The topic of whether President Joe Biden has forgiven any student loans has been a central issue in American politics and education policy. Since taking office, Biden has faced mounting pressure from progressive lawmakers, advocacy groups, and student loan borrowers to address the $1.7 trillion student debt crisis. While he has taken steps to provide temporary relief, such as extending the pause on federal student loan payments and interest accrual during the COVID-19 pandemic, Biden has not yet implemented broad-scale student loan forgiveness. However, he has forgiven targeted amounts of debt for specific groups, including borrowers defrauded by for-profit colleges and those eligible under the Public Service Loan Forgiveness program. Despite these actions, calls for more comprehensive forgiveness, such as canceling $10,000 to $50,000 per borrower, continue to dominate public discourse, leaving many to question the extent and timing of further relief measures.

| Characteristics | Values |

|---|---|

| Total Student Loan Forgiveness | Over $132 billion forgiven for 3.6 million borrowers (as of May 2024) |

| Key Programs | Public Service Loan Forgiveness (PSLF), Income-Driven Repayment (IDR) adjustments, targeted relief for defrauded students, and other initiatives |

| PSLF Forgiveness | Over $62 billion forgiven for 779,000 public service workers (as of May 2024) |

| IDR Adjustments | $39 billion forgiven for 804,000 borrowers due to payment count corrections (as of April 2024) |

| Borrower Defense to Repayment | $15.5 billion forgiven for 615,000 students defrauded by predatory schools (as of March 2024) |

| One-Time Pandemic Adjustment | $7.7 billion forgiven for 425,000 borrowers through temporary pandemic-related fixes (as of February 2024) |

| Other Targeted Relief | $7.8 billion forgiven for specific groups, including disabled borrowers and those with total and permanent disability discharges |

| Legal Challenges | Multiple lawsuits have blocked or delayed parts of the forgiveness plans, particularly the broad $400 billion debt cancellation proposal |

| Current Status of Broad Forgiveness | Supreme Court struck down Biden's $400 billion debt cancellation plan in June 2023, citing lack of congressional authorization |

| Future Plans | Administration continues to pursue targeted relief and regulatory changes to reduce student debt burden |

Explore related products

$17.99 $18.99

$7.99 $14.99

What You'll Learn

![]()

Biden's Student Loan Forgiveness Plan

As of the latest updates, President Biden's administration has implemented a series of targeted student loan forgiveness initiatives, collectively referred to as the Biden Student Loan Forgiveness Plan. This plan is not a blanket solution but a strategic approach to alleviate the burden on specific groups of borrowers. One of the most notable actions is the Public Service Loan Forgiveness (PSLF) waiver, which temporarily relaxed rules to allow more public servants to qualify for debt cancellation. For instance, borrowers who had previously been in the wrong repayment plan or had certain types of loans became eligible for forgiveness after 10 years of qualifying payments. This waiver, which expired in October 2022, resulted in billions of dollars in debt relief for over 170,000 borrowers.

Another key component is the targeted loan cancellation for defrauded students under the Borrower Defense to Repayment program. This initiative has provided relief to students who attended predatory for-profit institutions, such as ITT Tech and Corinthian Colleges. As of 2023, the Biden administration has approved over $13 billion in discharges for more than 600,000 borrowers under this program. These actions highlight a shift from broad forgiveness to addressing systemic issues and protecting vulnerable borrowers.

