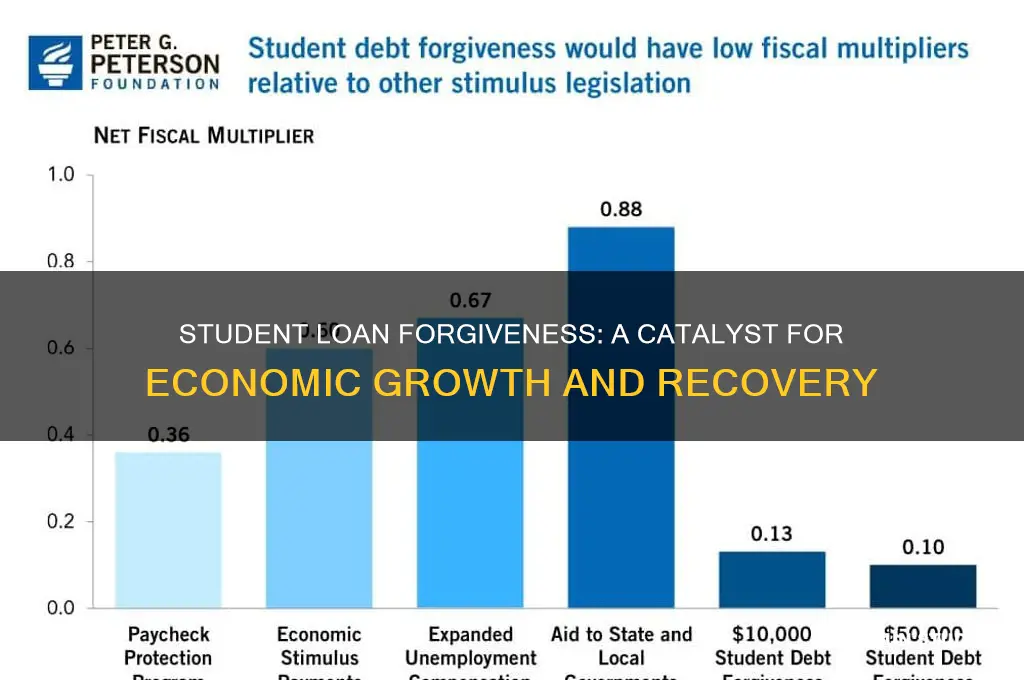

Student loan forgiveness has the potential to significantly boost the economy by alleviating the financial burden on millions of borrowers, thereby freeing up disposable income for other expenditures. When individuals are no longer constrained by high monthly loan payments, they are more likely to spend on goods and services, invest in homes, or start businesses, all of which stimulate economic growth. Additionally, reduced debt levels can improve credit scores, enabling borrowers to access better financial opportunities. On a broader scale, this policy can address wealth inequality, particularly among marginalized communities, and foster long-term economic stability by empowering a generation to contribute more actively to the economy.

Explore related products

What You'll Learn

- Increased consumer spending from debt-free graduates stimulates local businesses and markets

- Reduced debt burden allows young professionals to invest in homes and assets

- Higher disposable income boosts savings, investments, and retirement planning for millennials

- Forgiveness encourages entrepreneurship, creating new jobs and innovative businesses nationwide

- Lower default rates improve credit scores, expanding access to loans and economic growth

![]()

Increased consumer spending from debt-free graduates stimulates local businesses and markets

Student loan forgiveness can free up a significant portion of disposable income for millions of graduates, transforming them from debt-burdened individuals into active participants in the economy. When graduates are no longer shackled by monthly loan payments, they gain financial flexibility, which often translates into increased consumer spending. This spending doesn’t just disappear into a void; it flows directly into local businesses and markets, creating a ripple effect of economic growth. For instance, a graduate saving $300 per month on loan payments might spend that money at local restaurants, gyms, or retail stores, directly supporting small businesses in their community.

