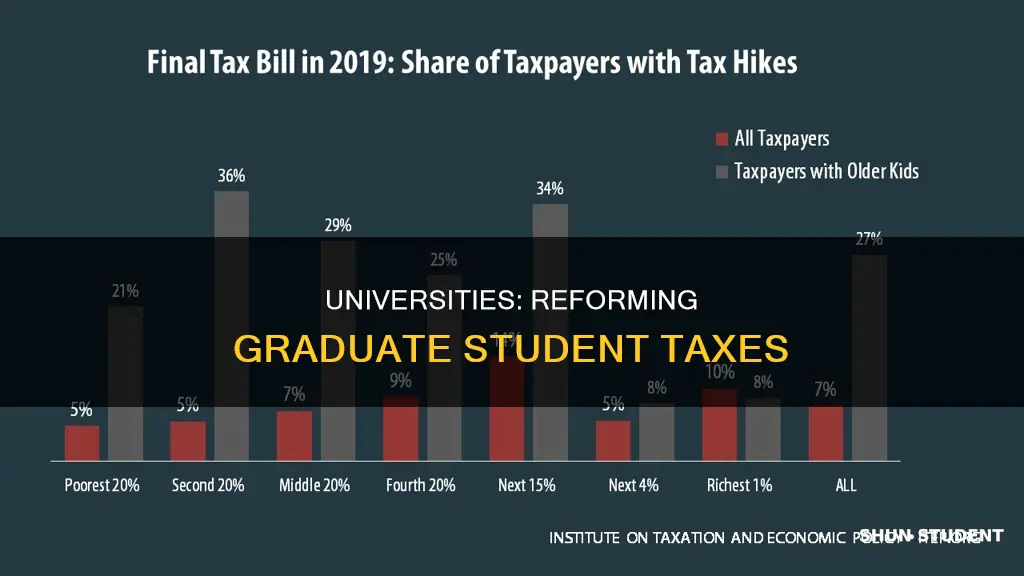

The University of California's graduate students and leaders are pushing back against tax reforms that could increase their taxes by more than 30%, with some liabilities soaring by 400%. The House bill treats tuition fee reductions as taxable income, pushing students into higher tax brackets. This could affect the financial stability of higher education institutions, threatening their accessibility and affordability. The Republican Tax Plan targets woke elite universities, imposing taxes on investment returns, which could cost universities billions. The Tax Cuts and Jobs Act proposes to repeal student loan interest reductions and graduate student tuition waivers, impacting students from middle-to-low-income families and deterring diversity in higher education. These tax reforms have sparked protests and walkouts, with graduate students lobbying Congress to prevent a detrimental impact on their financial stability and America's competitiveness.

| Characteristics | Values |

|---|---|

| Graduate students' tax bill | Could soar by thousands of dollars |

| Tuition reductions | Treated as taxable income |

| Impact on students | Forced out of school or deterred from enrolling |

| Impact on universities | Threatens overall affordability and accessibility of higher education |

| Impact on research and higher education | Affects graduate students who are key contributors to research and teaching |

| Tax liability | Could increase by more than 30% for many graduate students |

| Tax liability in certain cases | Could soar by 400% |

| Tax on university endowments | Target "woke" schools |

| Tax plan by Republicans | Could hurt at least 58 colleges |

| Universities affected by Republican tax plan | Harvard, Yale, Princeton, and smaller colleges like McPherson College |

| Tax rate for universities with endowments of at least $2 million per student | 21% |

| Loss for Harvard, Yale, and Princeton due to the tax | Estimated at $850 million, $690 million, and $586 million per year, respectively |

| Loss for Pomona College due to the tax | $40 million per year |

| Loss of scholarships at Pomona College due to the tax | 460 full scholarships |

Explore related products

What You'll Learn

![]()

The impact of repealing critical higher education tax benefits

Firstly, the financial burden on graduate students would increase substantially. Currently, graduate students benefit from tax provisions such as the qualified tuition reduction, which covers the cost of their education in exchange for their work as research or teaching assistants. If this tax benefit is repealed, students would be required to pay taxes on their tuition benefit, resulting in a significant increase in their tax liability. In some cases, their tax bill could soar by thousands of dollars, pushing them into higher tax brackets typically associated with wealthier households. This could force students to abandon their graduate studies or deter them from enrolling in the first place, particularly those from lower socioeconomic backgrounds.

Secondly, the repeal of higher education tax benefits could have a detrimental effect on scientific research and innovation. According to the American Council on Education, 57% of graduate students pursuing degrees in science, technology, engineering, and mathematics (STEM) benefit from the tuition reduction tax provision. By repealing this provision, universities may struggle to attract and retain graduate students in these critical fields, hindering scientific advancements and limiting opportunities for discovery and innovation.

