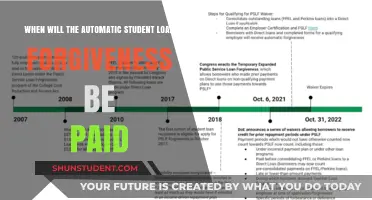

The topic of student debt forgiveness has been a subject of intense debate and anticipation, particularly in the United States, where millions of borrowers are burdened by staggering educational loans. With the recent announcement of a federal student debt relief plan, many are eager to understand how this initiative will work in practice. The program aims to provide financial relief by canceling a portion of borrowers' debt, with the amount forgiven depending on factors such as income and loan type. Eligible individuals may have up to $10,000 or $20,000 of their debt forgiven, offering a much-needed lifeline to those struggling with repayment. This paragraph sets the stage for a detailed exploration of the mechanics, eligibility criteria, and potential impact of the student debt forgiveness program, addressing the pressing concerns of borrowers nationwide.

Explore related products

What You'll Learn

- Eligibility Criteria: Who qualifies for debt forgiveness based on income, loan type, and employment status

- Application Process: Steps and documentation required to apply for student debt forgiveness

- Loan Types Covered: Federal vs. private loans and which ones are eligible for forgiveness

- Forgiveness Amounts: Maximum debt relief amounts and how they are determined for borrowers

- Tax Implications: Whether forgiven debt is taxable and potential financial consequences

![]()

Eligibility Criteria: Who qualifies for debt forgiveness based on income, loan type, and employment status

To qualify for student debt forgiveness, understanding the eligibility criteria is crucial. These criteria are primarily based on income, loan type, and employment status, each playing a pivotal role in determining who can benefit from this relief. Let’s break it down step by step to ensure clarity and actionable insights.

Income Thresholds: The Financial Gatekeeper

Income limits are a cornerstone of eligibility. For instance, under the Biden administration’s plan, individuals earning less than $125,000 annually or households earning under $250,000 qualify for up to $10,000 in debt forgiveness. Pell Grant recipients can receive an additional $10,000, capping at $20,000. These thresholds are not arbitrary; they aim to target relief to lower- and middle-income borrowers. To verify income, the Department of Education typically uses tax returns from the most recent filing year. If your income fluctuates, consider filing an amended return to reflect your current financial situation accurately.

Loan Types: Not All Debt Is Created Equal

Eligibility also hinges on the type of loan you hold. Federal student loans, such as Direct Loans, Perkins Loans, and Federal Family Education Loans (FFEL) held by the Department of Education, are generally eligible. However, privately held FFEL loans and Perkins Loans not owned by the Department of Education are excluded. To check your loan type, log into your account on the Federal Student Aid website. If you have a mix of eligible and ineligible loans, focus on consolidating or refinancing the eligible ones to maximize forgiveness benefits.

Employment Status: Public Service as a Pathway

Employment plays a dual role in eligibility. First, borrowers in public service roles—such as teachers, nurses, and government workers—may qualify for the Public Service Loan Forgiveness (PSLF) program, which forgives remaining debt after 120 qualifying payments. Second, during the COVID-19 payment pause, even periods of unemployment or underemployment were considered eligible for forgiveness, provided other criteria were met. If you’re unsure about your employment status’s impact, consult the PSLF Help Tool or contact your loan servicer for personalized guidance.

Practical Tips for Maximizing Eligibility

To ensure you meet the criteria, take proactive steps. First, update your contact information with your loan servicer to receive timely notifications. Second, if you’re near the income threshold, consider strategies like contributing to retirement accounts or deductibles to lower your taxable income. Third, if your loans are ineligible, explore consolidation options to make them qualify. Finally, stay informed about policy updates, as eligibility rules can evolve.

In summary, eligibility for student debt forgiveness is a nuanced interplay of income, loan type, and employment status. By understanding these criteria and taking strategic actions, borrowers can navigate the system effectively and secure the relief they need.

When Will Federal Student Loan Payments Resume? Key Dates and Updates

You may want to see also

Explore related products

![]()

Application Process: Steps and documentation required to apply for student debt forgiveness

Applying for student debt forgiveness requires a clear understanding of the steps involved and the documentation needed to support your application. The process varies depending on the specific forgiveness program, but there are common elements across most initiatives. Typically, the first step is to determine your eligibility, which often hinges on factors like your employment sector, income level, and the type of loans you hold. For instance, the Public Service Loan Forgiveness (PSLF) program requires applicants to have made 120 qualifying payments while working full-time for a government or nonprofit organization. Understanding these criteria is crucial before proceeding.

Once eligibility is confirmed, the next step involves gathering the necessary documentation. This often includes proof of employment, such as pay stubs or employer certification forms, and records of loan payments. For income-driven repayment (IDR) plans, you may need to provide tax returns or pay stubs to verify your income. It’s essential to organize these documents meticulously, as incomplete applications can lead to delays or denials. Some programs, like the recent one-time student debt relief initiative, may require additional forms, such as the Federal Student Aid (FSA) ID, to verify your identity and loan details.