Consider the multiplier effect of this spending. When a debt-free graduate spends $100 at a local coffee shop, that money doesn’t stop there. The coffee shop owner might use it to pay employees, purchase supplies from local vendors, or invest in expanding their business. This cycle continues, amplifying the initial spending and creating a broader economic impact. Studies suggest that every dollar of student loan forgiveness could generate $1.03 in GDP, with a significant portion of that flowing into local economies. This isn’t just theoretical—cities like Burlington, Vermont, have seen tangible benefits from student loan repayment programs, with increased foot traffic and revenue for small businesses.

To maximize this effect, graduates should prioritize spending in areas that directly benefit their communities. For example, instead of funneling money into large online retailers, they could allocate a portion of their savings to local farmers’ markets, independent bookstores, or community-based services. Practical steps include creating a budget that designates a percentage of freed-up income for local spending, or joining community-supported agriculture (CSA) programs. Graduates aged 25–34, who often have the highest student debt burdens, are particularly well-positioned to drive this change, as they are in prime spending years and often live in urban or suburban areas with robust local economies.

However, it’s crucial to avoid pitfalls that could diminish this economic boost. For instance, while increased spending is beneficial, graduates should also consider saving or investing a portion of their freed-up income to build long-term financial stability. Additionally, local businesses must be prepared to capitalize on this influx of spending by offering quality products and services that attract and retain customers. Policymakers can play a role too, by incentivizing local spending through tax breaks or grants for small businesses, ensuring that the economic benefits are sustainable and widespread.

In conclusion, increased consumer spending from debt-free graduates isn’t just a personal win—it’s a catalyst for local economic revitalization. By strategically directing their spending, graduates can strengthen the businesses and markets that form the backbone of their communities. This approach not only fosters immediate growth but also builds a more resilient and interconnected local economy for the future.

Discovering Your Eligible Student Loans for Forgiveness: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Reduced debt burden allows young professionals to invest in homes and assets

Student loan forgiveness can significantly reduce the financial strain on young professionals, freeing up income that would otherwise be allocated to monthly loan payments. This immediate increase in disposable income allows individuals to redirect funds toward substantial investments, such as purchasing a home or acquiring assets like vehicles, stocks, or retirement accounts. For instance, a borrower with a $30,000 loan balance and a 6% interest rate might save approximately $300 per month, which could be used for a down payment on a house or to build an emergency fund. This shift not only improves personal financial stability but also stimulates broader economic activity.

Consider the housing market, a cornerstone of economic growth. With reduced debt burdens, young professionals are more likely to qualify for mortgages, as their debt-to-income ratios improve. For example, a borrower earning $60,000 annually with $400 in monthly student loan payments might struggle to secure a mortgage. However, with those payments eliminated, they could afford a higher monthly housing expense, increasing their chances of homeownership. This surge in first-time homebuyers drives demand for real estate, boosts construction jobs, and increases spending on home furnishings and renovations, creating a ripple effect across multiple sectors.

Asset accumulation is another critical area where student loan forgiveness can make a difference. Without the weight of student loans, young professionals can allocate funds to long-term investments, such as retirement accounts or stock portfolios. For instance, a 25-year-old who invests $300 monthly in a diversified index fund with an average annual return of 7% could accumulate over $700,000 by age 65. This not only secures their financial future but also injects capital into financial markets, supporting business growth and innovation. Additionally, increased investment in assets like education or professional certifications can enhance productivity and earning potential, further fueling economic growth.

However, maximizing these benefits requires strategic planning. Young professionals should prioritize creating a budget that allocates freed-up funds toward high-impact areas like homeownership or retirement savings. For example, setting aside 20% of the saved loan payment for a down payment and investing the remaining 80% in a tax-advantaged retirement account can balance short-term goals with long-term financial security. Caution should also be exercised to avoid lifestyle inflation, where increased disposable income leads to higher spending on non-essential items, undermining the potential economic benefits of loan forgiveness.

In conclusion, reducing the debt burden through student loan forgiveness empowers young professionals to invest in homes and assets, driving economic growth through increased consumer spending, housing market activity, and long-term capital investment. By strategically redirecting funds, individuals can not only improve their financial well-being but also contribute to a more robust and dynamic economy. This dual benefit underscores the transformative potential of student loan forgiveness as both a personal and macroeconomic tool.

