The topic of student debt and the amount students owe to the government is a pressing issue in many countries. With the rising cost of higher education, an increasing number of students are turning to government loans to fund their studies. This has led to a significant accumulation of debt, which can have long-term implications for both the students and the economy. Understanding the extent of this debt, the factors contributing to it, and the potential solutions is crucial for policymakers, educators, and students alike.

Explore related products

$14.99 $14.99

What You'll Learn

![]()

Tuition fees and room/board costs

The cost of higher education is a significant concern for many students and their families. Tuition fees and room and board costs can vary widely depending on the institution and location. Public universities generally have lower tuition fees compared to private universities, but room and board costs can be similar across both types of institutions.

For the academic year 2022-2023, the average tuition fee for in-state students at public four-year universities in the United States was $10,950, while the average room and board cost was $12,320. For out-of-state students, the average tuition fee was $27,800, with room and board costs averaging $12,320. Private universities had even higher tuition fees, with an average of $39,400 for the academic year 2022-2023.

In addition to tuition fees and room and board costs, students may also need to pay for textbooks, transportation, and other miscellaneous expenses. These costs can add up quickly and contribute to the overall debt that students may owe to the government.

One way to help manage the cost of higher education is to apply for financial aid. The Free Application for Federal Student Aid (FAFSA) is a form that students can fill out to determine their eligibility for federal student aid, including grants, loans, and work-study programs. Many states and institutions also offer their own financial aid programs, so it's important for students to research and apply for all available options.

Another way to reduce the cost of higher education is to consider attending a community college or a two-year institution before transferring to a four-year university. Tuition fees and room and board costs are generally lower at community colleges, and students can often save money by living at home while attending.

In conclusion, the cost of higher education can be a significant burden for students and their families. By understanding the various costs involved and exploring financial aid options, students can make informed decisions about their education and minimize the amount of debt they owe to the government.

Unlocking Financial Aid: A Guide to CARES Act Benefits for Students

You may want to see also

Explore related products

$15.99 $20

![]()

Interest rates on student loans

The interest rates on student loans are a critical factor in determining how much students ultimately owe the government. These rates can vary significantly depending on the type of loan, the lender, and the borrower's credit history. For instance, federal student loans typically have fixed interest rates that are set by Congress, while private student loans often have variable rates that can fluctuate based on market conditions.

One unique aspect of student loan interest rates is the concept of capitalization. When interest accrues on a student loan, it can be added to the principal balance if not paid promptly. This means that students may end up paying interest on their interest, which can substantially increase the total amount owed over time. To avoid this, it's crucial for borrowers to make regular payments and to consider paying more than the minimum amount due each month.

Another important consideration is the difference between subsidized and unsubsidized loans. Subsidized loans are available to students who demonstrate financial need, and the government pays the interest on these loans while the borrower is in school. Unsubsidized loans, on the other hand, require the borrower to pay the interest from the time the loan is disbursed. Understanding the distinction between these types of loans can help students make informed decisions about their borrowing options.

Furthermore, interest rates can also impact the repayment term of a student loan. Loans with higher interest rates may require shorter repayment terms to minimize the total amount paid, while loans with lower interest rates may offer longer repayment terms with smaller monthly payments. Borrowers should carefully consider their financial situation and future earning potential when choosing a repayment plan.

In conclusion, the interest rates on student loans play a significant role in determining the overall cost of borrowing. By understanding the different types of loans, the concept of capitalization, and the implications of interest rates on repayment terms, students can make more informed decisions about their financial future and minimize the amount they owe the government.

Decoding Tax Refunds: A Student's Guide to Maximizing Returns

You may want to see also

Explore related products

![]()

Repayment plans and forgiveness programs

Navigating the complexities of student loan repayment can be daunting, but understanding the various repayment plans and forgiveness programs available can significantly ease the burden. One of the most common repayment plans is the Standard Repayment Plan, which offers a fixed monthly payment over a 10-year period. However, for those struggling to make ends meet, income-driven repayment plans such as the Revised Pay As You Earn (REPAYE) Plan or the Income-Based Repayment (IBR) Plan can be more manageable, as they cap monthly payments at a percentage of the borrower's discretionary income.

For borrowers who have taken out loans for graduate or professional studies, the Grad PLUS Loan offers a fixed or variable interest rate and allows for borrowing up to the full cost of attendance. Repayment for Grad PLUS Loans typically begins six months after graduation, and borrowers can choose from various repayment plans, including the Standard Repayment Plan and income-driven plans.

Forgiveness programs provide another avenue for relief, particularly for those working in public service or certain nonprofit organizations. The Public Service Loan Forgiveness (PSLF) Program, for example, offers forgiveness of the remaining loan balance after 120 qualifying monthly payments for borrowers who work full-time in a public service job. Similarly, the Teacher Loan Forgiveness Program provides up to $17,500 in forgiveness for eligible teachers who have been working in low-income schools for at least five consecutive years.

