be as low as $120 per month, making it easier to manage while working in public service.

Qualifying employers include government organizations at any level (federal, state, local, or tribal), 501(c)(3) nonprofit organizations, and some other types of nonprofits that provide specific public services. It’s crucial to confirm your employer’s eligibility using the Employer Certification Form, as working for a for-profit organization—even in a public service role—does not qualify. For instance, a teacher working at a for-profit charter school would not meet the employer requirement, while one employed by a public school district would.

The type of loan you have also matters. Only Direct Loans are eligible for PSLF. If you have Federal Family Education Loans (FFEL) or Perkins Loans, you must consolidate them into a Direct Consolidation Loan to qualify. Consolidation can reset your payment count, so time this step carefully. For example, if you’ve already made 60 qualifying payments under FFEL, consolidating will restart your count, but it’s necessary to make the remaining 60 payments under the Direct Loan program.

Lastly, payment timing and documentation are critical. Payments must be made on time and in full to qualify. Periods of deferment, forbearance, or default do not count toward the 120 payments. Keep detailed records, including payment stubs and employment certification forms, as the Department of Education may request verification. Borrowers who have successfully received forgiveness often cite meticulous record-keeping as a key factor in their approval. By understanding and adhering to these specific requirements, you can position yourself to join the growing number of individuals who have had their student loans forgiven through PSLF.

Student Loan Forgiveness: What’s in the New Stimulus Bill?

You may want to see also

Explore related products

![]()

Application Process Steps

The Public Service Loan Forgiveness (PSLF) program offers a lifeline to borrowers burdened by student debt, but navigating its application process requires precision and patience. The first critical step is confirming your eligibility, which hinges on making 120 qualifying payments while working full-time for a qualifying employer, such as a government or nonprofit organization. Use the Department of Education’s Employer Qualification Form to verify your employer’s eligibility early in your career to avoid disqualifying payments.

Once eligibility is confirmed, consolidate your loans, if necessary, into a Direct Loan, the only type eligible for PSLF. Submit a consolidation application through StudentLoans.gov, ensuring all non-Direct Loans are included. After consolidation, enroll in an income-driven repayment (IDR) plan to lower monthly payments and align with PSLF requirements. Popular options include REPAYE or PAYE, which cap payments at 10-15% of discretionary income.

Next, submit the Employment Certification Form (ECF) annually or whenever you change employers. This form updates your payment count and confirms ongoing eligibility. While not mandatory, it’s a safeguard against administrative errors and provides peace of mind. Keep copies of all submitted forms and payment records in a dedicated file for future reference.

The final step is submitting the PSLF application after completing 120 qualifying payments. This form is available on the Federal Student Aid website and requires detailed documentation, including payment history and employer certifications. Be prepared for a waiting period of 60-90 days for processing. If approved, your remaining loan balance is forgiven tax-free, marking the culmination of years of dedication to public service.

Caution: Common pitfalls include missing payments, incorrect repayment plans, or employer disqualifications. Regularly review your account on StudentLoans.gov and consult with your loan servicer to address discrepancies promptly. Persistence and attention to detail are key to successfully navigating this transformative program.

Is Edfinancial Forgiving Student Loans? What Borrowers Need to Know

You may want to see also

![]()

Common Rejection Reasons

The Public Service Loan Forgiveness (PSLF) program promises debt relief after a decade of qualifying payments, but many applicants face rejection. Understanding common pitfalls can help borrowers navigate the process more successfully. One frequent issue is ineligible repayment plans. Only income-driven repayment (IDR) plans—such as Income-Based Repayment (IBR), Pay As You Earn (PAYE), or Revised Pay As You Earn (REPAYE)—qualify for PSLF. Borrowers on the Standard Repayment Plan, for instance, may make 120 payments but still fall short because their plan doesn’t meet program requirements. Switching to an IDR plan as early as possible is critical, as payments made under ineligible plans do not count toward forgiveness.