Texas Student Loan Forgiveness: Eligibility and Application Guide

You may want to see also

Explore related products

![]()

Higher disposable income boosts savings, investments, and retirement planning for millennials

Millennials, burdened by an average student loan debt of $33,000, often delay financial milestones like saving, investing, and planning for retirement. Student loan forgiveness could free up a significant portion of their monthly income, enabling them to redirect funds toward these critical areas. For instance, forgiving $10,000 in debt could save a borrower approximately $100 per month, assuming a standard 10-year repayment plan at a 6% interest rate. This extra disposable income, when multiplied across millions of borrowers, could inject billions into the economy annually through increased savings and investments.

Consider the ripple effect of higher disposable income on savings. A millennial earning $50,000 annually with $300 monthly student loan payments could save an additional $3,600 per year if those payments were eliminated. By allocating this amount to a high-yield savings account with a 3% annual return, they could accumulate over $11,000 in savings within three years. Financial advisors recommend saving at least 20% of income, a goal more attainable without the burden of student debt. This increased savings rate not only provides financial security but also stimulates economic growth by increasing the pool of funds available for lending and investment.

Investment opportunities also expand with higher disposable income. Millennials could allocate a portion of their newfound funds to diversified portfolios, such as index funds or ETFs, which historically yield 7-10% annual returns. For example, investing $200 monthly over 30 years at a 9% return could grow to nearly $300,000. This wealth accumulation not only benefits individuals but also fuels capital markets, supporting businesses and innovation. Additionally, millennials are more likely to invest in socially responsible funds, aligning financial growth with environmental and social impact.

Retirement planning, often neglected due to debt obligations, becomes feasible with student loan forgiveness. A 25-year-old millennial could maximize a Roth IRA by contributing the annual limit of $6,500 (including catch-up contributions) with the extra income. Over 40 years, this could grow to over $1.5 million, assuming an 8% annual return. Employers’ 401(k) matching programs further amplify savings, effectively providing free money toward retirement. By starting early and consistently contributing, millennials can bridge the retirement gap exacerbated by delayed savings due to student debt.

However, realizing these benefits requires strategic planning. Millennials should prioritize creating an emergency fund with 3-6 months’ expenses before investing. Utilizing automated savings tools and budgeting apps can ensure consistent contributions. Consulting a financial advisor can help tailor strategies to individual goals, such as homeownership or early retirement. While student loan forgiveness provides the means, disciplined financial habits ensure long-term prosperity. This combination of relief and responsibility not only transforms individual financial trajectories but also contributes to a more robust, resilient economy.

Is Edfinancial Eligible for Student Loan Forgiveness? Key Details Explained

You may want to see also

Explore related products

![]()

Forgiveness encourages entrepreneurship, creating new jobs and innovative businesses nationwide

Student loan debt often shackles young professionals to stable, income-secure jobs rather than risky ventures. Forgiveness breaks these chains, freeing individuals to pursue entrepreneurial dreams. Consider the aspiring tech founder who, unburdened by monthly payments, can afford to take the leap, hire a small team, and develop a groundbreaking app. Or the culinary graduate who opens a farm-to-table restaurant, employing local farmers and revitalizing a struggling downtown. Each forgiven loan becomes seed capital for a potential economic multiplier, as these new businesses generate jobs, stimulate local spending, and contribute to tax revenues.

Data from the Federal Reserve Bank of Philadelphia suggests that student debt reduces the likelihood of entrepreneurship by 12%. Conversely, forgiveness could reverse this trend, unleashing a wave of innovation and job creation. Imagine a nation where thousands of such ventures flourish, not just in tech hubs but in rural towns and underserved communities. The economic ripple effect would be profound, fostering a more dynamic and resilient economy.

However, forgiveness alone isn’t a silver bullet. Pairing it with accessible business resources—such as microloans, mentorship programs, and streamlined regulatory processes—maximizes its impact. For instance, a forgiven loan combined with a $10,000 startup grant and access to a business incubator could turn a fledgling idea into a thriving enterprise. Policymakers must ensure that forgiveness programs are designed to empower, not just relieve, by integrating support systems that nurture entrepreneurial success.

