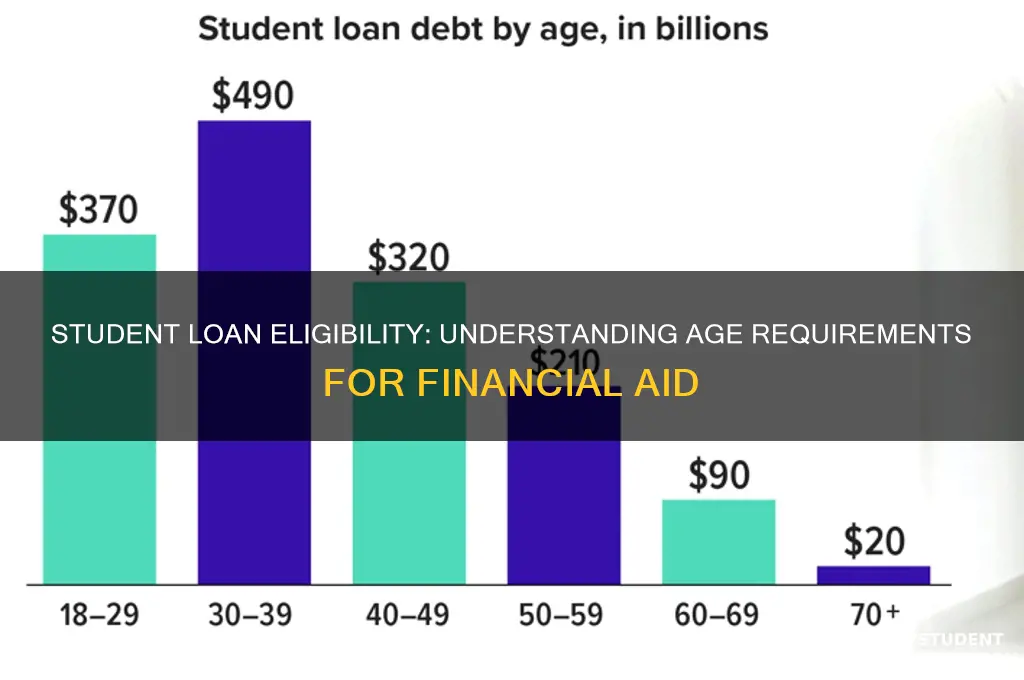

Understanding when you become eligible for student loans is crucial for planning your educational journey. In most countries, eligibility for student loans typically begins at the age of 18, as this is the legal age of majority. However, specific requirements can vary depending on your location, the type of loan, and whether you are considered a dependent or independent student. For instance, in the United States, federal student loans are available to students enrolled in eligible programs, regardless of age, as long as they meet other criteria such as financial need and enrollment status. Private loans may have additional age or credit requirements. It’s essential to research the rules in your region and consult with financial aid offices or loan providers to ensure you meet all eligibility criteria.

| Characteristics | Values |

|---|---|

| Minimum Age for Eligibility | No specific minimum age; eligibility is based on enrollment status. |

| Maximum Age for Eligibility | No maximum age limit; students of any age can apply if enrolled. |

| Enrollment Requirement | Must be enrolled in an eligible program at a qualifying institution. |

| Citizenship/Residency | U.S. citizens or eligible non-citizens (e.g., permanent residents). |

| Financial Need | Varies; some loans (e.g., Subsidized Direct Loans) require need. |

| Credit History | Not required for most federal student loans (e.g., Direct Loans). |

| Loan Types Available | Direct Subsidized, Direct Unsubsidized, PLUS Loans, Perkins Loans. |

| Repayment Start Date | Typically begins 6 months after graduation or dropping below half-time. |

| Interest Rates | Fixed rates determined annually by the U.S. Department of Education. |

| Loan Limits | Varies by year in school, dependency status, and loan type. |

| Grace Period | 6 months for most loans before repayment begins. |

| Deferment/Forbearance Options | Available for eligible borrowers (e.g., economic hardship, unemployment). |

| Loan Forgiveness Programs | Available for certain professions (e.g., Public Service Loan Forgiveness). |

| Application Process | Complete the FAFSA (Free Application for Federal Student Aid). |

| Renewal Requirements | Annual FAFSA submission and maintaining satisfactory academic progress. |

