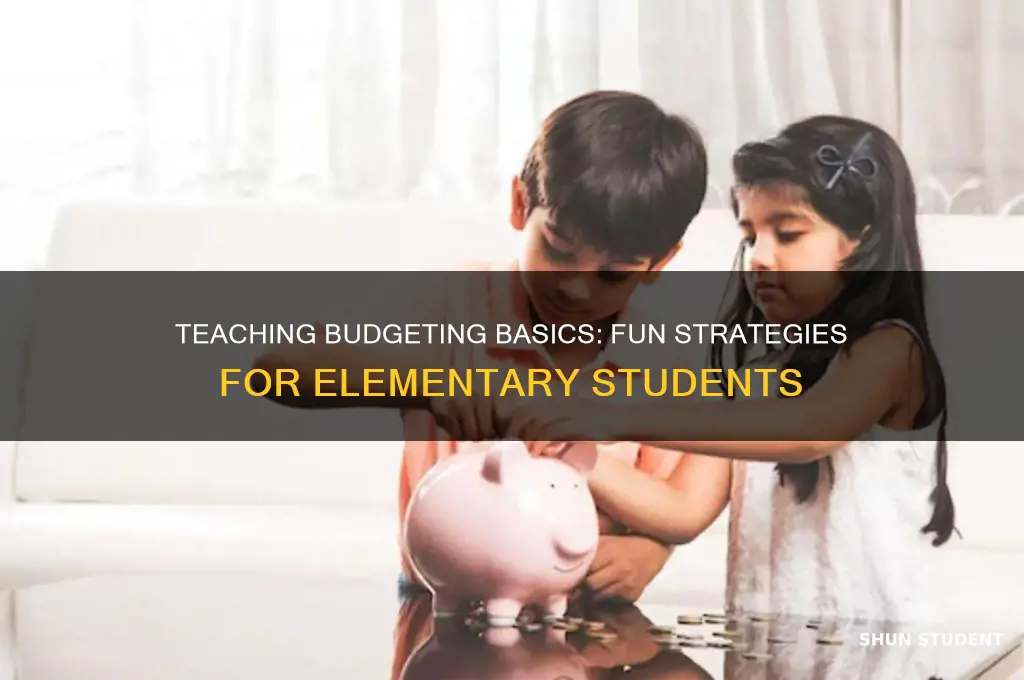

Teaching budgeting to elementary students is a valuable skill that lays the foundation for financial literacy and responsible money management. By introducing basic concepts like saving, spending, and sharing in a simple and engaging way, educators can help young learners understand the importance of making thoughtful financial decisions. Using age-appropriate tools such as piggy banks, visual charts, and interactive games, children can grasp the idea of prioritizing needs over wants and setting goals for their money. Incorporating real-life scenarios, like planning for a class party or saving for a toy, makes the lessons relatable and practical. Early exposure to budgeting not only empowers students to manage their allowance but also fosters habits that will benefit them throughout their lives.

Explore related products

What You'll Learn

- Use Real-Life Examples: Incorporate everyday scenarios like saving for toys or snacks to make budgeting relatable

- Hands-On Activities: Use play money, jars, or apps to simulate earning, saving, and spending

- Set Simple Goals: Teach kids to set small, achievable savings goals, like buying a favorite book

- Needs vs. Wants: Explain the difference between essentials (needs) and desires (wants) with clear examples

- Track Progress: Use charts or stickers to help kids visually track their savings and spending habits

![]()

Use Real-Life Examples: Incorporate everyday scenarios like saving for toys or snacks to make budgeting relatable

Teaching budgeting to elementary students becomes more engaging and understandable when you use real-life examples that resonate with their daily experiences. Children often have tangible goals, such as saving for a favorite toy, a special snack, or a trip to the movies. These scenarios provide a natural framework for introducing budgeting concepts. For instance, if a student wants a toy that costs $20 and they receive $5 per week as allowance, you can guide them to calculate how many weeks they need to save. This not only teaches them about saving but also introduces the idea of delayed gratification, a key aspect of financial literacy.

