Student loan consolidation can significantly impact the path to loan forgiveness, particularly for borrowers pursuing Public Service Loan Forgiveness (PSLF) or income-driven repayment (IDR) forgiveness. Consolidation combines multiple federal loans into a single Direct Consolidation Loan, simplifying repayment but potentially resetting the clock on forgiveness timelines. For PSLF, consolidating can restart the required 120 qualifying payments, unless the borrower consolidates before switching jobs or ensures all prior payments are counted. Under IDR plans, consolidation may also reset the payment counter, delaying forgiveness. However, consolidation can be beneficial if it allows borrowers to switch to a forgiveness-eligible repayment plan or if they have loans from the Federal Family Education Loan (FFEL) program, which are not eligible for PSLF unless consolidated into the Direct Loan program. Careful consideration of individual circumstances is essential to avoid unintended consequences and maximize forgiveness opportunities.

Explore related products

What You'll Learn

- Eligibility Changes: Consolidation may reset payment counts, affecting eligibility for forgiveness programs like PSLF

- Interest Rates: New rates are averaged, potentially increasing costs compared to original loans

- Loan Types: Federal consolidation excludes private loans, limiting forgiveness options for mixed debt

- Repayment Plans: Consolidation allows access to income-driven plans, which can aid forgiveness timelines

- Forgiveness Progress: Prior qualifying payments may not count toward forgiveness after consolidation

![]()

Eligibility Changes: Consolidation may reset payment counts, affecting eligibility for forgiveness programs like PSLF

Student loan consolidation can be a double-edged sword for borrowers pursuing forgiveness programs like Public Service Loan Forgiveness (PSLF). One critical yet often overlooked consequence is the potential reset of payment counts. For PSLF, borrowers must make 120 qualifying payments under a specific repayment plan while working full-time for an eligible employer. Consolidation, however, can erase progress by restarting this counter, effectively delaying the path to forgiveness. This reset occurs because the new consolidated loan is considered a single, new loan, and previous payments no longer count toward the required 120.

Consider a borrower who has already made 60 qualifying payments under PSLF. If they consolidate their loans, those 60 payments are nullified, and the count begins anew. This setback can add years to the forgiveness timeline, particularly for those nearing the finish line. For example, a borrower with 10 years of payments (120 months) would have to start over, delaying forgiveness by up to a decade. This is especially problematic for older borrowers or those in time-sensitive careers, as it extends their financial burden and reduces the benefits of forgiveness programs.

To mitigate this risk, borrowers should carefully evaluate their eligibility for PSLF before consolidating. If already enrolled in PSLF and nearing the 120-payment mark, consolidation is generally inadvisable. However, if a borrower has made fewer than 120 payments and is struggling with multiple loans, consolidation might still be beneficial—but only if they switch to an income-driven repayment plan immediately afterward. This ensures that post-consolidation payments qualify for PSLF. Borrowers should also consult the Federal Student Aid website or a loan servicer to confirm their payment count and eligibility status before proceeding.

A practical tip is to use the PSLF Help Tool provided by the U.S. Department of Education to assess eligibility and track payments. This tool can help borrowers determine whether consolidation aligns with their forgiveness goals. Additionally, borrowers should avoid consolidating Federal Family Education Loans (FFEL) into the Direct Loan program unless they are certain about their PSLF eligibility, as FFEL loans are not eligible for PSLF unless consolidated into Direct Loans. By weighing these factors, borrowers can make informed decisions that preserve their progress toward loan forgiveness.

Will Biden Deliver on Student Loan Forgiveness? What We Know

You may want to see also

Explore related products

![]()

Interest Rates: New rates are averaged, potentially increasing costs compared to original loans

Student loan consolidation can be a double-edged sword, particularly when it comes to interest rates. One of the most significant changes borrowers face is the averaging of interest rates from their original loans. This means the new consolidated loan’s rate is a weighted average of the old rates, rounded up to the nearest one-eighth of 1%. For example, if you had two loans with rates of 4.5% and 6.8%, the consolidated rate would be 5.625%, not 5.65%. While this might seem like a minor adjustment, it can lead to higher overall costs over the life of the loan, especially if the original loans had lower rates.