The application process itself usually involves submitting your documentation through an online portal or mailing it to the designated loan servicer. For example, PSLF applicants must submit the Employment Certification Form periodically and the final PSLF application after completing 120 qualifying payments. It’s advisable to keep copies of all submitted materials and track the status of your application. Additionally, stay informed about deadlines, as missing them can disqualify you from the program. For instance, the one-time debt relief application had a specific window for submission, and late applications were not accepted.

A critical aspect of the application process is avoiding common pitfalls. One frequent mistake is failing to update your loan servicer with accurate employment or contact information, which can disrupt the verification process. Another is neglecting to recertify income annually for IDR plans, which can result in higher payments or disqualification. To streamline the process, consider creating a checklist of required documents and deadlines. Tools like the Department of Education’s Loan Simulator can also help you understand your repayment options and forgiveness pathways.

In conclusion, navigating the student debt forgiveness application process demands attention to detail, organization, and proactive communication with loan servicers. By understanding the steps, gathering the right documentation, and avoiding common errors, you can maximize your chances of successfully securing debt relief. Remember, each program has unique requirements, so always refer to official guidelines and seek assistance if needed. With persistence and preparation, the path to financial freedom through debt forgiveness becomes more attainable.

Funding Student Loan Forgiveness: Exploring Potential Sources and Solutions

You may want to see also

Explore related products

![]()

Loan Types Covered: Federal vs. private loans and which ones are eligible for forgiveness

Federal student loans are the primary focus of most debt forgiveness programs, and understanding the nuances between federal and private loans is crucial for borrowers seeking relief. Federal loans, such as Direct Subsidized, Direct Unsubsidized, and PLUS loans, are eligible for a variety of forgiveness programs, including Public Service Loan Forgiveness (PSLF) and income-driven repayment (IDR) plans. These programs typically require borrowers to make consistent payments for a specified period, often 10-25 years, depending on the plan. For instance, PSLF forgives the remaining balance on federal loans after 120 qualifying payments for those working full-time in public service jobs.

In contrast, private student loans are generally excluded from federal forgiveness programs. Private lenders, such as banks or credit unions, issue these loans and are not bound by federal regulations governing forgiveness. Borrowers with private loans may have limited options, often relying on lender-specific programs or refinancing to manage their debt. However, some states and employers offer assistance programs that may include private loan forgiveness, though these are less common and often come with stringent eligibility criteria.

A key distinction lies in the repayment terms and protections offered. Federal loans provide access to IDR plans, which cap monthly payments at a percentage of the borrower’s discretionary income, making them more manageable for low-income earners. These plans also offer forgiveness after 20-25 years of payments, depending on the plan. Private loans rarely offer such flexibility, typically requiring fixed payments that can strain borrowers with limited incomes. For example, a borrower with $50,000 in federal loans under the Revised Pay As You Earn (REPAYE) plan might pay as little as 10% of their discretionary income monthly, with forgiveness after 20 years.

To maximize eligibility for forgiveness, borrowers should prioritize consolidating private loans into a federal Direct Consolidation Loan if possible, though this is rarely feasible. Instead, focus on federal loan forgiveness by enrolling in an IDR plan and ensuring payments qualify for programs like PSLF. For private loans, explore refinancing options to lower interest rates or seek employer-based assistance programs. For instance, teachers in low-income schools may qualify for up to $17,500 in federal loan forgiveness through the Teacher Loan Forgiveness program, but private loans remain ineligible.

In summary, federal loans offer robust forgiveness pathways, while private loans provide limited relief. Borrowers should carefully review their loan types, enroll in appropriate federal programs, and explore alternative solutions for private debt. Understanding these distinctions ensures informed decision-making and maximizes the potential for debt relief.

Student Loan Forgiveness Application Launch Date: What Borrowers Need to Know

You may want to see also

Explore related products

![]()

Forgiveness Amounts: Maximum debt relief amounts and how they are determined for borrowers

The maximum debt relief amounts under student loan forgiveness programs are not one-size-fits-all. They are determined by a combination of factors, including the borrower's income, family size, and the type of loan they hold. For instance, under the Public Service Loan Forgiveness (PSLF) program, borrowers can have their remaining balance forgiven after making 120 qualifying payments while working full-time for a qualifying employer. However, the forgiveness amount is not capped; instead, it is the remaining balance after meeting the payment and employment requirements.

In contrast, income-driven repayment (IDR) plans, such as Pay As You Earn (PAYE) or Revised Pay As You Earn (REPAYE), offer forgiveness after 20-25 years of qualifying payments, depending on the plan. The maximum forgiveness amount under these plans is the remaining balance after the repayment period. However, the forgiven amount may be considered taxable income, which can significantly impact the borrower's financial situation. For example, if a borrower has $50,000 in remaining debt after 20 years of PAYE payments, the entire amount may be forgiven, but they could face a substantial tax bill.

