Navigating the complexities of student loan forgiveness can be daunting, especially for borrowers with Navient loans. Understanding how to qualify for Navient student loan forgiveness requires familiarity with programs like Public Service Loan Forgiveness (PSLF), income-driven repayment (IDR) forgiveness, or specific settlement opportunities. Eligibility often hinges on factors such as loan type, repayment plan, employment in public service, or participation in certain programs. Borrowers must stay informed about application processes, documentation requirements, and deadlines to maximize their chances of success. Additionally, keeping track of updates from the Department of Education and Navient can help borrowers take advantage of new opportunities or changes in policy. With careful planning and persistence, achieving Navient student loan forgiveness is possible for those who meet the criteria.

| Characteristics | Values |

|---|---|

| Eligibility Programs | Public Service Loan Forgiveness (PSLF), Teacher Loan Forgiveness, Income-Driven Repayment (IDR) Forgiveness, Total and Permanent Disability (TPD) Discharge |

| PSLF Requirements | 120 qualifying payments while working full-time for a government or non-profit organization |

| Teacher Loan Forgiveness Eligibility | Teaching full-time for 5 consecutive years in a low-income school or educational service agency |

| IDR Forgiveness Timeline | 20-25 years of qualifying payments under an income-driven repayment plan (e.g., IBR, PAYE, REPAYE) |

| TPD Discharge Criteria | Total and permanent physical or mental disability verified by a physician or Veterans Affairs |

| Navient-Specific Settlements | Eligibility for loan cancellation or refund due to past misconduct (e.g., 2022 settlement with 38 states) |

| Application Process | Submit Employment Certification Form (PSLF), Teacher Loan Forgiveness Application, or IDR recertification annually |

| Loan Types Covered | Federal Direct Loans, FFEL loans (if consolidated into Direct Loans) |

| Tax Implications | PSLF and TPD discharge are tax-free; IDR forgiveness may be taxable (check current laws) |

| Navient Contact | Visit Navient’s website or call their customer service for program-specific guidance |

| Documentation Needed | Proof of employment, income, disability, or teaching service, depending on the program |

| Recent Updates (2023) | Temporary IDR Account Adjustment and PSLF waiver (expired Oct 31, 2023) to count previously ineligible payments |

Explore related products

What You'll Learn

- Income-Driven Repayment Plans: Qualify for forgiveness after 20-25 years of payments based on income

- Public Service Loan Forgiveness (PSLF): Work full-time in public service and make 120 qualifying payments

- Teacher Loan Forgiveness: Teach full-time in low-income schools for 5 consecutive years

- Disability Discharge: Apply for forgiveness if you have a permanent disability certification

- Borrower Defense to Repayment: Claim forgiveness if your school misled you or violated laws

![]()

Income-Driven Repayment Plans: Qualify for forgiveness after 20-25 years of payments based on income

For those burdened by Navient student loans, income-driven repayment (IDR) plans offer a lifeline. These plans adjust your monthly payments based on your income and family size, potentially lowering them significantly. But the real game-changer? After 20 to 25 years of consistent payments, any remaining balance is forgiven. This isn’t a loophole—it’s a federal program designed to provide relief for borrowers struggling to manage their debt.

To qualify, you must first enroll in one of four IDR plans: Income-Based Repayment (IBR), Pay As You Earn (PAYE), Revised Pay As You Earn (REPAYE), or Income-Contingent Repayment (ICR). Each plan calculates payments differently, but all cap them at a percentage of your discretionary income, typically 10-20%. For instance, if your annual income is $40,000 and your family size is two, your discretionary income might be calculated as the difference between your income and 150% of the federal poverty guideline for your family size. This results in a manageable monthly payment, often far below what standard repayment plans demand.

However, the path to forgiveness isn’t automatic. You must recertify your income and family size annually to remain on an IDR plan. Miss a recertification deadline, and you risk being kicked off the plan, resetting the forgiveness clock. Additionally, forgiven amounts may be taxed as income, though current laws exempt forgiven balances through 2025 under the American Rescue Plan Act. Planning for potential tax liability is crucial, as it could result in a substantial bill if not managed properly.

One often-overlooked benefit of IDR plans is their flexibility. If your income drops—say, due to job loss or reduced hours—your payments can adjust downward, even to $0. This ensures that repayment remains feasible during financial hardships. Conversely, if your income rises, payments increase, but they’re still capped at a reasonable percentage of your earnings. This dynamic structure makes IDR plans a practical long-term solution for borrowers with fluctuating incomes.

