The student loan bubble, a growing concern in the realm of higher education, refers to the mounting debt accumulated by students and graduates, which now exceeds $1.7 trillion in the United States alone. Fueled by rising tuition costs, limited access to affordable education, and aggressive lending practices, this crisis has far-reaching implications for individuals, the economy, and society as a whole. As borrowers struggle to repay their loans, often facing high interest rates and limited job prospects, the question arises: how will the student loan bubble impact the financial stability of millions, and what measures can be taken to address this pressing issue before it reaches a breaking point?

| Characteristics | Values |

|---|---|

| Total U.S. Student Loan Debt (2023) | $1.77 trillion |

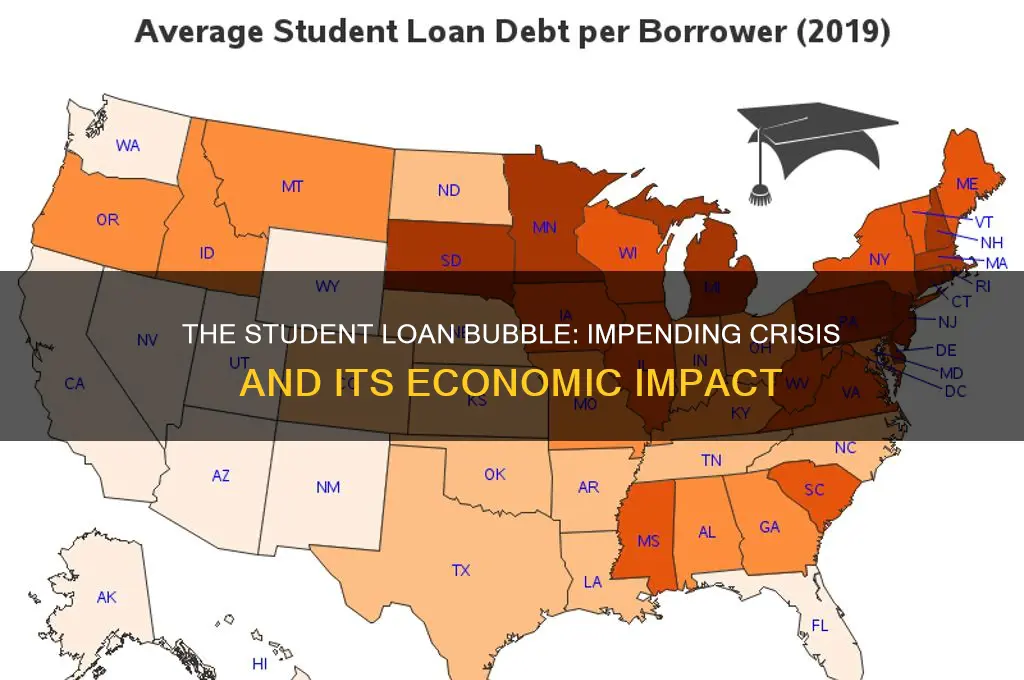

| Average Student Loan Debt per Borrower | $37,787 |

| Number of Student Loan Borrowers in the U.S. | 43.4 million |

| Percentage of Students Borrowing for College | ~70% |

| Default Rate on Federal Student Loans (3-year cohort) | 10.1% (2020 data, latest available) |

| Impact on Homeownership | Delayed homeownership by 7 years on average for borrowers |

| Effect on Consumer Spending | Reduced disposable income, limiting spending on goods/services |

| Government Response | Temporary payment pauses, income-driven repayment plans, limited loan forgiveness programs |

| Economic Risk | Potential drag on GDP growth, reduced consumer confidence |

| Demographic Impact | Disproportionate burden on low-income and minority borrowers |

| Inflation Impact on Borrowers | Increased cost of living reduces ability to repay loans |

| Private vs. Federal Loans | Private loans account for ~8% of total debt, with higher interest rates and fewer protections |

| Loan Forgiveness Programs | Limited scope (e.g., Public Service Loan Forgiveness, Biden’s $10k forgiveness plan, currently blocked) |

| Political Debate | Bipartisan disagreement on solutions, with calls for reform vs. maintaining status quo |

| Long-term Economic Consequences | Potential for reduced economic mobility and increased wealth inequality |

Explore related products

$8.34 $17.99

What You'll Learn

- Causes of the Bubble: Excessive borrowing, rising tuition costs, and aggressive lending practices fuel the crisis

- Economic Impact: Reduced consumer spending, delayed homeownership, and slower economic growth due to debt burden

- Policy Solutions: Loan forgiveness, income-driven repayment, and tuition-free college proposals to address the issue

- Social Consequences: Increased mental stress, delayed life milestones, and widening wealth inequality among graduates

- Future Outlook: Potential for market correction, shifts in higher education funding, and long-term systemic changes

![]()

Causes of the Bubble: Excessive borrowing, rising tuition costs, and aggressive lending practices fuel the crisis

The student loan bubble, a looming crisis in higher education financing, is not the result of a single factor but a toxic combination of excessive borrowing, skyrocketing tuition costs, and predatory lending practices. Let's dissect these causes and their interplay.