Critics argue that broad forgiveness could lead to moral hazard, but targeted programs can mitigate this risk. For example, tying forgiveness to business creation in economically distressed areas ensures that benefits align with broader economic goals. A graduate who starts a renewable energy company in a coal-dependent region not only creates jobs but also drives sustainable development. Such strategic forgiveness transforms individual relief into a tool for nationwide economic transformation.

Ultimately, student loan forgiveness isn’t just about alleviating personal debt—it’s about unlocking human potential. By freeing individuals to innovate and create, we invest in a future where entrepreneurship thrives, jobs abound, and communities prosper. The cost of forgiveness pales in comparison to the long-term gains of a more vibrant, inclusive economy.

Can County Government Jobs Erase Your Student Loan Debt?

You may want to see also

Explore related products

![]()

Lower default rates improve credit scores, expanding access to loans and economic growth

Student loan forgiveness can significantly reduce default rates, a critical factor in improving individual credit scores. When borrowers are no longer burdened by unmanageable debt, they are less likely to miss payments or default entirely. For instance, data from the Consumer Financial Protection Bureau shows that borrowers with reduced loan balances through forgiveness programs see an average credit score increase of 20 to 40 points within six months. This improvement is particularly impactful for younger borrowers, aged 25 to 34, who often carry the highest student debt loads and have limited credit histories. By lowering default rates, forgiveness programs create a ripple effect, enhancing financial stability for millions.

The mechanism behind this improvement is straightforward: credit scores are heavily influenced by payment history and debt-to-income ratios. When student loans are forgiven, both metrics improve. For example, a borrower with $30,000 in forgiven debt might see their debt-to-income ratio drop from 45% to 30%, a threshold lenders view favorably. This shift not only boosts their credit score but also signals to lenders that they are a lower-risk borrower. Practical steps for borrowers post-forgiveness include monitoring their credit reports for errors, paying other debts on time, and avoiding new high-interest loans to maximize these gains.

Expanding access to loans is a direct consequence of improved credit scores, and this access fuels economic growth. With higher credit scores, individuals can qualify for mortgages, auto loans, and small business loans at lower interest rates. Consider the case of a forgiven borrower who secures a mortgage at 4% instead of 6% due to their improved credit. Over a 30-year loan, this saves them over $60,000 in interest, freeing up funds for other economic activities. Similarly, small business loans enable entrepreneurship, creating jobs and stimulating local economies. A study by the Federal Reserve found that for every $10,000 in forgiven student debt, borrowers are 7% more likely to start a business within two years.

However, the benefits of lower default rates and improved credit scores extend beyond individual borrowers. Financial institutions also gain from reduced risk, allowing them to lend more confidently and expand their portfolios. This increased lending activity injects liquidity into the economy, supporting sectors like housing, automotive, and retail. For policymakers, the takeaway is clear: targeted student loan forgiveness is not just a social policy but an economic strategy. By reducing defaults, it creates a virtuous cycle of improved credit, expanded lending, and sustained growth, benefiting both individuals and the broader economy.

Updating Income for Student Loan Forgiveness: A Step-by-Step Guide

You may want to see also

Frequently asked questions

Student loan forgiveness frees up disposable income for borrowers, allowing them to spend more on goods and services, which boosts demand and supports businesses.

Yes, by reducing debt burdens, forgiveness enables individuals to take risks, start businesses, and create jobs, fostering economic growth and innovation.

With reduced debt, borrowers are more likely to qualify for mortgages, increasing homeownership rates and stimulating the housing market and related industries.

Yes, forgiveness allows workers to pursue career changes or take lower-paying but fulfilling jobs without the burden of debt, enhancing labor market efficiency.

It reduces default rates, improves credit scores, and increases long-term financial stability, enabling borrowers to contribute more to the economy through investments and savings.

![Principles of Political Economy and Taxation [1911 Edition]](https://m.media-amazon.com/images/I/81Xx2WBrKnL._AC_UL320_.jpg)