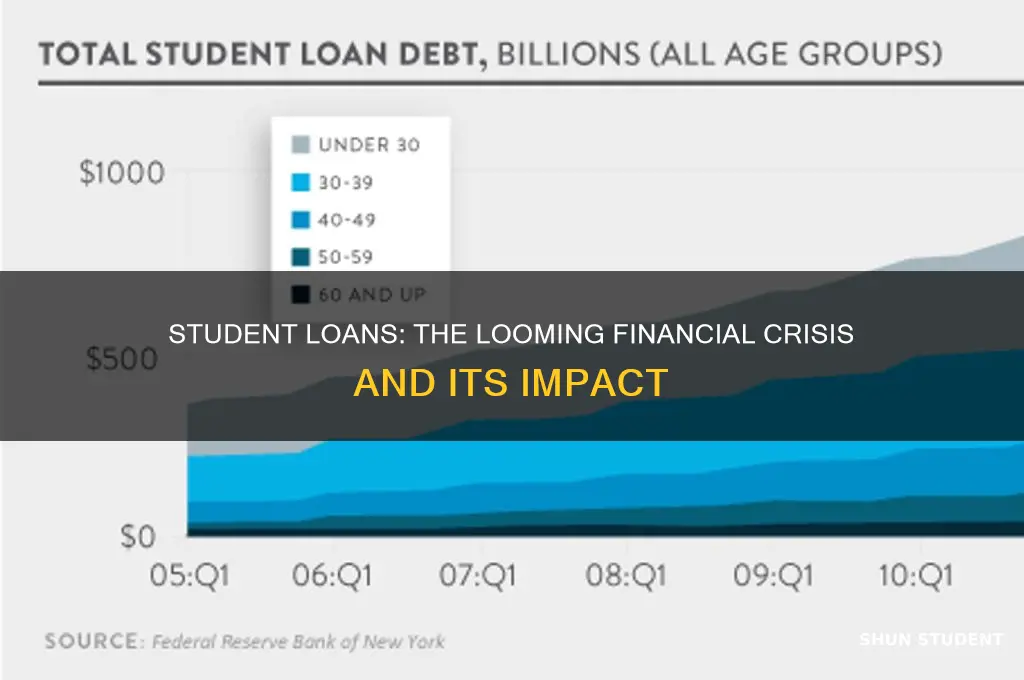

Student loans have become a ticking time bomb in the global economy, with the potential to trigger a widespread financial crisis. As the cost of higher education continues to soar, millions of students are forced to take on massive debt to finance their studies, often with little understanding of the long-term consequences. The current student loan debt in the United States alone exceeds $1.7 trillion, surpassing credit card and auto loan debt, and putting immense strain on individual borrowers, the education system, and the overall economy. With high interest rates, inflexible repayment plans, and limited options for discharge, many borrowers find themselves trapped in a cycle of debt, unable to make payments, and facing default, which can have devastating effects on their credit scores, job prospects, and overall financial stability, ultimately threatening to destabilize the entire financial system.

| Characteristics | Values |

|---|---|

| Total U.S. Student Loan Debt (2023) | $1.77 trillion (Federal Reserve, Q3 2023) |

| Average Student Loan Debt per Borrower | $37,787 (Education Data Initiative, 2023) |

| Delinquency Rate (90+ days overdue) | 7.3% (Federal Reserve, 2023) |

| Percentage of Borrowers in Default | 10.8% (U.S. Department of Education, 2023) |

| Impact on Homeownership | 35% of student loan borrowers delay homeownership (National Association of Realtors, 2023) |

| Effect on Consumer Spending | Reduces annual spending by $1,000 per borrower (JPMorgan Chase Institute, 2023) |

| Contribution to Inflation | Student loan payments resuming in 2023 added ~0.3% to inflation (Moody’s Analytics, 2023) |

| Risk of Systemic Financial Contagion | Limited direct risk, but indirect effects on consumer credit and spending (Federal Reserve, 2023) |

| Government Loan Forgiveness Programs | $144 billion in debt forgiven (U.S. Department of Education, 2023) |

| Economic Growth Impact | Reduces GDP growth by 0.1-0.2% annually (Brookings Institution, 2023) |

| Psychological and Social Costs | 60% of borrowers report mental health issues due to debt (American Psychological Association, 2023) |

| Income-Driven Repayment Enrollment | 40% of federal borrowers enrolled (U.S. Department of Education, 2023) |

| Private Student Loan Debt | $150 billion (MeasureOne, 2023) |

| Loan Payment Resumption Impact (2023) | $5 billion monthly reduction in disposable income (Goldman Sachs, 2023) |