For Navient borrowers, navigating IDR plans requires vigilance and proactive management. Start by contacting Navient to discuss your eligibility and apply for the plan that best fits your financial situation. Keep meticulous records of your payments and recertification dates. Consider setting calendar reminders to ensure you never miss a deadline. While the 20-25 year timeline may seem daunting, the promise of forgiveness offers a tangible end to student loan debt, making the journey worthwhile for many.

Defrauded Student Loan Forgiveness: A Step-by-Step Application Guide

You may want to see also

Explore related products

![]()

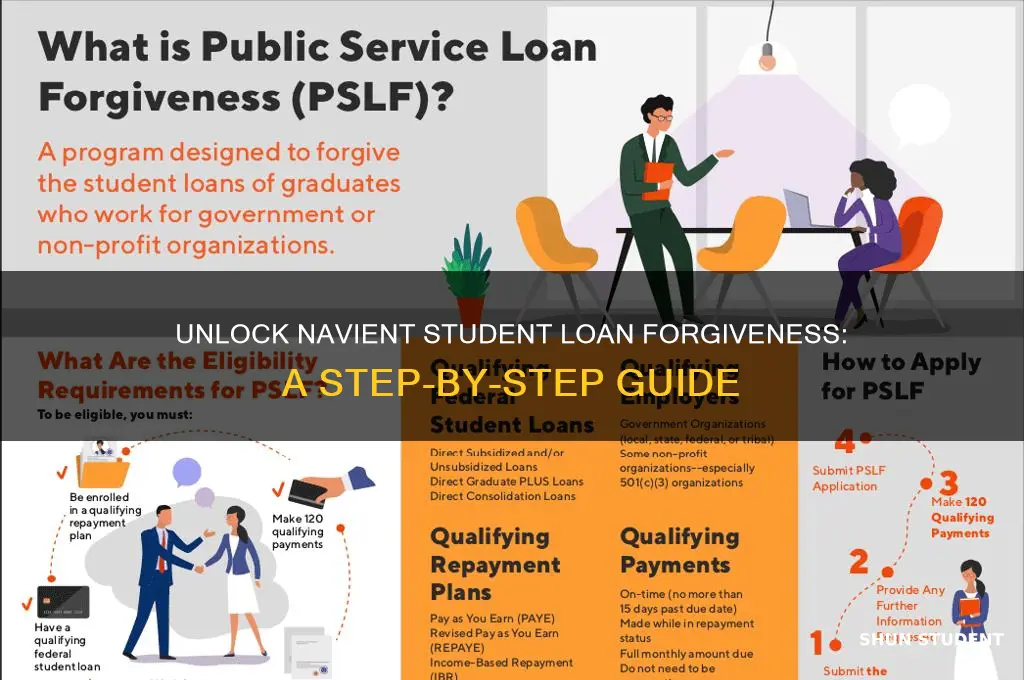

Public Service Loan Forgiveness (PSLF): Work full-time in public service and make 120 qualifying payments

One of the most direct paths to Navient student loan forgiveness is through the Public Service Loan Forgiveness (PSLF) program. This federal initiative offers a clear, albeit demanding, roadmap: commit to full-time public service employment and make 120 qualifying monthly payments. Unlike income-driven repayment plans that forgive remaining balances after 20–25 years, PSLF can eliminate your debt in just 10 years, provided you meet its stringent criteria. This makes it a particularly attractive option for borrowers with careers in government, education, healthcare, or nonprofit sectors.

To qualify, your employer must be a government organization at any level (federal, state, local, or tribal) or a qualifying nonprofit organization. Examples include public schools, universities, hospitals, and 501(c)(3) nonprofits. Private companies, even those with public service missions, do not count unless they meet specific IRS criteria. Additionally, your employment must be full-time, defined as either 30 hours per week or the employer’s definition of full-time, whichever is greater. Part-time workers can combine hours from multiple qualifying employers to meet this requirement, but each employer must independently qualify.

The 120 qualifying payments must be made under an income-driven repayment plan (IDR), such as Income-Based Repayment (IBR), Pay As You Earn (PAYE), or Revised Pay As You Earn (REPAYE). Payments made under the Standard Repayment Plan or while in school, in grace, or in deferment do not count. Each payment must be made on time, in full, and while employed full-time in public service. It’s critical to track these payments meticulously, as administrative errors are common. Use the Department of Education’s Employment Certification Form annually to confirm your employer’s eligibility and payment count.

