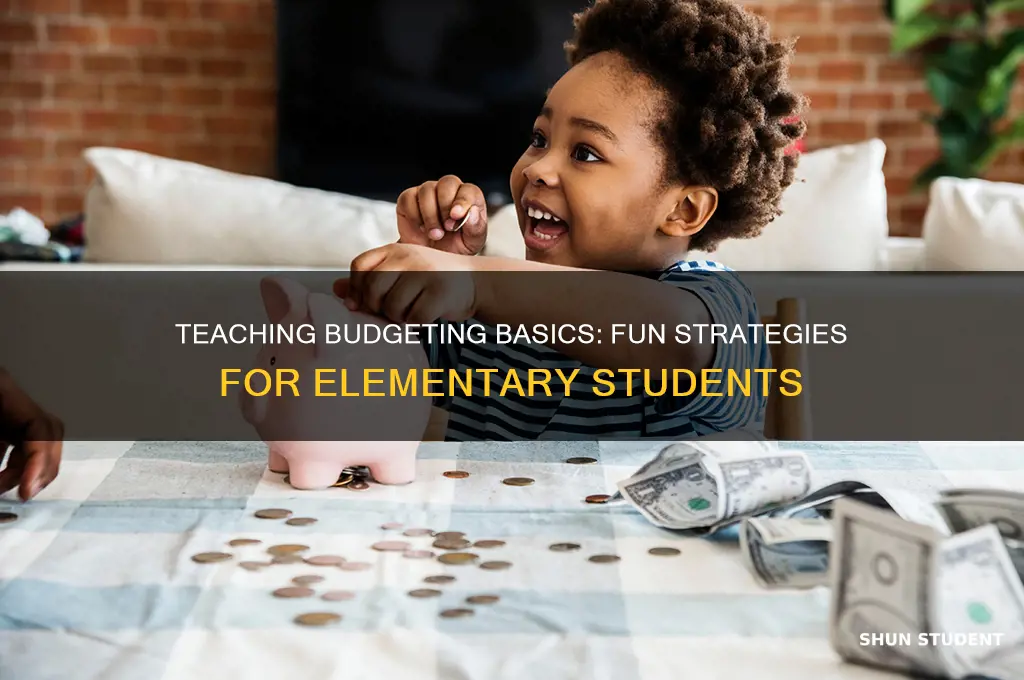

Teaching budgeting to elementary students is a valuable skill that lays the foundation for financial literacy and responsible money management later in life. By introducing basic concepts like saving, spending, and sharing in a simple and engaging way, educators can help young learners understand the importance of making thoughtful financial decisions. Using hands-on activities, visual aids, and relatable examples, such as allowance or saving for a toy, makes abstract ideas tangible and fun. Early exposure to budgeting not only fosters financial awareness but also instills habits like goal-setting and prioritizing, empowering students to navigate their financial futures with confidence.

Explore related products

What You'll Learn

- Using Real-Life Examples: Incorporate everyday scenarios like saving for toys or treats to make budgeting relatable

- Hands-On Activities: Use play money, jars, or games to simulate earning, saving, and spending decisions

- Goal Setting: Teach students to set short-term goals, like buying a small item, to practice budgeting

- Needs vs. Wants: Differentiate between essentials (needs) and desires (wants) to prioritize spending wisely

- Tracking Progress: Introduce simple charts or journals to help students monitor their saving and spending habits

![]()

Using Real-Life Examples: Incorporate everyday scenarios like saving for toys or treats to make budgeting relatable

Elementary students often struggle to grasp abstract financial concepts like budgeting. By grounding lessons in tangible, everyday scenarios—such as saving for a coveted toy or a special treat—educators can bridge this gap. For instance, a 7-year-old might want a $20 action figure but only receives $5 weekly allowance. This real-life example becomes a natural framework for teaching goal-setting, delayed gratification, and basic math skills. The familiarity of the situation keeps students engaged and helps them see budgeting as a practical tool, not just a classroom exercise.

To implement this approach, start by asking students about their personal financial goals. Are they saving for a video game, a pet, or a trip to the ice cream shop? Use these responses to create tailored scenarios. For younger students (ages 5–7), focus on simple, short-term goals like saving for a sticker pack or a small toy. Older elementary students (ages 8–10) can tackle more complex objectives, such as budgeting for a birthday gift or a class field trip. Pair these scenarios with visual aids like charts or jars to track progress, making the process concrete and rewarding.

One effective strategy is to simulate real-life budgeting through hands-on activities. For example, set up a classroom "store" where students can "buy" items using play money. Assign prices to items like pencils, erasers, or snacks, and give each student a fixed budget. This activity not only reinforces budgeting skills but also teaches decision-making and prioritization. For added realism, introduce discounts or sales to mimic real-world shopping experiences. Such activities make learning interactive and memorable, ensuring students retain the lessons long after the activity ends.