Explore related products

What You'll Learn

- Minimum Age Requirements: Federal and private loan age limits

- Enrollment Status Impact: Full-time vs. part-time student eligibility

- Credit History Role: How credit score affects loan approval

- Parental Involvement: Dependency status and its influence on loans

- Repayment Age Limits: Maximum age for loan repayment plans

![]()

Minimum Age Requirements: Federal and private loan age limits

Federal student loans, primarily offered through the U.S. Department of Education, do not impose a minimum age requirement for eligibility. Instead, the focus is on enrollment status and financial need. To qualify, you must be enrolled in an eligible program at a participating school, maintain satisfactory academic progress, and demonstrate financial need for subsidized loans. Unsubsidized loans, however, are available regardless of financial need, provided you meet enrollment criteria. This means a 16-year-old dual-enrolled high school student or a 60-year-old pursuing a degree could both access federal loans, assuming they meet the other eligibility criteria. The absence of an age limit reflects the federal government’s commitment to making education accessible across all age groups.

Private student loans operate under a different framework, with age being a critical factor. Most private lenders require borrowers to be at least 18 years old, the legal age of majority in most states, to enter into a binding loan agreement. However, some lenders may allow younger applicants if they have a creditworthy cosigner who is at least 18. For example, a 17-year-old planning to start college in the fall might secure a private loan with a parent or guardian as a cosigner. This age requirement ensures borrowers are legally capable of managing the financial responsibility of a loan. Unlike federal loans, private lenders prioritize creditworthiness, income, and age to mitigate risk.

The disparity between federal and private loan age limits highlights the importance of understanding your options based on your age. If you’re under 18, federal loans are your primary avenue for funding education without a cosigner. For those 18 and older, both federal and private loans become accessible, though federal loans typically offer more favorable terms, such as lower interest rates and flexible repayment plans. Private loans, while more restrictive in terms of age and credit requirements, can fill funding gaps when federal aid falls short. For instance, a 20-year-old student might use federal loans to cover tuition and supplement with a private loan for living expenses.

Practical tips for navigating these age requirements include starting with federal loans if you’re under 18, as they are more accessible and do not require a cosigner. If you’re 18 or older, compare federal and private loan options to determine the best fit for your financial situation. For younger students, consider building a relationship with a cosigner early to ensure smooth access to private loans if needed. Additionally, explore scholarships and grants, which have no age restrictions and do not require repayment. Understanding these age-based eligibility rules empowers you to make informed decisions about financing your education.

Student Loan Forgiveness: Who Qualifies and Who Doesn't?

You may want to see also

Explore related products

![]()

Enrollment Status Impact: Full-time vs. part-time student eligibility

Your enrollment status—whether you're a full-time or part-time student—significantly influences your eligibility for student loans. Lenders and federal aid programs often have distinct criteria tied to how many credits you’re taking each semester. Full-time students, typically enrolled in 12 or more credits per term, generally qualify for the maximum loan amounts available. Part-time students, usually taking fewer than 12 credits, may face reduced loan limits or stricter repayment terms. Understanding these differences is crucial for planning your financial aid strategy.

For federal student loans, such as Direct Subsidized and Unsubsidized Loans, full-time enrollment is not a strict requirement, but it does impact the amount you can borrow. Part-time students are still eligible, but their loan limits are prorated based on the number of credits they’re taking. For example, a part-time student enrolled in 6 credits might receive only half the loan amount available to a full-time student. Private lenders often have even stricter requirements, with some refusing to lend to part-time students altogether. This disparity highlights the importance of aligning your enrollment status with your financial needs.

Beyond loan amounts, enrollment status affects other aspects of financial aid, such as grace periods and repayment timelines. Full-time students typically enjoy a six-month grace period after graduation before loan repayment begins. Part-time students, however, may find their grace period reduced or eliminated, depending on the lender. Additionally, some loan forgiveness programs, like Public Service Loan Forgiveness, require full-time enrollment during the qualifying employment period. Part-time students may need to strategize differently to meet these requirements.

