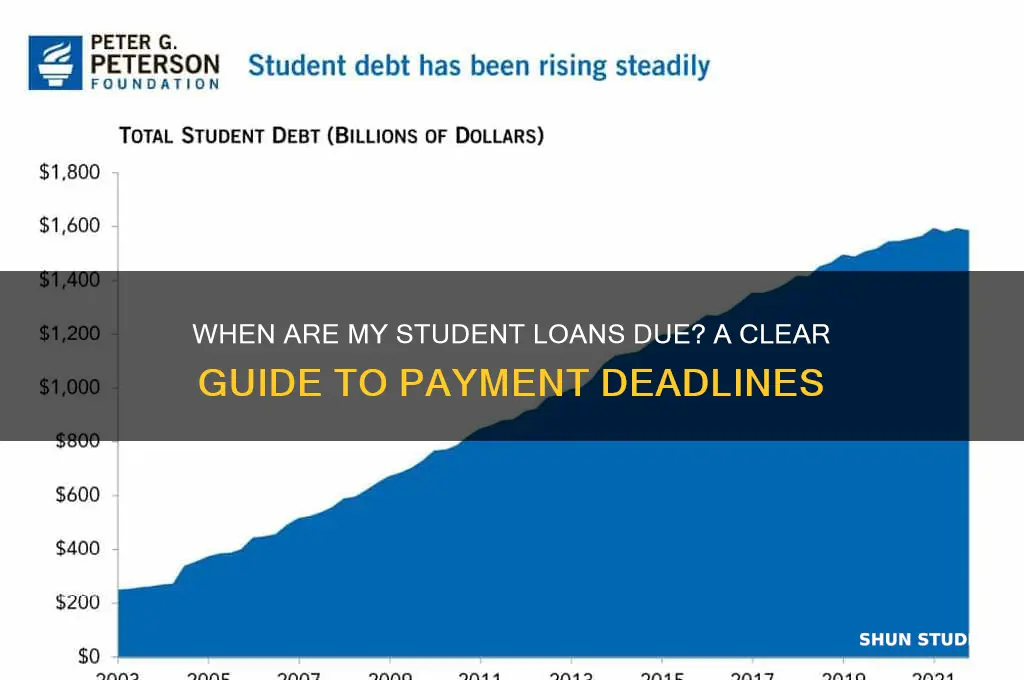

Understanding when your student loan payments are due is crucial for maintaining financial health and avoiding penalties. Typically, student loan repayment begins six months after you graduate, leave school, or drop below half-time enrollment, a period known as the grace period. Once this grace period ends, your first payment will be due, and you’ll receive a billing statement or notice from your loan servicer outlining the due date, payment amount, and payment options. It’s essential to review your loan agreement or contact your loan servicer to confirm the exact due date, as it can vary depending on the type of loan and lender. Setting up automatic payments or creating a repayment plan can help ensure you never miss a due date and stay on track with your financial obligations.

Explore related products

What You'll Learn

- Understanding Loan Terms: Review your loan agreement for repayment start date and grace period details

- Grace Period End: Most loans require payments 6 months after graduation or leaving school

- Loan Servicer Notices: Check emails or mail from your servicer for due date notifications

- Online Account Access: Log into your loan account to view payment schedules and deadlines

- First Payment Date: Mark your calendar for the exact date your first payment is due

![]()

Understanding Loan Terms: Review your loan agreement for repayment start date and grace period details

Your student loan agreement is a legally binding contract that outlines the terms of your repayment. Buried within its pages are two critical dates: your repayment start date and the end of your grace period. These dates dictate when your first payment is due and when interest begins to accrue, making them essential to understand. Ignoring them can lead to late fees, damage to your credit score, and even loan default.

Think of your loan agreement as a roadmap for repayment. It details the loan amount, interest rate, repayment plan options, and those crucial dates. Don't let it gather dust in a drawer – carefully review it to avoid unpleasant surprises.

Locating these dates requires a bit of detective work. Look for sections titled "Repayment Terms," "Grace Period," or "Deferment." The repayment start date is typically 6 months after you graduate, leave school, or drop below half-time enrollment. This grace period allows you to get financially settled before payments begin. However, interest may still accrue during this time, depending on your loan type. For example, subsidized federal loans generally don't accrue interest during the grace period, while unsubsidized loans do.

Understanding these nuances is crucial for budgeting and planning.

Don't rely on your lender to remind you when payments are due. Mark your calendar, set up automatic payments, and consider enrolling in your lender's online portal for easy access to account information. If you're unsure about any aspect of your loan terms, contact your loan servicer immediately. They are there to help you navigate the repayment process and avoid costly mistakes. Remember, knowledge is power – understanding your loan agreement empowers you to manage your student debt responsibly.