Consider a borrower with $30,000 in loans at 3.76% and $20,000 at 5.54%. The weighted average would be approximately 4.53%, rounded up to 4.625%. Over a 10-year repayment term, this slight increase could add hundreds of dollars in interest payments. The impact is more pronounced for borrowers with a mix of low and high-rate loans, as the averaging process tends to pull the overall rate upward. This is particularly relevant for those pursuing forgiveness programs, as higher interest accrual can offset the benefits of reduced monthly payments.

To mitigate this, borrowers should carefully evaluate their current interest rates before consolidating. If most loans have rates below the potential consolidated rate, it may be wiser to keep them separate. For instance, a borrower with multiple loans under 4% might find consolidation less advantageous. Tools like the Federal Student Aid Loan Simulator can help model different scenarios, allowing borrowers to compare total costs with and without consolidation.

Another strategy is to prioritize paying down higher-interest loans before consolidating. By reducing the principal on loans with rates above the potential consolidated rate, borrowers can lower the weighted average and minimize cost increases. For example, allocating extra payments to a 7% loan while maintaining minimum payments on a 4% loan can shift the balance in favor of a lower consolidated rate.

Ultimately, while consolidation can simplify repayment, the interest rate averaging process demands careful consideration. Borrowers pursuing forgiveness programs must weigh the convenience of a single payment against the potential for higher costs. In some cases, maintaining separate loans or refinancing with a private lender might offer better terms. Understanding this trade-off is crucial for making an informed decision that aligns with long-term financial goals.

Forgiving Student Loans: Inflation Impact and Economic Consequences Explained

You may want to see also

Explore related products

![]()

Loan Types: Federal consolidation excludes private loans, limiting forgiveness options for mixed debt

Federal student loan consolidation is a tool often touted for simplifying repayment, but it comes with a critical limitation: it excludes private loans. This restriction can significantly hinder borrowers with mixed debt—those juggling both federal and private loans—who are seeking forgiveness options. While federal consolidation bundles multiple federal loans into a single Direct Consolidation Loan, it leaves private loans untouched, creating a fragmented repayment landscape. This division is problematic because most forgiveness programs, such as Public Service Loan Forgiveness (PSLF) or income-driven repayment (IDR) forgiveness, apply exclusively to federal loans. Borrowers with private loans must address them separately, often through refinancing or direct repayment, which can complicate their financial strategy and delay overall debt relief.

Consider a borrower with $30,000 in federal loans and $20,000 in private loans. By consolidating the federal loans, they might gain access to forgiveness programs like PSLF after 10 years of qualifying payments. However, the private loans remain ineligible for these programs and must be managed independently. This dual repayment structure can lead to higher monthly payments and longer repayment timelines, as private loans typically lack the flexible repayment plans and forgiveness opportunities available for federal loans. For instance, private loans often carry variable interest rates and stricter terms, making them more challenging to manage alongside a consolidated federal loan.

The exclusion of private loans from federal consolidation also limits strategic planning for forgiveness. Borrowers with mixed debt may need to prioritize paying off private loans aggressively while simultaneously making qualifying payments on their consolidated federal loan to pursue forgiveness. This balancing act requires careful budgeting and a clear understanding of each loan type’s terms. For example, a borrower might allocate extra funds to pay down high-interest private loans while ensuring they meet the minimum payment requirements for their federal loan to stay on track for PSLF. Without a consolidated approach, borrowers risk missing out on forgiveness opportunities or falling into default on their private loans.

One practical tip for borrowers with mixed debt is to explore private loan refinancing as a complementary strategy to federal consolidation. Refinancing private loans can lower interest rates or adjust repayment terms, making them more manageable while pursuing federal loan forgiveness. However, this approach requires a strong credit profile or a cosigner, which not all borrowers may have. Another option is to focus on paying off private loans first, freeing up cash flow to maximize payments toward the consolidated federal loan. This strategy, while effective, demands discipline and a long-term financial commitment.

In conclusion, federal consolidation’s exclusion of private loans creates a significant barrier for borrowers with mixed debt seeking forgiveness. It forces them to navigate two separate repayment systems, each with its own rules and limitations. Borrowers must carefully assess their loan portfolio, prioritize high-interest private debt, and explore refinancing or accelerated repayment strategies to optimize their path to debt relief. While federal consolidation can simplify federal loan management, it is not a one-size-fits-all solution for mixed debt. Understanding this limitation is crucial for crafting a realistic and effective forgiveness strategy.

