Understanding whether your Navient student loans qualify for forgiveness can be a complex but crucial process, especially given the various federal programs and recent changes in loan forgiveness policies. To determine eligibility, borrowers should first identify the type of loans they hold, as only federal loans, such as Direct Loans, may qualify for programs like Public Service Loan Forgiveness (PSLF) or income-driven repayment (IDR) forgiveness. Navient, as a loan servicer, primarily manages federal loans, so borrowers should review their loan agreements or log into their Navient account to confirm their loan type. Additionally, staying informed about recent updates, such as the limited PSLF waiver or IDR account adjustments, can provide opportunities for forgiveness that were previously unavailable. Consulting with a loan servicer or using the Department of Education’s tools, like the PSLF Help Tool, can also clarify eligibility and guide borrowers through the application process.

| Characteristics | Values |

|---|---|

| Eligibility for Forgiveness | Borrowers must meet specific criteria under programs like PSLF, IDR, or settlements. |

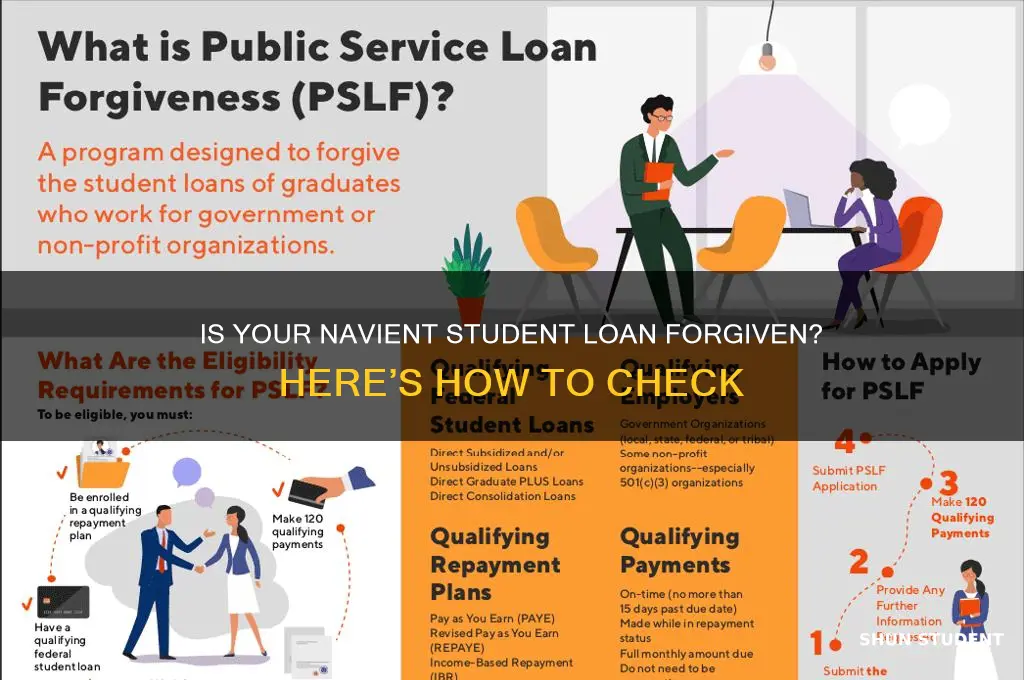

| Public Service Loan Forgiveness (PSLF) | Requires 120 qualifying payments while working full-time for a government or nonprofit organization. |

| Income-Driven Repayment (IDR) Forgiveness | Forgiveness after 20-25 years of qualifying payments, depending on the plan. |

| Navient Settlement Forgiveness | Certain borrowers may receive automatic forgiveness due to state settlements (e.g., 2022 settlements). |

| Notification Method | Borrowers are typically notified via email, mail, or updates on their loan servicer account. |

| Loan Type Eligibility | Federal student loans serviced by Navient (e.g., Direct Loans) are eligible; private loans are not. |

| Application Requirement | Some programs (e.g., PSLF) require submitting an application; others may be automatic. |

| Tax Implications | Forgiveness may be tax-free under certain programs (e.g., PSLF, IDR). |

| Loan Status Check | Borrowers can check their loan status on the Federal Student Aid website or their Navient account. |

| Fraud or Mismanagement Forgiveness | Borrowers may qualify if Navient mismanaged their loans (e.g., incorrect payment processing). |

| State-Specific Forgiveness | Some states offer forgiveness programs for residents (check state education agencies). |

| Private Loan Forgiveness | Private loans serviced by Navient are not eligible for federal forgiveness programs. |

| Updates and Resources | Regularly check the U.S. Department of Education and Navient websites for updates. |

