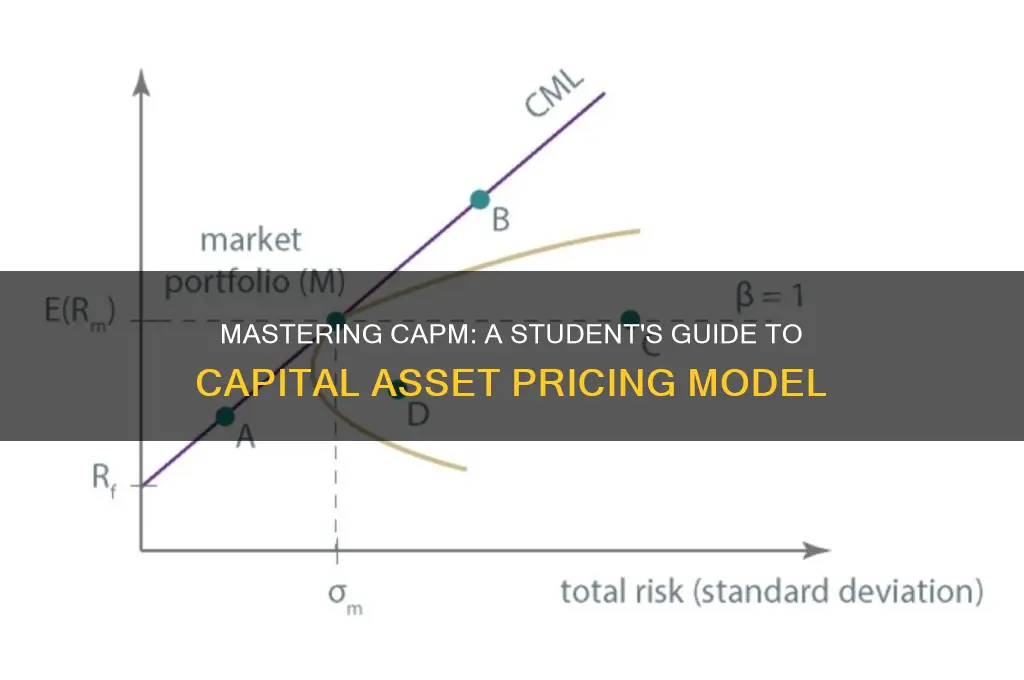

Teaching your students about the Capital Asset Pricing Model (CAPM) requires a structured and intuitive approach. Begin by explaining the fundamental concept of CAPM as a tool to determine the expected return of an investment, considering its risk relative to the overall market. Introduce key terms such as systematic risk (beta), risk-free rate, and market return, ensuring students grasp their significance. Use real-world examples and visual aids, like graphs illustrating the Security Market Line (SML), to make abstract ideas tangible. Encourage hands-on practice through exercises involving beta calculation and expected return estimation. Finally, relate CAPM to broader financial decision-making, emphasizing its role in portfolio management and investment analysis, to help students see its practical applications.

| Characteristics | Values |

|---|---|

| Definition | A model that describes the relationship between systematic risk and expected return for assets. |

| Key Formula | ( E(R_i) = R_f + \beta_i (E(R_m) - R_f) ), where ( E(R_i) ) = expected return of asset, ( R_f ) = risk-free rate, ( \beta_i ) = beta of asset, ( E(R_m) ) = expected market return. |

| Risk-Free Rate (R_f) | Latest U.S. Treasury bond yield (e.g., 3-month T-bill rate: ~5.0% as of Oct 2023). |

| Market Return (E(R_m)) | Historical average S&P 500 return (~10% annually, adjusted for inflation). |

| Beta ((\beta)) | Measure of systematic risk; calculated as covariance of asset returns with market returns divided by market variance. |

| Systematic vs. Unsystematic Risk | Focus on systematic risk (market risk), which cannot be diversified away, unlike unsystematic risk. |

