Navient, one of the largest student loan servicers in the United States, offers various forgiveness programs that can help borrowers reduce or eliminate their student loan debt, but the number of years it takes for Navient to forgive loans depends on the specific program and the borrower's eligibility. For instance, Public Service Loan Forgiveness (PSLF) requires 120 qualifying payments, typically spanning 10 years, while income-driven repayment plans like Income-Based Repayment (IBR) or Pay As You Earn (PAYE) may offer forgiveness after 20 to 25 years of consistent payments. Additionally, Navient may also participate in loan forgiveness programs tied to specific professions, such as teacher loan forgiveness, which can reduce debt after 5 years of eligible service. Understanding the terms and requirements of these programs is crucial for borrowers seeking relief from their student loans.

Explore related products

What You'll Learn

![]()

Income-Driven Repayment Forgiveness

Income-Driven Repayment (IDR) plans offer a lifeline to borrowers struggling with federal student loans, including those serviced by Navient. These plans tie monthly payments to income and family size, ensuring affordability. But the real game-changer? After 20 or 25 years of consistent payments, the remaining balance is forgiven. This isn’t a loophole—it’s a built-in feature designed to prevent lifelong debt for low-income earners. However, the clock doesn’t start ticking until you enroll in an IDR plan, so procrastination can cost you years of eligibility.

To qualify for forgiveness, you must stick to an IDR plan like Income-Based Repayment (IBR), Pay As You Earn (PAYE), or Revised Pay As You Earn (REPAYE). Each plan has unique eligibility rules, but all require annual recertification of income and family size. Miss a recertification deadline, and you risk being kicked out of the program, resetting your forgiveness timeline. For example, if you’re single with an income of $40,000 and $50,000 in loans, your monthly payment under REPAYE would be roughly $125, compared to $500 under the Standard 10-year plan. Over 25 years, that’s a savings of $95,000—plus forgiveness of any remaining balance.

Tax implications are a critical but often overlooked aspect of IDR forgiveness. The forgiven amount is typically treated as taxable income, which could result in a hefty bill come tax season. For instance, if $30,000 is forgiven, you might owe $7,500 in taxes (assuming a 25% tax bracket). However, the *American Rescue Act of 2021* temporarily waives taxes on forgiven student loans through 2025, providing a window of relief. Planning ahead by setting aside funds or consulting a tax professional can soften the blow when this provision expires.

Choosing the right IDR plan requires strategy. REPAYE caps payments at 10% of discretionary income and offers interest subsidies, making it ideal for borrowers with high debt-to-income ratios. IBR, on the other hand, limits payments to 10% or 15% of discretionary income, depending on when the loan was taken out, and forgives after 20 or 25 years. PAYE is the most restrictive, requiring loans taken out after October 2007 and capping payments at 10% of income. A 30-year-old teacher with $80,000 in loans, for example, might save $60,000 over 20 years under IBR compared to the Standard plan.

Finally, Navient’s role in this process is administrative—they service the loan but don’t control the forgiveness terms, which are set by federal law. Borrowers must proactively manage their accounts, ensuring payments are counted toward IDR forgiveness. Mistakes like misapplied payments or missed recertifications are common, so documenting every interaction and keeping records is essential. While the path to forgiveness is long, IDR plans transform student loans from a burden into a manageable commitment, offering a clear end date for those who play by the rules.

Budget Cuts Threaten Student Loan Forgiveness: What Borrowers Need to Know

You may want to see also

Explore related products

![]()

