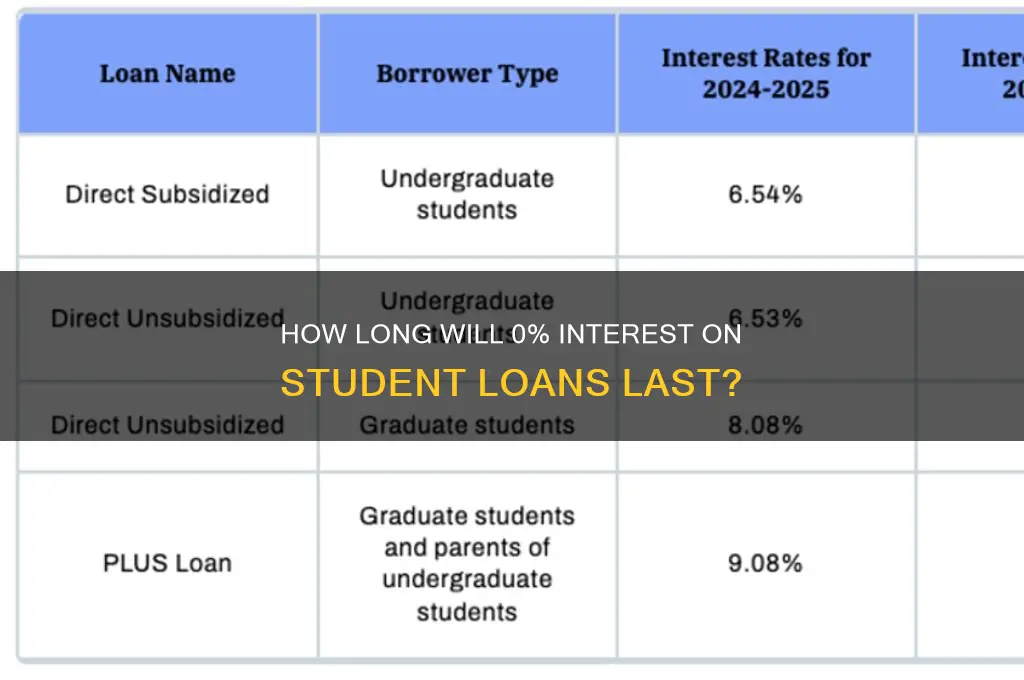

The duration of 0% interest on student loans has been a critical concern for borrowers, especially amid economic uncertainties and policy shifts. Since the onset of the COVID-19 pandemic, many countries, including the United States, implemented temporary interest waivers to alleviate financial strain on borrowers. However, these measures are not permanent, and their expiration dates vary depending on government decisions and legislative actions. As of now, borrowers are eagerly awaiting updates on whether these interest-free periods will be extended or phased out, as the end of such relief could significantly impact monthly payments and long-term financial planning. Understanding the timeline and potential changes is essential for students and graduates to manage their debt effectively.

| Characteristics | Values |

|---|---|

| Current Interest Rate | 0% (as of latest updates, temporary measure) |

| Start Date of 0% Interest | March 2020 (implemented due to COVID-19 pandemic) |

| Original End Date | September 30, 2023 (extended multiple times) |

| Latest Extension | Extended until June 30, 2024 (as of recent announcements) |

| Applicable Loans | Federal student loans held by the U.S. Department of Education |

| Impact on Borrowers | No interest accrues during this period; payments reduce principal |

| Future Plans | Uncertain; depends on federal policy and legislative decisions |

| Restart of Payments | Payments resume in October 2024 (after 0% interest period ends) |

| Interest Rate After Expiry | Returns to standard rates based on loan type and disbursement date |

| Eligibility | Applies to all federal student loan borrowers in repayment or forbearance |

| Source of Information | U.S. Department of Education and Federal Student Aid announcements |

Explore related products

$8.34 $17.99

What You'll Learn

![]()

Federal vs. private loan policies

The duration of 0% interest on student loans hinges critically on whether the loan is federal or private. Federal student loans, particularly those under the CARES Act provisions, have seen extended periods of 0% interest and paused payments, with the most recent extension lasting through August 2023. Private student loans, however, operate under entirely different rules, with interest accruing immediately and no standardized relief programs. This fundamental difference underscores the importance of understanding the policies governing your loan type.