Incorporating everyday scenarios like saving for snacks can make budgeting feel less abstract and more relevant. For example, if a child wants to buy a $2 candy bar every day after school but only has $10 for the week, you can help them decide whether to buy the candy daily or save for something bigger. This exercise encourages critical thinking about priorities and trade-offs, essential skills for effective budgeting. Visual aids, such as a simple chart or jar to track savings, can further reinforce the lesson and make progress tangible.

Another effective approach is to simulate real-life shopping experiences. Set up a pretend store in the classroom with items priced at different amounts, such as stickers, pencils, or small toys. Give each student a fixed amount of "money" and let them decide how to spend or save it. This activity not only teaches budgeting but also introduces the concept of comparing prices and making informed decisions. Discussing their choices afterward can highlight the importance of planning and sticking to a budget.

Family involvement can also enhance the learning process. Encourage students to discuss their savings goals with their families and work together to create a budget. For example, if a child wants to save for a video game, they can contribute a portion of their allowance while their parents match a percentage of their savings. This collaborative approach reinforces the idea that budgeting is a shared responsibility and can lead to meaningful conversations about money management at home.

Finally, storytelling can be a powerful tool to illustrate budgeting concepts through relatable narratives. Share stories about characters who save for something they want, face challenges, and learn valuable lessons along the way. For instance, a story about a child saving for a bike by doing extra chores can demonstrate the connection between earning, saving, and spending. These stories not only entertain but also provide a moral framework for understanding the importance of budgeting in achieving goals. By grounding lessons in real-life examples, you make budgeting accessible, practical, and memorable for elementary students.

Empowering Struggling Learners: Strategies to Teach Backward Students Effectively

You may want to see also

Explore related products

![]()

Hands-On Activities: Use play money, jars, or apps to simulate earning, saving, and spending

Teaching budgeting to elementary students through hands-on activities makes abstract financial concepts tangible and engaging. One effective method is using play money to simulate earning, saving, and spending. Start by providing each student with a set of pretend bills and coins. Assign them "jobs" within a classroom economy, such as being a librarian, cleaner, or teacher’s assistant, and pay them a predetermined amount for completing tasks. This teaches them the value of work and earning. Next, introduce the concept of spending by setting up a classroom store where students can buy small items like stickers or pencils using their play money. Encourage them to make choices, such as whether to spend all their money at once or save for a more expensive item later. This activity reinforces the idea that resources are limited and requires decision-making.

Another practical approach is using jars to physically represent saving, spending, and sharing. Label three jars with these categories and give students play money or tokens to divide among them. For example, if a student earns 10 pretend dollars, they could put 4 in the saving jar, 5 in the spending jar, and 1 in the sharing jar. This visual method helps students understand the importance of allocating money for different purposes. You can also introduce goals, such as saving for a larger item, and have students track their progress over time. This activity not only teaches budgeting but also fosters responsibility and goal-setting skills.

For a more modern twist, incorporate budgeting apps designed for kids. Apps like RoosterMoney or Greenlight provide a digital platform for children to track their earnings, savings, and spending. Set up virtual chores and allowances within the app, allowing students to see their balances grow as they complete tasks. Many of these apps also include features for setting savings goals and monitoring progress. Using technology makes learning interactive and relatable for tech-savvy students, while also preparing them for digital financial tools they may use in the future.

Combining these methods can create a comprehensive learning experience. For instance, start with play money and jars to build a foundational understanding of budgeting, then transition to apps for a more advanced, real-world application. Throughout these activities, encourage discussions about financial choices and their consequences. Ask questions like, "What would happen if you spent all your money at once?" or "Why is it important to save for the future?" These conversations deepen their understanding and critical thinking skills.

