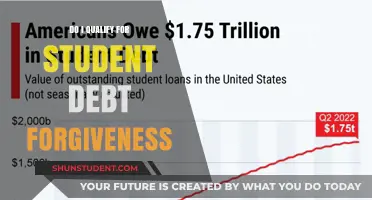

Applying for student debt forgiveness can be a life-changing opportunity for those burdened by educational loans, offering a pathway to financial relief and stability. With various programs available, such as Public Service Loan Forgiveness (PSLF), income-driven repayment plans, and temporary initiatives like the Biden administration’s one-time debt cancellation, understanding the eligibility criteria and application process is crucial. Each program has specific requirements, including the type of loans, repayment plans, and employment or income conditions, making it essential to research thoroughly and gather necessary documentation. By navigating these options carefully, borrowers can take proactive steps toward reducing or eliminating their student debt, easing the financial strain and paving the way for a more secure future.

| Characteristics | Values |

|---|---|

| Eligibility Requirements | Varies by program (e.g., income-driven repayment, public service, etc.) |

| Application Process | Online via Federal Student Aid (FSA) or specific program portals |

| Required Documents | Tax returns, pay stubs, loan information, employment certification |

| Programs Available | Public Service Loan Forgiveness (PSLF), IDR Forgiveness, Teacher Loan Forgiveness, etc. |

| Income-Driven Repayment (IDR) Forgiveness | After 20-25 years of qualifying payments, depending on the plan |

| Public Service Loan Forgiveness (PSLF) | 120 qualifying payments while working full-time for a qualifying employer |

| Teacher Loan Forgiveness | Up to $17,500 after 5 consecutive years in a low-income school |

| Application Deadline | Varies by program; some have no deadline, others are time-sensitive |

| Loan Types Eligible | Federal Direct Loans; FFEL or Perkins Loans may require consolidation |

| Tax Implications | Forgiveness may be tax-free depending on the program and timing |

| Processing Time | 3-6 months or longer, depending on the program and documentation |

| Appeal Process | Available for denied applications; requires additional documentation |

| Updates (as of 2023) | One-time account adjustment for IDR payments and limited PSLF waiver |

| Contact Information | Federal Student Aid: 1-800-4-FED-AID or studentaid.gov |

Explore related products

What You'll Learn

- Eligibility Requirements: Check income, loan type, repayment plan, and employment status for forgiveness programs

- Application Process: Gather documents, complete forms, and submit via official channels for review

- Public Service Loan Forgiveness (PSLF): Work full-time in public service and make 120 qualifying payments

- Income-Driven Repayment (IDR) Forgiveness: Enroll in IDR plan; balance forgiven after 20-25 years

- Loan Cancellation Programs: Explore options for teachers, nurses, or other profession-specific forgiveness programs

![]()

Eligibility Requirements: Check income, loan type, repayment plan, and employment status for forgiveness programs

To qualify for student debt forgiveness, understanding your eligibility is the first critical step. Each forgiveness program has specific criteria, and missing even one requirement can disqualify your application. Start by verifying your income, as many programs, like the Public Service Loan Forgiveness (PSLF) and income-driven repayment (IDR) plans, have income caps or adjustments based on family size. For instance, if your income is below 150% of the federal poverty guideline, you might qualify for reduced payments or faster forgiveness under certain plans. Use the Federal Student Aid website to calculate your adjusted gross income (AGI) and compare it against program thresholds.

Next, scrutinize your loan type, as not all loans are eligible for forgiveness. Federal Direct Loans, including Direct Subsidized, Unsubsidized, PLUS, and Consolidation Loans, are typically eligible for programs like PSLF and IDR forgiveness. However, Federal Family Education Loans (FFEL) and Perkins Loans often require consolidation into a Direct Loan to qualify. If you’re unsure about your loan type, log into your account on StudentAid.gov or contact your loan servicer for clarification. Consolidation can take 6–8 weeks, so plan accordingly if this step is necessary.