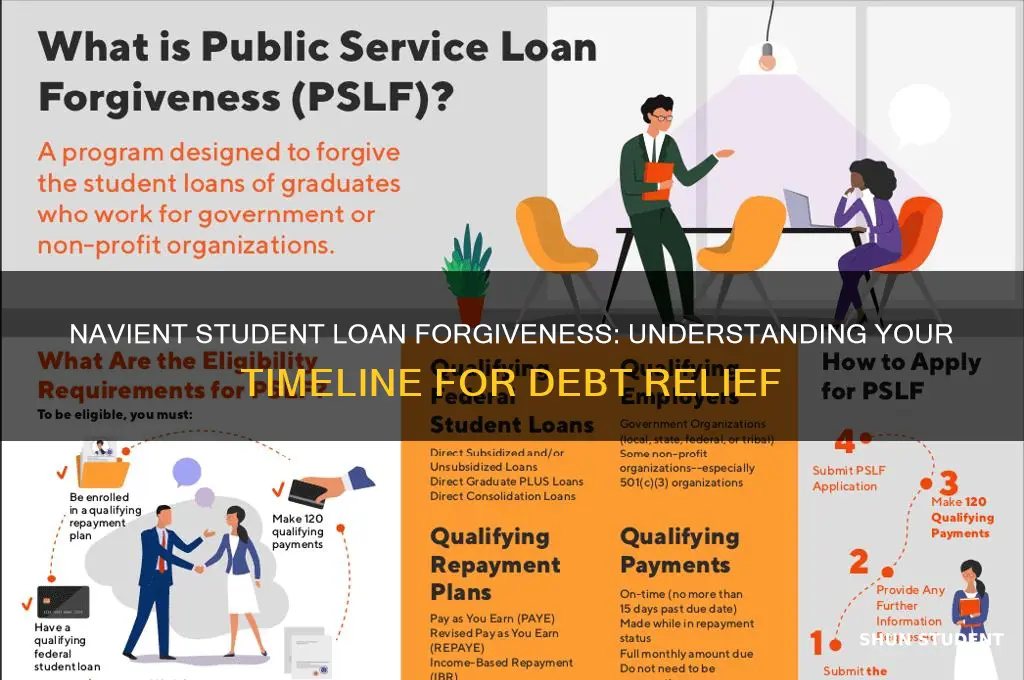

Public Service Loan Forgiveness (PSLF)

One critical aspect of PSLF is ensuring your loans are eligible. Only Direct Loans qualify, so if you have Federal Family Education Loans (FFEL) or Perkins Loans, you’ll need to consolidate them into a Direct Consolidation Loan. This step is non-negotiable—without it, your payments won’t count toward PSLF, even if you work in public service. For instance, a teacher with $50,000 in FFEL loans who consolidates into a Direct Loan can start the 120-payment clock immediately, whereas those who skip consolidation remain ineligible.

Navigating PSLF requires vigilance and documentation. Submit the Employment Certification Form (ECF) annually or whenever you change employers to ensure your payments are tracking correctly. This form verifies your employer’s eligibility and the number of qualifying payments you’ve made. A common pitfall is assuming your payments are counting without confirmation—a mistake that can cost you years of progress. For example, a social worker who changes jobs every three years could lose track of their payment count without consistent ECF submissions.

Finally, PSLF isn’t a quick fix—it takes at least 10 years of commitment to public service. However, the payoff is significant: any remaining balance is forgiven tax-free after 120 payments. Compare this to income-driven plans, which forgive debt after 20–25 years but may require paying taxes on the forgiven amount. For a nurse earning $60,000 with $100,000 in debt, PSLF could save tens of thousands of dollars compared to other forgiveness options. The key is staying informed, organized, and dedicated to the process.

Student Loan Forgiveness After Death: A Guide for Borrowers

You may want to see also

Explore related products

![]()

Teacher Loan Forgiveness Program

Teachers burdened by student loan debt have a powerful ally in the Teacher Loan Forgiveness Program. This federal initiative offers a clear path to reducing, or even eliminating, a portion of your loans after a committed period of service.

Here's the breakdown: after completing five consecutive, full-time academic years of teaching in a low-income school or educational service agency, you could qualify for forgiveness of up to $17,500 on your Direct Subsidized and Unsubsidized Loans. This program specifically targets those who dedicate themselves to serving communities with the greatest need, making a tangible difference in the lives of students while simultaneously easing their own financial burden.

Eligibility hinges on more than just time served. The school or agency you teach in must be designated as low-income by the Department of Education, and your teaching must be your primary responsibility. Secondary roles like coaching or administrative duties don't count towards the required years. It's crucial to verify your school's eligibility status annually, as it can change.

While Navient, as a loan servicer, doesn't directly "forgive" loans, they play a crucial role in the process. They manage your loan account, process your payments, and, importantly, submit the necessary paperwork to the Department of Education once you've completed your qualifying service. Think of them as the administrative bridge between your dedication in the classroom and the financial relief you've earned.

Keep in mind, this program isn't a quick fix. It requires a sustained commitment to teaching in underserved communities. However, for those passionate about education and seeking long-term financial stability, the Teacher Loan Forgiveness Program offers a rewarding path forward.

To maximize your chances of success, stay organized. Keep meticulous records of your teaching years, school eligibility status, and any communication with Navient. Don't hesitate to reach out to your loan servicer with questions – they are there to guide you through the process. Remember, this program is an investment in both your future and the future of the students you serve.