Finally, reinforce learning by connecting these activities to real-life scenarios. For example, after using play money in the classroom store, discuss how they might apply similar decisions when shopping with their parents. If using jars, relate saving to a long-term goal, like buying a toy or game. By bridging the gap between simulation and reality, students are more likely to retain the lessons and apply them in their daily lives. Hands-on activities not only make budgeting fun but also empower elementary students with essential financial skills.

Teaching Romance Novels: Engaging Students with Love Stories and Literary Analysis

You may want to see also

Explore related products

$10.17 $16.99

![]()

Set Simple Goals: Teach kids to set small, achievable savings goals, like buying a favorite book

Teaching elementary students about budgeting starts with helping them understand the importance of setting simple, achievable goals. At this age, kids are just beginning to grasp the concept of money, so it’s crucial to keep goals small and relatable. For example, encourage them to save for something they genuinely want, like a favorite book, a toy, or a special snack. This not only makes the goal tangible but also motivates them to stay committed. Begin by asking them to identify something they’d like to buy and then break it down into manageable steps. This process teaches them that saving is purposeful and rewarding.

To set these goals effectively, guide students in creating a clear plan. Start by determining the cost of the item they want and then help them calculate how much they need to save each week or month. For instance, if a book costs $10 and they receive $2 per week as allowance, explain that saving half of their allowance for five weeks will help them reach their goal. Use visual tools like charts or jars to track progress, as this reinforces the idea of working toward a target. Visual aids also make the process more engaging and easier for young learners to understand.

Encourage kids to think about their priorities when setting goals. Teach them to distinguish between needs and wants, emphasizing that saving for a goal might mean skipping smaller purchases along the way. For example, if they want to buy a book, they might decide to save their allowance instead of spending it on candy. This lesson helps them develop decision-making skills and understand the trade-offs involved in budgeting. It also fosters patience and delayed gratification, which are essential financial habits.

Regularly check in with students to discuss their progress and celebrate milestones. If they’ve saved half the amount needed for their book, acknowledge their achievement and encourage them to keep going. Celebrating small wins keeps them motivated and reinforces the idea that saving is a positive habit. Additionally, use these check-ins to troubleshoot any challenges they’re facing, such as temptation to spend their savings. This ongoing support helps them stay focused and builds their confidence in managing money.

Finally, tie the concept of goal-setting to real-life experiences. Take them on a trip to a bookstore or show them how to compare prices online to find the best deal on their desired book. This practical application deepens their understanding of budgeting and makes the goal even more exciting. By combining hands-on activities with clear, achievable targets, you’re not only teaching them how to save but also laying the foundation for lifelong financial literacy.

Effective Strategies for Teaching Students with Attention Deficit Disorder

You may want to see also

Explore related products

![]()

Needs vs. Wants: Explain the difference between essentials (needs) and desires (wants) with clear examples

Teaching elementary students about budgeting begins with helping them understand the fundamental difference between needs and wants. This concept is the cornerstone of financial literacy, as it lays the groundwork for making thoughtful spending decisions. Start by defining these terms in simple, relatable language. Needs are essential items or services required for survival, safety, and well-being, such as food, shelter, clothing, and education. Wants, on the other hand, are desires for things that are not necessary but would be nice to have, like toys, video games, or extra snacks. Use visual aids, like a chart or pictures, to illustrate this distinction and make it easier for students to grasp.

To reinforce the concept, provide clear examples that resonate with their daily lives. For instance, explain that a warm coat in winter is a need because it protects them from the cold, while a trendy jacket with a favorite cartoon character on it is a want. Another example could be that a balanced meal at home is a need, whereas eating at a fast-food restaurant is a want. Encourage students to share their own examples to help them internalize the difference. This interactive approach ensures they actively engage with the material and apply it to their own experiences.

Hands-on activities can further solidify their understanding. For example, create a sorting game where students categorize items as needs or wants. Provide a list of items like "a bicycle," "a toothbrush," "a smartphone," or "a pizza," and have them place each item in the correct category. Discuss any disagreements to clarify why certain items fall into one category over the other. This activity not only makes learning fun but also helps students think critically about their choices.