For federal loan borrowers, the 0% interest period has been a lifeline, saving them thousands in interest costs. For example, a borrower with a $30,000 federal loan at a 5% interest rate would have avoided approximately $1,250 in interest annually during the pause. However, this relief is not indefinite. The Department of Education has tied the end of the 0% interest period to the resolution of ongoing litigation over student loan forgiveness, creating uncertainty for borrowers. To prepare, federal loan holders should calculate their monthly payments post-pause and explore income-driven repayment plans or loan consolidation options.

Private loan borrowers face a starkly different reality. Without federal oversight, private lenders are under no obligation to offer 0% interest or payment pauses. Some lenders introduced temporary relief programs during the pandemic, but these were often limited to 3–6 months and required proactive enrollment. For instance, a borrower with a $20,000 private loan at 8% interest would accrue $1,600 in interest annually, even during economic hardship. To mitigate this, private loan borrowers should negotiate directly with lenders for reduced rates, consider refinancing when rates are favorable, or explore state-specific relief programs.

A comparative analysis reveals that federal loans offer greater flexibility and borrower protections, while private loans prioritize lender profitability. For instance, federal loans allow for deferment, forbearance, and public service loan forgiveness, whereas private loans rarely offer such benefits. Borrowers with both federal and private loans should prioritize paying down private debt first due to higher interest rates and fewer safeguards. Additionally, tracking legislative updates and enrolling in autopay (which often reduces federal loan rates by 0.25%) can further optimize repayment strategies.

In conclusion, the longevity of 0% interest on student loans is dictated by the loan’s origin—federal or private. Federal borrowers benefit from extended relief tied to policy decisions, while private borrowers must navigate lender-specific terms. Proactive steps, such as recalculating payments, exploring repayment plans, and refinancing, can help borrowers manage the transition when 0% interest ends. Understanding these distinctions empowers borrowers to make informed decisions and minimize long-term financial strain.

How Student Loans Impact Your Financial Aid Eligibility Explained

You may want to see also

Explore related products

![]()

CARES Act extension updates

The CARES Act, enacted in March 2020, provided a lifeline to millions of student loan borrowers by pausing federal student loan payments, setting interest rates to 0%, and halting collections on defaulted loans. Initially set to expire in September 2020, this relief has been extended multiple times, most recently until December 31, 2022. Borrowers must now focus on understanding the implications of these extensions and preparing for the eventual resumption of payments.

Analytically, the repeated extensions reflect the ongoing economic challenges faced by many Americans. The Department of Education has cited the need to ensure a smooth transition back to repayment, particularly for those who have experienced financial hardship during the pandemic. However, the extensions also raise questions about the long-term sustainability of such measures. For instance, while 0% interest has saved borrowers billions in accrued interest, it has also delayed the reduction of principal balances for those who could afford to continue payments.

Instructively, borrowers should take specific steps to maximize the benefits of this extended relief period. First, verify that your loans qualify for the CARES Act protections, as only federal student loans are eligible. Private loans are not covered. Second, consider using the payment pause to pay down high-interest debt or build an emergency fund. If you’re in a stable financial position, making voluntary payments during this period can reduce your overall loan balance faster, thanks to the 0% interest rate.

Persuasively, it’s crucial for policymakers to address the root causes of student loan debt rather than relying solely on temporary fixes. While the CARES Act extensions provide immediate relief, they do not solve the systemic issues of rising tuition costs and insufficient financial aid. Advocates argue for more permanent solutions, such as income-driven repayment reforms or targeted loan forgiveness programs, to prevent future crises.

