The topic of student loan debt is a pressing concern for many individuals pursuing higher education. The cost of tuition, fees, and living expenses can quickly accumulate, leading students to rely on loans to finance their studies. However, the long-term financial implications of these loans can be significant, with interest rates and repayment terms that may result in students paying back substantially more than they initially borrowed. This paragraph aims to delve into the complexities of student loan debt, exploring the various factors that contribute to the final amount students end up paying after taking out loans for their education.

Explore related products

What You'll Learn

- Tuition Fees: Breakdown of average costs across different institutions and programs

- Room and Board: Estimating living expenses on and off campus

- Books and Supplies: Average costs for educational materials

- Loan Interest Rates: Overview of current interest rates for student loans

- Repayment Plans: Different strategies and timelines for repaying student loans

![]()

Tuition Fees: Breakdown of average costs across different institutions and programs

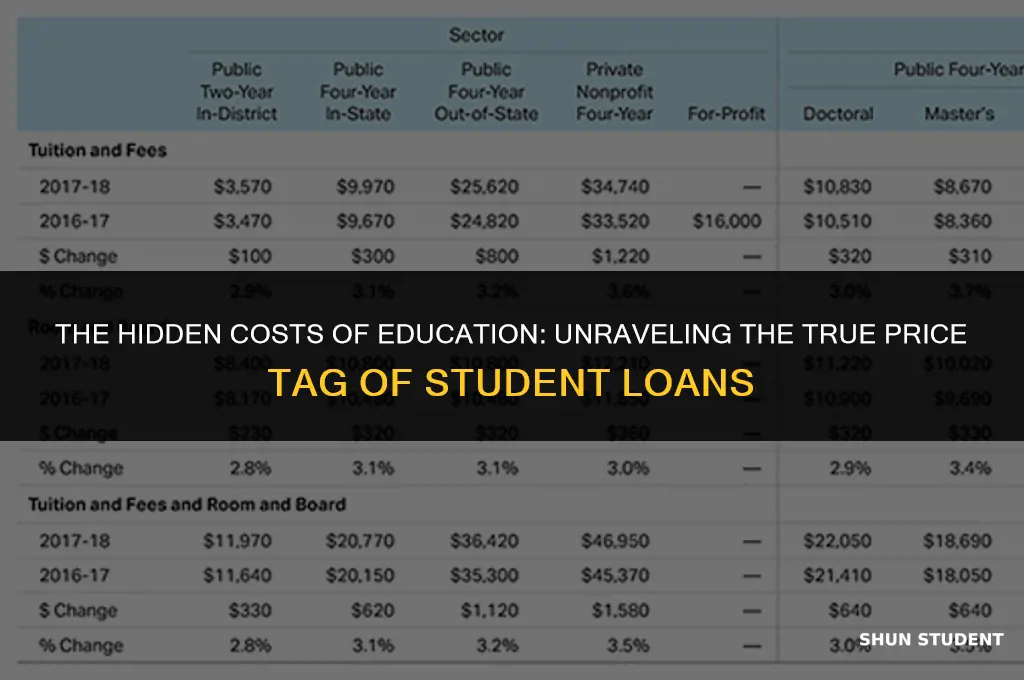

The cost of higher education varies significantly depending on the institution and program chosen. Public universities generally offer lower tuition fees compared to private institutions. For instance, the average annual tuition fee for an undergraduate degree at a public university in the United States is approximately $7,250 for in-state students and $21,180 for out-of-state students. In contrast, private universities can charge upwards of $30,000 to $60,000 per year.

Furthermore, the type of program also impacts tuition fees. STEM programs, such as engineering and computer science, often have higher fees due to the specialized resources and facilities required. On the other hand, humanities and social sciences programs tend to be less expensive. For example, a four-year engineering degree at a top-tier private university can cost over $200,000, while a similar program in the humanities may cost around $150,000.

It's also important to consider additional fees that can add up over the course of a student's education. These may include application fees, enrollment fees, technology fees, and parking fees. For instance, some universities charge an application fee of $50 to $100, while others may waive this fee for certain applicants. Enrollment fees, which cover the cost of registering for classes, can range from $100 to $500 per semester.

In addition to tuition and fees, students must also consider the cost of living, which can vary greatly depending on the location of the institution. For example, a student attending a university in a major city like New York or San Francisco will likely face higher living expenses compared to a student attending a university in a smaller town or rural area. On-campus housing and meal plans can also add significant costs, with some universities charging over $10,000 per year for room and board.

