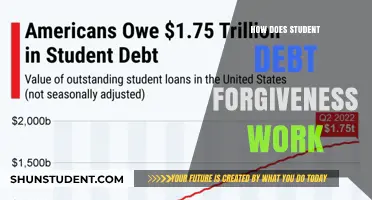

Forgiving student loans has become a pressing concern for millions of borrowers burdened by escalating debt and limited financial resources. With the rising cost of education and stagnant wages, many graduates find themselves trapped in a cycle of repayment that can span decades, hindering their ability to achieve financial stability, buy homes, or start families. Understanding how to navigate student loan forgiveness programs, such as Public Service Loan Forgiveness (PSLF), income-driven repayment plans, or potential government initiatives, is crucial for alleviating this burden. By exploring eligibility criteria, application processes, and available resources, borrowers can take proactive steps toward reducing or eliminating their student debt, paving the way for a more secure financial future.

Explore related products

What You'll Learn

- Income-Driven Repayment Plans: Adjust payments based on income; lower monthly costs; qualify for forgiveness after 20-25 years

- Public Service Loan Forgiveness (PSLF): Work in public service; make 120 payments; remaining balance forgiven tax-free

- Teacher Loan Forgiveness: Teach full-time in low-income schools; get up to $17,500 forgiven after 5 years

- Loan Discharge Options: Qualify for discharge due to disability, school closure, or borrower defense claims

- State & Employer Assistance: Explore state-based repayment programs or employer student loan repayment benefits

![]()

Income-Driven Repayment Plans: Adjust payments based on income; lower monthly costs; qualify for forgiveness after 20-25 years

For those struggling with student loan debt, income-driven repayment (IDR) plans offer a lifeline by tying monthly payments to earnings, ensuring affordability. These plans are particularly beneficial for borrowers with federal loans, as they can significantly reduce monthly costs and provide a pathway to loan forgiveness after 20 to 25 years of consistent payments. Unlike standard repayment plans, which have fixed monthly amounts, IDR plans recalculate payments annually based on your adjusted gross income and family size, making them ideal for individuals with fluctuating or lower incomes.

To enroll in an IDR plan, start by submitting your financial information through the Federal Student Aid website. There are four main types of IDR plans: Income-Based Repayment (IBR), Pay As You Earn (PAYE), Revised Pay As You Earn (REPAYE), and Income-Contingent Repayment (ICR). Each plan has specific eligibility criteria, such as loan type and income thresholds. For instance, PAYE and REPAYE require you to demonstrate partial financial hardship, while IBR has different terms for new and older borrowers. Carefully review each plan’s requirements to determine which best suits your situation.

One of the most appealing aspects of IDR plans is the potential for loan forgiveness. After making qualifying payments for 20 to 25 years, depending on the plan, any remaining balance is forgiven. However, it’s crucial to understand the tax implications: forgiven amounts may be considered taxable income, though temporary tax exemptions exist under the American Rescue Plan Act of 2021 for forgiveness through 2025. To maximize benefits, keep detailed records of your payments and stay informed about policy changes that could affect your forgiveness timeline.

While IDR plans offer relief, they aren’t without drawbacks. Lower monthly payments mean you’ll pay more interest over time, potentially increasing the total cost of your loan. Additionally, switching jobs or experiencing a significant income increase could raise your monthly payments. To mitigate these risks, consider making extra payments when possible to reduce the principal balance faster. Also, regularly update your income information to ensure your payments remain aligned with your financial situation.

In practice, IDR plans can transform overwhelming debt into manageable obligations. For example, a borrower earning $40,000 annually with $50,000 in loans might see monthly payments drop from $500 under a standard plan to $200 or less under an IDR plan. Over time, consistent payments not only make the debt more bearable but also bring the borrower closer to forgiveness. By leveraging these plans strategically, borrowers can regain financial stability while working toward a debt-free future.

Did Ben Shapiro Receive Student Loan Forgiveness? The Truth Revealed

You may want to see also

Explore related products

![]()

Public Service Loan Forgiveness (PSLF): Work in public service; make 120 payments; remaining balance forgiven tax-free

For those burdened by student debt, Public Service Loan Forgiveness (PSLF) offers a clear, if demanding, path to financial liberation. The program’s core requirement is straightforward: commit to a decade of public service employment while making 120 qualifying payments, and the remainder of your federal student loans vanishes—tax-free. This isn’t a loophole or a gamble; it’s a legislated incentive designed to reward careers in sectors like government, education, healthcare, and nonprofits. However, the devil is in the details, and understanding those details is critical to success.

