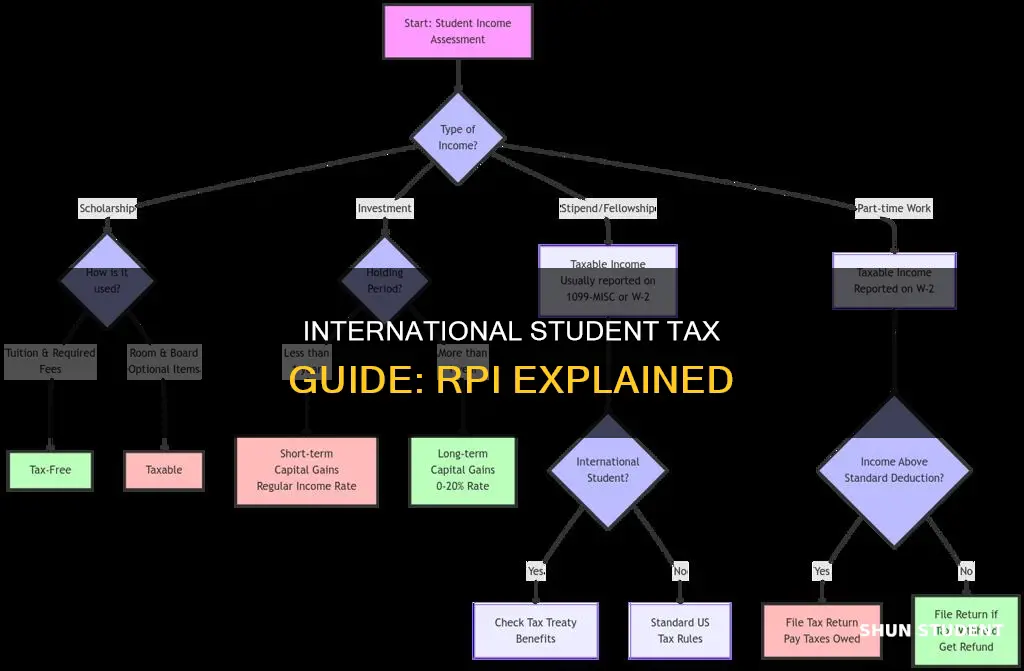

International students at RPI are considered nonresident aliens for tax purposes and are required to file tax returns if they were in the US during the previous calendar year and earned income. They may receive a W-2, a 1042-S, or both. The Form 1042-S will report fellowship stipends and payments exempt under a tax treaty, while all other payments are reported on a W-2. International students should wait until both forms are available before filing their tax returns. Additionally, international students will receive assistance from the Payroll or Student Employment Office during the hiring process.

| Characteristics | Values |

|---|---|

| Tax forms | W-4, IT-2104E, W-2, 1042S, 1040-NR |

| Tax assistance | Provided by the Payroll or Student Employment Office during the hiring process |

| Tax treaties | May be partially or completely exempt from tax |

| Tax status | International students are considered nonresident aliens for tax purposes |

| Tax returns | Required if in the US during the previous calendar year and earned income |

| Tax rates | Vary by state |

Explore related products

What You'll Learn

![]()

International students and tax treaties

International students on F-1 visas are considered nonresident aliens for tax purposes for the first five calendar years of their stay in the US. They are taxed only on US-sourced income. If their country of residence has signed a tax treaty with the US, they may be partially or completely exempt from tax.

International students may receive a W-2 only, a 1042S only, or both. The Form 1042S will report fellowship stipends and payments exempt under a tax treaty. All other payments are reported on a W-2. International students should wait until both forms have been made available before filing their tax returns.

Students from countries that have a tax treaty with the US that includes a wage article may claim exemption or a reduction of income tax withholding if the payment meets the requirements of the treaty and the student completes the required forms with the University's Tax Department. The taxes covered under a treaty exemption include Federal, Virginia, and/or D.C. tax. Maryland does not recognize tax treaties.

In order for the university to consider granting a tax withholding exception under a treaty provision, the student is required to complete Form 8233, Exemption from Withholding on Compensation for Independent Personal Services of a Nonresident Alien Individual. Additionally, students must complete a country-specific statement that details the terms of the treaty. Both forms, along with a list of applicable tax treaties, are available at the Tax Department. The university has the right to reject a Form 8233 if it has reason to believe that such exemption is not warranted or if the form is completed inaccurately. Since Forms 8233 and the country-specific statement must be submitted by the university to the IRS for their review and approval, it is imperative that these and all other tax documents be completed at the time of hire to avoid the withholding of tax or the delay of paychecks.

Loans for International Students: Where to Get Them?

You may want to see also

Explore related products

![]()

Tax exemptions for international students

International students in the US on an F-1 visa are considered nonresident aliens for tax purposes for the first five calendar years of their stay. During this time, they are exempt from FICA taxes on wages, including Social Security and Medicare taxes. However, they are required to file a US tax return (Form 1040-NR) for income from US sources. While there is no specific international student tax, the amount of tax an international student will have to pay depends on their personal circumstances.

International students may receive a W-2 form, a 1042-S form, or both. The Form 1042-S will report fellowship stipends and payments exempt under a tax treaty, while all other payments are reported on a W-2. International students should wait until both forms have been received before filing their tax returns.

