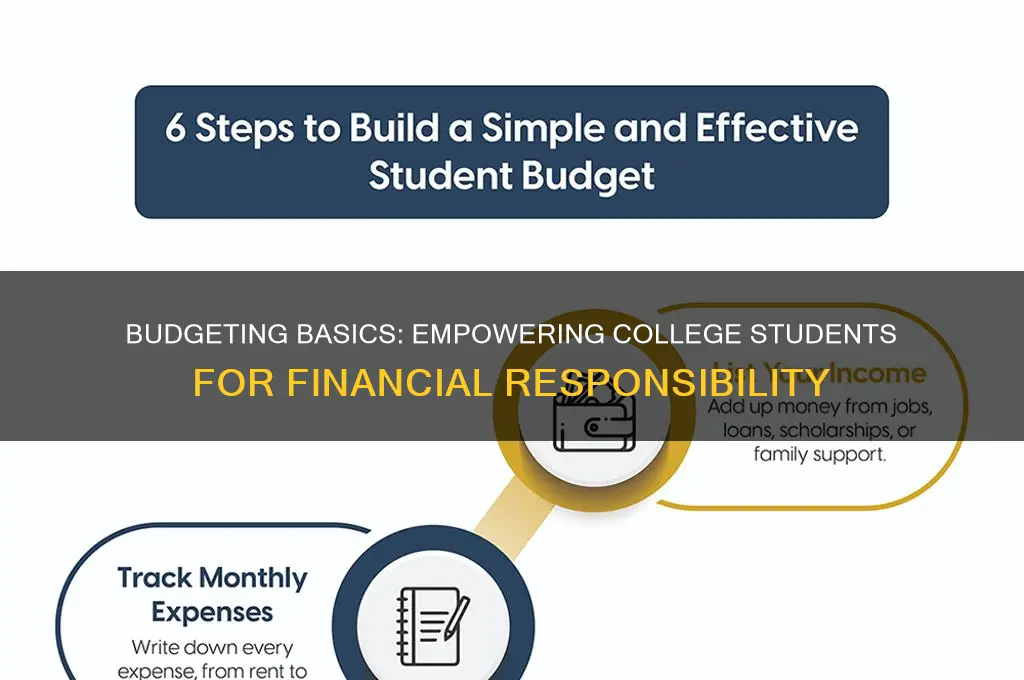

Budgeting is a critical skill that can empower college students to take control of their finances and develop lifelong habits of financial responsibility. By creating and adhering to a budget, students learn to prioritize their spending, distinguish between needs and wants, and allocate their limited resources effectively. This practice not only helps them avoid unnecessary debt but also fosters a deeper understanding of financial planning, saving, and long-term goal setting. As they navigate the challenges of student life, budgeting equips them with the tools to make informed decisions, build financial resilience, and lay a strong foundation for a secure future.

| Characteristics | Values |

|---|---|

| Financial Awareness | Budgeting helps students understand their income (e.g., part-time job earnings, allowances) and expenses (tuition, books, rent, food), fostering a clear picture of their financial situation. |

| Spending Discipline | Allocating money to specific categories (e.g., essentials, entertainment) teaches students to prioritize needs over wants, reducing impulsive spending. |

| Savings Habit | Incorporating savings into a budget encourages students to set aside funds for emergencies or future goals, promoting long-term financial stability. |

| Debt Management | Budgeting helps students track and manage student loans or credit card debt, ensuring timely payments and minimizing interest accumulation. |

| Goal Setting | Creating a budget allows students to set and work toward financial goals, such as saving for a study abroad program or paying off debt. |

| Accountability | Regularly reviewing a budget holds students accountable for their spending habits, encouraging adjustments to stay on track. |

| Financial Independence | Budgeting empowers students to manage their finances without relying on parents or guardians, building self-reliance. |

| Stress Reduction | A well-planned budget reduces financial uncertainty and stress, allowing students to focus on academics and personal growth. |

| Long-Term Financial Planning | Early budgeting habits lay the foundation for future financial success, including retirement planning and investments. |

| Adaptability | Budgeting teaches students to adjust their spending based on changing circumstances, such as fluctuating income or unexpected expenses. |

| Critical Thinking | Analyzing income and expenses enhances problem-solving skills, helping students make informed financial decisions. |

| Resource Management | Budgeting encourages efficient use of limited resources, teaching students to maximize value from their money. |