To get a better understanding of the total cost of attendance, students should research the specific institutions and programs they are interested in and create a budget that includes tuition, fees, living expenses, and other costs. This will help them make informed decisions about their education and plan accordingly for the financial commitment required.

The Cost of Knowledge: A Breakdown of Book Expenses for CSUF Students

You may want to see also

Explore related products

![]()

Room and Board: Estimating living expenses on and off campus

Estimating living expenses is a crucial step in understanding the total cost of attending college. Room and board, which typically includes housing and meals, can vary significantly depending on whether a student chooses to live on or off campus. On-campus living often involves residence halls or dormitories, which may offer a range of amenities such as meal plans, laundry facilities, and security services. These costs are usually bundled together and can be paid directly to the college or university.

Off-campus living, on the other hand, requires students to secure their own housing, which could be an apartment, house, or room rental. This option may offer more flexibility and independence but also comes with additional responsibilities such as utility bills, groceries, and transportation costs. Students living off campus may need to budget for unexpected expenses like furniture, household items, and potential repairs.

To accurately estimate room and board expenses, students should research the average costs in their chosen area, considering factors such as location, housing type, and lifestyle preferences. Online resources, local real estate listings, and student forums can provide valuable insights into the cost of living in a particular region. Additionally, students should factor in the cost of meal plans or groceries, depending on their living arrangements, and consider any potential savings from cooking at home or using campus dining facilities.

When comparing on-campus and off-campus living expenses, it's essential to weigh the pros and cons of each option. While on-campus living may offer convenience and a sense of community, off-campus living can provide more privacy and potentially lower costs, depending on the location and housing choice. Students should also consider the impact of living expenses on their overall financial aid package, as room and board costs can significantly affect the amount of loans and grants they receive.

Ultimately, understanding and estimating room and board expenses is a critical component of financial planning for college students. By carefully considering their options and budgeting accordingly, students can make informed decisions about their living arrangements and minimize the financial burden of higher education.

Decoding Student Worker Wages: A Comprehensive Guide to Earnings

You may want to see also

Explore related products

![]()

Books and Supplies: Average costs for educational materials

The cost of educational materials can significantly impact a student's overall expenses. Books and supplies are essential for most courses, and their prices can vary widely depending on the institution and the field of study. On average, students can expect to spend between $1,000 and $2,000 per year on books and supplies, according to recent estimates. However, this figure can be much higher for certain majors, such as engineering or architecture, where specialized textbooks and software are required.

One way to reduce costs is to purchase used books or rent them from online retailers. Many students also opt to buy digital versions of textbooks, which can be more affordable and convenient for accessing course materials. Additionally, some institutions offer book rental programs or have partnerships with local bookstores to provide discounted rates for students.

Another factor to consider is the cost of supplies, which can include everything from notebooks and pens to lab equipment and art supplies. These expenses can add up quickly, especially for students who need to purchase specialized items for their courses. To save money, students can shop around for the best prices, take advantage of sales and discounts, and consider purchasing generic or off-brand products.

Financial aid can also play a role in covering the costs of educational materials. Many scholarships and grants specifically target students who need assistance with purchasing books and supplies. Additionally, some institutions offer emergency funds or book vouchers to students who are struggling to afford their course materials.

In conclusion, the cost of books and supplies is an important consideration for students when budgeting for their education. By exploring different options for purchasing materials, taking advantage of financial aid, and being mindful of their spending, students can reduce their overall expenses and focus on their academic success.

Unveiling the Pay Scale for Student Workers at CSUEB

You may want to see also

Explore related products

![]()

Loan Interest Rates: Overview of current interest rates for student loans

As of 2023, the interest rates for federal student loans in the United States range from 4.99% to 7.54%, depending on the type of loan and the borrower's undergraduate or graduate status. These rates are fixed for the life of the loan, meaning they do not fluctuate with market conditions. However, they are subject to change by Congress and have historically been adjusted in response to economic conditions and policy decisions.

For private student loans, interest rates can vary widely among lenders and are often based on the borrower's creditworthiness. Rates can be fixed or variable, with variable rates typically tied to a benchmark such as the LIBOR or Prime rate. As of 2023, private student loan interest rates range from around 5% to over 12%, with some lenders offering rates as low as 3% for highly qualified borrowers.

When considering the total cost of student loans, it's important to factor in not just the principal amount borrowed, but also the interest that accrues over time. For example, a $30,000 loan with a 5% interest rate would result in approximately $8,000 in interest paid over a 10-year repayment period, bringing the total cost to around $38,000. This highlights the importance of understanding and comparing interest rates when taking out student loans, as even a small difference in rates can significantly impact the total amount paid over the life of the loan.