Additionally, international students who are employed by a school, college, or university where they are enrolled at least half-time may be exempt from Social Security and Medicare taxes under the "student FICA exemption". This exemption applies to services performed for the purpose of pursuing a course of study. However, off-campus jobs or working for other employers do not qualify for this exemption.

It's important to note that the tax rules for international students can be complex, and specific tax treaties between the US and the student's home country may impact their tax liability. International students are advised to seek guidance from a qualified tax professional or refer to official government sources for the most accurate and up-to-date information.

International Student UCAS Deadlines: When to Apply

You may want to see also

Explore related products

![H&R Block Tax Software Deluxe + State 2024 with Refund Bonus Offer (Amazon Exclusive) Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51+fonAXhPL._AC_UY218_.jpg)

![TurboTax Deluxe 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71UbHaUeeUL._AC_UY218_.jpg)

![]()

Tax on graduate fellowship payments

Fellowship stipends and payments may be exempt from tax under a tax treaty. However, by law, taxes may be required to be withheld from graduate fellowship payments made to international students. Students who are US citizens for tax purposes do not have any withholding on their fellowship stipends, which are generally for tuition. All stipends and fellowships are considered by the IRS to be taxable income, to the extent that they exceed the cost of books, fees, equipment and supplies required for a course of instruction.

Any travel reimbursement to a graduate student that does not meet the criteria for a scholarship is considered taxable scholarship income. This is self-reported income per IRS Publication 970, and it is the recipient's responsibility to maintain records for these payments. A fellowship is an amount paid to an individual to aid in the pursuit of study or research to enhance their training in a specific field of interest. If a fellowship requires an individual to perform services, it will be considered compensation for those services and is subject to payroll wage reporting and withholding.

Fellowships are tax-free if the candidate is a degree student at an educational institution that maintains a regular faculty and curriculum and the amounts received are used to pay for tuition and fees required for enrollment or attendance, or for fees, books, supplies, and equipment required for courses. Amounts used for incidental expenses, such as room and board, travel, and optional equipment, are not tax-free.

International students are considered nonresident aliens for tax purposes and are taxed only on US-sourced income. They must file a tax return if they earned an income in the previous calendar year.

Understanding Tax Benefits: International Students and American Opportunity

You may want to see also

Explore related products

$13.9 $25

![]()

Tax forms for international students

International students in the US are required to file their tax returns if they were in the country during the previous calendar year and earned an income. Those on an F-1 visa are considered nonresident aliens for tax purposes and must pay tax on their income. This includes income from employment earnings, taxable scholarships, and fellowship grants.

International students should wait to receive their W-2 and 1042-S forms before filing their tax returns. The W-2 form reports all payments made to students during the calendar year, including income and taxable stipends. The 1042-S form reports fellowship stipends and payments exempt under a tax treaty.

International students who are nonresident aliens for tax purposes must file a US tax return (Form 1040-NR) for income from US sources. They may also need to submit Form 8843, an informational statement required by the IRS for nonresident taxpayers. This form should be submitted for every nonresident taxpayer present in the US during the previous calendar year, including spouses, partners, and children.

It is important to note that international students should seek advice from a qualified tax professional or the IRS for specific guidance on completing their tax forms.

International Students: Food Stamps Eligibility

You may want to see also

Explore related products

![]()

Tax on OPT income

OPT stands for Optional Practical Training, which is a program that allows international students to work in the US after graduation and gain practical experience. Students with F-1 visas may apply for 12 months of OPT after each level of education is completed. If you earn an income from an OPT, you will be required to pay taxes.

Tax Forms

Students on OPT are required to pay taxes on their income and will complete a W-4 tax form with their new employer before they begin to be paid. F-1 students on OPT may also need to fill out Form 8843, which is used for information by the IRS and is required of all F-1 students, even if they do not earn an income during the tax year. Additionally, international students may receive a W-2, a 1042S, or both. The Form 1042S will report fellowship stipends and payments exempt under a tax treaty, while all other payments are reported on a W-2.

Tax Status

International students on F-1 visas are generally considered nonresident aliens for tax purposes during the first five calendar years of their stay in the US. However, if an F-1 student has been in the US for more than five years, they will typically be considered a resident alien for tax purposes. This status will determine the tax forms that need to be completed and how the student will be taxed.

Tax Rates

OPT students are taxed on their wages at graduated rates from 10% to 37%, depending on their income level. Additionally, local, state, and federal taxes may be deducted from their income, and these deductions can be seen on their paystubs. The tax percentage withheld on scholarships and grants for F-1 and J-1 visa holders is 14%.

Tax Exemptions

F-1 students on OPT are exempt from FICA (Social Security and Medicare) taxes unless they have been in the United States for more than five years. Depending on their personal circumstances, F-1 students on OPT may also claim a tax treaty that can partially reduce or fully exempt their income from paying taxes.

International Students: Claiming Tax Refunds Made Easy

You may want to see also

Frequently asked questions

International students at RPI are required to pay taxes on their income, including graduate fellowship payments. They are also required to file tax returns if they were in the US during the previous calendar year and earned income.

International students at RPI can receive assistance with their taxes from the Payroll or Student Employment Office during the hiring process. They can also access tax-related information on the International Services for Students and Scholars web page.

International students at RPI may receive a W-2, a 1042-S, or both. The Form 1042-S will report fellowship stipends and payments exempt under a tax treaty, while all other payments are reported on a W-2.