Despite its benefits, PSLF is notorious for its complexity and low approval rates. Common pitfalls include incorrect repayment plans, ineligible employers, and payment processing errors. For instance, switching repayment plans mid-stream can reset your payment count, and even minor payment delays can disqualify a month. To avoid these issues, stay in consistent communication with your loan servicer, keep detailed records, and submit employment certification forms regularly. Tools like the PSLF Help Tool on the Federal Student Aid website can streamline the process and reduce errors.

In conclusion, PSLF offers a structured pathway to Navient student loan forgiveness for those committed to public service careers. While its requirements are strict, the reward of debt elimination after 10 years makes it a worthwhile pursuit. By understanding the eligibility criteria, adhering to payment rules, and proactively managing your documentation, you can navigate the program’s challenges and maximize your chances of success. For borrowers in qualifying roles, PSLF is not just a forgiveness program—it’s a strategic investment in a debt-free future.

Complete Guide to Applying for ITT Student Loan Forgiveness

You may want to see also

Explore related products

![]()

Teacher Loan Forgiveness: Teach full-time in low-income schools for 5 consecutive years

Teachers burdened by student loan debt can find relief through the Teacher Loan Forgiveness program, a federal initiative designed to incentivize teaching in low-income schools. This program offers a clear path to forgiveness: commit to five consecutive years of full-time teaching in a designated low-income school, and you could have up to $17,500 of your Direct Subsidized and Unsubsidized Loans or your Subsidized and Unsubsidized Federal Stafford Loans forgiven.

This program isn't just about debt relief; it's a strategic investment in both your financial future and the education of students in underserved communities.

To qualify, you'll need to meet specific criteria. Firstly, ensure you're employed as a full-time teacher, not a substitute, in a public elementary or secondary school identified as low-income by the federal government. The school must be listed in the Annual Directory of Designated Low-Income Schools for Teacher Cancellation Benefits. Secondly, your teaching assignment must be your primary responsibility, encompassing at least 700 hours per school year. Finally, you must be a "highly qualified teacher" as defined by the No Child Left Behind Act, possessing a bachelor's degree, full state certification, and demonstrating competence in your subject matter.

Tracking your progress is crucial. Maintain meticulous records of your employment, including contracts, pay stubs, and school district documentation. After completing your five-year commitment, submit a Teacher Loan Forgiveness Application to your loan servicer, along with the required documentation.

While the Teacher Loan Forgiveness program offers significant benefits, it's important to consider its limitations. The $17,500 forgiveness cap applies to most teachers, but those teaching secondary school math or science, or special education at any level, may be eligible for up to $5,000 in additional forgiveness. Additionally, this program only applies to Direct Loans and Federal Stafford Loans; private loans are ineligible.

The Teacher Loan Forgiveness program presents a compelling opportunity for teachers to alleviate student loan debt while making a meaningful impact in underserved communities. By carefully reviewing the eligibility requirements, diligently documenting your service, and strategically planning your teaching career, you can leverage this program to achieve financial freedom and contribute to a brighter future for your students.

Unlock Student Debt Forgiveness: A Step-by-Step Application Guide

You may want to see also

Explore related products

![]()

Disability Discharge: Apply for forgiveness if you have a permanent disability certification

If you have a permanent disability, you may qualify for a total and permanent disability (TPD) discharge, which can eliminate your federal student loan debt, including loans serviced by Navient. This process, while rigorous, offers a lifeline to those whose disabilities prevent them from working. To begin, you’ll need to provide documentation proving your disability, such as a physician’s certification or proof of Social Security Disability Insurance (SSDI) benefits. The U.S. Department of Education reviews applications closely, so accuracy and completeness are critical. Once approved, your loans are discharged, and you’re no longer obligated to repay them, though you may face tax implications depending on the year of discharge.

The application process for a disability discharge involves several steps. First, obtain a certification from a licensed physician verifying that you are totally and permanently disabled. Alternatively, if you receive SSDI benefits, you can submit a notice of award from the Social Security Administration (SSA). For veterans, a service-related disability certification from the Department of Veterans Affairs (VA) suffices. After gathering the necessary documentation, submit it to the loan servicer, in this case, Navient, or directly to the U.S. Department of Education. Be aware that there’s a three-year monitoring period during which you must provide annual documentation confirming your income doesn’t exceed the poverty line or that your disability status hasn’t changed.

