The issue of student debt has become a pressing concern in today's society, as the rising cost of higher education continues to outpace inflation and wage growth. With college tuition fees soaring and living expenses increasing, many students are forced to take out substantial loans to finance their education. As a result, the question of how many students will be in debt after college is a critical one, as it highlights the long-term financial implications of pursuing a degree. Recent studies suggest that a significant proportion of graduates will face substantial debt burdens, with many struggling to repay their loans in a timely manner. This trend not only affects individual students but also has broader economic consequences, as high levels of student debt can hinder economic mobility, reduce consumer spending, and limit opportunities for wealth accumulation.

| Characteristics | Values |

|---|---|

| Percentage of college graduates with debt | Approximately 65% (Class of 2022, Education Data Initiative) |

| Average student loan debt | $28,950 (Class of 2022, Education Data Initiative) |

| Total student loan debt in the U.S. | Over $1.7 trillion (as of 2023, Federal Reserve) |

| Percentage of borrowers under 30 | 38% (Federal Reserve, 2023) |

| Percentage of borrowers aged 30-49 | 40% (Federal Reserve, 2023) |

| Percentage of borrowers with private loans | 13% (Education Data Initiative, 2022) |

| Percentage of borrowers with federal loans | 87% (Education Data Initiative, 2022) |

| Average monthly loan payment | $393 (Education Data Initiative, 2022) |

| Percentage of students borrowing for college | 43% of undergraduate students (National Center for Education Statistics, 2021-2022) |

| Debt burden by degree type | Bachelor's degree: $30,000; Graduate degree: $71,000 (Education Data Initiative, 2022) |

| Percentage of Black students with debt | 83% (Education Data Initiative, 2022) |

| Percentage of White students with debt | 69% (Education Data Initiative, 2022) |

| Percentage of Hispanic students with debt | 64% (Education Data Initiative, 2022) |

| Percentage of students defaulting on loans | 7.3% (Cohort default rate, U.S. Department of Education, 2020) |

Explore related products

What You'll Learn

- Average Student Loan Debt: National and global statistics on student debt post-graduation

- Debt by Degree Type: Debt levels for associate, bachelor’s, and graduate degrees

- Repayment Challenges: Factors like unemployment and low wages affecting debt repayment

- Debt by Institution: Comparison of debt levels from public vs. private colleges

- Debt Forgiveness Programs: Availability and impact of loan forgiveness initiatives

![]()

Average Student Loan Debt: National and global statistics on student debt post-graduation

Student loan debt has become a defining financial burden for millions of graduates worldwide. In the United States, the average student loan debt for the class of 2023 stands at approximately $28,800, according to data from the Education Data Initiative. This figure varies significantly by state, with graduates in states like New Hampshire and Pennsylvania facing averages exceeding $39,000, while those in Utah and Wyoming carry less than $19,000. These disparities reflect differences in tuition costs, availability of scholarships, and local economic conditions. Globally, the picture is equally stark. In the UK, the average student debt for 2023 graduates is around £45,000 (approximately $57,000), largely due to higher tuition fees at institutions like Oxford and Cambridge. Meanwhile, countries like Germany and Norway offer tuition-free or low-cost education, resulting in minimal or no student debt for their graduates.

Analyzing these statistics reveals a clear trend: the higher the cost of education, the greater the debt burden. In the U.S., for instance, students attending private colleges graduate with an average debt of $33,000, compared to $23,000 for public college graduates. This gap underscores the impact of institutional pricing on long-term financial health. Globally, the contrast between tuition-free systems and high-cost models highlights the role of government policy in shaping student debt outcomes. For example, Canada’s average student debt of $28,000 is mitigated by provincial loan assistance programs, while Australia’s income-contingent loan system caps repayments at a percentage of earnings, reducing financial strain on graduates.

To navigate this landscape, graduates must adopt practical strategies to manage their debt effectively. One key step is to understand the terms of repayment plans. In the U.S., federal loan borrowers can opt for income-driven repayment plans, which cap monthly payments at 10–20% of discretionary income. Similarly, UK graduates repay loans only when earning above £27,295 annually, with payments scaling based on income. Another strategy is to prioritize high-interest debt. For example, private student loans in the U.S. often carry interest rates above 10%, making them a costly burden. Refinancing these loans at lower rates can save thousands over the repayment period. Additionally, graduates should explore loan forgiveness programs, such as the U.S. Public Service Loan Forgiveness program, which forgives remaining debt after 10 years of qualifying payments in public service roles.