Comparatively, the CARES Act extensions stand out when compared to pre-pandemic student loan policies. Before 2020, borrowers had limited options for pausing payments, often requiring formal forbearance or deferment requests. The automatic nature of the CARES Act relief has set a precedent for how quickly and comprehensively the government can act in times of widespread financial distress. However, this also highlights the need for clearer communication about future expectations, as borrowers may now anticipate similar relief in other economic downturns.

Descriptively, the landscape of student loan policy remains in flux as December 31, 2022, approaches. Borrowers are advised to stay informed through official channels, such as the Department of Education’s Federal Student Aid website. Additionally, preparing for repayment resumption includes updating contact information with loan servicers, reviewing repayment plans, and exploring options like Public Service Loan Forgiveness if eligible. The end of the CARES Act extensions will mark a significant shift, and proactive planning is essential to avoid falling behind.

How to Apply for Obama Student Loan Forgiveness Program: A Guide

You may want to see also

Explore related products

![]()

Income-driven repayment impacts

The 0% interest rate on federal student loans, implemented as part of pandemic relief measures, has been a lifeline for many borrowers. However, this benefit is temporary, and its expiration date remains uncertain. For those enrolled in income-driven repayment (IDR) plans, the impact of this interest-free period is particularly significant, offering both immediate relief and long-term strategic opportunities.

Consider the mechanics of IDR plans: monthly payments are capped at a percentage of discretionary income, typically 10-20%, depending on the plan. During the 0% interest period, every dollar paid goes directly toward reducing the principal balance, rather than being split between interest and principal as usual. For borrowers with high balances, this accelerates debt reduction at an unprecedented rate. For example, a borrower with a $50,000 loan at 5% interest, paying $300 monthly under an IDR plan, would normally see only $75 applied to the principal. With 0% interest, the entire $300 reduces the balance, shaving years off the repayment timeline.

However, this advantage comes with a caveat: the temporary nature of the 0% interest rate. Once it expires, interest will accrue again, potentially slowing progress for those who haven’t maximized this window. Borrowers should prioritize making extra payments during this period, even if their required IDR payment is low. For instance, allocating an additional $100 monthly toward the principal can save thousands in interest over the life of the loan. Tools like the Department of Education’s Loan Simulator can help estimate the impact of extra payments under current conditions.

Another critical aspect is the interplay between IDR and loan forgiveness programs. Under IDR plans, any remaining balance is forgiven after 20-25 years of qualifying payments. The 0% interest period effectively shortens the time needed to reach forgiveness by reducing the principal faster. Borrowers nearing the forgiveness threshold should focus on maintaining consistent payments to capitalize on this accelerated timeline. Conversely, those early in repayment should view this period as a chance to minimize the balance before interest resumes, reducing the total amount subject to forgiveness calculations.

Finally, the psychological impact of 0% interest on IDR borrowers cannot be overlooked. Seeing the principal balance decrease month-over-month provides tangible motivation to stay on track. This period also offers a rare opportunity to experiment with budgeting strategies, such as redirecting funds from paused payments toward debt reduction. For example, a borrower who would normally pay $200 monthly can allocate that amount, plus any discretionary funds, to accelerate repayment without feeling the pinch of interest accumulation.

In summary, the 0% interest rate on student loans is a game-changer for IDR borrowers, but its benefits require proactive management. By understanding the mechanics of IDR plans, making strategic extra payments, and aligning efforts with forgiveness goals, borrowers can maximize this temporary relief and set themselves on a faster path to financial freedom.

Can Library Page Jobs Qualify for Student Loan Forgiveness?

You may want to see also

Explore related products

![]()

Loan forgiveness programs overview

The duration of 0% interest on student loans is a pressing concern for borrowers, but it’s equally critical to understand how loan forgiveness programs intersect with this timeline. While interest-free periods provide temporary relief, forgiveness programs offer a pathway to eliminate debt entirely under specific conditions. These programs vary widely in eligibility, requirements, and benefits, making them a complex but potentially transformative option for borrowers.

