Applying for student aid forgiveness can be a lifeline for borrowers struggling with the burden of educational debt. Various programs, such as Public Service Loan Forgiveness (PSLF), Teacher Loan Forgiveness, and income-driven repayment plans, offer pathways to reduce or eliminate student loans after meeting specific criteria. To begin, borrowers must first determine their eligibility by reviewing program requirements, such as employment in qualifying public service roles or teaching in low-income schools. Next, they should gather necessary documentation, including employment certification forms and proof of eligible loan types. Submitting applications accurately and on time is crucial, as processing times can vary. Staying informed about updates to forgiveness programs and maintaining consistent loan payments are also essential steps to ensure a successful outcome.

| Characteristics | Values |

|---|---|

| Eligibility Programs | Public Service Loan Forgiveness (PSLF), Teacher Loan Forgiveness, Income-Driven Repayment (IDR) Forgiveness, Perkins Loan Cancellation, Total and Permanent Disability (TPD) Discharge |

| Application Process | Submit Employment Certification Form (PSLF), Teacher Loan Forgiveness Application, IDR Forgiveness after 20-25 years of payments, Perkins Cancellation Application, TPD Discharge Application |

| Documentation Required | Proof of employment (PSLF), Teaching service certification, Income verification (IDR), Disability documentation (TPD), Loan details |

| Processing Time | Varies by program (e.g., PSLF takes 60-90 days, TPD up to 120 days) |

| Loan Types Covered | Federal Direct Loans, FFEL Loans (for some programs), Perkins Loans |

| Tax Implications | PSLF and TPD are tax-free; IDR and Teacher Forgiveness may be taxable |

| Application Deadline | No deadline for most programs, but specific deadlines for Perkins and TPD |

| Approval Criteria | Full-time qualifying employment (PSLF), Teaching in low-income schools, Disability certification, Completion of repayment term (IDR) |

| Appeal Process | Available for denied applications (e.g., PSLF, TPD) |

| Latest Updates (as of 2023) | Temporary PSLF waiver (ended Oct 31, 2022), IDR Account Adjustment (2023) |

| Where to Apply | Federal Student Aid website (studentaid.gov), Loan servicer portal |

Explore related products

What You'll Learn

- Eligibility Requirements: Understand income, employment, and loan type criteria for forgiveness programs

- Application Process: Gather documents, complete forms, and submit via official channels accurately

- Repayment Plans: Explore income-driven plans to qualify for forgiveness after consistent payments

- Loan Consolidation: Combine loans to simplify eligibility for forgiveness programs

- Deadlines & Updates: Stay informed on program changes and submission deadlines to avoid missing out

![]()

Eligibility Requirements: Understand income, employment, and loan type criteria for forgiveness programs