Explore related products

What You'll Learn

- Eligibility Criteria: Understand federal forgiveness programs like PSLF, IDR, or closed school discharge requirements

- Loan Type Check: Confirm if loans are federal or private; only federal loans qualify for forgiveness

- Program Updates: Stay informed on Navient settlements, waivers, or new forgiveness initiatives announced

- Application Process: Learn how to apply for forgiveness through official channels like the DOE

- Account Review: Check loan servicer updates or notifications about forgiveness status in your account

![]()

Eligibility Criteria: Understand federal forgiveness programs like PSLF, IDR, or closed school discharge requirements

Determining if your Navient student loans qualify for forgiveness hinges on understanding the eligibility criteria of federal programs. These programs, such as Public Service Loan Forgiveness (PSLF), Income-Driven Repayment (IDR) plans, and Closed School Discharge, each have distinct requirements that borrowers must meet. Without grasping these specifics, you risk missing out on opportunities to reduce or eliminate your debt.

Public Service Loan Forgiveness (PSLF) demands a meticulous approach. To qualify, you must make 120 qualifying payments while working full-time for a government or nonprofit organization. Payments under IDR plans often count toward this total, but only Direct Loans are eligible—a critical detail for Navient borrowers, as some loans may need consolidation into the Direct Loan program. Track your employment certification annually to ensure each payment counts. For example, teachers in low-income schools or nurses at nonprofit hospitals are prime candidates, but only if they adhere to the program’s strict guidelines.

Income-Driven Repayment (IDR) plans offer forgiveness after 20–25 years of payments, depending on the plan. These plans cap monthly payments at a percentage of your discretionary income, making them ideal for borrowers with high debt relative to their earnings. For instance, if you earn $40,000 annually with $100,000 in loans, your payments under Revised Pay As You Earn (REPAYE) would be roughly 10% of your discretionary income. After 240–300 payments, the remaining balance is forgiven, though you may owe taxes on the forgiven amount. Navient borrowers should confirm their loans are in an IDR plan and recertify income and family size annually to maintain eligibility.

Closed School Discharge provides relief if your school closed while you were enrolled or shortly after withdrawal. For example, if you attended a for-profit college that shut down due to accreditation issues, you might qualify. However, you must not have transferred credits to another school or received a dischargeable transcript. Navient borrowers should submit a discharge application with proof of enrollment dates and the school’s closure. Unlike PSLF or IDR, this program offers immediate forgiveness without a waiting period, but eligibility is narrowly defined.

Understanding these programs requires proactive research and documentation. Navient borrowers should review their loan types, employment history, and repayment plans to align with federal forgiveness criteria. Missteps, such as missing payments or failing to recertify income, can derail progress. By strategically navigating these programs, borrowers can transform overwhelming debt into manageable—or even forgivable—obligations.

Unlocking Financial Freedom: Strategies to Forgive Student Debt Effectively

You may want to see also

Explore related products

$8.34 $17.99

![]()

Loan Type Check: Confirm if loans are federal or private; only federal loans qualify for forgiveness

Determining whether your Navient student loans are eligible for forgiveness begins with a critical first step: verifying the loan type. Only federal student loans qualify for forgiveness programs, while private loans do not. Navient services both federal and private loans, so assuming your loans are federal simply because Navient is your servicer is a common mistake. Log into your Navient account and review the loan details. Federal loans often include terms like "Direct Subsidized," "Direct Unsubsidized," or "Federal Family Education Loan (FFEL)." Private loans, on the other hand, may have names tied to banks or financial institutions. If you’re unsure, contact Navient directly or check your original loan documents. This distinction is non-negotiable—without federal loans, forgiveness programs like Public Service Loan Forgiveness (PSLF) or income-driven repayment plans are off the table.

Let’s break this down into actionable steps. First, access your Navient account online or through their mobile app. Navigate to the "Loans" section and examine each loan’s description. Look for keywords that indicate federal status, such as "Direct" or "FFEL." If the loan name includes a bank’s name (e.g., "Sallie Mae" or "Wells Fargo"), it’s likely private. Second, cross-reference your findings with the National Student Loan Data System (NSLDS), a federal database that lists all your federal loans. If a loan appears in NSLDS, it’s federal; if not, it’s private. Third, if you’re still uncertain, call Navient’s customer service at 1-888-272-5543 and ask explicitly whether your loans are federal or private. This clarity is essential before pursuing any forgiveness options.