In addition to interest rates, borrowers should also be aware of fees associated with student loans, such as origination fees, late payment fees, and prepayment penalties. These fees can add to the overall cost of the loan and should be considered when comparing loan options. Furthermore, borrowers may be eligible for certain benefits or discounts, such as interest rate reductions for setting up automatic payments or for having a cosigner with good credit.

To minimize the total cost of student loans, borrowers should aim to pay off their loans as quickly as possible, taking advantage of any opportunities to make extra payments or refinance to a lower interest rate. Additionally, borrowers should carefully consider their repayment plan options, such as income-driven repayment plans, which can help manage monthly payments but may result in more interest paid over time.

In conclusion, understanding and comparing loan interest rates is crucial for students and borrowers to make informed decisions about their student loan options. By considering factors such as fixed vs. variable rates, fees, and repayment plan options, borrowers can better navigate the complexities of student loan financing and work towards minimizing the total cost of their education.

Unlocking Education in Spain: A Guide to Student Visa Costs

You may want to see also

Explore related products

![]()

Repayment Plans: Different strategies and timelines for repaying student loans

Navigating the complex landscape of student loan repayment can be daunting, but understanding the various repayment plans available can empower borrowers to make informed decisions. The Standard Repayment Plan, for instance, offers a straightforward approach, spreading payments evenly over a 10-year period. This plan is ideal for those who can afford consistent monthly payments and want to pay off their loans as quickly as possible. However, for borrowers with lower incomes or those who expect their earnings to increase over time, alternative plans such as the Graduated Repayment Plan or the Income-Driven Repayment Plans may be more suitable.

The Graduated Repayment Plan starts with lower payments that gradually increase every two years, aligning with the borrower's expected career advancement and salary growth. This plan provides a more manageable entry point for new graduates while still maintaining a 10-year repayment timeline. On the other hand, Income-Driven Repayment Plans, such as the Revised Pay As You Earn (REPAYE) Plan or the Income-Based Repayment (IBR) Plan, cap monthly payments at a percentage of the borrower's discretionary income. These plans are particularly beneficial for those with high loan balances relative to their income, as they offer lower monthly payments and potential loan forgiveness after 20 or 25 years of qualifying payments.

For borrowers seeking to minimize interest payments and pay off their loans faster, the Snowball Method or the Avalanche Method can be effective strategies. The Snowball Method involves paying off the smallest loan balance first while making minimum payments on other loans, then using the freed-up funds to tackle the next smallest balance. This approach provides a psychological boost as borrowers see their loans disappear one by one. In contrast, the Avalanche Method prioritizes loans with the highest interest rates, aiming to reduce the overall interest paid over the life of the loans. This method can lead to significant savings in interest but may require more discipline and a longer repayment timeline.

Understanding the nuances of each repayment plan and strategy is crucial for borrowers to make the most informed decisions about their student loan repayment. By considering factors such as income, loan balance, and repayment timeline, borrowers can choose a plan that best fits their financial situation and goals. Additionally, regularly reviewing and adjusting repayment strategies as circumstances change can help borrowers stay on track and potentially save money in the long run.

Exploring Student Earnings in Ukraine: A Comprehensive Guide

You may want to see also

Frequently asked questions

The total amount students end up paying after loans can vary widely depending on factors such as the initial loan amount, interest rates, repayment terms, and any additional fees. On average, students may end up paying anywhere from 1.5 to 2 times the original loan amount after interest and fees are factored in.

Common factors that affect the total repayment amount for student loans include the principal amount borrowed, the interest rate (which can be fixed or variable), the repayment term (length of time to repay the loan), and any additional fees such as origination fees or late payment penalties.

Students can estimate their total repayment amount by using online loan calculators or by reviewing the loan terms and conditions provided by their lender. These tools can help students understand the impact of different interest rates, repayment terms, and fees on their overall repayment amount.

Yes, there are several strategies students can use to minimize their repayment amount. These include making larger payments than the minimum required, paying off loans with higher interest rates first, considering loan consolidation or refinancing options, and taking advantage of any available loan forgiveness or repayment assistance programs.

If students are unable to repay their loans, they may face several consequences, including accruing additional interest and fees, damaging their credit score, and potentially facing legal action from their lender. In some cases, unpaid student loans can also lead to wage garnishment or the withholding of tax refunds and Social Security benefits.