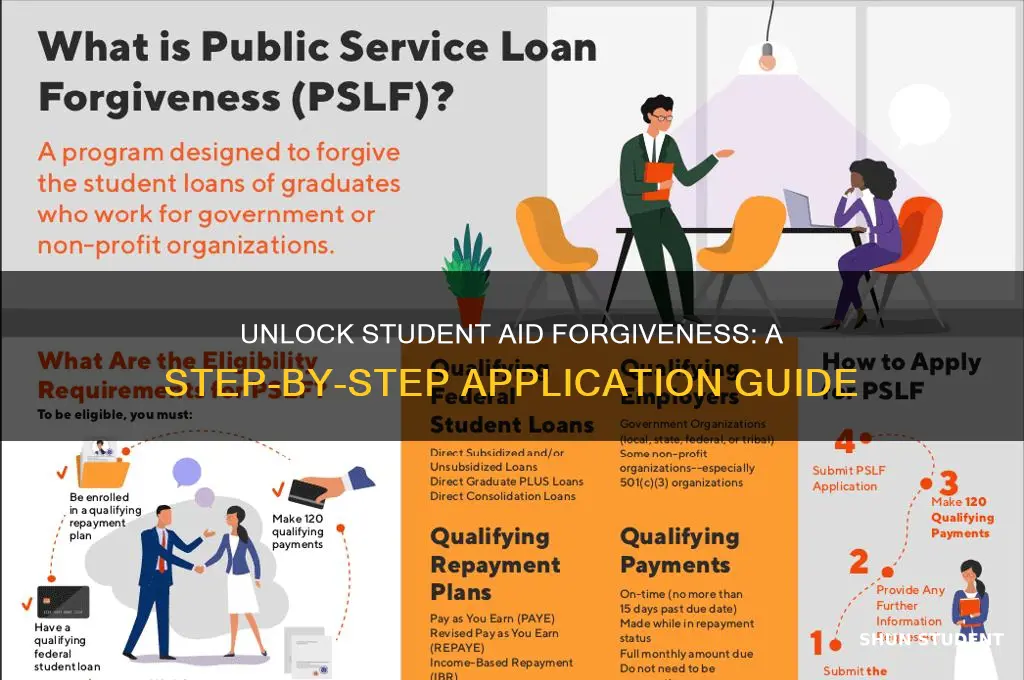

Navigating the eligibility maze for student loan forgiveness programs requires a clear understanding of three critical factors: income, employment, and loan type. Each program has its own set of rules, but these three pillars often determine whether you qualify for relief. For instance, income-driven repayment (IDR) plans, which can lead to loan forgiveness after 20-25 years, cap monthly payments at a percentage of your discretionary income. This means your earnings directly influence both your payment amount and your path to forgiveness. Similarly, Public Service Loan Forgiveness (PSLF) requires 120 qualifying payments while working full-time for a government or nonprofit organization, highlighting the importance of employment type and tenure. Understanding these intersections is the first step toward determining your eligibility.

Let’s break it down further. Income thresholds vary widely across programs. For example, the Revised Pay As You Earn (REPAYE) plan calculates payments as 10% of discretionary income, while the Income-Based Repayment (IBR) plan caps payments at 10% or 15% depending on when you borrowed. If your income falls below a certain threshold, your payment could be as low as $0, still counting toward forgiveness. Employment criteria are equally specific. PSLF demands full-time work (at least 30 hours per week) in a qualifying public service role, with no exceptions for part-time or contract work. Loan type is another non-negotiable—only Direct Loans are eligible for PSLF, meaning Federal Family Education Loans (FFEL) or Perkins Loans must be consolidated into a Direct Loan to qualify. These details underscore the need for meticulous planning and documentation.

Consider this scenario: A teacher earning $45,000 annually with $60,000 in Direct Loans under the REPAYE plan would pay approximately $240 per month, with forgiveness possible after 20 years. However, if they switch to a higher-paying private sector job, their payments increase, potentially delaying forgiveness. Conversely, a social worker earning $35,000 with the same loan amount might pay as little as $150 per month, reaching forgiveness sooner. This comparison highlights how income and employment choices directly impact forgiveness timelines. It’s not just about meeting the criteria—it’s about strategically aligning your career and financial decisions with program requirements.

Practical tips can make this process less daunting. First, use the Department of Education’s Loan Simulator to estimate payments and forgiveness timelines under different plans. Second, certify your employment annually for PSLF to ensure each payment counts toward the 120 required. Third, keep detailed records of your income, employment, and payments—these documents are your safety net if eligibility is ever questioned. Finally, stay informed about policy changes; for example, the limited PSLF waiver in 2021-2022 allowed past payments to count, even if they were previously ineligible. Such opportunities can accelerate your path to forgiveness but require proactive engagement.

In conclusion, eligibility for student loan forgiveness hinges on a delicate balance of income, employment, and loan type. Each program has its own rules, but understanding these criteria empowers you to make informed decisions. Whether you’re a teacher, nurse, or nonprofit worker, aligning your financial and career choices with program requirements is key. By leveraging tools, staying organized, and staying informed, you can navigate the system effectively and move closer to financial freedom.

Parent PLUS Loan Forgiveness: A Step-by-Step Guide for Borrowers

You may want to see also

Explore related products

![]()

Application Process: Gather documents, complete forms, and submit via official channels accurately

Applying for student aid forgiveness requires meticulous preparation, starting with gathering the right documents. This isn’t a scavenger hunt but a strategic collection process. Essential items include tax returns, pay stubs, loan statements, and proof of employment or hardship. For income-driven repayment plans, you’ll need IRS transcripts or tax return copies. If pursuing Public Service Loan Forgiveness (PSLF), gather employment certification forms (Form 120) and proof of eligible employment. Treat this step as the foundation—missing a single document can derail your application, so double-check official checklists provided by the Department of Education or your loan servicer.

Once documents are in hand, the next hurdle is completing forms accurately. This isn’t a fill-in-the-blank exercise; it’s a precision task. For instance, the PSLF application requires detailed employer information, including Federal Employer Identification Numbers (EINs). Income-driven repayment forms demand exact income figures, often requiring you to differentiate between gross and net pay. Mistakes here are costly—a single typo can lead to delays or denials. Use official guides or video tutorials available on the Federal Student Aid website to ensure every field is completed correctly. If unsure, contact your loan servicer for clarification—it’s better to ask than assume.

Submission is where many applicants falter, often due to overlooking official channels. For federal programs, submissions must go through the Department of Education’s platforms, such as the PSLF Help Tool or your loan servicer’s portal. Avoid third-party services promising expedited processing—they’re unnecessary and may incur fees. Keep records of submission dates and confirmation numbers as proof. For mailed applications, use certified mail with return receipt to track delivery. Accuracy here isn’t just about content but also about adhering to procedural requirements, ensuring your application isn’t lost in bureaucratic limbo.