Practical tips can help part-time students maximize their loan eligibility. First, communicate with your school’s financial aid office to understand how your credit load affects aid. Second, explore alternative funding sources, such as scholarships or work-study programs, which are often available regardless of enrollment status. Finally, consider accelerating your course load if possible to qualify for full-time benefits without extending your degree timeline. Balancing your academic pace with financial constraints is key to navigating the full-time vs. part-time dilemma.

In conclusion, enrollment status plays a pivotal role in determining your student loan eligibility and terms. While full-time students generally access more favorable loan conditions, part-time students can still secure funding by understanding the rules and planning strategically. By weighing your options and leveraging available resources, you can make informed decisions that align with your educational and financial goals.

Student Loan Forgiveness: What Happens After 120 Payments?

You may want to see also

Explore related products

![]()

Credit History Role: How credit score affects loan approval

Your credit score is a financial fingerprint, a numerical representation of your reliability as a borrower. When it comes to student loans, this three-digit number plays a pivotal role in determining not just approval, but also the interest rate you'll pay and the terms of your loan. Lenders view your credit score as a crystal ball, predicting the likelihood of you repaying the debt. A high score, typically above 670, signals responsible financial behavior and makes you a more attractive borrower, increasing your chances of securing a loan with favorable terms. Conversely, a low score can raise red flags, potentially leading to loan denial or higher interest rates, making repayment more burdensome.

Understanding this dynamic is crucial for students, especially those under 21, who may have limited or no credit history.

Building credit takes time, and starting early is advantageous. Students can begin by becoming authorized users on a parent's credit card, ensuring responsible usage and timely payments. Secured credit cards, backed by a deposit, are another option for establishing credit history. These strategies, coupled with consistent on-time payments for any existing loans or bills, can gradually build a positive credit profile. Remember, a strong credit score not only increases your chances of student loan approval but also opens doors to better financial opportunities in the future, from renting an apartment to securing a car loan.

While age itself doesn't directly determine student loan eligibility, it often correlates with credit history. Most students under 18 lack the legal capacity to enter into loan agreements independently. However, federal student loans, a primary source of funding for many students, don't require a credit check, making them accessible to borrowers regardless of age or credit history. Private student loans, on the other hand, often necessitate a creditworthy cosigner, typically a parent or guardian, for borrowers under 21. This cosigner's credit history becomes a crucial factor in the approval process, highlighting the interconnectedness of age, credit, and loan eligibility.

It's important to note that even with a cosigner, a student's credit history, if existent, can still influence the loan terms. A student with a budding but positive credit history may secure a lower interest rate compared to someone with no credit history at all. This underscores the importance of financial literacy and responsible credit management from a young age. By understanding the impact of credit scores and taking proactive steps to build a positive credit history, students can position themselves for financial success, not just in securing student loans but throughout their lives.

Will Student Loan Deferment Return? Exploring the Possibility of Another Extension

You may want to see also

Explore related products

![]()

Parental Involvement: Dependency status and its influence on loans

In the United States, students under 24 are typically considered dependent on their parents for financial aid purposes, unless they meet specific criteria such as being married, having dependents, or serving in the military. This dependency status directly impacts the amount of student loan assistance available, as it requires parental financial information to be included in the Free Application for Federal Student Aid (FAFSA). For instance, dependent students may qualify for lower loan limits compared to independent students, who are assessed solely on their own income and assets. Understanding this distinction is crucial for planning how to finance higher education effectively.

Consider the scenario of a 20-year-old college student living with their parents. Despite being legally an adult, their dependency status ties their financial aid eligibility to their family’s income. If their parents have a higher income, the student may receive less need-based aid, including subsidized loans with lower interest rates. Conversely, an independent student of the same age, perhaps one who has been self-supporting for at least a year, would be evaluated independently, potentially qualifying for higher loan limits and more favorable terms. This disparity highlights the need for students to assess their dependency status carefully and explore options like filing an appeal if their circumstances warrant it.

To navigate this system, students should first determine their dependency status using the FAFSA guidelines. Key questions include whether they provide more than half of their own financial support, are married, have dependents, or meet other criteria outlined by the Department of Education. If classified as dependent, students can still maximize their loan eligibility by encouraging parents to contribute to a 529 plan or other education savings accounts, which are treated more favorably in financial aid calculations than taxable income. Independent students, on the other hand, should focus on building a credit history or finding a cosigner to secure private loans with better terms.