Understanding Student Loan Non-Profit Forgiveness: A Comprehensive Guide

You may want to see also

Explore related products

$8.34 $17.99

![]()

Disability Discharge Options

If you’re struggling with student loans due to a disability, Navient offers a pathway to relief through its Disability Discharge Options. This federal program allows borrowers to have their loans forgiven if they meet specific criteria, providing a financial lifeline for those facing long-term health challenges. Understanding the process and requirements is crucial to navigating this option successfully.

Eligibility hinges on proving a permanent disability, as defined by the U.S. Department of Education. This includes conditions that prevent you from engaging in substantial gainful activity, as certified by a physician, the Social Security Administration (SSA), or the Department of Veterans Affairs (VA). For SSA recipients, you must provide documentation of benefits received under Title II or Title XVI of the Social Security Act, with a review period of five to seven years. VA beneficiaries need proof of a service-related disability with a 100% rating. Physician certification requires a licensed doctor to confirm your inability to work due to a physical or mental impairment expected to last continuously for at least 60 months or result in death.

The application process involves submitting detailed documentation to Navient’s designated servicer for disability discharge. For SSA recipients, this includes a Benefits Planning Query (BPQY) or Notice of Award letter. VA beneficiaries must provide a certification letter confirming their disability rating. Physician certification requires a completed form from a doctor, which can be found on the Federal Student Aid website. Once submitted, Navient will review your application, and if approved, your loans will be discharged, freeing you from repayment obligations.

A critical aspect to note is the three-year monitoring period that follows a disability discharge. During this time, you must not earn income exceeding the poverty guideline for your family size, take out additional federal student loans, or receive a new Direct Loan or TEACH Grant. Failure to comply may result in loan reinstatement. However, if you meet all conditions during this period, the discharge becomes permanent, and your loans are forgiven.

Practical tips for a smoother process include gathering all necessary documents before applying and keeping copies for your records. If you’re unsure about eligibility or the application process, contact Navient’s disability services team for guidance. Additionally, consider consulting with a financial advisor or disability advocate to ensure you’re maximizing all available resources. Disability discharge isn’t just a legal process—it’s a chance to reclaim financial stability in the face of adversity.

PhD Loan Forgiveness: Strategies to Erase Your Student Debt

You may want to see also

Explore related products

$6.99

![]()

Loan Forgiveness for Borrower Defense

Borrowers who believe they were defrauded by their college or university may qualify for loan forgiveness through the Borrower Defense to Repayment (BDTR) program. This federal initiative offers a lifeline to those burdened by student debt incurred at institutions that misled them or violated state laws. For Navient borrowers, understanding the BDTR process is crucial, as it could mean the difference between years of repayment and complete loan discharge.

To initiate the BDTR process, borrowers must submit a formal claim to the U.S. Department of Education, detailing the alleged misconduct by their school. This claim should include evidence of the institution's wrongdoing, such as misleading advertising, falsified job placement rates, or accreditation issues. Navient, as the loan servicer, plays a limited role in this process, as the decision to grant forgiveness rests solely with the Department of Education. However, borrowers should continue making payments until their claim is approved to avoid delinquency.

The timeline for BDTR approval varies significantly, with some cases resolved within months and others taking years. Factors influencing this duration include the complexity of the claim, the volume of applications, and the Department of Education's current processing capacity. Historically, successful BDTR claims have resulted in full loan forgiveness, including principal and interest, as well as refunds for prior payments. For instance, students of Corinthian Colleges and ITT Tech have received substantial relief through this program.

While BDTR offers a promising avenue for loan forgiveness, it is not without challenges. Borrowers must navigate a detailed application process and provide compelling evidence to support their claims. Additionally, the program has faced political and administrative hurdles, leading to delays and uncertainty. To maximize their chances of success, borrowers should: (1) gather all relevant documentation, (2) consult with legal aid or advocacy groups, and (3) remain persistent in following up with the Department of Education. For Navient borrowers, staying informed and proactive is key to unlocking potential forgiveness through Borrower Defense.

Understanding the Allocation Process for Student Loan Forgiveness Programs

You may want to see also

Frequently asked questions

Navient, as a loan servicer, administers forgiveness through federal programs like Income-Driven Repayment (IDR). Forgiveness typically occurs after 20–25 years of qualifying payments, depending on the plan.

Navient does not offer 10-year forgiveness directly. However, Public Service Loan Forgiveness (PSLF) forgives loans after 10 years of qualifying payments and employment in public service, which Navient services.

If you’ve made 20 years of qualifying payments under an income-driven plan serviced by Navient, you may be eligible for loan forgiveness through the federal government, not Navient directly.