Moreover, the financial implications of repealing these tax benefits extend beyond individual students. University leaders argue that such reforms could threaten the financial stability of higher education institutions by impacting charitable giving, tax-exempt bond financing, and unrelated business income taxation. This could ultimately affect the affordability and accessibility of higher education, limiting universities' ability to drive innovation and economic growth.

Additionally, the proposed tax reforms do not exist in isolation. They are part of a broader context of tax changes, including the removal of the Affordable Care Act mandate and the elimination of the student loan interest deduction. These cumulative changes could further exacerbate the financial strain on graduate students, making it increasingly challenging for them to pursue their academic and research aspirations.

Overall, the impact of repealing critical higher education tax benefits could be far-reaching, with potential consequences for both individual graduate students and the broader higher education landscape. While the specific outcomes are difficult to predict, it is clear that such changes would significantly reshape the financial dynamics of graduate education and research.

Vermont's University Student Population: A Comprehensive Overview

You may want to see also

Explore related products

![]()

The financial stability of higher education institutions

The House bill proposes to treat tuition reductions as taxable income, which could push graduate students into higher tax brackets. This change could not only affect graduate students but also the broader research and higher education landscape, as graduate students are integral to universities' research and teaching endeavours. Furthermore, the bill's impact on charitable giving, tax-exempt bond financing, and unrelated business income taxation could further threaten the financial stability of higher education institutions.

The University of California is not alone in its concerns. The Republican Tax Plan, also known as the "Tax Cut and Jobs Act," has been criticized for potentially harming at least 58 colleges. This plan includes a hefty tax on university endowments, which could cost some universities millions of dollars annually. The goal of this proposal is to target "woke, elite universities" that are believed to operate more like corporations. However, smaller colleges with substantial endowments may also be affected, such as McPherson College in Kansas.

The potential impact of these tax changes on the financial stability of higher education institutions is significant. Universities may need to re-evaluate their tuition waiver policies and consider increasing stipends to help graduate students cover the additional tax costs. However, this would place a greater financial burden on graduate programs and advisors. The tax reforms could ultimately make graduate school unaffordable for many students, especially those from middle-to-low-income families, and deter diversity in higher education.

While the specific details of the tax code changes may evolve, universities are left questioning the permanence of these alterations. Institutions are faced with the challenge of determining whether to make immediate structural adjustments or to await potential reversals by future Congresses. This uncertainty adds a layer of complexity to the financial decision-making process within higher education.

Who Can Access University Libraries?

You may want to see also

Explore related products

![]()

The impact on graduate students' monthly take-home pay

The impact of university tax changes on graduate students' monthly take-home pay could be significant. The proposed tax reform bills, such as the Tax Cuts and Jobs Act, aim to increase taxes for graduate students by treating tuition reductions as taxable income. This could result in a substantial increase in tax liability for many students, with some facing up to a 400% surge in their tax bills.

For example, a graduate student at Columbia University with a stipend of $38,000 and a tuition waiver of $51,000 currently pays $3,726 in taxes. Under the House's proposed legislation, their taxes could rise to $13,413, reducing their monthly take-home pay for essential expenses like food, rent, and health costs. Their monthly take-home pay would decrease from $2,885 to $2,078, a significant reduction that could impact their standard of living and ability to continue their studies.

The mix of funding graduate students receive will also play a role in the impact on their take-home pay. Those with fellowships and scholarships may be shielded from the full impact of the tax changes, as these are often tax-exempt. However, those relying solely on stipends and tuition waivers will likely see a more substantial reduction in their monthly income.

Additionally, the proposed tax changes could disproportionately affect graduate students from middle-to-low-income families, as they may not have family support to offset the increased tax burden. This could deter diversity in higher education and hinder the brightest minds from pursuing graduate studies, particularly in STEM fields, impacting America's competitiveness in science and technology.

The overall impact on graduate students' monthly take-home pay will depend on the final version of the tax laws passed and the specific financial circumstances of each student. Universities and students are closely monitoring the situation, with some universities considering ways to mitigate the potential financial burden on their graduate students.

Exploring University of West Florida's Student Population

You may want to see also

Explore related products

![]()

The impact on graduate students from middle-to-low income families

The Tax Cuts and Jobs Act, which includes a provision that would require graduate students to pay taxes on tuition benefits, has been criticised for its potential negative impact on graduate students from middle-to-low income families. This provision would effectively increase the tax liability for many graduate students, with some facing increases of up to 400%.