One common misconception is that the disability discharge process is quick and effortless. In reality, it requires patience and attention to detail. For instance, if you’re using a physician’s certification, the doctor must complete a specific form provided by the Department of Education, detailing the nature and permanence of your disability. Errors or incomplete forms can delay approval. Additionally, while the monitoring period may seem intrusive, it’s designed to ensure the program’s integrity and prevent fraud. Understanding these nuances can help you navigate the process more effectively.

For those considering this route, practical tips can make a significant difference. Keep all medical records and correspondence organized in one place for easy access. If you’re on SSDI, ensure your benefit status is up-to-date before applying. Veterans should request their disability certification well in advance, as VA processing times can vary. Finally, consider consulting a student loan advisor or disability advocate to review your application before submission. Their expertise can identify potential issues and improve your chances of approval.

In conclusion, the disability discharge program is a powerful tool for borrowers with permanent disabilities, but it demands careful preparation and follow-through. By understanding the requirements, gathering the right documentation, and staying organized, you can increase your likelihood of success. While the process may seem daunting, the potential relief from student loan debt makes it a worthwhile pursuit for those who qualify.

Biden's Student Loan Forgiveness: Step-by-Step Application Guide

You may want to see also

Explore related products

![]()

Borrower Defense to Repayment: Claim forgiveness if your school misled you or violated laws

If your school misled you or engaged in illegal practices, you may qualify for student loan forgiveness through the Borrower Defense to Repayment program. This federal initiative allows borrowers to seek discharge of their federal student loans if their educational institution violated state or federal laws directly related to their loans or education. It’s a powerful tool for those who feel they were defrauded or deceived, but the process requires careful documentation and a clear understanding of eligibility criteria.

To initiate a Borrower Defense claim, start by gathering evidence that demonstrates your school’s misconduct. This could include misleading marketing materials, false job placement rates, or proof of illegal practices such as predatory recruiting tactics. For example, if your school claimed a 90% job placement rate but later investigations revealed it was closer to 30%, this discrepancy could form the basis of your claim. Additionally, document how these actions directly impacted your decision to enroll and your subsequent financial burden. The more specific and detailed your evidence, the stronger your case will be.

Once you’ve compiled your evidence, submit your claim through the Federal Student Aid website. The application requires a detailed narrative explaining how your school misled you, along with supporting documents. Be concise but thorough—clearly outline the violation, its impact on your education and finances, and why you believe you qualify for forgiveness. Keep in mind that processing times can vary, and there’s no guarantee of approval, so continue making payments on your loans until you receive a decision to avoid delinquency.

A critical caution: Borrower Defense to Repayment applies only to federal student loans, not private ones. If your loans were serviced by Navient, ensure they are federal Direct Loans, as these are eligible for the program. Private loans serviced by Navient are not covered, though you may explore other options like settlement or refinancing. Additionally, be wary of third-party companies promising to expedite your claim for a fee—the application process is free, and these services often provide no added value.

In conclusion, Borrower Defense to Repayment offers a pathway to relief for borrowers who were wronged by their educational institutions. By meticulously documenting your school’s misconduct and following the application process, you can take a proactive step toward financial freedom. While the journey may be lengthy, the potential for full loan discharge makes it a worthwhile pursuit for eligible borrowers.

Great Lakes Student Loan Forgiveness: Step-by-Step Application Guide

You may want to see also

Frequently asked questions

Eligibility for Navient student loan forgiveness typically depends on the specific program, such as Public Service Loan Forgiveness (PSLF), Teacher Loan Forgiveness, or income-driven repayment (IDR) forgiveness. Requirements include making qualifying payments, working in eligible public service or teaching roles, or enrolling in an IDR plan.

To apply for PSLF, submit the Employment Certification Form (ECF) annually or when you change employers to ensure your payments qualify. After 120 qualifying payments, submit the PSLF application through the U.S. Department of Education’s website, not directly through Navient.

No, Navient student loan forgiveness programs, such as PSLF or IDR forgiveness, only apply to federal student loans. Private loans are not eligible for these programs.

The Navient settlement resolved allegations of unfair lending practices and provided loan cancellation for certain borrowers. If you qualify, you’ll receive automatic forgiveness without needing to apply. Check the settlement website or your loan servicer for updates.

Enroll in an IDR plan through Navient, which caps your monthly payments based on your income. After 20–25 years of qualifying payments (depending on the plan), any remaining balance may be forgiven. Keep track of your payments and ensure you recertify your income annually.