Explore related products

What You'll Learn

- Tracking Expenses: Learn to monitor spending habits to identify areas for saving

- Setting Financial Goals: Define short-term and long-term objectives to stay motivated

- Prioritizing Needs vs. Wants: Distinguish essentials from luxuries to allocate funds wisely

- Emergency Savings: Build a safety net for unexpected expenses or financial setbacks

- Avoiding Debt Traps: Use budgeting to minimize reliance on loans or credit cards

![]()

Tracking Expenses: Learn to monitor spending habits to identify areas for saving

College students often find themselves juggling limited funds while navigating the newfound freedom of managing their own finances. Tracking expenses is a critical skill that empowers them to take control of their financial lives. By monitoring spending habits, students can identify areas where they may be overspending and make informed decisions to save money.

The Power of Awareness: Uncovering Spending Patterns

Imagine your bank account as a mystery novel, and each transaction is a clue. Tracking expenses is like becoming the detective, piecing together the story of your financial habits. Start by gathering all your financial information: bank statements, credit card bills, receipts, and even those forgotten Venmo charges. Categorize your spending into areas like groceries, entertainment, transportation, and subscriptions. Many budgeting apps and spreadsheets can automate this process, making it less daunting.

A 2020 study by the Financial Industry Regulatory Authority (FINRA) found that individuals who track their spending are more likely to save consistently and feel more confident about their financial future. This awareness is the first step towards making conscious choices about where your money goes.

From Data to Action: Identifying Savings Opportunities

Once you've categorized your spending, analyze the data. Are there surprise categories where your money disappears? Maybe those daily coffee runs add up to a significant monthly expense, or subscription services you rarely use are draining your account. For instance, a student spending $5 on coffee every weekday would spend $1,300 annually. Cutting back to three coffees a week could save $520 a year – enough for textbooks or a weekend getaway. Look for recurring expenses that can be reduced or eliminated without sacrificing your well-being.

Consider the "50/30/20" rule as a starting point: aim to allocate 50% of your income to needs (rent, groceries, utilities), 30% to wants (entertainment, dining out), and 20% to savings and debt repayment. Adjust these percentages based on your individual circumstances, but use them as a framework to guide your spending decisions.

Sustainable Habits: Making Tracking a Lifestyle

Tracking expenses isn't a one-time event; it's a habit that needs to be cultivated. Set aside time each week to review your spending and adjust your budget as needed. Treat it like a date with your financial health. There are numerous apps and tools available to make this process easier, from simple spreadsheet templates to sophisticated budgeting software. Find a system that works for you and stick with it. Remember, consistency is key. The more regularly you track, the more accurate your financial picture will be, and the easier it will be to identify areas for improvement.

By consistently tracking expenses, college students can transform their financial lives. They'll gain valuable insights into their spending habits, make informed decisions about their money, and ultimately build a foundation for long-term financial security.

Effective Strategies for Teaching English to Deaf Students

You may want to see also

Explore related products

![]()

Setting Financial Goals: Define short-term and long-term objectives to stay motivated

College students often juggle limited income, rising expenses, and the pressure to build a future. Setting clear financial goals transforms budgeting from a chore into a roadmap for success. Short-term goals, like saving $200 for textbooks or paying off a credit card balance within six months, provide immediate focus and achievable milestones. Long-term goals, such as building a $5,000 emergency fund or saving for a post-graduation trip, offer direction and motivation. Without these objectives, budgeting risks becoming aimless, making it harder to resist impulse purchases or stay committed during financial setbacks.

Consider the difference between a student who budgets blindly and one who sets a goal to save $1,000 by the end of the semester. The goal-oriented student tracks expenses, prioritizes needs over wants, and celebrates progress, while the other may overspend on non-essentials, feeling discouraged by a lack of tangible results. Research shows that goal-setting increases financial discipline by 60%, as it activates the brain’s reward system, reinforcing positive behaviors. For instance, using apps like Mint or YNAB to visualize progress can make goals feel more attainable, turning abstract numbers into actionable steps.

However, setting goals isn’t enough—they must be SMART: Specific, Measurable, Achievable, Relevant, and Time-bound. A vague goal like “save money” lacks clarity, while “save $50 per month for six months to cover summer housing” provides a clear target. Break long-term goals into smaller, monthly benchmarks to avoid overwhelm. For example, saving $10,000 for graduate school in two years becomes more manageable when framed as $417 per month. Pairing goals with deadlines creates urgency, making it easier to say no to unnecessary spending.