Does Canada Forgive Student Loans? Exploring Government Repayment Assistance

You may want to see also

Explore related products

![]()

Grace Period End: Most loans require payments 6 months after graduation or leaving school

One of the most critical milestones in your student loan journey is the end of the grace period. This six-month window after graduation or leaving school is a built-in buffer, designed to give you time to find employment and stabilize financially before payments begin. However, many borrowers underestimate the importance of tracking this deadline, leading to missed payments and unnecessary penalties. To avoid this, mark your calendar six months from your graduation date or the day you drop below half-time enrollment—whichever comes first. Federal loans, such as Direct Subsidized and Unsubsidized Loans, typically offer this grace period, but private loans may have different terms, so review your loan agreement carefully.

Understanding how the grace period works can save you from financial stress. During this time, interest on subsidized federal loans is paid by the government, but unsubsidized loans and most private loans continue to accrue interest. This means your balance grows even if you’re not making payments. For example, if you have a $30,000 unsubsidized loan at a 5% interest rate, approximately $125 in interest will accrue each month during the grace period. To minimize long-term costs, consider making interest payments during this time if your budget allows. This prevents capitalization, where unpaid interest is added to the principal balance, increasing the total amount you’ll repay.

Not all loans provide a grace period, and assuming yours does without verifying could be a costly mistake. For instance, PLUS Loans for graduate students or parents do not include a grace period, and payments are due as soon as the loan is fully disbursed. Similarly, some private lenders may offer a grace period, but it’s often shorter or non-existent. Always check your loan terms or contact your loan servicer to confirm your repayment start date. If you’re unsure, log into your student loan account or use the National Student Loan Data System (NSLDS) to access details about your federal loans.

Proactive planning is key to a smooth transition into repayment. Start by creating a budget that accounts for your estimated monthly loan payment. If you’re struggling to find employment, consider enrolling in an income-driven repayment plan or requesting a forbearance to temporarily pause payments. However, these options should be used sparingly, as they can increase the total cost of your loan. Additionally, set up automatic payments to ensure you never miss a due date. Most servicers offer a small interest rate reduction (typically 0.25%) for enrolling in autopay, which can save you money over the life of the loan.

In summary, the end of the grace period is a pivotal moment in managing your student loans. By knowing your exact repayment start date, understanding how interest accrues, and verifying your loan terms, you can avoid common pitfalls. Use this six-month window wisely—whether by making interest payments, budgeting for future installments, or exploring repayment options. Staying informed and prepared ensures you take control of your financial future from day one.

Top Student Loan Forgiveness Programs: Which One Fits You Best?

You may want to see also

Explore related products

![]()

Loan Servicer Notices: Check emails or mail from your servicer for due date notifications

Your loan servicer is your primary source of information regarding student loan repayment, including due dates. They are obligated to send you regular notices, typically via email or physical mail, outlining key details such as payment amounts, due dates, and any changes to your loan terms. These communications are not just formalities; they are essential tools to keep you informed and on track with your repayment schedule. Ignoring or overlooking these notices can lead to missed payments, late fees, and potential damage to your credit score.

To effectively utilize these notices, start by ensuring your contact information is up-to-date with your loan servicer. Log into your account on their website or call their customer service line to verify your email address and mailing address. If you’ve recently moved or changed email providers, updating this information is crucial. Once confirmed, make it a habit to check your email inbox and physical mailbox regularly, especially around the time your payments are due. Many servicers send reminders a week or two before the due date, giving you ample time to prepare.

Analyzing the content of these notices is equally important. Pay close attention to the payment due date, the minimum amount required, and any additional fees or interest accrued. Some servicers also include information about autopay options, which can help you avoid late payments by automatically deducting the amount from your bank account. If you notice discrepancies or have questions about the details provided, don’t hesitate to contact your servicer directly. Clarifying any confusion early can prevent costly mistakes down the line.

For those who prefer digital communication, consider opting into email notifications if your servicer offers them. These emails often include direct links to your account, making it easy to log in and make payments. However, if you rely solely on email, be cautious of phishing attempts. Always verify that the email is from your official loan servicer by checking the sender’s address and looking for secure website links (starting with "https"). If in doubt, log into your account independently rather than clicking on links in suspicious emails.

Lastly, keep a record of these notices for your financial records. Save emails in a dedicated folder or file physical mail in a safe place. This documentation can be invaluable if there’s ever a dispute about payment dates or amounts. By staying vigilant and proactive with loan servicer notices, you’ll not only stay informed about your due dates but also develop a disciplined approach to managing your student loan repayment.

When Will Student Loan Payments Resume? Key Dates and Updates

You may want to see also

Explore related products

![Due Date [Blu-ray]](https://m.media-amazon.com/images/I/91ri7sb6sWL._AC_UY218_.jpg)

![Due Date [DVD] [2010]](https://m.media-amazon.com/images/I/71aDP+fh07L._AC_UY218_.jpg)

![]()

Online Account Access: Log into your loan account to view payment schedules and deadlines

One of the most direct ways to determine when your student loan payments are due is by accessing your loan account online. Nearly all loan servicers provide digital platforms where borrowers can view detailed information about their loans, including payment schedules, deadlines, and outstanding balances. This method is not only convenient but also ensures you have the most up-to-date information directly from the source. Logging in regularly can help you avoid missed payments and stay informed about any changes to your repayment terms.