It’s important to emphasize that while wants are not inherently bad, they should be prioritized after needs are met. Teach students that budgeting is about balancing these two categories. For instance, if they receive an allowance, they should first allocate money for needs (like school supplies) and then decide if they have enough left for a want (like a new toy). This lesson helps them develop a mindset of responsibility and planning.

Finally, relate the concept of needs vs. wants to real-life scenarios. Discuss how families make budgeting decisions, such as choosing to buy generic groceries to save money for a family vacation. Explain that even adults face these choices daily. By connecting the lesson to their own lives and the lives of those around them, students will see the practical value of distinguishing between needs and wants and how it applies to long-term financial health.

Effective Strategies for Teaching Adjectives to Autistic Learners

You may want to see also

Explore related products

![]()

Track Progress: Use charts or stickers to help kids visually track their savings and spending habits

Teaching elementary students how to track their progress in budgeting is a crucial step in helping them develop financial literacy. One effective method is to use charts to visually represent their savings and spending habits. Start by creating a simple bar chart or graph where the x-axis represents time (weeks or months) and the y-axis represents the amount of money saved or spent. Each time the child adds to their savings or makes a purchase, update the chart together. This visual tool helps them see their progress at a glance, making abstract financial concepts more tangible. For younger students, use brightly colored markers or crayons to make the chart engaging and fun.

In addition to charts, stickers can be a motivating way to track progress. Designate a sticker chart specifically for budgeting milestones, such as saving a certain amount or sticking to a spending plan for a week. For example, every time a child saves $5, they earn a sticker. Once the chart is filled, reward them with a small prize or privilege, like choosing a family activity. This reinforces positive financial behavior and keeps them excited about their goals. Ensure the stickers are visually appealing and age-appropriate to maintain their interest.

Another effective strategy is to combine charts and stickers into a savings thermometer. Draw a large thermometer on poster board, with increments representing savings goals. As the child saves, color in the thermometer and add stickers to mark their progress. This method is particularly effective for long-term savings goals, like buying a toy or contributing to a family vacation fund. It provides a clear visual of how close they are to their goal, fostering a sense of accomplishment.

For tech-savvy students, consider using digital tools to track progress. Many budgeting apps or websites offer kid-friendly interfaces with charts, graphs, and virtual stickers. These tools can sync with allowance or savings accounts, automatically updating their progress. However, always ensure the platforms are safe and age-appropriate. Pair digital tracking with regular discussions to explain the numbers and reinforce the lessons learned.

Finally, make tracking progress a routine activity. Set aside a specific time each week to review the charts, stickers, or digital tools together. Use this opportunity to discuss their spending and saving decisions, asking open-ended questions like, "What helped you save more this week?" or "How do you feel about your progress so far?" This not only keeps them accountable but also encourages critical thinking about their financial habits. Consistency is key to helping them internalize the importance of tracking their budget.

Effective Strategies for Teaching English to Non-English Speaking Students

You may want to see also

Frequently asked questions

The best age to start teaching budgeting to elementary students is around 5 to 7 years old. At this age, children begin to understand basic concepts of money, such as coins and bills, and can grasp simple ideas like saving and spending.

Use hands-on activities like playing store, using play money, or creating a classroom economy. Incorporate games, visual aids, and real-life examples to make learning fun and relatable.

Focus on three main concepts: earning (understanding the value of work), saving (setting aside money for future goals), and spending (making thoughtful choices about how to use money).

Use examples like saving allowance for a toy, deciding between buying candy or saving for a bigger purchase, or planning a family outing with a limited budget. Relate lessons to their daily experiences.

Utilize piggy banks, budgeting apps designed for kids, worksheets, and storybooks about money. Online resources and interactive games can also reinforce learning in a fun way.