Comparing national approaches to student debt reveals opportunities for reform. Countries like Sweden and New Zealand offer interest-free student loans, significantly reducing the long-term cost of borrowing. In contrast, the U.S. and UK systems, while offering repayment flexibility, often leave graduates with decades of debt. Policymakers could draw lessons from these models to design more equitable systems. For instance, capping interest rates or expanding grant-based aid could alleviate the burden on students. Graduates themselves can advocate for such changes while taking proactive steps to manage their debt, such as budgeting rigorously and seeking employer-sponsored repayment assistance programs.

Ultimately, the global student debt crisis demands both individual action and systemic change. Graduates must educate themselves on repayment options and leverage available tools to minimize their financial strain. Simultaneously, governments and institutions should reevaluate funding models to ensure education remains a pathway to opportunity, not a source of lifelong debt. By combining personal strategies with advocacy for broader reform, graduates can navigate their debt more effectively while contributing to a more sustainable future for higher education.

Forgiving Student Loan Debt: Inflationary Impact or Economic Boost?

You may want to see also

Explore related products

$14.99 $14.99

![]()

Debt by Degree Type: Debt levels for associate, bachelor’s, and graduate degrees

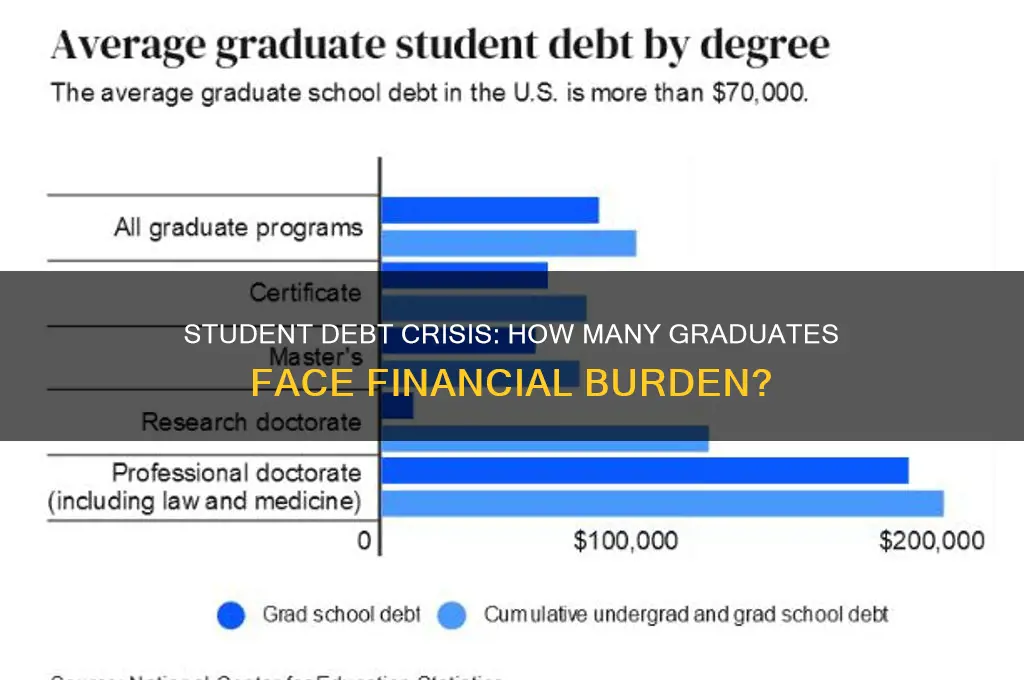

The type of degree a student pursues significantly influences their debt burden upon graduation. Associate degrees, typically completed in two years, often result in the lowest average debt. According to recent data, students earning associate degrees graduate with an average debt of $8,000 to $13,000. This is largely due to the lower cost of community colleges and shorter program duration, making it a more affordable option for those seeking quick entry into the workforce or a stepping stone to a bachelor’s degree. However, the return on investment varies by field; technical and vocational programs often yield higher starting salaries, offsetting the debt more effectively than liberal arts or general studies programs.

Bachelor’s degrees, the most common undergraduate credential, come with a steeper price tag. Graduates with a bachelor’s degree typically carry an average debt of $25,000 to $30,000, though this can soar to $50,000 or more at private institutions or out-of-state public universities. The longer duration of these programs, combined with rising tuition costs, contributes to higher debt levels. Yet, bachelor’s degree holders generally earn significantly more than those with only a high school diploma, often justifying the investment. For instance, the median weekly earnings for bachelor’s degree holders are nearly double those of high school graduates, according to the Bureau of Labor Statistics.