To qualify, your employer must be a government organization at any level (federal, state, local), a 501(c)(3) nonprofit, or another type of nonprofit providing specific public services. Your role doesn’t necessarily require direct public-facing work—administrative positions within qualifying organizations often count. Payments must be made under an income-driven repayment plan, ensuring affordability, and must be on time and in full. Each payment takes you one step closer to forgiveness, but tracking progress is on you. Submit the Employment Certification Form annually to ensure your employer and payments qualify—a small but crucial administrative task that prevents costly mistakes.

Consider the trade-offs. PSLF demands a 10-year commitment to public service, which may limit earning potential compared to private-sector careers. Yet, for many, the stability of government work, the mission-driven nature of nonprofits, or the fulfillment of teaching or healthcare roles outweighs this drawback. Pairing PSLF with an income-driven plan like REPAYE can further reduce monthly payments, making the commitment more manageable. For example, a teacher earning $45,000 annually with $60,000 in loans might pay as little as $200 monthly under REPAYE, with the remaining balance forgiven after 120 payments.

Success stories abound, but so do pitfalls. Common errors include missing the employer certification step, making payments under the wrong repayment plan, or consolidating loans at the wrong time (which resets the payment count). The Temporary Expanded Public Service Loan Forgiveness (TEPSLF) program offers a safety net for those who’ve made payments under a non-qualifying plan, but it’s not automatic—you must apply. Stay vigilant, document every step, and treat PSLF as a long-term strategy requiring patience and precision.

In a landscape of confusing repayment options, PSLF stands out as a tangible goal for those aligned with public service. It’s not a quick fix, but for those willing to commit, it’s a rare opportunity to emerge debt-free without a tax penalty. Start by confirming your employer’s eligibility, enroll in an income-driven plan, and certify your employment annually. With persistence, the finish line—120 payments and full forgiveness—is within reach.

Can For-Profit Healthcare Workers Get Student Loan Forgiveness?

You may want to see also

Explore related products

![]()

Teacher Loan Forgiveness: Teach full-time in low-income schools; get up to $17,500 forgiven after 5 years

Teaching full-time in a low-income school isn’t just a career choice—it’s a pathway to shedding up to $17,500 in student loan debt after five years. The Teacher Loan Forgiveness program targets educators who commit to serving in Title I schools, where students from low-income families make up at least 30% of enrollment. This federal initiative rewards dedication to underserved communities while offering a tangible solution to the burden of student loans. If you’re a teacher with eligible loans, this program could be your most direct route to financial relief.

To qualify, you must meet specific criteria. First, ensure your loans are Federal Direct Loans or Federal Family Education Loans (FFEL); private loans are ineligible. Next, teach full-time for five consecutive academic years in a designated low-income school. Secondary teachers in math, science, or special education can claim the maximum $17,500, while other teachers can receive up to $5,000. Keep detailed records of your employment and loan types, as documentation is critical when applying for forgiveness.

While the program is straightforward, pitfalls exist. For instance, missing a single year of consecutive service resets your progress. Additionally, if you switch schools mid-term, ensure the new school still qualifies under Title I guidelines. Teachers should also be aware that this program cannot be combined with Public Service Loan Forgiveness (PSLF), so choose the path that aligns best with your long-term goals. Pro tip: Use the Department of Education’s Teacher Cancellation Low Income Directory to verify your school’s eligibility annually.

The impact of this program extends beyond personal finances. By incentivizing educators to serve in high-need areas, it addresses systemic educational disparities. Teachers who participate often report a deeper sense of fulfillment, knowing their work directly improves opportunities for underserved students. However, the trade-off is a commitment to often challenging environments, requiring resilience and passion. If you’re up for the challenge, this program offers both financial freedom and a chance to make a lasting difference.

In summary, Teacher Loan Forgiveness is a powerful tool for educators burdened by student debt. By committing five years to a low-income school, you can eliminate a significant portion of your loans while contributing to a critical societal need. Research your eligibility, plan your timeline, and stay organized to maximize this opportunity. For teachers seeking purpose and relief, this program is a win-win—transforming both your financial future and the lives of your students.

Does Northrop Grumman Qualify for Student Loan Forgiveness Programs?

You may want to see also

Explore related products

$14.95 $14.95

![]()

Loan Discharge Options: Qualify for discharge due to disability, school closure, or borrower defense claims

For those burdened by student loans, certain circumstances may qualify you for a complete discharge, effectively erasing your debt. This isn't a universal solution, but for individuals facing specific challenges, it offers a potential path to financial freedom. Let's delve into three key discharge options: disability, school closure, and borrower defense claims.

Disability Discharge: A Lifeline for Those Facing Health Challenges

If a permanent disability prevents you from engaging in substantial gainful activity, you may be eligible for a Total and Permanent Disability (TPD) discharge. This applies to federal student loans, including Direct Loans, Perkins Loans, and FFEL Program loans. The process involves submitting an application and supporting documentation from a physician certifying your disability. The Department of Education also automatically considers borrowers receiving Social Security Disability Insurance (SSDI) or those with a 100% disability rating from the VA for TPD discharge.