Finally, treat this process as a marathon, not a sprint. Set aside dedicated time to gather documents, complete forms, and submit them. Create a checklist to track progress and deadlines. For example, PSLF requires 120 qualifying payments, so monitor your payment count and recertify income annually for income-driven plans. Stay organized with digital folders or physical binders for all loan-related paperwork. By approaching each step methodically, you’ll not only increase your chances of approval but also reduce stress, turning a daunting task into a manageable—and ultimately rewarding—endeavor.

Biden's Student Loan Forgiveness: A Step-by-Step Application Guide

You may want to see also

Explore related products

![]()

Repayment Plans: Explore income-driven plans to qualify for forgiveness after consistent payments

Income-driven repayment (IDR) plans are a cornerstone for borrowers seeking student loan forgiveness, particularly under programs like Public Service Loan Forgiveness (PSLF) or IDR forgiveness after 20–25 years of payments. These plans cap monthly payments at a percentage of your discretionary income, making them manageable for lower earners. For instance, the Revised Pay As You Earn (REPAYE) plan sets payments at 10% of discretionary income, while Pay As You Earn (PAYE) and Income-Based Repayment (IBR) plans vary between 10–15%, depending on when loans were taken out. To qualify, borrowers must recertify their income and family size annually, ensuring payments remain aligned with their financial situation.

The path to forgiveness through IDR plans requires meticulous record-keeping and adherence to rules. For example, PSLF applicants must make 120 qualifying payments while working full-time for a government or nonprofit employer. Similarly, IDR forgiveness requires 240–300 payments (20–25 years), depending on the plan. Borrowers should track payments using their loan servicer’s portal and request annual payment counts to avoid discrepancies. A common pitfall is switching plans without understanding how it affects the payment count; for instance, switching from IBR to REPAYE resets the counter unless specific conditions are met.

Choosing the right IDR plan involves analyzing your income, family size, and long-term goals. For borrowers with high debt relative to income, PAYE or REPAYE may offer lower payments and faster forgiveness. However, those expecting income growth might prefer IBR, which caps payments at 15% of discretionary income but recalculates based on current earnings. Married borrowers should consider filing taxes separately to exclude their spouse’s income from the calculation, though this may have tax implications. Tools like the Federal Student Aid Loan Simulator can model outcomes for different plans, helping borrowers make informed decisions.

A critical but often overlooked aspect is the tax treatment of forgiven amounts. Under current law, forgiven balances through IDR plans are taxable as income, except for PSLF. For example, a borrower with $50,000 forgiven after 25 years could face a tax bill of $12,500 (assuming a 25% tax rate). To mitigate this, borrowers can set aside a portion of their monthly savings into a taxable account, earning interest to offset future tax liabilities. Additionally, advocating for legislative changes to make IDR forgiveness tax-free could provide long-term relief.

In conclusion, income-driven repayment plans are a viable pathway to student loan forgiveness, but success hinges on understanding plan mechanics, maintaining eligibility, and planning for tax consequences. Borrowers should proactively recertify income, track payments, and select the plan that aligns with their financial trajectory. While the process demands diligence, the potential for debt relief makes it a worthwhile strategy for those burdened by student loans.

Nonprofit Student Loan Forgiveness: A Step-by-Step Application Guide

You may want to see also

Explore related products

![]()

Loan Consolidation: Combine loans to simplify eligibility for forgiveness programs

Loan consolidation can be a strategic move for borrowers navigating the complex landscape of student aid forgiveness. By merging multiple federal student loans into a single Direct Consolidation Loan, you streamline your repayment process and potentially unlock eligibility for forgiveness programs that require specific loan types. This approach is particularly beneficial if you have a mix of Federal Family Education Loan (FFEL) Program loans or Perkins Loans, which may not qualify for certain forgiveness plans on their own. Consolidating these into a Direct Loan opens doors to programs like Public Service Loan Forgiveness (PSLF) or income-driven repayment (IDR) forgiveness.

Consider this scenario: A borrower with both FFEL and Direct Loans wants to pursue PSLF. Since FFEL loans are ineligible for PSLF, consolidating them into a Direct Consolidation Loan is a prerequisite. This single action simplifies their repayment structure and makes them eligible for forgiveness after 10 years of qualifying payments in public service. However, beware: consolidating resets the clock on any progress made toward IDR forgiveness, so weigh the trade-offs carefully. For instance, if you’ve already made 5 years of payments toward 20- or 25-year IDR forgiveness, consolidating could restart your timeline.