To determine the maximum debt relief amount, borrowers should consider their current income, expected future earnings, and the type of loan they hold. Federal student loans, such as Direct Loans and Perkins Loans, are generally eligible for forgiveness programs, while private loans are typically not. Borrowers with high debt-to-income ratios may benefit more from IDR plans, as their monthly payments are capped at a percentage of their discretionary income. For instance, under the REPAYE plan, monthly payments are limited to 10% of discretionary income, making it an attractive option for borrowers with high debt levels.

A critical aspect of maximizing debt relief is understanding the nuances of each forgiveness program. For example, the PSLF program requires borrowers to work for a qualifying employer, such as a government or non-profit organization, and make 120 qualifying payments. Borrowers must also be enrolled in an IDR plan to qualify for PSLF. In comparison, IDR plans do not require borrowers to work for a specific employer, but the forgiveness amount may be taxed as income. By carefully evaluating their options and seeking guidance from financial aid experts, borrowers can develop a strategy to minimize their debt burden and maximize their forgiveness amount.

Ultimately, the key to unlocking the maximum debt relief amount lies in proactive planning and strategic decision-making. Borrowers should regularly review their loan status, income, and family size to ensure they are on track to meet the requirements for forgiveness. They should also consider refinancing options, if applicable, to lower their interest rates and reduce their overall debt burden. By staying informed and taking a proactive approach, borrowers can navigate the complexities of student loan forgiveness and secure the maximum debt relief amount possible. This may involve seeking advice from financial advisors, attending workshops, or utilizing online resources to stay up-to-date on changes to forgiveness programs and eligibility requirements.

Does Student Loan Debt Disappear When You Pass Away?

You may want to see also

Explore related products

![]()

Tax Implications: Whether forgiven debt is taxable and potential financial consequences

Forgiven student debt can feel like a financial lifeline, but it’s not without strings attached. One critical question borrowers must grapple with is whether this forgiven amount will be treated as taxable income by the IRS. The answer hinges on the type of forgiveness program and the borrower’s circumstances. For instance, under the American Rescue Plan Act of 2021, student loan forgiveness through income-driven repayment plans, Public Service Loan Forgiveness (PSLF), or temporary relief programs like those tied to the COVID-19 pandemic is exempt from federal income tax through 2025. However, this exemption is not permanent, and borrowers should stay informed about potential legislative changes.

Understanding the tax implications requires a closer look at the Internal Revenue Code, specifically Section 108, which generally treats forgiven debt as taxable income. However, exceptions exist, such as insolvency (when your debts exceed your assets) or bankruptcy. For student loans, the Tax Cuts and Jobs Act of 2017 expanded the exclusion for certain types of forgiveness, particularly for borrowers in public service roles or those on income-driven plans. For example, a teacher qualifying for PSLF after 10 years of payments would not owe taxes on the forgiven amount. Yet, borrowers in private loan forgiveness programs or those not covered by recent exemptions may still face a tax bill, potentially wiping out a significant portion of the financial relief.

The financial consequences of taxable forgiven debt can be severe, particularly for low- or middle-income borrowers. Imagine a borrower with $50,000 in forgiven debt taxed at a 22% federal rate, resulting in an $11,000 tax liability. Without proper planning, this could push them into a higher tax bracket or reduce their refund. To mitigate this, borrowers should consider setting aside funds in anticipation of tax season or exploring payment plans with the IRS. Additionally, consulting a tax professional can help identify strategies, such as adjusting withholdings or claiming deductions, to offset the impact.

Comparing the tax treatment of student loan forgiveness to other forms of debt relief highlights its unique challenges. For instance, mortgage debt forgiven under the Mortgage Forgiveness Debt Relief Act is generally tax-free, but this law has specific eligibility criteria and expiration dates. Student loan forgiveness, while sometimes exempt, lacks consistent long-term protections. This disparity underscores the need for borrowers to stay proactive, monitoring policy changes and advocating for permanent tax-free forgiveness. After all, the goal of debt relief is financial stability, not a tax trap.

In practical terms, borrowers should take three immediate steps: first, verify the tax status of their forgiveness program with their loan servicer or the Department of Education. Second, estimate their potential tax liability using online calculators or IRS resources. Third, adjust their financial plan accordingly, whether by saving more, reducing other taxable income, or seeking professional advice. While forgiven student debt can provide significant relief, understanding and preparing for its tax implications is essential to avoid unexpected financial strain.

Do Student Loan Forgiveness Companies Deliver on Their Promises?

You may want to see also

Frequently asked questions

Eligibility for student debt forgiveness depends on the specific program. Generally, it may include borrowers with federal student loans who meet income thresholds or other criteria set by the government.

The amount forgiven varies by program. For example, some plans forgive up to $10,000 for eligible borrowers, with an additional $10,000 for Pell Grant recipients, while others may offer full forgiveness after a certain number of qualifying payments.

It depends on the program. Some forgiveness programs require borrowers to submit an application, while others may automatically apply forgiveness based on existing data. Check the official guidelines for the specific program.

Tax treatment varies. Some forgiveness programs, like those under the American Rescue Plan, are tax-free through 2025. However, other programs may treat forgiven debt as taxable income, so consult a tax professional for your situation.