Another major rejection reason is employment certification errors. PSLF requires borrowers to work full-time for a qualifying employer, such as a government or nonprofit organization. However, many applicants fail to submit the Employment Certification Form (ECF) annually or when switching jobs. This oversight can lead to gaps in documentation, causing payments to be disqualified. For example, a teacher who changes schools mid-career might forget to recertify their employment, only to discover years later that some payments were not counted. Submitting the ECF regularly ensures a clear record of qualifying employment.

Payment miscalculations also trip up many borrowers. PSLF requires 120 *qualifying* payments, which must be made on time, in full, and while employed by a qualifying employer. Partial payments, late payments, or payments made during periods of unemployment or ineligible employment do not count. For instance, a borrower who makes 119 qualifying payments and one late payment will need to start over. Using autopay and maintaining meticulous records can help avoid such mistakes.

Lastly, loan type ineligibility is a common but often overlooked issue. Only Direct Loans qualify for PSLF; Federal Family Education Loans (FFEL) and Perkins Loans do not. Borrowers with these loan types must consolidate them into a Direct Consolidation Loan to become eligible. However, consolidating resets the payment count, meaning borrowers lose credit for any payments made before consolidation. A social worker with 50 qualifying payments on FFEL loans, for example, would restart at zero after consolidating. Checking loan types early and consolidating promptly can prevent this setback.

By addressing these common rejection reasons—ineligible repayment plans, employment certification errors, payment miscalculations, and loan type ineligibility—borrowers can significantly improve their chances of PSLF approval. Proactive steps, such as switching to an IDR plan, submitting the ECF regularly, ensuring timely payments, and consolidating ineligible loans, are essential for navigating the program’s complexities.

Nurse Loan Forgiveness: Unlock Debt-Free Freedom with These Strategies

You may want to see also

![]()

Success Stories & Tips

The Public Service Loan Forgiveness (PSLF) program has indeed delivered on its promise for thousands of borrowers, wiping out hundreds of thousands of dollars in student debt. Take Sarah, a 38-year-old social worker, who saw her $120,000 loan balance vanish after 10 years of consistent payments while working for a nonprofit. Her success wasn’t luck—it was the result of meticulous planning, including annual employment certification and switching to an income-driven repayment plan to lower her monthly payments. Stories like Sarah’s highlight that while the PSLF process can be complex, it’s navigable with the right strategy.

One critical tip from successful applicants is to certify your employment annually, not just at the end of the 10-year period. This ensures your employer qualifies under PSLF guidelines and catches any discrepancies early. For instance, John, a public school teacher, discovered halfway through his repayment period that his charter school didn’t qualify. By switching to a district school and certifying annually, he stayed on track. Another pro tip: consolidate FFEL or Perkins Loans into a Direct Consolidation Loan if necessary, as only Direct Loans qualify for PSLF. This step alone has saved countless borrowers from disqualification.

A common thread among success stories is the use of income-driven repayment (IDR) plans. These plans cap monthly payments at a percentage of discretionary income, often making them lower than standard plans. For example, Emily, a nonprofit lawyer, reduced her monthly payment from $800 to $250 by enrolling in Pay As You Earn (PAYE). Lower payments not only ease financial stress but also maximize the amount forgiven after 10 years. Pairing IDR with PSLF is a strategic move, as any remaining balance is forgiven tax-free.

However, beware of pitfalls. Many borrowers fall short due to payment miscounts or employer misclassification. Michael, a nurse practitioner, lost two years of qualifying payments because his hospital’s HR department incorrectly filed his employment certification. His takeaway? Submit your own certifications and follow up with the PSLF servicer to confirm receipt. Additionally, keep detailed records of all payments and correspondence—this documentation can be a lifeline if disputes arise.

Finally, persistence pays off. The PSLF process can be bureaucratic and frustrating, but those who stay informed and proactive reap the rewards. Online communities and resources, like the Department of Education’s PSLF Help Tool, offer invaluable guidance. By learning from others’ successes and mistakes, borrowers can navigate the program with confidence, turning a mountain of debt into a manageable—and ultimately forgivable—burden.