Imagine a young adult, fresh out of high school, facing the pressure to attend college for a better future. Universities, with their glossy brochures and promises of high-paying jobs, entice them with seemingly limitless loan options. This scenario, played out millions of times, highlights the first culprit: excessive borrowing. Easy access to loans, often without proper financial literacy education, encourages students to take on debt far exceeding their future earning potential.

This borrowing frenzy is further exacerbated by rising tuition costs. Since the 1980s, college tuition has outpaced inflation by a staggering margin. Public universities, once considered affordable, now rival private institutions in cost. This relentless rise is fueled by administrative bloat, lavish campus amenities, and a reliance on student loan dollars. Universities, knowing students can access loans, have little incentive to control costs, creating a vicious cycle.

Aggressive lending practices complete this unholy trinity. Lenders, both public and private, often target vulnerable populations with misleading terms and high interest rates. Deceptive marketing tactics, lack of transparency, and the absence of borrower protections trap students in a web of debt they struggle to escape. For-profit colleges, in particular, have been notorious for exploiting this system, leaving students with worthless degrees and mountains of debt.

The consequences of this bubble are far-reaching. Graduates, burdened by debt, delay major life milestones like buying homes, starting families, and saving for retirement. This stifles economic growth and contributes to widening wealth inequality. The taxpayer also bears the burden, as defaulted loans strain government resources. Addressing this crisis requires a multi-pronged approach: increased investment in affordable public education, stricter regulations on lending practices, and robust financial literacy programs to empower students to make informed borrowing decisions.

Why Colleges Invest in Students Through Scholarships: A Win-Win Strategy

You may want to see also

Explore related products

![]()

Economic Impact: Reduced consumer spending, delayed homeownership, and slower economic growth due to debt burden

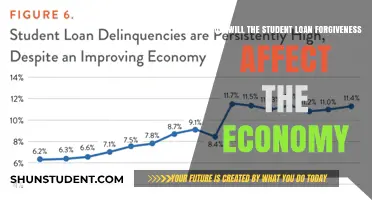

The student loan bubble, now exceeding $1.7 trillion in the U.S., is reshaping consumer behavior in profound ways. Graduates burdened with an average debt of $30,000 are cutting back on discretionary spending, prioritizing loan repayments over dining out, travel, and retail purchases. This shift isn’t just anecdotal; data from the Federal Reserve shows that households with student debt spend 20% less on non-essential items compared to debt-free peers. The ripple effect? A contraction in industries reliant on consumer spending, from hospitality to retail, as millions divert funds toward debt servicing rather than economic participation.

Delayed homeownership is another cascading consequence of this debt burden. Traditionally, individuals in their late 20s and early 30s drive the first-time homebuyer market, but student loans are pushing this milestone back by an average of seven years. A 2021 study by the National Association of Realtors found that 45% of millennials cite student debt as the primary obstacle to saving for a down payment. With the median home price in the U.S. hovering around $350,000, even those with stable incomes struggle to qualify for mortgages while allocating 10–15% of their monthly earnings to loan repayments. This delay not only stifles individual wealth accumulation but also weakens the housing market, a cornerstone of economic stability.

Slower economic growth emerges as the macro-level fallout of these micro-decisions. When consumer spending—which accounts for 70% of U.S. GDP—is suppressed, and major purchases like homes are postponed, the economy loses critical momentum. The International Monetary Fund estimates that countries with high student debt levels experience a 0.2–0.3% reduction in annual GDP growth. For the U.S., this translates to billions in lost economic output annually. Small businesses, often funded by personal savings or home equity loans, face reduced access to capital as borrowers remain trapped in debt cycles. The result? A self-perpetuating cycle of stagnation, where reduced spending and investment further dampen growth prospects.

To mitigate these effects, policymakers and individuals must act strategically. For borrowers, refinancing loans to secure lower interest rates (currently averaging 5.5% for federal loans) can free up monthly cash flow. Employers can offer student loan repayment assistance as a benefit, with up to $5,250 tax-free annually under recent legislation. On a systemic level, expanding income-driven repayment plans and public service loan forgiveness programs could alleviate immediate financial pressure. Without such interventions, the student loan bubble risks becoming a long-term drag on both personal finances and national economic vitality.

