The University of Phoenix has been accused of using deceptive advertising practices to attract students, falsely claiming to work with major companies to create job opportunities for its students. As a result, the US Department of Education has announced that it will approve federal student loan forgiveness for eligible students who were deceived by the school's claims. This has led to discussions and investigations surrounding student loan forgiveness and cancellation, with many former and current students of the University of Phoenix exploring options for loan relief.

| Characteristics | Values |

|---|---|

| Eligibility | Students who attended between September 21, 2012, and December 31, 2014, were deceived by the school's claims, and submitted a valid application for relief through ED's Borrower Defense program. |

| Application Process | File a borrower defense application on the Borrower Defense page. Check the status of your application under "Manage My Applications." |

| Decision Basis | FTC's 2019 court action against the University of Phoenix for deceptive advertising practices to attract students. |

| Notification | The Department of Education will notify applicants via email if their claim is approved. |

| Loan Status During Application | Loans will remain in forbearance/stopped collections status until a decision is made. |

| Impact of FTC Settlement | Receiving a refund from the FTC's settlement does not affect eligibility for loan forgiveness through ED's borrower defense program. |

| Additional Options | Texas and California residents misled by job opportunity claims may join a class-action lawsuit investigation. |

Explore related products

What You'll Learn

![]()

Student loan forgiveness eligibility for University of Phoenix students

The US Department of Education has announced that it will approve federal student loan forgiveness for students who attended the University of Phoenix between 21 September 2012 and 31 December 2014, were deceived by the school's claims, and submitted a valid application for relief through the Borrower Defense program. This decision was based on the Federal Trade Commission's (FTC) 2019 court action against the University of Phoenix for using deceptive advertising practices to attract students. The University of Phoenix falsely claimed to work with employers such as Microsoft, Twitter, Adobe, and Yahoo to create job opportunities for its students.

If you attended the University of Phoenix during the specified period and believe you were deceived by the school's claims, you may be eligible for loan forgiveness. To apply for loan forgiveness, you must submit a valid application for relief through the Borrower Defense program. This program allows students who feel they were scammed by their college or university to apply for federal loan forgiveness.

Even if you received a refund from the FTC's settlement, you are still eligible to apply for loan forgiveness through the ED's Borrower Defense program. Be sure to mention any refunds or settlements you received when you apply.

To submit your application, visit the borrower defense page to learn more about the process and submit your claim. You can check the status of your application on the borrower defense page under "Manage My Applications."

It is important to note that the loan forgiveness process may take time, and there have been reports of students still waiting to hear back about their applications. Additionally, some students have expressed concerns about the eligibility period, as the deceptive practices of the University of Phoenix may have occurred before 2012.

Transfer Students: Maryland's Acceptance Rates and Trends

You may want to see also

Explore related products

![]()

Deceptive advertising and false job placement claims

The University of Phoenix has been accused of deceptive advertising and false job placement claims. The Federal Trade Commission (FTC) pursued legal action against the university, alleging that it had engaged in deceptive advertising strategies and made false claims about post-graduation job opportunities for students. The FTC's investigation revealed that the university had used misleading advertising campaigns that falsely led prospective students to believe that it had partnerships with various companies, including AT&T, Microsoft, Yahoo!, Twitter, and the American Red Cross. The university allegedly implied that these partnerships would provide students with employment opportunities after graduation.

The University of Phoenix's advertising campaigns, such as the "Let's Get to Work" campaign, featured logos from prominent employers, creating the false impression of partnerships and tailored curriculum for specific companies. The FTC's case against the university also included allegations of misleading advertising targeted at military personnel and Hispanic students, suggesting that these groups were disproportionately influenced by the misleading claims.