Graduate degrees represent the highest level of education but also the most substantial debt. Students pursuing master’s degrees graduate with an average debt of $40,000 to $55,000, while those completing professional degrees (e.g., law, medicine) often face debts exceeding $100,000. The rationale for such high debt lies in the potential for significantly higher earnings in specialized fields. For example, medical doctors and lawyers frequently earn six-figure salaries, making the debt manageable over time. However, this is not universal; graduates in fields like social work or the arts may struggle to repay loans on lower salaries, highlighting the importance of aligning degree choice with career goals and earning potential.

A comparative analysis reveals a clear trend: debt increases with the level of education, but so does earning potential. Associate degrees offer a low-debt pathway with moderate returns, bachelor’s degrees balance higher debt with stronger earnings, and graduate degrees carry the highest risk but also the greatest reward. Prospective students should weigh these factors carefully, considering not only the cost of tuition but also the long-term financial outlook of their chosen field. Practical tips include researching average salaries for specific degrees, exploring scholarships and grants to reduce reliance on loans, and attending in-state public institutions to minimize costs. Ultimately, the decision should align with both personal aspirations and financial realities.

FAA Employment: Eligible for Student Loan Forgiveness Programs?

You may want to see also

Explore related products

![]()

Repayment Challenges: Factors like unemployment and low wages affecting debt repayment

Student debt doesn't vanish at graduation. For many, it lingers, a financial albatross exacerbated by the harsh realities of the post-college landscape. Unemployment, a specter haunting recent graduates, throws a wrench into even the most meticulously planned repayment strategies. Imagine graduating with a degree in hand, only to face a job market offering limited opportunities. Months, even years, of job searching can quickly deplete savings, forcing borrowers to defer payments, accruing interest that balloons the original debt.

A 2022 study by the Federal Reserve found that 43% of recent college graduates were either unemployed or underemployed, highlighting the precarious position many find themselves in when attempting to repay student loans.

Low wages, another common hurdle, further complicate the repayment journey. Entry-level positions often offer salaries barely sufficient to cover living expenses, leaving little room for substantial loan payments. Consider a graduate with $30,000 in debt and a starting salary of $40,000. After taxes and living expenses, the remaining amount for loan repayment might be a mere $200-$300 per month, resulting in a repayment period stretching over decades. This prolonged repayment timeline not only extends the financial burden but also limits opportunities for saving, investing, or achieving other financial goals.

The average student loan payment for borrowers aged 25-34 is $393, according to the Federal Reserve, a significant chunk of income for those starting their careers.

The interplay of unemployment and low wages creates a vicious cycle. Unemployment leads to deferred payments and accruing interest, while low wages make it difficult to catch up even when employed. This cycle can trap borrowers in a state of perpetual financial stress, impacting their overall well-being and limiting their ability to build a secure future.

Breaking this cycle requires a multi-pronged approach. Graduates should prioritize building emergency funds to weather periods of unemployment. Exploring income-driven repayment plans can adjust monthly payments based on income, providing temporary relief. Additionally, advocating for policies that address the root causes of unemployment and stagnant wages is crucial for creating a more sustainable environment for student loan repayment.

Who Qualifies for Student Loan Forgiveness? Eligibility Explained

You may want to see also

Explore related products

![]()

Debt by Institution: Comparison of debt levels from public vs. private colleges

The choice between public and private colleges significantly influences student debt levels, with private institutions often leading to higher financial burdens. Data from the College Board reveals that the average debt for graduates of private nonprofit colleges is approximately $32,600, compared to $22,000 for public college graduates. This disparity stems from higher tuition costs at private schools, even when accounting for financial aid. For instance, the average annual tuition for a private college is $38,070, while public institutions charge $10,740 for in-state students. Families considering these options must weigh the potential return on investment, as private colleges may offer more personalized resources but at a steeper price.

Analyzing the factors behind these debt disparities highlights the role of institutional funding models. Public colleges receive state funding, which helps keep tuition lower, whereas private colleges rely heavily on tuition and endowments. However, private schools often provide more generous merit-based aid, which can offset costs for some students. A practical tip for prospective students is to compare net prices—the actual cost after grants and scholarships—rather than sticker prices. Tools like the College Scorecard can help families estimate debt based on institutional type and financial aid packages.