However, educators must be mindful of potential pitfalls. Avoid scenarios that highlight financial disparities among students, as this can lead to discomfort or embarrassment. Instead, focus on universal goals that resonate with all students, such as saving for a class reward or a group activity. Additionally, ensure the math involved is age-appropriate; overly complex calculations can frustrate younger learners. For instance, limit budgeting exercises for 6-year-olds to single-digit prices and simple addition, while 10-year-olds can handle multi-step problems involving percentages or fractions.

In conclusion, using real-life examples to teach budgeting transforms abstract concepts into actionable skills. By anchoring lessons in relatable scenarios like saving for toys or treats, educators make financial literacy accessible and engaging for elementary students. This approach not only equips them with essential life skills but also fosters a sense of empowerment and responsibility. With careful planning and sensitivity to students' developmental stages, real-life budgeting examples can become a cornerstone of effective financial education.

Can Teachers Sue Students for False Accusations? Legal Insights

You may want to see also

Explore related products

![]()

Hands-On Activities: Use play money, jars, or games to simulate earning, saving, and spending decisions

Elementary students learn best by doing, and hands-on activities with play money, jars, or games transform abstract budgeting concepts into tangible experiences. For instance, a simple activity involves giving each student $20 in play money and a list of items with varying costs (e.g., $2 for a toy car, $5 for a book, $10 for a board game). Students must decide how to allocate their funds, practicing prioritization and trade-offs. This activity, suitable for ages 6–10, reinforces the idea that choices have consequences and resources are limited.

To deepen the lesson, incorporate jars labeled "Save," "Spend," and "Share" to introduce the concept of budgeting categories. Provide students with $10 weekly in play money and instruct them to divide it among the jars. For younger students (ages 5–7), use visual aids like stickers or drawings to represent savings goals, such as a new toy or a class treat. Older students (ages 8–11) can track their decisions over time, learning how consistent saving leads to long-term goals. This method not only teaches budgeting but also fosters responsibility and delayed gratification.

Games like "Budget Bingo" or "Money Maze" add an element of competition and fun. In "Budget Bingo," students fill their cards with items they’d buy within a $50 budget, then cross them off as the teacher calls out prices. The first to complete a row wins. For "Money Maze," create a life-sized board game where students roll dice to move through scenarios like "Earn $10 for chores" or "Spend $5 on snacks." Each decision impacts their final balance, making the lesson engaging and memorable. These games are ideal for group settings and work well with students aged 7–12.

A cautionary note: while hands-on activities are effective, they require clear instructions and supervision. Ensure play money and props are age-appropriate and durable. For younger students, keep activities short (10–15 minutes) to maintain focus. For older students, extend the duration (20–30 minutes) to allow for deeper decision-making. Always debrief after the activity, asking questions like, "Why did you choose to save instead of spend?" or "What would you do differently next time?" This reflection solidifies learning and encourages critical thinking.

In conclusion, hands-on activities with play money, jars, or games are powerful tools for teaching budgeting to elementary students. They make abstract concepts concrete, encourage decision-making, and provide immediate feedback. By tailoring activities to age groups and incorporating reflective discussions, educators can ensure students not only understand budgeting but also develop habits that will benefit them throughout their lives.

Engaging Students: Creative Strategies for Teaching Film Analysis and Appreciation

You may want to see also

Explore related products

![]()

Goal Setting: Teach students to set short-term goals, like buying a small item, to practice budgeting

Elementary students often struggle with delayed gratification, making budgeting an abstract and challenging concept. Introducing short-term goal setting bridges this gap by providing tangible, achievable targets. For instance, a student might aim to buy a $5 toy within two months. This specific goal transforms budgeting from a vague idea into a concrete plan, fostering both financial literacy and self-discipline.

To implement this approach, start by helping students identify a small, desirable item within their financial reach. Encourage them to calculate how much they need to save weekly or monthly to achieve their goal. For younger students (ages 6–8), use visual aids like sticker charts or jars to represent progress. Older elementary students (ages 9–11) can benefit from simple spreadsheets or budgeting apps designed for kids. The key is to make the process interactive and relatable, ensuring students stay engaged.

A common pitfall is setting goals that are too ambitious or unrealistic. For example, a $20 video game might be out of reach for a student saving $1 a week. Instead, guide them toward smaller, incremental goals that build confidence. Additionally, emphasize flexibility—if a student falls short one week, help them adjust their plan rather than abandon it. This teaches resilience and adaptability, essential skills for long-term financial health.

The takeaway is clear: short-term goal setting turns budgeting into a game of progress and achievement. By focusing on small, attainable milestones, students not only learn to manage money but also develop a sense of accomplishment. This foundational skill sets the stage for more complex financial decisions later in life, proving that even the simplest goals can have profound, lasting impact.