Dept of Health Employees: Student Loan Forgiveness Options Explained

You may want to see also

Explore related products

![]()

Repayment Plans: Consolidation allows access to income-driven plans, which can aid forgiveness timelines

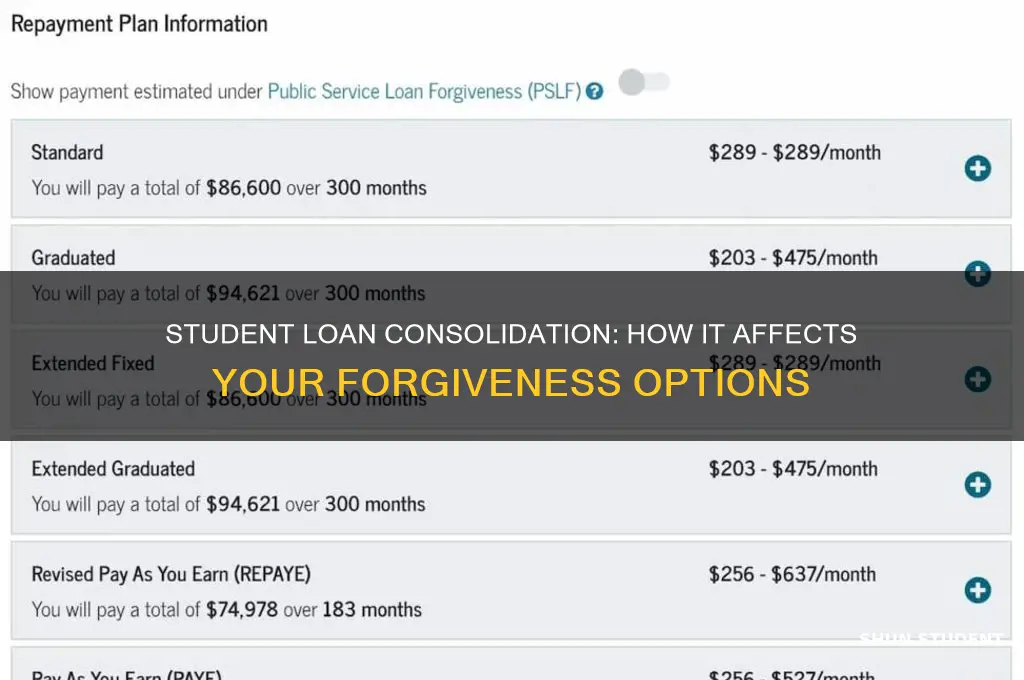

Student loan consolidation can be a strategic move for borrowers aiming to streamline their debt and potentially accelerate their path to forgiveness. One of its most significant advantages is unlocking access to income-driven repayment (IDR) plans, which are otherwise unavailable for certain types of federal loans, such as Federal Family Education Loans (FFEL) or Perkins Loans. By consolidating these loans into a Direct Consolidation Loan, borrowers can enroll in IDR plans like Pay As You Earn (PAYE), Revised Pay As You Earn (REPAYE), or Income-Based Repayment (IBR). These plans cap monthly payments at a percentage of discretionary income (typically 10-20%), making them more manageable for lower-income earners.

The real benefit of IDR plans lies in their connection to loan forgiveness programs. Under these plans, any remaining balance is forgiven after 20 or 25 years of qualifying payments, depending on the plan and loan type. For example, a borrower earning $40,000 annually with $60,000 in consolidated loans might see their monthly payment drop from $600 under the Standard Repayment Plan to $200 under REPAYE. Over 20-25 years, this reduced payment structure not only eases financial strain but also ensures that the borrower remains on track for forgiveness, even if their income doesn’t significantly increase.

However, consolidation isn’t without its nuances. When consolidating, any unpaid interest on the original loans capitalizes, increasing the principal balance. While this might seem counterintuitive, the long-term benefits of accessing IDR plans often outweigh the immediate cost. For instance, a borrower with $10,000 in capitalized interest might still save thousands over the life of the loan by reducing their monthly payments and qualifying for forgiveness sooner. It’s a trade-off that requires careful consideration of current financial circumstances and future earning potential.