Your repayment plan plays a pivotal role in determining eligibility for forgiveness. Income-driven repayment plans, such as Pay As You Earn (PAYE), Revised Pay As You Earn (REPAYE), Income-Based Repayment (IBR), and Income-Contingent Repayment (ICR), are designed to align payments with your income and family size. For example, under REPAYE, any remaining balance is forgiven after 20–25 years of qualifying payments, depending on the loan type. Switching to an IDR plan can lower your monthly payments and accelerate your path to forgiveness, but ensure you recertify your income annually to avoid losing eligibility.

Finally, your employment status is a cornerstone for programs like PSLF, which requires 10 years of full-time work (at least 30 hours per week) in a qualifying public service job. Examples of eligible employers include government organizations, 501(c)(3) nonprofits, and certain other nonprofits providing public services. Keep detailed records of your employment, including pay stubs, contracts, and employer certifications, as these will be required to prove eligibility. Even if you switch jobs, as long as each position meets the criteria, your time accumulates toward the 10-year requirement.

By systematically checking your income, loan type, repayment plan, and employment status, you can pinpoint which forgiveness programs you’re eligible for and take actionable steps to maximize your benefits. Ignoring these details could delay or derail your application, so approach each requirement with precision and thoroughness.

Student Loan Forgiveness: Essential Steps and Timing for Debt Relief

You may want to see also

Explore related products

![]()

Application Process: Gather documents, complete forms, and submit via official channels for review

Applying for student debt forgiveness begins with meticulous document gathering. This isn’t just about finding old loan statements; it’s about assembling a comprehensive portfolio that proves eligibility. Start by collecting proof of employment, especially if you’re pursuing Public Service Loan Forgiveness (PSLF). This includes W-2 forms, pay stubs, and employer certification forms spanning your qualifying years. For income-driven repayment (IDR) forgiveness, gather tax returns and pay stubs to verify income history. Don’t overlook loan disbursement records, as they confirm the type and date of loans, which dictate eligibility for certain programs. Treat this step as an audit of your financial and professional life—the more thorough, the smoother the process.

Once your documents are in order, the next hurdle is navigating the forms. Each forgiveness program has its own set of applications, often riddled with jargon and specific requirements. For PSLF, the Employment Certification Form (ECF) is your starting point, but it’s just the first in a series of submissions. IDR forgiveness requires an annual recertification of income, while Teacher Loan Forgiveness demands proof of teaching credentials and school eligibility. Pro tip: Use the official government websites to download forms, as third-party sites may contain outdated versions. Fill out each field meticulously; a single error can delay approval by months. Think of this step as a high-stakes exam—precision is non-negotiable.

Submitting your application via official channels is where many applicants falter. The Department of Education and loan servicers have strict guidelines for submission, often preferring certified mail or secure online portals. For PSLF, submissions must go directly to the U.S. Department of Education’s PSLF servicer, FedLoan Servicing. IDR applications are typically handled by your loan servicer, but double-check their submission process to avoid missteps. Caution: Avoid unofficial channels or services promising expedited processing—these are often scams. Track your submission with delivery confirmations and save digital copies of all documents. This step is less about paperwork and more about strategy—ensure your application lands in the right hands at the right time.

The final phase is the review process, a waiting game that tests patience. After submission, expect a confirmation notice, but don’t be alarmed if weeks or months pass without updates. During this time, resist the urge to resubmit or inundate servicers with calls; instead, use the waiting period to organize your records and prepare for potential follow-up requests. If your application is denied, don’t panic—denials often stem from minor errors or missing documentation. Appeal by addressing the specific issue and resubmitting promptly. Think of this phase as a marathon, not a sprint. Persistence and organization are your greatest allies in securing forgiveness.