Explore related products

$8.34 $19

What You'll Learn

![]()

Rising Default Rates

Student loan default rates are climbing, and this trend is a ticking time bomb for the economy. Data from the Federal Reserve shows that over 10% of student loan borrowers are in default, a figure that has been steadily rising over the past decade. This isn't just a personal finance issue; it's a systemic risk. When borrowers default, it triggers a cascade of negative consequences: damaged credit scores, wage garnishments, and a reduced ability to participate in the economy. For lenders, particularly the federal government, which holds the majority of student debt, defaults mean significant losses. These losses can strain government budgets, potentially leading to cuts in other essential services or increased taxes to compensate.

Consider the broader economic implications. A surge in defaults can depress consumer spending, as borrowers redirect their income toward debt repayment or face reduced purchasing power due to wage garnishments. This slowdown in spending can ripple through industries, from housing to retail, stifling growth and job creation. For instance, a young professional burdened with unmanageable student debt may delay buying a home, getting married, or starting a family—all of which are critical drivers of economic activity. Multiply this scenario by millions, and you have a recipe for stagnation.

To mitigate this risk, policymakers must act decisively. One practical step is to expand income-driven repayment plans, which cap monthly payments at a percentage of the borrower’s income. For example, the Revised Pay As You Earn (REPAYE) plan limits payments to 10% of discretionary income and forgives remaining balances after 20–25 years of consistent payments. Increasing awareness of such programs and simplifying the application process could prevent defaults before they occur. Additionally, institutions should invest in financial literacy programs targeting students aged 18–24, the demographic most likely to underestimate the long-term impact of their borrowing decisions.

However, caution is warranted. While forgiveness programs can provide relief, they must be designed to avoid moral hazard—the risk that borrowers will take on excessive debt expecting it to be forgiven. Striking this balance requires targeted solutions, such as means-tested forgiveness for low-income borrowers or those in public service roles. Without careful implementation, blanket forgiveness could exacerbate the problem by encouraging reckless borrowing in the future.

In conclusion, rising default rates are not just a symptom of the student loan crisis but a catalyst for broader financial instability. Addressing this issue demands a multi-faceted approach: proactive repayment assistance, early financial education, and targeted relief measures. Failure to act could turn a manageable problem into a full-blown economic crisis, undermining the very promise of education as a pathway to prosperity.

Pell Grants and Student Loan Forgiveness: What You Need to Know

You may want to see also

Explore related products

![]()

Stifled Consumer Spending

The weight of student loan debt doesn't just crush individual dreams; it chokes the life out of consumer spending, a vital engine of economic growth. Consider this: the average student loan payment for borrowers aged 25-34 is roughly $393 per month, according to the Federal Reserve. That's money not being spent on cars, houses, or even dinners out. It's a silent tax on young adulthood, siphoning funds away from the very activities that stimulate economic activity.

Imagine a young professional, Sarah, burdened by $40,000 in student loans. Her monthly payment, around $400, could easily translate into a down payment on a used car, a weekend getaway, or a significant contribution to a retirement account. Instead, it disappears into the black hole of debt repayment, leaving Sarah with limited disposable income and a diminished capacity to participate in the consumer economy.

This isn't just Sarah's story; it's a national trend. A 2022 study by the Roosevelt Institute found that student debt reduces annual consumption by $86 billion. This translates to fewer purchases at local businesses, less investment in housing, and a dampening effect on overall economic growth. The ripple effect is profound: businesses suffer from reduced demand, potentially leading to layoffs and further economic contraction.

Think of it as a vicious cycle. Student debt stifles spending, which weakens businesses, leading to job losses and potentially pushing more individuals into debt. Breaking this cycle requires addressing the root cause: the skyrocketing cost of higher education and the unsustainable burden of student loans.