To maximize the benefits of consolidation and IDR plans, borrowers should take proactive steps. First, assess eligibility for specific IDR plans by comparing income, family size, and loan type. Second, use online calculators to estimate monthly payments and forgiveness timelines under different scenarios. Third, apply for consolidation and IDR enrollment simultaneously to avoid delays. Finally, recertify income and family size annually to ensure payments remain aligned with financial reality. By strategically leveraging consolidation and IDR plans, borrowers can transform an overwhelming debt burden into a manageable path toward forgiveness.

Devry Student Loan Forgiveness: A Comprehensive Guide to Debt Relief

You may want to see also

Explore related products

![]()

Forgiveness Progress: Prior qualifying payments may not count toward forgiveness after consolidation

Consolidating student loans can reset the clock on forgiveness progress, potentially erasing years of qualifying payments. This is a critical issue for borrowers pursuing Public Service Loan Forgiveness (PSLF) or income-driven repayment (IDR) forgiveness. When federal loans are combined into a Direct Consolidation Loan, the new loan effectively starts from zero in terms of payment counts, even if the borrower had made years of eligible payments on the original loans. For example, a borrower with 80 qualifying PSLF payments (nearly 7 years) could lose all that progress if they consolidate, forcing them to restart the 120-payment requirement.

The mechanics behind this reset are rooted in the Department of Education’s rules. Consolidation creates a new loan with its own payment history, separate from the original loans. While the new loan retains eligibility for forgiveness programs, the prior payment counts do not transfer. This is particularly damaging for PSLF borrowers, who must make 120 qualifying payments under a specific repayment plan and employment criteria. A single misstep, such as consolidating at the wrong time, can delay forgiveness by years. For instance, a teacher with 10 years of payments might need to wait another decade if their prior payments are nullified.

Borrowers considering consolidation must weigh the trade-offs carefully. Consolidation can simplify repayment by combining multiple loans into one, potentially lowering monthly payments through extended repayment terms. However, this convenience comes at a steep cost for those nearing forgiveness. For IDR borrowers, the reset can be equally devastating. Under plans like REPAYE or IBR, forgiveness typically occurs after 20–25 years of qualifying payments. Consolidating midway through this period can extend the timeline significantly, increasing the total interest paid over the life of the loan.

To mitigate this risk, borrowers should explore alternatives before consolidating. For instance, if the goal is to lower monthly payments, switching to an IDR plan might achieve this without resetting forgiveness progress. Additionally, borrowers nearing the 120-payment threshold for PSLF should avoid consolidation altogether. Those with a mix of loan types (e.g., FFEL or Perkins Loans) should consolidate only if necessary to gain access to PSLF, ensuring they do so strategically to minimize payment count loss.

In summary, consolidation can be a double-edged sword for borrowers pursuing loan forgiveness. While it offers repayment simplicity, the potential loss of prior qualifying payments can delay forgiveness by years. Borrowers must carefully evaluate their situation, considering their proximity to forgiveness and the specific requirements of their repayment plan. Consulting with a loan servicer or financial advisor can provide clarity, ensuring consolidation aligns with long-term forgiveness goals rather than derailing them.

How to Secure Kaplan Student Loan Forgiveness: A Comprehensive Guide

You may want to see also

Frequently asked questions

Consolidating student loans can impact eligibility for forgiveness programs. For example, consolidating Federal Family Education Loan (FFEL) loans into a Direct Consolidation Loan may make them eligible for Public Service Loan Forgiveness (PSLF), but it resets the payment count. Additionally, income-driven repayment (IDR) forgiveness timelines may restart after consolidation.

Consolidating student loans does not inherently speed up forgiveness. In fact, it may reset the clock on forgiveness programs like PSLF or IDR forgiveness, requiring borrowers to start over with their qualifying payment count. However, consolidation can simplify repayment by combining multiple loans into one, making it easier to track progress toward forgiveness.

Consolidation itself does not change the total amount forgiven under programs like PSLF or IDR forgiveness. However, if consolidation resets the payment count, borrowers may end up making more payments before reaching forgiveness. Additionally, consolidating loans with varying interest rates may result in a higher weighted average interest rate, potentially increasing the total cost of the loan before forgiveness is applied.