Will Bernie Sanders Eliminate Student Loan Debt? A Comprehensive Analysis

You may want to see also

Explore related products

![]()

Policy Solutions: Loan forgiveness, income-driven repayment, and tuition-free college proposals to address the issue

The student loan crisis has reached a tipping point, with over 45 million Americans collectively owing nearly $1.7 trillion. This debt burden stifles economic mobility, delays major life milestones, and threatens broader financial stability. Policy solutions like loan forgiveness, income-driven repayment, and tuition-free college proposals aim to deflate this bubble, but each approach carries distinct trade-offs.

Loan forgiveness programs offer immediate relief but raise questions of fairness and cost. Broad-based forgiveness, such as the Biden administration’s proposed $10,000 to $20,000 per borrower, could eliminate debt for millions of low-balance holders. However, critics argue this benefits higher-earning graduates disproportionately and shifts the burden to taxpayers. Targeted forgiveness, like Public Service Loan Forgiveness (PSLF), rewards specific professions (e.g., teachers, nurses) but requires stringent eligibility criteria, often excluding those most in need. A middle ground might involve means-tested forgiveness, capping eligibility at certain income levels to ensure resources reach those with the greatest financial strain.

Income-driven repayment (IDR) plans address affordability by capping monthly payments at a percentage of discretionary income, typically 10-20%. These plans, such as Pay As You Earn (PAYE) or Revised Pay As You Earn (REPAYE), offer long-term relief but can extend repayment periods to 20-25 years, accruing interest that may exceed the original principal. For example, a borrower with $50,000 in debt at 6% interest could pay over $80,000 under REPAYE. To mitigate this, policymakers could cap interest capitalization or forgive remaining balances after a fixed period, say 10 years of consistent payments. Such reforms would balance borrower protection with fiscal responsibility.

Tuition-free college proposals tackle the root cause by eliminating the need for loans altogether. Programs like New York’s Excelsior Scholarship or Tennessee’s Promise cover tuition for eligible students, reducing reliance on debt. However, these initiatives often exclude living expenses, which comprise over 70% of college costs, and may impose strict eligibility criteria, such as GPA requirements or in-state residency. A more comprehensive approach, like a federal tuition-free model, could pair free tuition with need-based grants for housing, books, and other essentials. While costly—estimates range from $50 billion to $100 billion annually—such investment could yield long-term economic benefits by increasing college access and reducing future debt burdens.

Each policy solution offers a piece of the puzzle but requires careful design to maximize impact. Loan forgiveness provides immediate relief but must be targeted to avoid moral hazard. Income-driven repayment ensures affordability but needs safeguards against interest traps. Tuition-free college addresses systemic issues but demands significant upfront investment. Together, these measures could deflate the student loan bubble, but their success hinges on balancing equity, feasibility, and long-term sustainability.

Will College Students Be Sent Home Amid Rising Concerns?

You may want to see also

Explore related products

$7.34 $9.99

![]()

Social Consequences: Increased mental stress, delayed life milestones, and widening wealth inequality among graduates

The student loan bubble has left an indelible mark on the mental health of graduates, with studies showing a direct correlation between high debt levels and increased anxiety, depression, and stress. For instance, a 2021 survey by the American Psychological Association found that 68% of student loan borrowers reported feeling overwhelmed by their debt, leading to sleepless nights, reduced productivity, and strained relationships. This mental burden is exacerbated by the constant pressure to meet monthly payments, often at the expense of personal well-being. To mitigate this, graduates can explore debt consolidation options, seek counseling services, or join support groups to share experiences and coping strategies.

Delayed life milestones are another stark consequence of the student loan crisis. Burdened by debt, many graduates are forced to postpone major life decisions such as buying a home, starting a family, or even getting married. For example, data from the Federal Reserve shows that the homeownership rate among young adults with student debt is 8 percentage points lower than their debt-free peers. This delay not only impacts individual happiness but also has broader societal implications, such as declining birth rates and a slower economy. Graduates can counteract this by creating a structured repayment plan, prioritizing high-interest loans, and exploring income-driven repayment programs to free up funds for other life goals.

Wealth inequality among graduates is widening at an alarming rate, as those from lower-income backgrounds are disproportionately affected by student debt. While wealthier graduates often receive financial support from family, their less privileged counterparts must rely heavily on loans, accruing more debt and limiting their ability to build wealth. For instance, a Brookings Institution report revealed that 20 years after entering college, the average wealth of a student from a low-income family is $6,000, compared to $200,000 for a high-income student. This disparity perpetuates systemic inequality, making it harder for low-income graduates to achieve financial stability. Policymakers and institutions must address this by expanding grant-based aid, capping interest rates, and implementing loan forgiveness programs targeted at underserved communities.