Policymakers must consider solutions like debt forgiveness programs, income-driven repayment plans, and increased investment in affordable public education. By alleviating the student debt burden, we can unleash the spending power of millions, fueling economic growth and creating a more prosperous future for all. The alternative is a stagnant economy, burdened by a generation saddled with debt and unable to fully participate in the consumer marketplace.

Parent PLUS Loan Forgiveness: What Borrowers Need to Know

You may want to see also

Explore related products

![]()

Housing Market Slowdown

The housing market, a cornerstone of economic stability, is increasingly vulnerable to the ripple effects of the student loan crisis. As graduates enter the workforce burdened by substantial debt, their ability to save for down payments diminishes significantly. For instance, the average student loan debt in the U.S. exceeds $30,000, with many borrowers facing monthly payments that rival rent costs. This financial strain delays homeownership, particularly among millennials and Gen Z, who traditionally drive first-time homebuyer activity. Without this demographic’s participation, the housing market loses momentum, leading to slower sales and stagnant prices.

Consider the lifecycle of a potential homebuyer. A 25-year-old with $40,000 in student loans at a 6% interest rate faces monthly payments of approximately $400. Over a decade, this totals nearly $50,000, money that could have been saved for a 20% down payment on a median-priced home. Instead, these funds service debt, leaving borrowers renting longer than previous generations. This delay creates a bottleneck in the housing market, as existing homeowners, unable to sell to first-time buyers, postpone upgrades or downsizing. The result? A slowdown in transactions that ripples through construction, real estate, and related industries.

To mitigate this, policymakers and lenders must address the root cause: student debt. One practical solution is expanding income-driven repayment plans that cap monthly payments at 10% of discretionary income. For a borrower earning $50,000 annually, this could reduce payments to $200–$250 per month, freeing up $150–$200 for savings. Additionally, incentivizing employers to offer student loan repayment assistance as a benefit could accelerate debt payoff timelines. For example, a $100 monthly employer contribution could shorten a 10-year repayment plan by 2–3 years, enabling faster homeownership.

However, caution is warranted. Lowering lending standards to accommodate debt-burdened buyers risks repeating the 2008 subprime mortgage crisis. Instead, focus on systemic solutions like public service loan forgiveness expansions or debt forgiveness for specific sectors. Pairing these with financial literacy programs can empower borrowers to navigate both debt and homeownership responsibly. Without such interventions, the housing market slowdown will persist, exacerbating economic inequality and stifling growth. The takeaway? Student loans aren’t just a personal finance issue—they’re a housing market time bomb requiring proactive defusal.

California Student Loan Forgiveness: A Comprehensive Guide to Debt Relief

You may want to see also

Explore related products

![]()

Increased Government Debt Burden

The escalating volume of student loans is not just a personal financial issue for borrowers; it is a burgeoning liability for governments, particularly in countries with income-driven repayment plans or loan forgiveness programs. In the United States, for instance, federal student loan debt surpassed $1.7 trillion in 2023, making it the largest non-mortgage debt category. When borrowers struggle to repay these loans—often due to low wages, underemployment, or economic downturns—the government absorbs the shortfall, either through direct write-offs or subsidized repayment plans. This shifts the debt burden from individuals to the public sector, exacerbating national debt levels. For context, the U.S. federal debt-to-GDP ratio has already exceeded 120%, and student loan defaults contribute measurably to this figure.

Consider the mechanics of income-driven repayment plans, which cap monthly payments at a percentage of discretionary income and forgive remaining balances after 20–25 years. While these programs provide relief to borrowers, they effectively transfer long-term financial risk to the government. A 2021 Congressional Budget Office report estimated that the federal government loses approximately 20 cents on every dollar lent through such programs. Multiply this by millions of borrowers, and the fiscal impact becomes staggering. In the UK, the situation is similar, with the Institute for Fiscal Studies projecting that over 80% of student loans will never be fully repaid, costing taxpayers billions annually.