A practical tip for dependent students is to explore state-specific or institutional aid programs that may have different eligibility criteria than federal loans. For example, some states offer grants or scholarships based on academic merit rather than financial need, bypassing the dependency issue altogether. Additionally, students can petition their college’s financial aid office for a dependency override in cases of extenuating circumstances, such as family estrangement or abuse. While not guaranteed, a successful override can significantly increase access to loans and other aid.

In conclusion, parental involvement and dependency status play a pivotal role in determining student loan eligibility and terms. By understanding the rules, strategically planning financial contributions, and leveraging available resources, students can mitigate the impact of dependency status on their ability to finance their education. Whether dependent or independent, proactive steps can ensure access to the necessary funds for achieving academic and career goals.

Does Your Employer Meet Public Service Loan Forgiveness Criteria?

You may want to see also

Explore related products

![]()

Repayment Age Limits: Maximum age for loan repayment plans

Student loan repayment plans often come with age-related considerations, particularly when it comes to maximum age limits for certain repayment structures. For instance, income-driven repayment (IDR) plans in the U.S. typically recalculate monthly payments annually based on income and family size, but they also have a built-in forgiveness component after 20–25 years of qualifying payments. If you’re 40 when you begin an IDR plan, you could be in your late 60s by the time forgiveness kicks in, aligning with retirement age. This raises questions about how repayment age limits intersect with life stages and financial planning.

Analyzing these limits reveals a strategic layer to student loan management. For example, the UK’s Plan 2 loans are written off 30 years after the first payment, regardless of age, but payments are tied to income above a threshold (£22,010 annually as of 2023). If you start repaying at 25, the loan could be forgiven by age 55, well before traditional retirement. In contrast, Australia’s HECS-HELP loans are repaid through the tax system once income exceeds a threshold ($51,550 annually as of 2023) and have no explicit age cap, but the system effectively balances repayment with earning potential over a lifetime. These examples highlight how age limits—or their absence—shape long-term financial obligations.

From a practical standpoint, understanding repayment age limits can inform decisions about loan consolidation, refinancing, or switching plans. For instance, if you’re nearing the maximum age for a specific repayment plan’s benefits, consolidating loans to reset the clock might be advantageous. However, caution is warranted: refinancing federal loans into private ones could eliminate access to age-friendly forgiveness programs. Similarly, older borrowers should weigh the trade-offs of extending repayment terms, as lower monthly payments might mean paying more interest over time, particularly if retirement income is lower than expected.

A comparative look at global systems underscores the diversity in repayment age limits. Canada’s Repayment Assistance Plan (RAP) adjusts payments based on income and family size but doesn’t impose a maximum age for participation. Meanwhile, Japan’s scholarship-loan hybrid programs often require full repayment by age 65, reflecting cultural norms around intergenerational financial responsibility. These variations suggest that age limits are not just financial tools but also reflect societal values about education, debt, and aging.

In conclusion, repayment age limits are a critical yet often overlooked aspect of student loan planning. By understanding how these limits interact with your financial timeline, you can make informed decisions that minimize long-term burdens. Whether you’re a recent graduate or mid-career professional, factoring in age-related repayment caps can help align your loan strategy with broader life goals, ensuring that education debt doesn’t outlast your ability to manage it effectively.

Does Student Loan Forgiveness Include Navient Borrowers? What You Need to Know

You may want to see also

Frequently asked questions

There is no specific age requirement for federal student loans in the U.S. Eligibility is based on enrollment in an eligible program, financial need (for some loans), and other criteria, not age.

Yes, you can apply for federal student loans if you are under 18, but you may need a parent or guardian to cosign or provide additional information, depending on the loan type and lender.

No, there is no upper age limit for federal student loans. Adults of any age can apply as long as they meet the eligibility requirements, such as enrollment in an eligible program.

Private student loans may have age restrictions or require a cosigner if the borrower is under 18 or lacks sufficient credit history. Policies vary by lender, so it’s important to check with the specific provider.