Is Student Loan Forgiveness Automatic for Borrowers? Find Out Now

You may want to see also

![]()

Recent Policy Updates

The Public Service Loan Forgiveness (PSLF) program has seen significant policy updates in recent years, reshaping its impact on borrowers. One of the most notable changes came in October 2021 with the introduction of the Limited PSLF (TEPSLF) Waiver, which temporarily relaxed the program’s stringent rules. This waiver allowed borrowers to receive credit for past payments made under any federal loan repayment plan, regardless of whether they were previously ineligible under PSLF guidelines. For example, payments made under graduated or extended repayment plans, which were previously excluded, now counted toward forgiveness. This shift resulted in thousands of borrowers qualifying for forgiveness who were previously denied, with the Department of Education reporting over $10 billion in loan forgiveness to more than 175,000 borrowers as of early 2023.

Another critical update is the expansion of qualifying employers under PSLF. Historically, only full-time employees of government or 501(c)(3) nonprofit organizations were eligible. However, recent policy changes clarified that certain types of nonprofit and public service employment, such as military service and tribal government work, now qualify. This expansion has opened the door for more borrowers to pursue forgiveness, particularly those in underserved or specialized sectors. For instance, teachers working in low-income schools and healthcare professionals in rural clinics now have clearer pathways to qualify, provided they meet the 120 qualifying payment threshold.

The implementation of the IDR Account Adjustment in 2023 further bolstered PSLF accessibility. This adjustment retroactively credited borrowers for time spent in forbearance, economic hardship deferment, or certain repayment plans toward their PSLF payment count. Borrowers who had been in repayment for years but faced setbacks due to administrative errors or misguidance suddenly found themselves closer to the 120-payment finish line. For example, a borrower who had been in forbearance for 24 months could now count that time toward their PSLF requirement, effectively shaving two years off their repayment timeline.

Despite these advancements, borrowers must navigate these updates with caution. The deadline for the Limited PSLF Waiver, which expired on October 31, 2023, underscores the importance of timely action. Borrowers who missed this deadline may still qualify under standard PSLF rules but will no longer benefit from the waiver’s flexibility. Additionally, the need for annual recertification of employment remains a critical step, as failing to do so can disrupt progress toward forgiveness. Practical tips include consolidating FFEL or Perkins Loans into a Direct Consolidation Loan, ensuring payments are made on time, and maintaining detailed records of employment and payments.

In conclusion, recent PSLF policy updates have democratized access to loan forgiveness, but they require proactive engagement from borrowers. By understanding these changes and taking strategic steps, such as consolidating loans and recertifying employment annually, borrowers can maximize their chances of achieving debt relief. The success stories of those who have already had their loans forgiven under these updated policies serve as both inspiration and a roadmap for others navigating the PSLF journey.

Is Forgiven Student Loan Debt Taxable? What Borrowers Need to Know

You may want to see also

Frequently asked questions

Yes, many borrowers have successfully had their student loans forgiven through the PSLF program. As of recent data, thousands of public service workers have received loan forgiveness after meeting the program’s requirements, such as making 120 qualifying payments while working full-time for an eligible employer.

The PSLF program requires 120 qualifying monthly payments, which typically takes about 10 years. After completing these payments and submitting the PSLF application, forgiveness is granted for the remaining loan balance.

Common reasons for PSLF denial include missing or incomplete paperwork, non-qualifying payments (e.g., late or partial payments), ineligible loan types (only Direct Loans qualify), and employment not certified by an eligible public service organization.

Only payments made on Direct Loans qualify for PSLF. If you’ve made payments on other loan types (e.g., FFEL or Perkins Loans), you may need to consolidate them into a Direct Consolidation Loan to qualify. However, only payments made *after* consolidation will count toward PSLF.