| Teaching Tools | Use Excel simulations, CAPM calculators, and real-world stock data (e.g., Apple, Tesla) to calculate beta and expected returns. |

| Assumptions | Efficient markets, rational investors, no taxes or transaction costs, and investors are risk-averse. |

| Limitations | Assumes beta is constant, ignores other risk factors (e.g., size, value), and relies on historical data. |

| Practical Applications | Used in portfolio management, cost of equity calculation, and investment decision-making. |

| Latest Data Sources | Yahoo Finance, Bloomberg, and Federal Reserve Economic Data (FRED) for up-to-date market returns and risk-free rates. |

| Visual Aids | Security Market Line (SML) graphs to illustrate the relationship between beta and expected returns. |

| Case Studies | Analyze historical performance of companies like Amazon or Netflix to demonstrate CAPM application. |

| Interactive Learning | Use platforms like Khan Academy or Investopedia for quizzes and tutorials on CAPM concepts. |

Explore related products

$46.99 $62.99

What You'll Learn

- CAPM Basics: Explain risk, return, and market portfolio concepts in simple terms

- Formula Breakdown: Teach the CAPM equation and its components step-by-step

- Risk-Free Rate: Clarify its role and how to identify it in practice

- Beta Calculation: Demonstrate how to measure systematic risk using historical data

- Application Examples: Use real-world scenarios to illustrate CAPM’s practical use

![]()

CAPM Basics: Explain risk, return, and market portfolio concepts in simple terms

Imagine you’re at a buffet. Each dish represents an investment, with its own flavor (return) and spice level (risk). The Capital Asset Pricing Model (CAPM) is like a guide that helps you balance your plate—maximizing flavor while managing how much heat you can handle. In CAPM, risk isn’t just about losing money; it’s about how much an investment’s returns bounce around compared to the overall market. Think of it as the unpredictability of a rollercoaster: the wilder the ride, the higher the risk. Return, on the other hand, is the reward for taking that risk—the profit you earn from your investment. CAPM ties these together by showing how much extra return you should expect for taking on additional risk.

Now, let’s talk about the market portfolio. Picture every investment in the world combined into one giant pie—stocks, bonds, real estate, you name it. This pie is the market portfolio, and it’s the benchmark for all other investments. CAPM assumes this portfolio is perfectly diversified, meaning all unsystematic risks (risks specific to individual investments) are canceled out. What’s left is systematic risk, or market risk, which affects everything equally. This is where the beta comes in—a measure of how much an individual investment moves with the market. A beta of 1 means it moves in lockstep with the market, while a beta above 1 means it’s more volatile, and below 1 means it’s less so.

To teach this, start with a simple analogy: compare investing to driving. Risk is like driving in stormy weather—the more unpredictable the conditions, the riskier the drive. Return is the destination—how far you get for your effort. The market portfolio is the highway system, representing all possible routes. Now, introduce beta as the car’s speed relative to traffic. A sports car (high beta) accelerates faster but is riskier, while a sedan (low beta) is steadier. Use real-world examples: Apple stock (high beta) vs. a utility company (low beta).

Next, walk through the CAPM formula: *Expected Return = Risk-Free Rate + Beta × (Market Return – Risk-Free Rate)*. Break it down step-by-step. The risk-free rate is the return from a safe investment, like a Treasury bond—think of it as staying home instead of driving. The market return is the average return of the highway system. Beta adjusts this for the investment’s volatility. For instance, if the risk-free rate is 2%, the market return is 8%, and an investment has a beta of 1.5, its expected return is 2% + 1.5 × (8% – 2%) = 11%.

Finally, emphasize the practical takeaway: CAPM helps investors decide if an investment’s return justifies its risk. If an asset’s expected return matches its risk, it’s fairly priced. If it’s higher, it’s undervalued; if lower, overvalued. Caution students that CAPM assumes a perfectly efficient market, which isn’t always true. Real-world factors like taxes, transaction costs, and investor behavior can skew results. Still, CAPM is a powerful tool for understanding the risk-return tradeoff—like knowing how much spice you can handle before biting into that buffet dish.