A persuasive argument for attending public colleges centers on their accessibility and lower debt outcomes. For students prioritizing affordability, public institutions offer a clear advantage. For example, in-state residents can save over $100,000 in tuition alone by choosing a public university over a private one. While private colleges may boast higher graduation rates and smaller class sizes, the long-term financial strain of debt can outweigh these benefits. Graduates with lower debt are better positioned to pursue career opportunities without being constrained by loan repayments.

Comparatively, private colleges may justify their higher costs through specialized programs, alumni networks, and research opportunities. However, this trade-off is not always equitable. Students from low-income backgrounds, in particular, may struggle to manage the debt burden of private institutions, even with financial aid. A cautionary note is that while private colleges often have larger endowments, not all students receive substantial aid. Families should scrutinize aid packages and consider the long-term implications of borrowing for a private education.

In conclusion, the decision between public and private colleges should be guided by a realistic assessment of financial impact. Public institutions offer a more affordable path with lower average debt, making them a prudent choice for budget-conscious students. Private colleges, while potentially offering unique advantages, come with a higher price tag that can lead to significant debt. By carefully evaluating net costs and future earnings potential, students can make informed decisions that align with their financial goals and minimize post-graduation stress.

Understanding the Timeline for Consolidating Student Loan Forgiveness Programs

You may want to see also

Explore related products

![]()

Debt Forgiveness Programs: Availability and impact of loan forgiveness initiatives

Student debt is a looming reality for millions of graduates, with recent statistics indicating that over 43 million Americans owe a collective $1.7 trillion in student loans. This financial burden often delays major life milestones like homeownership, starting a family, or even pursuing further education. Amidst this crisis, debt forgiveness programs have emerged as a beacon of hope, offering a pathway to financial freedom for eligible borrowers. However, the availability and impact of these initiatives vary widely, leaving many to navigate a complex landscape of eligibility criteria, application processes, and long-term benefits.

One of the most prominent examples is the Public Service Loan Forgiveness (PSLF) program, designed for borrowers who commit to working in public service roles for 10 years while making qualifying payments. While the program promises to forgive the remaining balance, its impact has been limited due to stringent eligibility rules and administrative hurdles. For instance, only 2% of applicants have received forgiveness since the program’s inception, highlighting the gap between promise and practice. Borrowers must meticulously track their payments and ensure their employer qualifies, a task easier said than done. Despite its flaws, PSLF remains a critical lifeline for those in qualifying professions, such as teachers, nurses, and nonprofit workers.

Another initiative, the Income-Driven Repayment (IDR) plans, ties monthly payments to a borrower’s income and offers forgiveness after 20–25 years of consistent payments. While this program is more accessible, its long-term impact is often overshadowed by accruing interest, which can balloon the total debt over time. For example, a borrower with $50,000 in loans at a 6% interest rate could end up paying nearly $80,000 over 25 years, even before forgiveness kicks in. This underscores the importance of understanding the trade-offs between immediate payment relief and long-term financial obligations.

The recent one-time student debt cancellation initiatives, such as the Biden administration’s proposal to forgive up to $20,000 for eligible borrowers, have sparked both hope and controversy. While such broad-scale forgiveness could alleviate debt for millions, its implementation faces legal and political challenges. For instance, the Supreme Court’s 2023 ruling blocked the plan, leaving borrowers in limbo. This highlights the precarious nature of relying on policy-driven solutions, which are often subject to shifting political winds.

To maximize the benefits of debt forgiveness programs, borrowers should take proactive steps. First, research all available options, including state-specific programs like the New York State Young Farmers Loan Forgiveness Incentive Program, which offers up to $10,000 annually for farmers under 40. Second, maintain detailed records of payments and employment, especially for programs like PSLF. Finally, consult with a financial advisor or loan counselor to tailor a strategy to individual circumstances. While debt forgiveness programs are not a panacea, they offer tangible relief for those who navigate their complexities with care and diligence.

Biden Student Loan Forgiveness: Do You Need to Apply?

You may want to see also

Frequently asked questions

Approximately 65% of college students in the United States graduate with student loan debt, according to recent data.

The average student loan debt for college graduates is around $28,000, though this varies by institution type, degree level, and other factors.

Students from private colleges tend to graduate with higher average debt, often exceeding $30,000, compared to students from public colleges, who average around $25,000 in debt.