It's crucial for borrowers to carefully review the eligibility criteria and application processes for these programs, as they can be quite stringent. Additionally, borrowers should be aware of potential tax implications associated with loan forgiveness, as the forgiven amount may be considered taxable income.

In conclusion, while the prospect of repaying student loans can be overwhelming, there are various repayment plans and forgiveness programs available to help borrowers manage their debt. By understanding these options and selecting the most appropriate plan, borrowers can take control of their financial future and minimize the impact of student loan debt on their lives.

Unlocking Financial Aid: How Much Do Students Really Get from FAFSA?

You may want to see also

Explore related products

![]()

Impact on credit scores

A significant concern for students who owe the government is the potential impact on their credit scores. Late payments or defaulting on student loans can lead to negative marks on a credit report, which can affect a person's ability to secure credit in the future. This can manifest in higher interest rates on credit cards, car loans, and mortgages, or even being denied credit altogether.

The impact on credit scores can be particularly severe for those who have co-signers on their loans. If the primary borrower defaults, the co-signer's credit score can also be negatively affected, potentially straining relationships and financial stability.

To mitigate the impact on credit scores, it's essential for students to make timely payments and communicate with their loan servicers if they're struggling to repay their loans. Options such as income-driven repayment plans, deferment, or forbearance can help borrowers manage their debt and avoid default.

It's also important for students to monitor their credit reports regularly to ensure that any errors or inaccuracies are addressed promptly. By staying proactive and informed, students can minimize the long-term consequences of their government debt on their credit scores.

Exploring Student Earnings in Ukraine: A Comprehensive Guide

You may want to see also

Explore related products

$19.99

$24.55 $30.99

![]()

Alternatives to government loans

Students facing the daunting task of funding their education often turn to government loans as a primary source of financial aid. However, these loans come with strings attached, including interest rates and repayment terms that can be burdensome. Fortunately, there are alternatives to government loans that students can explore to lighten their financial load.

One such alternative is private student loans, which are offered by banks, credit unions, and other financial institutions. These loans often have more flexible repayment terms and may offer lower interest rates than government loans, especially for students with good credit. However, it's important to note that private loans may require a cosigner and may not offer the same protections as government loans, such as income-driven repayment plans.

Another option for students is to consider scholarships and grants, which are essentially free money that does not need to be repaid. There are numerous scholarships and grants available, catering to a wide range of students with different backgrounds, interests, and academic achievements. Students can search for these opportunities online, through their school's financial aid office, or by contacting organizations directly.

Additionally, students may consider working part-time or full-time to help cover their educational expenses. This not only provides a source of income but also offers valuable work experience and networking opportunities. Students can explore on-campus jobs, internships, or off-campus employment in their field of study.

Lastly, students can look into income-sharing agreements (ISAs), which are contracts between a student and an investor where the investor agrees to pay for the student's education in exchange for a percentage of the student's future income. This option can be particularly appealing for students who are confident in their future earning potential but may not have the means to pay for school upfront.

In conclusion, while government loans are a common option for funding education, they are not the only choice. Students should explore a variety of alternatives, including private loans, scholarships, grants, work opportunities, and ISAs, to find the best fit for their financial needs and circumstances. By doing so, they can potentially reduce their debt burden and set themselves up for financial success after graduation.

Summer Slide: The Surprising Amount Students Forget Over Break

You may want to see also

Frequently asked questions

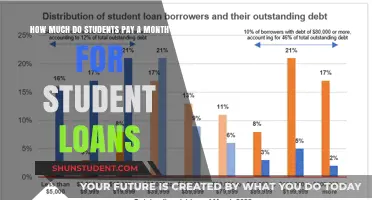

The amount students owe the government varies widely based on factors such as the type of loans taken, interest rates, and the duration of their education. As of recent data, the average student loan debt in the United States is around $30,000, but this can range significantly higher for those pursuing advanced degrees or attending private institutions.

There are several types of government loans available to students, including Direct Subsidized Loans, Direct Unsubsidized Loans, and PLUS Loans. Direct Subsidized Loans are for undergraduate students with financial need, and the government pays the interest while the student is in school. Direct Unsubsidized Loans are available to both undergraduate and graduate students and do not require financial need, but the student is responsible for the interest. PLUS Loans are for graduate students or parents of undergraduate students and have higher interest rates.

Interest rates on student loans can significantly impact the total amount owed over time. For example, a loan with a higher interest rate will accrue more interest each month, leading to a larger balance. Additionally, the way interest is capitalized (added to the principal balance) can also affect the total amount paid over the life of the loan. It's important for students to understand the interest rates on their loans and how they will impact their repayment.

There are several strategies for managing and repaying student loan debt. One approach is to prioritize high-interest loans for repayment first, while making minimum payments on others. Another strategy is to consolidate multiple loans into a single loan with a lower interest rate. Income-driven repayment plans are also available, which adjust monthly payments based on the borrower's income and family size. Additionally, some borrowers may be eligible for loan forgiveness programs based on their profession or service commitments.