Inspiring Moments and Lessons Learned During My Student Teaching Journey

You may want to see also

Explore related products

![SHRM CP Exam Prep Study Cards: SHRM CP 2025-2026 Test Prep for the Society for Human Resource Management Certification with Practice Test Questions [Full Color Cards]](https://m.media-amazon.com/images/I/61GMgkTStPL._AC_UL320_.jpg)

![]()

Formula Breakdown: Teach the CAPM equation and its components step-by-step

The Capital Asset Pricing Model (CAPM) is a cornerstone of modern finance, but its equation can seem daunting at first glance. To demystify it, break it down into its core components: Expected Return (ER) = Risk-Free Rate (Rf) + Beta (β) × (Market Return (Rm) – Risk-Free Rate (Rf)). Start by explaining each variable in plain language. The Risk-Free Rate is the return an investor can expect from an investment with zero risk, like a U.S. Treasury bond. Beta measures a stock’s volatility relative to the market—a beta of 1 means the stock moves in line with the market, while values above or below 1 indicate higher or lower volatility. The Market Return is the expected return of the overall market, often represented by an index like the S&P 500. Finally, the Market Risk Premium (Rm – Rf) quantifies the additional return investors demand for taking on market risk.

Next, illustrate how these components interact. Use a real-world example: suppose the risk-free rate is 2%, the market return is 8%, and a stock has a beta of 1.5. Plug these values into the equation: ER = 2% + 1.5 × (8% – 2%). Simplify step-by-step: first calculate the market risk premium (6%), then multiply by beta (9%), and finally add the risk-free rate (11%). The expected return is 11%. This example shows how CAPM quantifies the relationship between risk and return, rewarding investors for taking on additional volatility.

Caution students about common pitfalls when applying CAPM. Beta, for instance, is historical and may not predict future volatility accurately. The risk-free rate and market return are assumptions that can vary widely depending on economic conditions. Emphasize that CAPM is a theoretical model, not a crystal ball. It’s most useful for comparing investments within the same market context, not for precise predictions.

To reinforce understanding, assign a hands-on activity. Provide students with historical data for a stock and the market, and ask them to calculate its beta using Excel or a financial calculator. Then, have them use CAPM to estimate the stock’s expected return, comparing it to its actual historical return. This exercise bridges theory and practice, highlighting both the strengths and limitations of the model.

Conclude by framing CAPM as a foundational tool in portfolio management. It’s not just about calculating returns—it’s about understanding how risk and reward are interconnected. Encourage students to think critically about its assumptions and applications, fostering a deeper appreciation for the complexities of financial decision-making. With this step-by-step breakdown, CAPM becomes less of a formula and more of a lens for analyzing investment opportunities.

Empowering Educators: How Teacher Training Transforms Student Learning Outcomes

You may want to see also

Explore related products

![]()

Risk-Free Rate: Clarify its role and how to identify it in practice

The risk-free rate is the bedrock of the Capital Asset Pricing Model (CAPM), serving as the baseline return an investor can expect without taking any risk. In theory, it represents the return on an investment with zero uncertainty, typically approximated by the yield on a short-term government bond. Understanding its role is crucial because it anchors the entire model, influencing how we measure risk premiums and evaluate investment opportunities. Without a clear grasp of the risk-free rate, the CAPM’s framework loses its foundation, rendering its calculations meaningless.

In practice, identifying the risk-free rate isn’t as straightforward as it sounds. While short-term U.S. Treasury bills are commonly used as a proxy, this choice assumes a U.S.-centric perspective. For students in other countries, local government bonds denominated in their home currency are more appropriate. Additionally, the maturity of the bond matters; a 3-month Treasury bill is often preferred for its liquidity and minimal interest rate risk. Caution students against using longer-term bonds, as their yields incorporate expectations of future interest rate changes, deviating from the "risk-free" ideal.