School Closure: When Your Institution Shuts Down

The sudden closure of your school can leave you with debt and no degree. Fortunately, you may qualify for a closed school discharge if your school closes while you're enrolled or shortly after you withdraw. This discharge applies to federal loans, and you'll need to provide proof of enrollment and the school's closure date. Keep in mind that if you've already transferred credits to another institution, you may not be eligible.

Borrower Defense to Repayment: Holding Schools Accountable

If your school misled you or engaged in illegal practices, you might have grounds for a borrower defense to repayment claim. This discharge is based on the argument that you wouldn't have taken out the loans if not for the school's misconduct. Examples include schools lying about job placement rates, accreditation, or program quality. The process involves submitting a detailed claim outlining the school's actions and their impact on your decision to borrow.

Navigating the Process: Persistence is Key

Qualifying for loan discharge requires thorough documentation and persistence. Gather all relevant medical records, school closure notices, or evidence of school misconduct. Be prepared for a potentially lengthy process, as reviews can take time. Remember, these discharge options are designed to provide relief in specific, challenging situations. If you believe you meet the criteria, don't hesitate to explore these avenues and seek assistance from student loan advocates or legal professionals if needed.

Teacher Loan Forgiveness: What the Department of Education Offers

You may want to see also

Explore related products

![]()

State & Employer Assistance: Explore state-based repayment programs or employer student loan repayment benefits

State-based repayment assistance programs are a hidden gem for borrowers seeking relief from student loan debt. These initiatives, often overlooked, provide targeted support to residents in specific professions or industries. For instance, the Maryland Nurse Support Program offers up to $10,000 annually to nurses working in critical shortage areas, with a maximum lifetime benefit of $60,000. Similarly, California’s Assuming Program forgives up to $50,000 in loans for mental health professionals serving in underserved communities. To access these programs, borrowers must meet eligibility criteria, such as residency, employment in a designated field, and commitment to a service period. Research your state’s offerings through its higher education or workforce development agency, as these programs vary widely in scope and benefits.

Employer-sponsored student loan repayment benefits are increasingly becoming a competitive perk in the job market. Companies like Fidelity Investments and Peloton offer contributions ranging from $2,000 to $10,000 annually toward employees’ student loans. These programs often require employees to remain with the company for a specified period, typically 1–3 years, to retain the benefit. To maximize this opportunity, negotiate student loan repayment as part of your compensation package during hiring or performance reviews. Additionally, ensure your employer’s contributions are tax-free under the CARES Act, which allows up to $5,250 annually in tax-exempt student loan assistance through 2025.

Comparing state and employer assistance reveals distinct advantages and limitations. State programs often prioritize public service roles, such as teaching, healthcare, or law enforcement, making them ideal for borrowers in these fields. However, they may require multi-year commitments and have competitive application processes. Employer benefits, on the other hand, are more accessible but depend on your workplace’s policies and your ability to negotiate. For example, a teacher in Texas might benefit from the Teach for Texas Loan Repayment Program, while a software engineer could leverage their employer’s repayment benefit. Combining both strategies—securing a state program and an employer benefit—can accelerate debt repayment significantly.

To navigate these options effectively, start by auditing your eligibility for state programs using tools like the Student Loan Planner’s State Loan Assistance Finder. Simultaneously, research potential employers’ benefits through platforms like Goodly or by directly inquiring during job interviews. Caution: avoid overextending yourself in public service roles solely for loan forgiveness if the long-term career fit is uncertain. Instead, align these opportunities with your professional goals. Finally, maintain meticulous records of payments and service commitments to ensure compliance with program requirements. By strategically leveraging state and employer assistance, borrowers can transform overwhelming debt into manageable—or even forgivable—obligations.

Do Americans Support Student Loan Forgiveness? Exploring Public Opinion

You may want to see also

Frequently asked questions

Yes, certain programs like Public Service Loan Forgiveness (PSLF), Teacher Loan Forgiveness, or income-driven repayment plans can lead to complete loan forgiveness after meeting specific criteria, such as working in public service or making consistent payments for 10–25 years.

To qualify for PSLF, you must work full-time for a qualifying public service employer (e.g., government or nonprofit), make 120 eligible payments under an income-driven repayment plan, and submit the PSLF application after meeting these requirements.

Private student loans are not eligible for federal forgiveness programs. However, some private lenders may offer forgiveness or repayment assistance in rare cases, or you can explore refinancing or settlement options.

Income-driven repayment plans cap your monthly payments at a percentage of your discretionary income. After 20–25 years of consistent payments (depending on the plan), any remaining balance is forgiven, though you may owe taxes on the forgiven amount.