Is Liberty Student Loan Forgiveness Legitimate? Uncovering the Truth

You may want to see also

Explore related products

![]()

Public Service Loan Forgiveness (PSLF): Work full-time in public service and make 120 qualifying payments

Public Service Loan Forgiveness (PSLF) offers a pathway to debt relief for those committed to a career in public service. To qualify, you must work full-time for a qualifying employer—such as government organizations, non-profits, or certain public service entities—and make 120 eligible payments under an income-driven repayment plan. This program is not for everyone, but for those who meet the criteria, it can eliminate your remaining federal student loan balance tax-free after a decade of dedicated service.

Steps to Pursue PSLF:

- Confirm Employer Eligibility: Use the Federal Student Aid Employer Search Tool to verify your employer qualifies. Non-profits must hold 501(c)(3) status, and government organizations at any level (federal, state, local) typically qualify.

- Switch to an Income-Driven Repayment (IDR) Plan: Payments under standard plans do not count toward PSLF. Enroll in an IDR plan like REPAYE or PAYE to ensure your payments qualify.

- Submit the Employment Certification Form (ECF): File this form annually or when switching employers to track qualifying payments. It also helps catch errors early, as missed certifications can reset your payment count.

- Make 120 Qualifying Payments: Payments must be on time (within 15 days of the due date), for the full amount due, and under an IDR plan while working full-time for a qualifying employer.

Cautions and Common Pitfalls:

One of the biggest mistakes borrowers make is assuming their payments automatically qualify. For instance, payments made under the wrong repayment plan or while working part-time do not count. Additionally, consolidating loans can reset your payment count, so time consolidation carefully. Always keep records of your payments and employment certifications, as administrative errors are common.

Practical Tips for Success:

- Track Your Progress: Create a spreadsheet to log payments, employers, and ECF submissions.

- Stay Informed: PSLF rules can change; subscribe to updates from Federal Student Aid or follow reputable student loan experts.

- Consider Temporary Public Service: Even a few years in public service can reduce your debt significantly if you later switch careers.

By following these steps and avoiding common pitfalls, PSLF can be a powerful tool for those dedicated to public service. It requires patience and diligence, but the reward—full loan forgiveness—is well worth the effort.

Updating Income for Student Loan Forgiveness: A Step-by-Step Guide

You may want to see also

Explore related products

$14.95 $14.95

![]()

Income-Driven Repayment (IDR) Forgiveness: Enroll in IDR plan; balance forgiven after 20-25 years

For those burdened by federal student loans, Income-Driven Repayment (IDR) plans offer a lifeline, potentially leading to forgiveness after 20 to 25 years of consistent payments. These plans adjust your monthly payment based on your income and family size, making repayment manageable for those with limited earnings. However, the path to IDR forgiveness requires careful navigation to ensure eligibility and maximize benefits.

Understanding the Timeline and Eligibility

IDR forgiveness isn’t automatic; it hinges on enrolling in an eligible plan and making qualifying payments for 20 to 25 years, depending on the plan. For instance, Revised Pay As You Earn (REPAYE) and Pay As You Earn (PAYE) plans forgive balances after 20 years for undergraduate loans, while Income-Based Repayment (IBR) and Income-Contingent Repayment (ICR) plans extend to 25 years. Crucially, only federal student loans qualify—private loans are ineligible. Consolidating loans, if necessary, can make them eligible, but beware: consolidation resets your payment count toward forgiveness.

Steps to Enroll and Maintain Progress

To start, submit an IDR application through your loan servicer or the Federal Student Aid website. You’ll need to provide income documentation, such as tax returns or pay stubs, and recertify annually to keep payments aligned with your earnings. Missing recertification deadlines can lead to higher payments and disrupt your progress toward forgiveness. Pro tip: Set calendar reminders for recertification and keep detailed records of all payments and correspondence.

Tax Implications and Long-Term Planning

While IDR forgiveness offers relief, it comes with a potential tax liability. The forgiven amount may be treated as taxable income, though the American Rescue Plan Act of 2021 temporarily exempts forgiven student debt from taxation through 2025. Consult a tax professional to plan for potential future taxes. Additionally, consider how IDR fits into your broader financial goals. Lower monthly payments may free up funds for savings or investments, but the extended repayment period means paying more interest over time.