The compounding effect of this debt burden is twofold. First, it reduces government revenue available for critical public services, such as healthcare, infrastructure, and education. Second, it increases borrowing costs as credit rating agencies downgrade sovereign debt ratings in response to rising liabilities. For example, if a government’s debt-to-GDP ratio surpasses 130%, investors may demand higher yields on bonds, further straining fiscal health. This vicious cycle can lead to austerity measures, tax increases, or inflationary monetary policies, all of which have broader economic repercussions.

To mitigate this crisis, policymakers must balance borrower relief with fiscal responsibility. One practical step is to reform loan eligibility criteria, tying borrowing limits to expected post-graduation earnings for specific programs. For instance, a student pursuing a degree in a high-earning field like engineering could access larger loans than one studying a field with lower average salaries. Additionally, governments could incentivize institutions to reduce tuition costs by linking federal funding to affordability metrics. Finally, public-private partnerships could be explored to create income share agreements, where graduates repay a percentage of their income for a fixed period, reducing the need for large upfront loans.

In conclusion, the increased government debt burden from student loans is a ticking time bomb that threatens fiscal stability. Without proactive reforms, the cost of inaction will be borne by taxpayers and future generations. By addressing the root causes of rising tuition costs and aligning loan programs with economic realities, governments can avert a financial crisis while ensuring access to higher education remains equitable. The challenge is urgent, and the solutions require both creativity and political will.

Standardized Testing Pressure: Unraveling the Stress on Students' Mental Health

You may want to see also

Explore related products

![]()

Reduced Economic Mobility

The burden of student loans isn't just a personal finance issue; it's a drag on the entire economy, stifling the very engine of economic growth: social mobility.

Imagine a young graduate, brimming with potential, forced to choose between pursuing their dream career in a low-paying field like teaching or social work, and a higher-paying job they dislike, simply to service their debt. This is the reality for countless borrowers, effectively trapping them in a cycle of financial servitude.

High student debt burdens delay major life milestones. Homeownership, a cornerstone of wealth building, becomes a distant dream when monthly loan payments rival rent. Starting a family, another driver of economic activity, is often postponed due to financial insecurity. This ripple effect extends beyond individual lives, dampening consumer spending and hindering economic growth.

Consider the long-term consequences. A 25-year-old with $30,000 in student debt at a 6% interest rate will pay over $10,000 in interest alone over a standard 10-year repayment period. That's $10,000 that could have been invested in a retirement account, a down payment on a house, or starting a business. Multiply this scenario by millions of borrowers, and you have a significant drain on potential economic activity.

The impact is particularly stark for borrowers from low-income backgrounds. For them, student loans represent a gamble with potentially devastating consequences. Defaulting on loans can ruin credit scores, limiting access to future credit and exacerbating financial vulnerability. This creates a vicious cycle, perpetuating inequality and hindering social mobility for generations to come.

Breaking this cycle requires a multi-pronged approach. Loan forgiveness programs, while controversial, can provide much-needed relief for borrowers drowning in debt. Income-driven repayment plans, which cap monthly payments based on earnings, offer a more sustainable path to repayment. Investing in affordable public education and promoting vocational training can reduce reliance on student loans altogether. By addressing the root causes of student debt, we can unlock the economic potential of millions, fostering a more vibrant and equitable economy for all.

Heroes Act Student Loan Forgiveness: A Step-by-Step Application Guide

You may want to see also

Frequently asked questions

Student loans could trigger a financial crisis if widespread defaults lead to significant losses for lenders, reducing their ability to lend and causing a credit crunch. Additionally, high debt levels can suppress consumer spending, slow economic growth, and destabilize financial markets.

Student loan debt reduces disposable income, limiting spending on housing, cars, and other goods. This can stifle economic growth and increase the risk of defaults, which could ripple through financial institutions and markets.

Yes, if defaults become widespread, they could strain lenders and servicers, potentially leading to a cascade of losses. The interconnectedness of financial institutions means this risk could spread, similar to the 2008 mortgage crisis.

Student loan forgiveness could reduce default rates and free up consumer spending, mitigating economic risks. However, if not implemented carefully, it could increase government debt or inflation, creating new financial pressures.

Warning signs include rising delinquency and default rates, increasing borrower distress, and a slowdown in consumer spending. Additionally, if lenders tighten credit standards or reduce lending, it could signal growing concerns about loan performance.