Caution: Avoid setting overly ambitious goals that lead to frustration. A student earning $10/hour from a part-time job may struggle to save $1,000 in one month. Instead, start with realistic targets and adjust as income or circumstances change. Additionally, regularly review and update goals to reflect evolving priorities. For instance, a sudden internship opportunity might require reallocating funds from a travel goal to professional attire or transportation. Flexibility ensures goals remain motivating, not restrictive.

Ultimately, financial goals are the compass of budgeting, turning abstract financial responsibility into concrete actions. Short-term wins build confidence, while long-term vision fosters resilience. By aligning spending habits with specific objectives, college students not only manage money effectively but also cultivate a mindset of intentionality that extends beyond their academic years. Start small, stay consistent, and let goals be the bridge between present sacrifices and future rewards.

Teaching Haiku to Kids: Simple Steps for Elementary Classrooms

You may want to see also

Explore related products

![]()

Prioritizing Needs vs. Wants: Distinguish essentials from luxuries to allocate funds wisely

College students often face a stark reality: limited funds and endless choices. This financial tightrope act demands a critical skill—distinguishing needs from wants. Needs are non-negotiable expenses essential for survival and academic success, such as tuition, textbooks, housing, groceries, and transportation. Wants, on the other hand, are discretionary purchases like dining out, streaming subscriptions, or trendy clothing. Mastering this distinction is the cornerstone of budgeting, enabling students to allocate funds wisely and avoid financial pitfalls.

Consider a practical example: a student with $500 monthly after covering tuition and rent. Without prioritizing, they might spend $100 on coffee, $50 on a new video game, and $30 on impulse snacks, leaving only $320 for groceries, utilities, and other essentials. By categorizing expenses, they could redirect $180 from wants to needs, ensuring financial stability while still allowing for occasional treats. This approach fosters mindfulness, teaching students to question, "Do I need this now, or can it wait?"

Prioritizing needs over wants isn’t about deprivation—it’s about intentionality. Start by listing all monthly expenses and categorizing them as needs or wants. Use the 50/30/20 rule as a guideline: 50% of income for needs, 30% for wants, and 20% for savings or debt repayment. For college students, adjusting this to 60/20/20 might be more realistic, given tighter budgets. Apps like Mint or YNAB can automate tracking, making it easier to visualize spending patterns and adjust accordingly.

A cautionary note: wants often masquerade as needs. For instance, a student might justify a $5 daily latte as necessary for productivity. However, at $150 monthly, this "need" could fund a semester’s worth of groceries. Challenge these assumptions by asking, "What’s the minimum I require to function effectively?" Often, the answer reveals opportunities to cut costs without sacrificing quality of life.

Ultimately, prioritizing needs vs. wants is a transformative habit. It empowers students to make informed financial decisions, build resilience against impulse spending, and lay the foundation for long-term financial health. By focusing on essentials first, students not only survive college on a budget but also graduate with valuable skills for managing money in the real world.

Can Teachers Legally Share Your Grades with Other Students?

You may want to see also

Explore related products

![]()

Emergency Savings: Build a safety net for unexpected expenses or financial setbacks

College students often face financial unpredictability, from sudden medical bills to unexpected travel needs. Building an emergency savings fund is a critical step in fostering financial responsibility, providing a buffer against life’s curveballs. Start by setting a realistic goal—aim to save at least $500 to $1,000 initially, which can cover minor emergencies like a car repair or textbook costs. This small but significant safety net reduces reliance on high-interest debt, such as credit cards, when unexpected expenses arise.

To build this fund, treat emergency savings as a non-negotiable monthly expense. Allocate 5–10% of your income (from part-time jobs, stipends, or allowances) directly into a dedicated savings account. Automate this process by setting up recurring transfers from your checking account to your emergency fund. Keep this money in a separate, easily accessible account, but not so accessible that you’re tempted to spend it on non-emergencies. For example, a high-yield savings account offers better returns than a traditional one while maintaining liquidity.

A common pitfall is dipping into emergency savings for non-essential purchases. To avoid this, define what constitutes an emergency—unplanned expenses that threaten your financial stability, not discretionary spending like concert tickets or upgraded electronics. If you withdraw from the fund, prioritize replenishing it before saving for other goals, such as travel or entertainment. This discipline reinforces the purpose of the fund and ensures it remains intact for genuine emergencies.