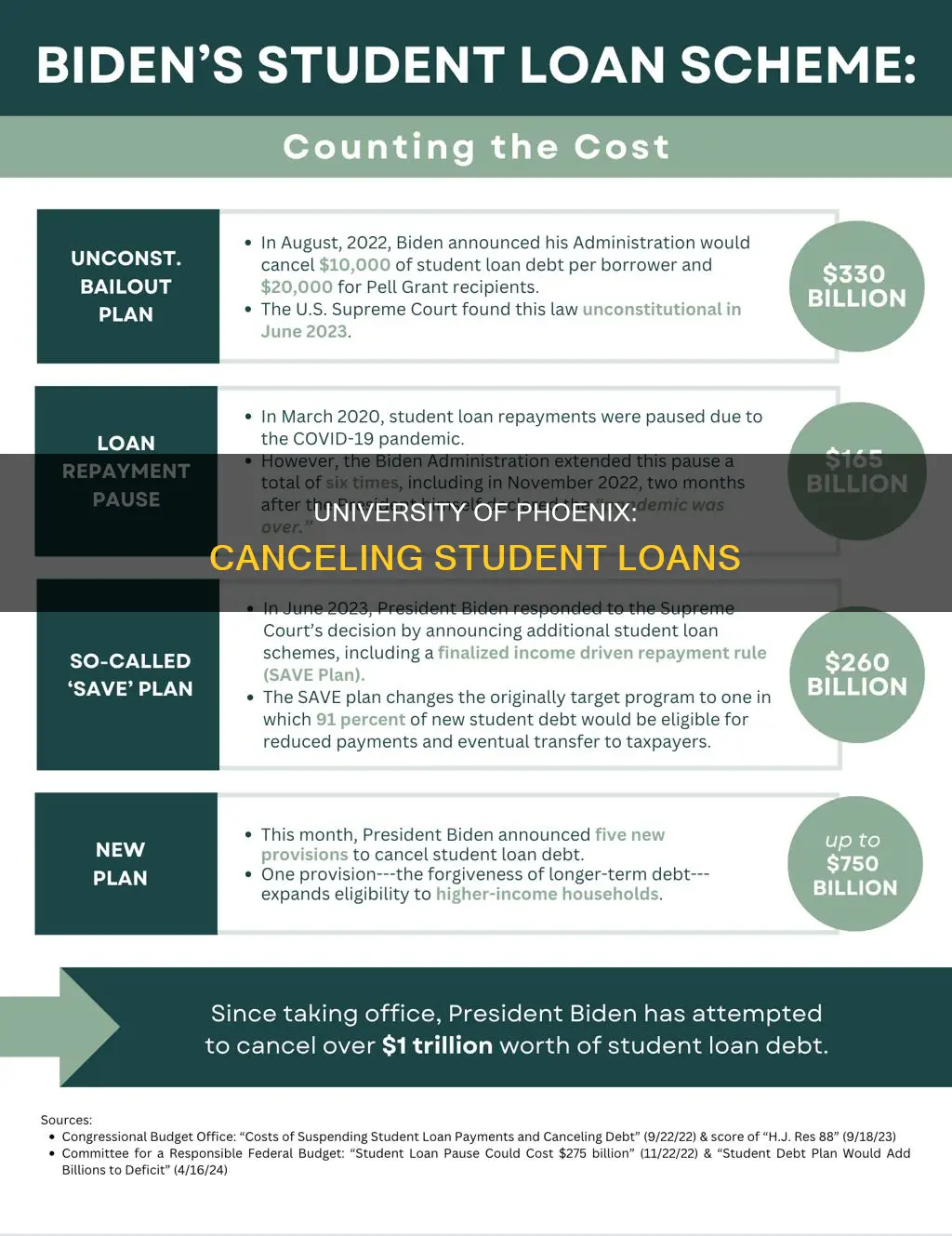

In 2019, the University of Phoenix agreed to a record-breaking settlement of $191 million with the FTC. The settlement included a $50 million cash payment to the FTC and the cancellation of $141 million in student debt for affected students. Despite the settlement, the university did not admit to any wrongdoing. The FTC's decision brought some relief to students who were harmed by the university's false claims, but the loan forgiveness only applied to a specific timeframe, leaving some students still burdened with loan debt.

Students who believe they were deceived by the University of Phoenix's false claims and were enrolled between September 21, 2012, and December 31, 2014, can apply for loan forgiveness through the Department of Education's Borrower Defense program. The eligibility criteria include submitting a valid application and providing evidence of being misled by the university's deceptive advertising practices. The Department of Education continues to process new and existing applications, and approved claims will result in full loan forgiveness.

Howard University College of Medicine: Inclusive or Exclusive?

You may want to see also

Explore related products

![]()

Borrower Defense to Repayment (BDTR) program

The Borrower Defense to Repayment (BDTR) program allows borrowers who have been defrauded or intentionally misled by their school to seek student loan forgiveness. In the case of the University of Phoenix, the US Department of Education has approved federal student loan forgiveness for students who attended the university between September 21, 2012, and December 31, 2014, and were deceived by the school's claims. This decision was based on the FTC's 2019 court action against the University of Phoenix for using deceptive advertising practices to attract students.

To be eligible for loan forgiveness through the BDTR program, students must have submitted a valid application for relief through the Department of Education's Borrower Defense program. The application process may vary depending on the specific circumstances and evidence of deception. In some cases, students may need to provide evidence such as emails or other documentation showing the university's false claims.

It is important to note that there may be deadlines or specific requirements for submitting a BDTR claim. For example, in one case, a borrower who submitted their BDTR form in October 2022 was told that they did not qualify because their application was submitted after the deadline of June 22, 2022. Therefore, it is essential to stay informed about any updates or changes to the BDTR program and its requirements.