Consider the Public Service Loan Forgiveness (PSLF) program, which forgives remaining loan balances after 120 qualifying payments for those working full-time in government or nonprofit roles. This program is not directly tied to 0% interest periods but can be strategically paired with them. For instance, during interest-free periods, borrowers can redirect funds toward larger principal payments, accelerating progress toward the 120-payment threshold. However, PSLF requires consistent employment in eligible sectors and adherence to specific repayment plans, such as income-driven options.

Another example is income-driven repayment (IDR) plans, which cap monthly payments at a percentage of discretionary income and offer forgiveness after 20–25 years, depending on the plan. During 0% interest periods, borrowers on IDR plans can minimize their overall debt burden by avoiding interest accrual while making qualifying payments. For instance, a borrower on the Revised Pay As You Earn (REPAYE) plan could see their remaining balance forgiven after 20–25 years, with the added benefit of no interest compounding during the interest-free period.

It’s essential to note that loan forgiveness programs often come with tax implications, as forgiven amounts may be treated as taxable income. For example, PSLF is tax-free, but forgiveness through IDR plans typically requires borrowers to pay taxes on the forgiven amount. Strategic planning, such as setting aside funds during 0% interest periods to cover potential tax liabilities, can mitigate this financial burden.

In summary, while 0% interest on student loans provides immediate relief, loan forgiveness programs offer long-term solutions for eliminating debt. By understanding the nuances of programs like PSLF and IDR, borrowers can maximize the benefits of interest-free periods and work toward a debt-free future. Pairing these strategies requires careful planning, but the potential payoff—freedom from student loan debt—is well worth the effort.

When Will Student Loan Forgiveness Be Unblocked: Latest Updates

You may want to see also

Explore related products

![]()

Post-pandemic interest resumption dates

The pause on federal student loan interest, a lifeline for millions during the pandemic, ended on September 1, 2023. This resumption marks a critical shift for borrowers, who must now factor interest accrual back into their repayment strategies. Understanding the timeline and implications of this change is essential for financial planning.

For context, the 0% interest rate was part of the CARES Act, implemented in March 2020 to alleviate economic strain. Extended multiple times, this benefit lasted over three years, saving borrowers billions in interest. However, the resumption date was always a known eventuality, though its exact timing was subject to political and economic factors. Borrowers who planned ahead by making voluntary payments during the pause effectively reduced their principal balance, positioning themselves better for the interest restart.

The resumption of interest accrual does not coincide with the restart of payments, which began in October 2023. This distinction is crucial: interest began compounding again on September 1, meaning balances grew even before payments were required. For example, a borrower with a $30,000 loan at 5% interest would see their balance increase by approximately $125 in the month of September alone. This underscores the importance of resuming payments promptly to minimize long-term costs.

To navigate this transition, borrowers should first confirm their loan servicer and update contact information to avoid missing critical notices. Next, evaluate repayment plans, particularly income-driven options, which can cap monthly payments based on earnings. Refinancing with private lenders is another strategy, but it forfeits federal benefits like forgiveness programs. Finally, consider budgeting tools or financial counseling to adjust to the new financial reality.

In summary, the post-pandemic interest resumption date of September 1, 2023, demands proactive measures. By understanding the timeline, preparing for increased balances, and exploring repayment options, borrowers can mitigate the impact of this change. The end of 0% interest is not just a return to pre-pandemic norms but a call to action for informed financial management.

Great Lakes Loans: Eligibility for Student Loan Forgiveness Explained

You may want to see also

Frequently asked questions

The duration of 0% interest on student loans depends on the specific policy or program. For example, during the COVID-19 pandemic, the U.S. government paused interest on federal student loans, but this was a temporary measure. Always check the latest updates from your loan servicer or government announcements for current details.

No, 0% interest on student loans is typically a temporary measure. It is often implemented during specific periods, such as economic crises or emergencies, and will end once the designated period concludes.

When the 0% interest period ends, interest will resume accruing on your student loans at the standard rate specified in your loan agreement. Payments may also restart, depending on the terms of the program or policy. Be prepared to resume regular payments and interest accumulation.