A common pitfall borrowers face is assuming all loans serviced by Navient are federal, especially if they consolidated their loans. Consolidation can blur the lines, but the rule remains: only federal loans consolidated through the Department of Education’s Direct Consolidation Loan program retain eligibility for forgiveness. Private loan consolidation, even if serviced by Navient, does not qualify. For example, if you consolidated private loans with Navient, those loans remain private and ineligible for federal forgiveness programs. Always verify the consolidation type in your Navient account or through NSLDS to avoid this trap.

Understanding the implications of loan type is crucial for strategic planning. Federal loans offer pathways like PSLF, which forgives remaining balances after 120 qualifying payments for public service workers, or income-driven repayment plans, which forgive balances after 20–25 years of payments. Private loans, however, lack these options. If your loans are private, focus instead on refinancing for lower interest rates or negotiating with Navient for alternative repayment plans. While less flexible than federal options, these strategies can still provide financial relief.

In summary, the loan type check is your gateway to determining forgiveness eligibility. Misidentifying private loans as federal can lead to wasted time and effort pursuing unavailable programs. By meticulously reviewing loan details, cross-referencing with NSLDS, and confirming with Navient, you can confidently chart your path forward. Remember: federal loans open doors to forgiveness; private loans require a different strategy. This clarity is the foundation for making informed decisions about your student debt.

Is Your Student Debt Forgiven? Key Signs to Look For

You may want to see also

Explore related products

$15.74 $20

$26.68 $17.19

![]()

Program Updates: Stay informed on Navient settlements, waivers, or new forgiveness initiatives announced

Navient, one of the largest student loan servicers, has been at the center of numerous legal settlements and forgiveness initiatives, leaving borrowers wondering about the status of their loans. Staying informed about program updates is crucial, as these changes can directly impact your eligibility for loan forgiveness or reduction. Here’s how to navigate this evolving landscape effectively.

Step 1: Monitor Official Sources Regularly

Start by bookmarking the official websites of the U.S. Department of Education, Federal Student Aid (FSA), and Navient. These platforms are the primary sources for announcements regarding settlements, waivers, and forgiveness programs. For instance, the 2022 Navient settlement resulted in $1.7 billion in loan cancellations for 66,000 borrowers, but only those who met specific criteria, such as having private loans originated by Sallie Mae before 2015, were eligible. Subscribing to FSA email updates or following their social media channels ensures you receive timely notifications.

Step 2: Understand Settlement Criteria and Deadlines

Each settlement or initiative comes with unique eligibility requirements and deadlines. For example, the Navient settlement required borrowers to have been in default for at least seven years on certain private loans. Similarly, Public Service Loan Forgiveness (PSLF) waivers have time-sensitive submission windows. Missing a deadline could mean losing out on forgiveness opportunities. Create a calendar reminder to check for updates quarterly, especially during periods of legislative activity or legal resolutions.

Caution: Beware of Scams

As forgiveness programs gain attention, scammers often exploit borrowers’ confusion. Avoid unsolicited offers promising immediate loan forgiveness in exchange for fees or personal information. Legitimate updates will always come from official sources and require no upfront payment. If in doubt, contact your loan servicer directly or consult the FSA’s scam prevention resources.

Staying informed about Navient program updates requires diligence but can yield significant financial benefits. By monitoring official channels, understanding eligibility criteria, and avoiding scams, you position yourself to take full advantage of forgiveness opportunities as they arise. Remember, knowledge is power—especially when it comes to managing student debt.

Unlocking Debt-Free Future: 25-Year Student Loan Forgiveness Application Guide

You may want to see also

Explore related products

![]()

Application Process: Learn how to apply for forgiveness through official channels like the DOE

Navigating the application process for student loan forgiveness can feel like deciphering a complex code, but understanding the official channels, such as the Department of Education (DOE), is the first step toward clarity. The DOE oversees several forgiveness programs, including Public Service Loan Forgiveness (PSLF) and income-driven repayment (IDR) plans, which may apply to Navient-serviced loans. To begin, log into your account on the Federal Student Aid website, where you can access the necessary forms and track your eligibility status. This centralized platform ensures you’re working directly with the authoritative source, minimizing the risk of scams or misinformation.