The BDTR program has provided significant relief to students harmed by the University of Phoenix's deceptive practices. The Biden-Harris administration has approved the dismissal of billions of dollars in debt for borrowers through borrower defense claims. This program ensures that students who have been misled or defrauded by their schools have a pathway to financial relief and protects them from the negative consequences of the university's deceptive actions.

If you believe you are eligible for loan forgiveness under the BDTR program, it is recommended to visit the borrower defense page to learn more about the process and submit your claim. You can also check the status of your application on the borrower defense page under "Manage My Applications." Additionally, if you have received a refund from the FTC's settlement, you are still eligible for loan forgiveness through the BDTR program, and it is important to mention this when applying.

Harvard University Student Population: How Many?

You may want to see also

Explore related products

![]()

Loan forgiveness for Texas and California residents

The US Department of Education has announced that it will consider federal student loan forgiveness for students who attended the University of Phoenix between 21 September 2012 and 31 December 2014 and were misled by the institution's false claims. If you attended during this period, you can submit a claim to the Borrower Defense Program.

Now, here is some information on student loan forgiveness for Texas and California residents:

Texas

The Texas Education Agency (TEA) provides student loan forgiveness for teachers and all other school staff. Teachers with certain types of student loans may qualify for partial loan forgiveness, deferment, or cancellation benefits. Eligibility depends on the type of loan, the date of the first loan, and whether the teacher serves in a designated low-income school or subject matter teacher shortage area. Teachers must have a federal Perkins loan to be eligible for loan forgiveness.

California

There are several programs that offer student loan forgiveness in California. Most of these are aimed at medical professionals and educators.

- The California SLRP offers a maximum of $50,000 of student loan forgiveness for your first two years of service in a California Health Professional Shortage Area (HPSA).

- The LVNLRP is for licensed and practicing vocational nurses and only requires one year of service. Nurses can receive up to $8,000 for working 12 months full-time at a qualified California facility, and can be awarded this amount up to three times.

- The BSNLRP program offers up to $15,000 of loan repayment for one year of service at a specific facility for nurses with a Bachelor of Science in Nursing (BSN) degree. Nurses can receive this award up to three times for a total of $45,000 in student debt forgiveness.

- The Allied Healthcare Loan Repayment Program can help medical professionals repay up to $16,000 per year of their qualified educational loans. Program participants must provide care at one of the 35 CMSP counties. Healthcare workers can qualify for the program up to three times for a maximum award of $48,000.

- The CalHealthCares Loan Repayment Program can provide up to $300,000 of loan payment assistance for eligible dentists and physicians.

Boston University Law Students: Where to Live?

You may want to see also

Explore related products

![]()

Loan forgiveness application process and requirements

The US Department of Education has approved federal student loan forgiveness for former students of the University of Phoenix who were deceived by the school's job placement claims. The decision is based on the Federal Trade Commission's (FTC) 2019 court action against the university for using deceptive advertising practices to attract students.

If you attended the University of Phoenix between 21 September 2012 and 31 December 2014, and were misled by the school's claims, you may be eligible for loan forgiveness. To apply for loan forgiveness, you must submit a valid application for relief through the Department of Education's Borrower Defense program.

The application process typically involves completing and submitting an application form, along with any supporting documentation, to the Department of Education. You can find the application form and instructions on the official website of the Department of Education or Studentaid.gov. The website also provides information on the paperwork you need to provide. This may include evidence of your attendance at the university during the specified period and any relevant correspondence or advertising materials that you believe were deceptive.

It is important to note that the loan forgiveness program is only applicable to federal student loans. Private student loans are not covered by this program. Additionally, if you have outstanding debts with the university itself, these may be automatically forgiven, but this does not apply to student loans.

If you are a resident of Texas or California and were misled by the University of Phoenix's job placement claims, you may also be eligible to join a class-action lawsuit investigation. Consulting an attorney can help you determine if you have a valid claim and guide you through the legal process.

Exploring Student Population at University of West Alabama

You may want to see also

Frequently asked questions

You can apply for the federal program called Borrower Defense to Repayment (BDTR) if you feel that you were scammed by the University of Phoenix. The Department of Education (ED) has approved full federal student loan forgiveness for some University of Phoenix students who were deceived by the school's claims and submitted a valid application for relief through ED's Borrower Defense program.

Students who attended the University of Phoenix between September 21, 2012, and December 31, 2014, and were deceived by the school's claims are eligible for loan forgiveness. Additionally, students who were enrolled between October 1, 2012, and December 31, 2016, and had outstanding debts with the university itself are also eligible for loan forgiveness.

To apply for student loan forgiveness, you must file a borrower defense application. You can find instructions and information on the paperwork required on websites like Studentaid.gov. If your application is approved, you will be notified via email, and your loan will remain in forbearance/stopped collections status.