A persuasive argument for the risk-free rate’s importance lies in its role as the opportunity cost of capital. When an investor chooses a risky asset over a risk-free one, the risk-free rate represents the return they forgo. This opportunity cost is a critical component of the CAPM’s equation, as it helps determine whether the expected return on a risky investment justifies the additional risk taken. Emphasize to students that ignoring this baseline can lead to mispriced assets and suboptimal investment decisions.

To illustrate the risk-free rate’s practical application, consider a scenario where a student is evaluating a stock with an expected return of 10%. If the risk-free rate is 2%, the excess return (8%) must compensate for the stock’s systematic risk. Here, the risk-free rate acts as a benchmark, allowing the student to assess whether the stock’s return adequately rewards the investor for bearing risk. Encourage students to use real-time data from financial platforms like Bloomberg or Yahoo Finance to track risk-free rates and observe how they fluctuate with economic conditions.

In conclusion, teaching the risk-free rate requires a blend of theoretical clarity and practical application. Start by defining its role as the foundation of the CAPM, then guide students in identifying it using appropriate proxies like short-term government bonds. Stress its significance as the opportunity cost of capital and illustrate its use through real-world examples. By mastering this concept, students will not only understand the CAPM’s mechanics but also develop a critical eye for evaluating investment opportunities in a risk-adjusted context.

Teaching Generalization Strategies for Students with Learning Disabilities

You may want to see also

Explore related products

![]()

Beta Calculation: Demonstrate how to measure systematic risk using historical data

Measuring systematic risk through beta calculation is a cornerstone of the Capital Asset Pricing Model (CAPM). Beta quantifies an asset’s volatility relative to the overall market, providing insight into how its returns move in response to market fluctuations. To teach this concept effectively, begin by explaining that beta is not about total risk but specifically about market risk—the risk that cannot be diversified away. Use historical data to illustrate how beta is calculated, emphasizing its reliance on past performance to predict future behavior. For instance, a beta of 1 indicates the asset moves in line with the market, while a beta greater than 1 suggests higher volatility and a beta less than 1 indicates lower volatility.

To demonstrate beta calculation, start with a step-by-step process using historical price data for the asset and the market index (e.g., S&P 500). First, calculate the daily returns for both the asset and the market over a specific period, such as one year. Next, find the covariance between the asset’s returns and the market’s returns. Divide this covariance by the variance of the market returns to obtain beta. For example, if the covariance is 0.002 and the market variance is 0.005, beta would be 0.4. This hands-on approach helps students see the mechanics behind beta and its interpretation.

While historical data is invaluable for beta calculation, caution students about its limitations. Beta assumes that past relationships between the asset and the market will persist, which may not always hold true, especially during market regime changes or economic shifts. Additionally, beta is sensitive to the time period chosen for analysis. A beta calculated over one year may differ significantly from one calculated over five years. Encourage students to experiment with different time frames to understand how beta can vary and to critically evaluate its reliability.

To make beta calculation more engaging, incorporate real-world examples. Compare the betas of tech stocks like Apple (typically high beta) and utility stocks (typically low beta) to highlight how different sectors respond to market movements. Use tools like Excel or financial software to automate calculations, allowing students to focus on interpreting results rather than manual computation. By grounding beta in practical applications, students can better grasp its role in portfolio management and investment decision-making.

In conclusion, teaching beta calculation requires a blend of theoretical explanation, hands-on practice, and critical analysis. By using historical data to demonstrate how systematic risk is measured, students gain a tangible understanding of beta’s significance in CAPM. Encourage them to question assumptions, explore variations, and apply beta in diverse contexts to build a robust foundation in this essential financial concept.