Currently, graduate students may receive funding packages that cover the cost of their graduate education, including tuition waivers, stipends, scholarships, and fellowships. However, under the proposed tax reform, the value of tuition waivers would be treated as taxable income. This change would significantly increase the tax burden for graduate students, especially those from middle-to-low income families who may not have the financial support of their families to offset these additional costs.

The impact of this tax reform on graduate students from middle-to-low income families could be significant. Firstly, it may deter students from pursuing graduate studies due to the increased financial burden. Graduate school may no longer be financially feasible for many, as the additional tax liability could exceed the modest stipends they receive. This could result in a decrease in diversity in higher education, as students from poorer backgrounds, who are often minorities, may be disproportionately affected.

Secondly, for those who do decide to enrol in graduate school, the increased tax burden may leave them with less disposable income for essential living expenses such as food, rent, and health care. This could impact their overall well-being and quality of life during their studies. Additionally, the tax reform may also eliminate certain tax benefits, such as the student loan interest deduction and the Lifetime Learning Credit, which could further increase the financial strain on graduate students from middle-to-low income families.

Furthermore, the proposed tax reform may have broader implications for higher education and research. Graduate students play a crucial role in the research and teaching enterprise of universities. A decrease in the number of graduate students due to the tax changes could negatively impact the overall research output and innovation capacity of universities. This, in turn, could have a detrimental effect on America's international competitiveness in science and technology fields.

While the intention behind the tax reform may be to target "woke, elite universities", the impact on graduate students from middle-to-low income families cannot be overlooked. It is important for policymakers to carefully consider the potential consequences of this tax reform and explore alternative solutions that do not disproportionately affect students from these socioeconomic backgrounds.

UCF Knights: Universal Studios Discounts for Students

You may want to see also

Explore related products

![]()

The impact on the financial feasibility of graduate school

The impact of proposed tax reforms on the financial feasibility of graduate school is a complex issue that has sparked concerns among students, universities, and higher education leaders. The House bill's proposal to treat tuition reductions as taxable income has been a significant point of contention, with potential consequences for both students and the broader higher education landscape.

For graduate students, the financial implications of these tax changes could be significant. Currently, many graduate students receive "qualified tuition reductions," where their graduate education costs are covered while they work for the university as research or teaching assistants. Under the House bill, these tuition waivers would become taxable, resulting in a substantial increase in tax liability for students. In some cases, students could see their tax bills soar by thousands of dollars, pushing them into higher tax brackets typically associated with wealthier households. This sudden increase in tax obligations could force students to abandon their graduate studies or deter them from enrolling in the first place.

The financial feasibility of graduate school is further impacted by the mix of funding sources and the sticker price of tuition. Students who rely on fellowships, scholarships, or stipends may find themselves in a precarious situation as their income becomes subject to higher taxes. Those attending costly private schools or paying out-of-state tuition are also likely to be disproportionately affected by the proposed tax changes. Additionally, the elimination of the student loan interest deduction and the repeal of the Lifetime Learning Credit in the House's tax plan further burden graduate students with increased costs and reduced financial assistance.

The financial implications of the proposed tax reforms extend beyond individual students and impact the broader higher education landscape. University leaders argue that the reforms could threaten the overall affordability and accessibility of higher education. This, in turn, could hinder universities' ability to serve as engines of innovation and economic growth. Additionally, the potential loss of critical tax benefits, changes to charitable giving, tax-exempt bond financing, and unrelated business income taxation are causes for concern among universities, as they play crucial roles in their ability to carry out education, research, healthcare, and public service missions.

While the specific consequences of the tax changes on the financial feasibility of graduate school are difficult to predict, it is clear that the impact could be significant. Students, universities, and higher education advocates have voiced their worries through protests, lobbying efforts, and social media campaigns. The outcome of these proposed tax reforms will undoubtedly shape the financial landscape of graduate education and influence the decisions of prospective graduate students in the coming years.

Student Health Insurance Expiry: Boston University Guide

You may want to see also

Frequently asked questions

Universities cannot change taxes, but they can influence legislation through lobbying. Universities have dispatched lobbyists to Capitol Hill to try to water down the impact of tax plans.

The Tax Cuts and Jobs Act could disproportionately and negatively impact graduate students by treating tuition waivers as taxable income. This could increase graduate student taxes three-fold.

Universities could change the status of tuition to scholarships, which are not taxed. Alternatively, universities could increase stipends to cover tax costs.

The Act could deter diversity in higher education by burdening graduate students from poor and middle-class backgrounds with a giant tax hike.

Universities' endowments could be taxed depending on the size of the endowment and enrollment, with a top rate of 21% for universities with endowments of at least $2 million per student.