Maximizing Forgiveness Opportunities

To accelerate progress, ensure every payment counts. Payments must be made on time and under an IDR plan to qualify. Periods of economic hardship deferment or forbearance generally don’t count toward forgiveness, so opt for IDR adjustments instead. If your income increases significantly, reassess your plan—you might switch to a standard repayment plan to pay off the loan faster, but only if it aligns with your financial goals.

By strategically enrolling in an IDR plan and staying vigilant about requirements, borrowers can turn a daunting debt into a manageable—and eventually forgivable—obligation.

Student Loan Forgiveness for Married Couples: Navigating Joint Relief Options

You may want to see also

Explore related products

![]()

Loan Cancellation Programs: Explore options for teachers, nurses, or other profession-specific forgiveness programs

For teachers burdened by student debt, the Teacher Loan Forgiveness Program offers a lifeline. Eligible educators can receive up to $17,500 in loan cancellation after completing five consecutive years of teaching in a low-income school. To qualify, you must be a highly qualified teacher in a designated elementary or secondary school, as determined by the Department of Education. The process begins with submitting a *Teacher Loan Forgiveness Application* to your loan servicer after completing the required service period. Keep detailed records of your employment and certifications, as these will be critical for approval. While $17,500 may not cover all debt, it significantly reduces the burden, especially for those in high-need fields like math, science, or special education.

Nurses, particularly those working in underserved areas, can explore the Nurse Corps Loan Repayment Program or the Public Service Loan Forgiveness (PSLF) program. The Nurse Corps program offers up to 85% of unpaid nursing education debt for registered nurses and nurse faculty in exchange for two to three years of service in a Critical Shortage Facility or as a nurse faculty member. Applicants must commit to full-time employment and provide proof of licensure and employment. Alternatively, PSLF forgives the remaining balance on federal loans after 120 qualifying payments while working full-time for a government or nonprofit organization. Nurses in public hospitals or clinics are prime candidates for this program. Both options require meticulous documentation and adherence to specific terms, but they can erase substantial debt for those dedicated to serving high-need communities.

Beyond teaching and nursing, profession-specific forgiveness programs exist for lawyers, doctors, and other public service workers. For instance, the National Health Service Corps Loan Repayment Program offers up to $50,000 in loan repayment for licensed healthcare professionals serving in Health Professional Shortage Areas. Similarly, the John R. Justice Program provides loan repayment assistance to public defenders and prosecutors. Each program has unique eligibility criteria, such as minimum service commitments and employment verification. Researching these options through the Federal Student Aid website or professional associations can uncover opportunities tailored to your career. While the application process may be rigorous, the potential for significant debt relief makes it a worthwhile pursuit.

When navigating profession-specific forgiveness programs, beware of common pitfalls. Missing deadlines, incomplete applications, or failing to meet service requirements can disqualify you. For example, PSLF applicants must use the *Employment Certification Form* periodically to ensure their payments qualify. Additionally, some programs require annual reapplication, so staying organized is crucial. Consider consulting with a financial advisor or loan counselor to maximize your chances of approval. While these programs demand commitment, they offer a clear path to financial freedom for those dedicated to their professions and communities.

California Tax Rules: Student Loan Forgiveness and Your Liability

You may want to see also

Frequently asked questions

Eligibility varies by program. Common options include Public Service Loan Forgiveness (PSLF), Teacher Loan Forgiveness, and income-driven repayment (IDR) plans. Generally, eligibility depends on factors like loan type, employment, and repayment plan.

To apply for PSLF, submit a PSLF form to your loan servicer after making 120 qualifying payments while working full-time for a qualifying employer (e.g., government or nonprofit). Ensure your loans are federal Direct Loans and you’re on an eligible repayment plan.

Required documents vary by program. Common documents include proof of employment (e.g., employer certification for PSLF), tax returns for IDR plans, and loan statements. Always check the specific program’s requirements for accurate documentation.