Effective Strategies for Teaching College Biology: Engaging and Inspiring Students

You may want to see also

Explore related products

$50.75 $64.99

$110 $136.95

![]()

Application Examples: Use real-world scenarios to illustrate CAPM’s practical use

Example 1: Portfolio Construction for a Retiree

Imagine a 65-year-old retiree with a $500,000 portfolio seeking stable income and capital preservation. Using CAPM, an advisor calculates the expected return of each asset class relative to its systematic risk (beta). Treasury bonds, with a beta near 0, offer a low but stable return, while tech stocks, with a beta of 1.5, carry higher volatility. By blending assets based on their beta-adjusted returns, the advisor constructs a portfolio targeting a 6% annual return with acceptable risk. This real-world application demonstrates how CAPM helps align investment choices with risk tolerance and financial goals.

Analysis of Market Anomalies

CAPM’s practical use isn’t limited to textbook scenarios—it’s often tested against market anomalies. For instance, the small-firm effect suggests small-cap stocks outperform large-cap stocks, contradicting CAPM’s assumption that higher returns compensate for higher risk. In 2020, small-cap indices outpaced the S&P 500 by 15% during the post-pandemic recovery, despite similar betas. This anomaly highlights CAPM’s limitations but also underscores its value as a baseline for identifying deviations from expected returns, prompting investors to explore alternative models like the Fama-French Three-Factor Model.

Step-by-Step Application in Corporate Finance

A mid-sized tech company is evaluating a $10 million R&D project with a beta of 1.3. The risk-free rate is 2%, the market return is 8%, and the company’s cost of equity must reflect its systematic risk. Using CAPM (Required Return = Risk-Free Rate + Beta × (Market Return – Risk-Free Rate)), the project’s required return is 9.8%. If the project’s expected return is only 9%, it’s rejected. This example shows how CAPM quantifies the trade-off between risk and return in capital budgeting, ensuring investments meet shareholder expectations.

Comparative Analysis: CAPM vs. Real Estate Investment

Real estate investors often overlook CAPM, but it’s a powerful tool for assessing rental property risk. Consider a $200,000 apartment in a growing urban area with a beta of 0.8 (derived from historical price correlations with the market). Using CAPM, the expected return is 7.2% (2% risk-free rate + 0.8 × (8% market return – 2%)). If the property’s projected cash-on-cash return is 6%, it underperforms relative to its risk. This comparative analysis encourages investors to diversify into assets with better risk-adjusted returns, even outside traditional equity markets.

Persuasive Case for Individual Investors

For individual investors, CAPM demystifies the relationship between risk and reward. Take a 30-year-old investor allocating 80% to stocks (beta = 1) and 20% to bonds (beta = 0). Their portfolio beta is 0.8, and CAPM predicts a 7.2% return. If their actual return is 9%, they’ve outperformed the market or benefited from unsystematic risk. This insight empowers investors to rebalance portfolios, exploit inefficiencies, or adjust expectations. By grounding decisions in CAPM, even novice investors can navigate markets with greater confidence and precision.

Handling Student Advances: A Teacher's Guide to Professional Boundaries

You may want to see also

Frequently asked questions

The Capital Asset Pricing Model (CAPM) is a financial model used to determine the expected return of an investment based on its risk relative to the overall market. It is important to teach because it helps students understand the relationship between risk and return, a fundamental concept in finance, and provides a framework for evaluating investment decisions.

The CAPM formula is: *Expected Return = Risk-Free Rate + Beta × (Market Return – Risk-Free Rate)*. Simplify by explaining each component: the risk-free rate is a safe return (e.g., Treasury bonds), beta measures an asset’s volatility compared to the market, and the market return is the average return of the overall market. Use real-world examples to illustrate how these elements interact.

Use case studies of stocks or portfolios to calculate expected returns using CAPM. Another activity is to simulate market scenarios with different risk-free rates, betas, and market returns, allowing students to see how changes in these variables affect expected returns. Additionally, comparing CAPM results to actual historical returns can reinforce its practical application.

Common misconceptions include assuming CAPM always predicts accurate returns (it’s a theoretical model, not a guarantee) or confusing beta with total risk (beta measures systematic risk, not all risks). Address these by emphasizing CAPM’s limitations and clarifying the distinction between systematic and unsystematic risk through examples and discussions.