Empowering Educators: Strategies for Teaching Students with Schizophrenia

You may want to see also

Explore related products

![]()

Needs vs. Wants: Differentiate between essentials (needs) and desires (wants) to prioritize spending wisely

Children as young as 3 can grasp the concept of delayed gratification, according to a study by the University of Minnesota. This foundational understanding is crucial when teaching elementary students about budgeting, particularly the distinction between needs and wants. At this age, their brains are wired to seek immediate rewards, so framing the conversation around essential needs versus desirable wants helps them develop a mindset for long-term financial health.

Step 1: Define Needs and Wants with Concrete Examples

Start by explaining that *needs* are items or services essential for survival and well-being, such as food, shelter, clothing, and education. *Wants*, on the other hand, are desires that make life more enjoyable but are not necessary, like toys, snacks, or the latest video game. Use age-appropriate visuals: a chart with pictures of a sandwich (need) versus a candy bar (want), or a house (need) versus a swimming pool (want). For younger students (ages 5–7), keep it simple with one-word associations: "apple" (need) vs. "ice cream" (want).

Step 2: Engage in Interactive Activities

Turn learning into a game. Provide students with a list of items (e.g., shoes, pizza, bicycle, doctor’s visit) and have them sort them into "needs" and "wants" categories. For older elementary students (ages 8–10), introduce a scenario-based activity: "If you have $10 and need a notebook for school, would you buy a $5 notebook or a $10 toy?" This encourages critical thinking and prioritization.

Caution: Avoid Moralizing Wants

While teaching the difference, avoid labeling wants as "bad" or "selfish." Instead, emphasize balance. Explain that while it’s okay to spend on wants occasionally, needs should always come first. For instance, say, "If you save part of your allowance, you can buy that toy *after* ensuring you have enough for lunch money."

Takeaway: Practical Application for Real-Life Budgeting

Encourage students to apply this concept to their own spending. Suggest they keep a mini-journal for a week, listing items they want to buy and categorizing them as needs or wants. For parents and teachers, reinforce this at home by discussing family budgets and involving kids in small financial decisions, like choosing between generic and branded cereal. By age 10, most children can understand the value of money and the importance of prioritizing needs, setting them up for smarter financial choices in the future.

Empowering Students: Effective Strategies for Teachers to Foster Success

You may want to see also

Explore related products

![]()

Tracking Progress: Introduce simple charts or journals to help students monitor their saving and spending habits

Elementary students thrive on visual feedback, making charts and journals ideal tools for tracking budgeting progress. A simple bar graph, for instance, can transform abstract numbers into a tangible representation of their savings growth. Each week, have students color in a bar corresponding to their current savings, creating a visual narrative of their financial journey. This not only reinforces their efforts but also fosters a sense of accomplishment as they see their bars climb higher.

For younger students (ages 6-8), start with a basic sticker chart. Every time they save a predetermined amount (e.g., $1), they earn a sticker. This tactile approach keeps them engaged and provides immediate gratification for their financial discipline. As they progress, introduce more complex charts like thermometers or pie charts to illustrate both savings and spending categories, gradually building their understanding of financial allocation.

While charts offer a visual snapshot, journals provide a deeper dive into spending habits. Encourage students to record each purchase, no matter how small, in a dedicated notebook. This practice promotes mindfulness and accountability, allowing them to identify patterns and make informed decisions. For example, a student might notice a recurring expense on snacks and decide to pack lunch instead, demonstrating the power of self-reflection in budgeting.

Combining charts and journals creates a comprehensive tracking system. Students can use their journals to record transactions and then transfer the data to their charts weekly. This dual approach not only reinforces learning but also caters to different learning styles. Visual learners benefit from the charts, while kinesthetic learners engage with the hands-on journaling process.

To maximize effectiveness, make tracking a collaborative effort. Display class charts on a bulletin board, fostering a sense of community and friendly competition. Organize periodic "budget check-ins" where students share their journal entries and discuss their progress. This peer-to-peer learning not only motivates students but also exposes them to diverse budgeting strategies, enriching their financial education. By integrating simple charts and journals, educators can empower elementary students to take ownership of their financial habits, setting them on a path toward lifelong financial literacy.

Empowering Student Leaders: Mastering the Art of Teaching a Class

You may want to see also

Frequently asked questions

Use hands-on activities like pretend play with toy money, create simple budgets for classroom projects, or use visual tools like charts and jars to represent income, savings, and spending.

Connect budgeting to their everyday lives by using examples like saving allowance for a toy or deciding how to spend birthday money. Relate it to their goals and interests to keep it engaging.

Use games like "The Game of Life" or apps like "PiggyBot," create worksheets with simple budgeting scenarios, or read books like *"A Smart Girl's Guide: Money"* to make learning fun and accessible.

Use sorting activities where students categorize items as needs (e.g., food, shelter) or wants (e.g., toys, candy). Discuss real-life examples to help them understand the importance of prioritizing needs.