To begin, locate the website of your loan servicer—this is the company that handles the billing and other services for your loan. Common servicers include Navient, FedLoan Servicing, and Great Lakes. If you’re unsure who your servicer is, check your most recent loan statement or visit the National Student Loan Data System (NSLDS) for federal loans. Once on the servicer’s website, create an account if you haven’t already. You’ll typically need your Social Security number, date of birth, and other identifying information. After logging in, navigate to the dashboard or account summary section, where payment schedules are usually prominently displayed.

While online account access is straightforward, it’s important to understand the nuances of what you’re viewing. Payment schedules often include due dates, minimum payment amounts, and any upcoming deadlines for actions like recertifying income-driven repayment plans. Pay attention to the grace period—usually six months after graduation for federal loans—as payments typically begin after this period ends. If you’re enrolled in auto-pay, ensure the due date aligns with your bank’s processing times to avoid late fees. For private loans, terms can vary widely, so scrutinize the details carefully.

A practical tip is to set calendar reminders based on the information you find in your online account. For example, if your payment is due on the 15th of each month, set a recurring reminder for the 10th to ensure you have time to address any issues. Additionally, consider downloading the servicer’s mobile app if available, as these often provide push notifications for upcoming payments. If you notice discrepancies or have questions about your schedule, contact your servicer immediately—most offer chat, phone, and email support.

In conclusion, online account access is a powerful tool for managing student loan payments. It provides clarity, control, and the ability to plan ahead. By familiarizing yourself with your loan servicer’s platform and regularly checking your payment schedule, you can stay on top of your financial obligations and avoid unnecessary penalties. Treat your online account as the primary resource for accurate, real-time information about your student loans.

When Will My Student Loans Be Updated: A Borrower's Guide

You may want to see also

Explore related products

$12.95 $22.99

![]()

First Payment Date: Mark your calendar for the exact date your first payment is due

Your first student loan payment is a milestone, and missing it can have serious consequences. It’s not just about avoiding late fees—it’s about protecting your credit score and staying in good standing with your loan servicer. The exact date this payment is due is called your *first payment date*, and it’s critical to know it well in advance. This date isn’t always immediately after graduation; it depends on your loan type and grace period. For federal loans, the grace period is typically six months after leaving school, but private loans vary widely—some require payment while you’re still in school. Ignoring this detail could lead to unnecessary stress and financial penalties.

To find your first payment date, start by reviewing your loan documents or logging into your loan servicer’s portal. Federal loan borrowers can visit StudentAid.gov to access their loan information, including repayment start dates. Private loan borrowers should check their lender’s website or contact customer service directly. Once you’ve identified the date, mark it boldly on your calendar—both physically and digitally. Set reminders a week and a day before to ensure it doesn’t slip your mind. If you’re unsure or can’t locate the information, reach out to your loan servicer immediately; procrastination could cost you.

Knowing your first payment date is only half the battle—preparing for it is equally important. Calculate your monthly budget to ensure you can afford the payment without strain. If the amount feels overwhelming, explore repayment plans like income-driven options or deferment/forbearance if you qualify. For example, if your standard monthly payment is $300 but your income is tight, switching to an income-driven plan might reduce it to $150. Additionally, consider setting up automatic payments; many servicers offer a small interest rate reduction (typically 0.25%) for enrolling in autopay, saving you money in the long run.

Finally, treat your first payment date as a financial wake-up call. It’s the moment your student loans transition from a future concern to a present responsibility. Use this opportunity to educate yourself about loan management tools, such as loan forgiveness programs or refinancing options. For instance, if you work in public service, you might qualify for Public Service Loan Forgiveness after 120 qualifying payments. By staying proactive and informed, you’ll not only meet your first payment deadline but also set yourself up for long-term financial success.

College Students' Patience: How Long Will They Wait in Line?

You may want to see also

Frequently asked questions

You will receive a loan repayment schedule from your loan servicer after your grace period ends, detailing your due dates, payment amounts, and other important information.

It’s your responsibility to make payments on time, even if you don’t receive a notice. Log into your loan servicer’s website or contact them directly to confirm your due date.

Yes, most federal student loans offer a 6-month grace period after graduation, leaving school, or dropping below half-time enrollment before payments are due. Private loans may have different terms.

Yes, many loan servicers allow you to request a due date change. Contact your servicer to discuss your options and eligibility.

Reach out to your loan servicer immediately to explore options like income-driven repayment plans, deferment, forbearance, or refinancing to avoid default.