The process of consolidating is straightforward but requires attention to detail. Start by visiting the Federal Student Aid website and submitting a Direct Consolidation Loan application. You’ll need to provide details about your existing loans and choose a repayment plan. Opt for an IDR plan if you’re aiming for forgiveness, as these cap monthly payments based on income and family size. For example, a single borrower earning $40,000 annually might pay as little as $200–$300 per month under the Revised Pay As You Earn (REPAYE) plan, making long-term repayment more manageable.

One critical caution: private loans cannot be included in federal consolidation. If you have both federal and private loans, consolidation will only address the federal portion. Private loans typically lack forgiveness options, so focus on refinancing them separately for better interest rates. Additionally, consolidating parent PLUS loans with other federal loans can complicate eligibility for certain IDR plans, as parent loans have limited options. Always review the terms of your new consolidated loan to ensure it aligns with your forgiveness goals.

In conclusion, loan consolidation is a powerful tool for simplifying eligibility for student aid forgiveness programs, but it’s not a one-size-fits-all solution. By understanding its benefits and limitations, you can make informed decisions that align with your financial goals. Whether you’re pursuing PSLF, IDR forgiveness, or just seeking a more manageable repayment structure, consolidation can be a pivotal step—but only if executed strategically.

Forgiving Student Debt: A Step-by-Step Guide to Loan Forgiveness

You may want to see also

Explore related products

![]()

Deadlines & Updates: Stay informed on program changes and submission deadlines to avoid missing out

Student aid forgiveness programs are dynamic, with deadlines and eligibility criteria shifting frequently. Missing a key date or update can mean the difference between approval and disqualification. To navigate this ever-changing landscape, proactive vigilance is essential.

Step 1: Identify Your Program’s Timeline

Each forgiveness program operates on its own schedule. For instance, Public Service Loan Forgiveness (PSLF) requires 120 qualifying payments, but the deadline to apply for temporary expanded eligibility under the 2023 waiver was October 31, 2023. Income-Driven Repayment (IDR) forgiveness deadlines vary based on enrollment date and plan type. Research your specific program’s timeline using official government resources like the Federal Student Aid website. Note recurring deadlines, such as annual recertification for IDR plans, and mark them in a digital calendar with reminders.

Step 2: Leverage Official Channels for Updates

Relying on third-party sources can lead to misinformation. Subscribe to updates directly from the U.S. Department of Education or your loan servicer. For example, signing up for email notifications from Federal Student Aid ensures you receive real-time alerts about policy changes, such as the recent one-time account adjustment for IDR forgiveness. Follow official social media accounts and bookmark the StudentAid.gov news section for announcements. Avoid unofficial forums or blogs that may misinterpret or exaggerate updates.

Step 3: Monitor Legislative Changes

Congressional actions can introduce new forgiveness opportunities or modify existing ones. For instance, the American Rescue Plan of 2021 made student loan forgiveness tax-free through 2025. Use tools like GovTrack to follow bills related to student loans. Set up alerts for keywords like “student loan forgiveness” or “Higher Education Act” to stay ahead of potential changes. While not all proposed legislation passes, early awareness allows you to prepare documentation or adjust your strategy.

Caution: Beware of Scams and Misinformation

Scammers often exploit confusion around deadlines and program changes. Legitimate forgiveness programs never require upfront fees or promise instant approval. If an offer seems too good to be true, verify it through official channels. For example, the “Biden-Harris Student Debt Relief Plan” was paused due to legal challenges, but scammers continued to target borrowers with fake application portals. Always confirm updates via StudentAid.gov before taking action.

Staying informed isn’t a one-time task—it’s an ongoing commitment. Allocate 15–30 minutes monthly to review your loan status, check for updates, and ensure compliance with program requirements. Use tools like spreadsheet trackers or apps like Mint to monitor deadlines alongside your financial goals. By treating deadlines and updates with the same urgency as tax filings or medical appointments, you’ll maximize your chances of securing forgiveness without unnecessary setbacks.

Disability Student Loan Forgiveness: A Step-by-Step Application Guide

You may want to see also

Frequently asked questions

Student aid forgiveness is a program that cancels or reduces federal student loan debt for eligible borrowers. Eligibility varies by program but often includes public service workers, teachers, and those with qualifying repayment plans or financial hardship.

To apply for PSLF, submit the PSLF & Temporary Expanded PSLF (TEPSLF) Certification & Application form to your loan servicer. Ensure you have made 120 qualifying payments while working full-time for a qualifying employer.

Yes, income-driven repayment (IDR) plans can lead to loan forgiveness after 20–25 years of qualifying payments, depending on the plan. Submit an application for forgiveness once you reach the required payment threshold.

Private student loans are not eligible for federal forgiveness programs. However, some private lenders offer their own forgiveness or assistance programs, so check with your lender for options.

Required documents vary by program but often include proof of employment (e.g., PSLF), income verification (e.g., IDR), and loan payment history. Always review program guidelines for specific documentation needs.