Once logged in, identify the forgiveness program that aligns with your circumstances. For instance, PSLF requires 120 qualifying payments while working full-time for a government or nonprofit organization. If you’re on an IDR plan, forgiveness typically occurs after 20–25 years of consistent payments, depending on the plan. Download the appropriate application form, such as the PSLF Form or IDR Recertification, and complete it meticulously. Errors or missing information can delay processing, so double-check details like your employer’s EIN for PSLF or updated income figures for IDR. Submitting supporting documents, like proof of employment or tax returns, strengthens your case and expedites approval.

While the application process is straightforward, it’s not without pitfalls. For example, not all Navient-serviced loans qualify for forgiveness—only federal loans are eligible, not private ones. Additionally, payments made under certain plans, like the Graduated Repayment Plan, may not count toward forgiveness unless they’re part of an IDR strategy. To avoid missteps, use the DOE’s Loan Simulator tool to model your repayment path and consult with a loan servicer or financial advisor if unsure. Remember, patience is key; processing times can range from several weeks to months, depending on the program and volume of applications.

Finally, stay proactive throughout the process. Regularly check your account for updates and respond promptly to any requests for additional information. If your application is denied, don’t despair—appeals are possible, and the DOE provides guidance on how to contest decisions. By leveraging official resources, staying organized, and maintaining persistence, you can navigate the application process with confidence and increase your chances of securing the forgiveness you deserve.

Tech Student Loan Forgiveness: A Step-by-Step Application Guide

You may want to see also

Explore related products

![]()

Account Review: Check loan servicer updates or notifications about forgiveness status in your account

Your Navient account is the primary hub for all communications regarding your student loans, including updates on forgiveness status. Log in regularly to review notifications, messages, or banners that may indicate changes to your loan balance or eligibility for forgiveness programs. These updates often appear in the "Announcements" or "Messages" section of your account dashboard. Neglecting to check these could mean missing critical information about your loan status.

Analyzing the content of these updates requires attention to detail. Look for keywords like "forgiveness," "discharge," or "cancellation" in any notifications. For example, if you’re enrolled in an income-driven repayment plan, a message might state, "Your qualifying payment count has been updated," which could signal progress toward Public Service Loan Forgiveness (PSLF). Cross-reference these updates with the requirements of the forgiveness program you’re pursuing to ensure alignment.

A proactive approach to account review involves setting a monthly reminder to log in and scrutinize your loan details. Pay particular attention to the "Loan Summary" section, where changes in the principal balance or loan status (e.g., from "Active" to "In Forgiveness Review") may appear. If you notice discrepancies or lack clarity, contact Navient’s customer service immediately. Documentation is key—screenshot or save any relevant updates for future reference, especially if disputing inaccuracies.

Comparatively, relying solely on email notifications can be risky, as these may end up in spam folders or be overlooked. Your account dashboard is a more reliable source, as it centralizes all loan-related information. Additionally, if you’ve switched servicers, ensure your new servicer’s portal reflects accurate data, as transitions can sometimes lead to errors in forgiveness tracking. Regular account reviews act as a safeguard against such oversights.

In conclusion, treating your Navient account as a dynamic tool rather than a static record is essential for staying informed about forgiveness status. By systematically reviewing updates, understanding their implications, and maintaining thorough documentation, you position yourself to capitalize on forgiveness opportunities and address issues before they escalate. This disciplined approach transforms account review from a chore into a strategic practice in managing your student loans.

Forgiving Student Loans in NYC: A Step-by-Step Guide to Relief

You may want to see also

Frequently asked questions

You can check the status of your Navient student loans by logging into your Navient account online or contacting Navient’s customer service directly. Additionally, monitor communications from Navient or the U.S. Department of Education for updates on loan forgiveness programs.

Yes, Navient student loans may be eligible for federal forgiveness programs like Public Service Loan Forgiveness (PSLF), Income-Driven Repayment (IDR) forgiveness, or other targeted forgiveness initiatives. Eligibility depends on the type of loan and program requirements.

If you believe your Navient loans qualify for forgiveness but haven’t been processed, gather documentation supporting your eligibility (e.g., employment certification for PSLF) and contact Navient or the Department of Education to review your case. You may also seek assistance from a student loan ombudsman or legal aid.