Comparing emergency savings to other financial priorities highlights its importance. While saving for long-term goals like a study abroad program or a post-graduation move is valuable, an emergency fund provides immediate protection. Without it, a single unexpected expense can derail your entire financial plan, forcing you to borrow money or sacrifice other goals. By prioritizing emergency savings early, you build a foundation for financial resilience that benefits you throughout college and beyond.

Finally, regularly review and adjust your emergency fund based on your circumstances. As your financial responsibilities grow—such as moving off-campus or taking on more independent expenses—increase your savings goal accordingly. Aim to eventually cover 3–6 months’ worth of living expenses, a standard benchmark for financial security. This proactive approach not only safeguards your finances but also instills habits of foresight and self-reliance, essential skills for lifelong financial responsibility.

Teaching Articles to Grade 1: Simple Strategies for Early Learners

You may want to see also

Explore related products

![]()

Avoiding Debt Traps: Use budgeting to minimize reliance on loans or credit cards

College students often find themselves at a financial crossroads, where the allure of easy credit and the necessity of loans can lead to long-term debt traps. Budgeting emerges as a critical tool to navigate this challenge, offering a structured approach to minimize reliance on loans and credit cards. By allocating funds wisely, students can cover essential expenses without overextending themselves financially. For instance, a monthly budget that prioritizes tuition, textbooks, and living expenses can reduce the need for additional borrowing. This proactive approach not only limits debt accumulation but also fosters a habit of financial discipline that extends beyond college years.

Consider the scenario of a student who receives a credit card offer with a high limit and low introductory interest rate. Without a budget, it’s easy to view this as "free money" for non-essential purchases like dining out or travel. However, budgeting forces a reality check by categorizing expenses into needs versus wants. A practical tip is to use the 50/30/20 rule: allocate 50% of income to necessities, 30% to discretionary spending, and 20% to savings or debt repayment. By adhering to this framework, students can avoid the temptation to overspend on credit, ensuring that loans are reserved for critical educational expenses rather than lifestyle inflation.

The psychological impact of budgeting cannot be overstated. It shifts the mindset from reactive spending to intentional saving, empowering students to make informed financial decisions. For example, tracking expenses through apps like Mint or Excel spreadsheets provides visibility into spending patterns, highlighting areas where cuts can be made. This awareness is particularly crucial for students who rely on loans, as it encourages them to borrow only what is absolutely necessary. A cautionary note: while budgeting helps manage existing debt, it’s equally important to avoid new debt by resisting impulsive purchases, even if they seem small.

Comparatively, students who budget effectively often graduate with significantly lower debt than their peers. A study by the Institute for College Access & Success found that the average student loan debt in 2022 was $31,300, but those who practiced strict budgeting reported debts 20-30% lower. This disparity underscores the tangible benefits of financial planning. Moreover, budgeting instills skills like prioritization and self-control, which are invaluable in managing credit card usage. For instance, paying off credit card balances in full each month avoids accruing interest, a practice made feasible through disciplined budgeting.

In conclusion, budgeting is not merely a tool for balancing income and expenses; it’s a shield against the debt traps that ensnare many college students. By creating a budget, students can align their spending with their financial goals, reducing the need for excessive loans or credit card usage. Practical steps include setting clear financial limits, tracking expenses diligently, and prioritizing needs over wants. The long-term takeaway is clear: budgeting during college lays the foundation for a lifetime of financial responsibility, ensuring that students graduate not just with a degree, but with the skills to thrive economically.

Can Teachers Text Students? Boundaries, Ethics, and Communication Guidelines

You may want to see also

Frequently asked questions

Budgeting requires students to track their income and expenses, providing a clear picture of where their money goes. This awareness helps identify unnecessary spending and encourages better financial decisions.

Yes, budgeting forces students to allocate funds to essential needs (like tuition and rent) before discretionary spending (like entertainment). This practice instills discipline and helps them focus on long-term goals.

By setting aside a portion of their income for savings, budgeting teaches students to build an emergency fund. This habit ensures they have a safety net for unexpected expenses, reducing financial stress.

Absolutely. Budgeting encourages living within one’s means and reduces reliance on credit cards or loans. It also helps students plan for debt repayment, such as student loans, in a structured way.