The cumulative effect of these social consequences creates a vicious cycle, where mental stress, delayed milestones, and wealth inequality reinforce one another. For example, a graduate struggling with mental health due to debt may find it harder to secure a high-paying job, further delaying their ability to pay off loans or achieve financial independence. To break this cycle, graduates should adopt a holistic approach: prioritize mental health through therapy or mindfulness practices, set realistic financial goals, and advocate for systemic changes that address the root causes of the student loan crisis. By doing so, they can reclaim control over their futures and mitigate the long-term impact of this burden.

Forgiving Student Debt: A Step-by-Step Guide to Loan Forgiveness

You may want to see also

Explore related products

![]()

Future Outlook: Potential for market correction, shifts in higher education funding, and long-term systemic changes

The student loan bubble, now exceeding $1.7 trillion in the U.S., has reached a critical mass, prompting speculation about an inevitable market correction. Historical precedents, such as the housing bubble of 2008, suggest that asset bubbles rarely deflate gently. For student loans, a correction could manifest as a surge in defaults, triggered by factors like economic recession or policy changes. If default rates climb above the current 10% average, lenders and the government could face significant losses, potentially leading to tighter lending standards or loan forgiveness programs. However, such a correction would also expose the fragility of a system where 45 million borrowers owe an average of $30,000, with many struggling to repay due to wage stagnation and underemployment.

Shifting the focus to higher education funding reveals a landscape ripe for transformation. Public universities, which educate 70% of U.S. students, rely heavily on state funding that has declined by 13% per student since 2008. This shortfall has been offset by tuition hikes, exacerbating student debt. A potential shift could involve increased federal or state investment in higher education, modeled after systems in Germany or Norway, where tuition is free or heavily subsidized. Alternatively, income-share agreements (ISAs), already piloted by institutions like Purdue University, could gain traction. Under ISAs, students repay a percentage of their income post-graduation, aligning repayment with earning potential and reducing default risk.

Long-term systemic changes must address the root causes of the student loan crisis, not just its symptoms. One proposal is to reevaluate the role of for-profit colleges, which account for 10% of enrollments but 28% of defaults. Stricter accreditation standards and transparency in graduation and employment rates could curb predatory practices. Additionally, expanding vocational and technical education could provide debt-free pathways to high-demand careers, such as nursing or IT, where median salaries exceed $60,000. For existing borrowers, policy reforms like automatic enrollment in income-driven repayment plans or tax-free loan forgiveness could alleviate financial strain and stimulate economic growth.

A comparative analysis of global approaches highlights viable alternatives. Australia’s Higher Education Loan Program (HELP) ties repayments to income, capping payments at 10% of earnings above a threshold. This model ensures affordability while maintaining fiscal sustainability. In contrast, the U.K.’s system, where loans are written off after 30 years, reduces long-term borrower stress but places a heavier burden on taxpayers. Adopting hybrid models, such as combining income-driven repayment with public funding for tuition, could balance individual and societal responsibilities. However, implementation would require bipartisan cooperation and a willingness to challenge entrenched interests in the education and financial sectors.

Ultimately, the future of the student loan bubble hinges on proactive measures to prevent collapse while fostering equitable access to education. A market correction, while painful, could catalyze reforms that prioritize affordability and accountability. Shifts in funding models, such as increased public investment or innovative repayment structures, could reduce reliance on debt. Long-term systemic changes, including regulatory reforms and expanded alternatives to traditional degrees, could rebuild trust in higher education as a pathway to opportunity. The stakes are high, but with strategic action, the crisis can become a turning point toward a more sustainable and inclusive system.

Biden's Student Loan Forgiveness Plan: Who Qualifies and How Much?

You may want to see also

Frequently asked questions

The student loan bubble refers to the rapidly growing and unsustainable accumulation of student loan debt in the United States and other countries. It is characterized by high levels of borrowing for education, often exceeding the ability of borrowers to repay, coupled with rising tuition costs and limited job prospects for graduates.

The student loan bubble could negatively impact the economy by reducing consumer spending, delaying major life milestones (like homeownership or starting a family), and increasing defaults, which could strain financial institutions and government budgets. It may also stifle entrepreneurship and economic mobility.

If the student loan bubble bursts, widespread defaults could occur, leading to significant financial losses for lenders and the government. This could trigger a ripple effect, reducing credit availability, lowering property values, and potentially causing a recession or economic downturn.

Student loan forgiveness could provide temporary relief for borrowers, but it does not address the root causes of the bubble, such as rising tuition costs and inadequate funding for public education. Without systemic reforms, the problem may re-emerge in the future.

Preventing or mitigating the student loan bubble requires addressing its underlying causes, such as capping tuition increases, expanding access to affordable public education, improving financial literacy, and implementing income-driven repayment plans. Policy changes to regulate predatory lending practices and increase accountability for educational institutions are also essential.