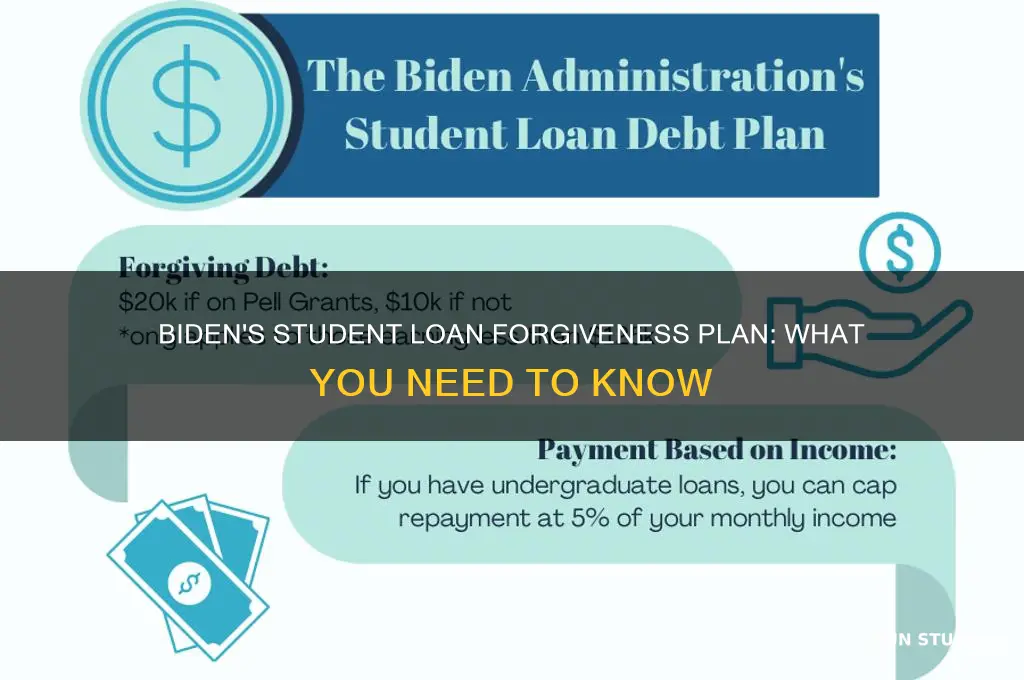

In addition to these measures, the administration has proposed a one-time cancellation of up to $20,000 in student debt for Pell Grant recipients and up to $10,000 for other federal loan borrowers earning less than $125,000 annually (or $250,000 for married couples). However, this proposal has been mired in legal challenges, with the Supreme Court striking it down in June 2023. Despite this setback, the administration continues to explore alternative pathways to provide relief, such as revising income-driven repayment (IDR) plans to reduce monthly payments and shorten the time to forgiveness.

For borrowers navigating these changes, it’s crucial to stay informed and take proactive steps. First, check eligibility for PSLF or Borrower Defense by reviewing the Federal Student Aid website. Second, enroll in an IDR plan to lower monthly payments and potentially qualify for forgiveness after 20–25 years. Third, monitor updates on the $10,000–$20,000 cancellation plan, as the administration may introduce revised criteria or new programs. Finally, avoid scams by only using official government resources for loan forgiveness applications.

While Biden’s plan has not forgiven all student loans, it has made significant strides in addressing specific inequities and providing relief to targeted groups. The focus on public servants, defrauded students, and low-income borrowers reflects a pragmatic approach to a complex issue. As the landscape evolves, borrowers must remain engaged and leverage available resources to maximize their chances of debt relief.

Unlock Public Service Loan Forgiveness: Your Step-by-Step Application Guide

You may want to see also

Explore related products

![]()

Eligibility Criteria for Loan Forgiveness

The Biden administration's student loan forgiveness initiatives have sparked widespread interest, but not all borrowers qualify. Understanding the eligibility criteria is crucial for those seeking relief. The Public Service Loan Forgiveness (PSLF) program, for instance, requires borrowers to make 120 qualifying payments while working full-time for a government or non-profit organization. This program is not new, but recent waivers have expanded eligibility, allowing previously ineligible payments to count toward the 120-payment threshold. For example, payments made under the Federal Family Education Loan (FFEL) program, which were previously excluded, can now be included if consolidated into a Direct Loan.

Another key initiative is the targeted loan cancellation for specific groups. Borrowers who attended predatory for-profit institutions, such as Corinthian Colleges or ITT Tech, may qualify for automatic discharges under the Borrower Defense to Repayment program. Additionally, those with total and permanent disabilities can have their loans discharged through the Total and Permanent Disability (TPD) discharge program. To apply for TPD discharge, borrowers must provide documentation from the Department of Veterans Affairs, the Social Security Administration, or a physician certifying their disability. It’s essential to note that these discharges are tax-free through 2025, thanks to recent legislative changes.

Income-driven repayment (IDR) plans also play a significant role in loan forgiveness eligibility. Borrowers on IDR plans can have their remaining balance forgiven after 20 or 25 years of qualifying payments, depending on the plan. The Biden administration’s IDR Account Adjustment, launched in 2022, retroactively credited borrowers for past payment periods, including those in forbearance or on non-qualifying repayment plans. This adjustment has brought many borrowers closer to forgiveness, particularly those who have been in repayment for decades. For example, a borrower who has been in repayment for 20 years but switched plans multiple times may now have those years count toward forgiveness.

Comparatively, the one-time student loan cancellation plan, which aimed to forgive up to $20,000 for Pell Grant recipients and $10,000 for non-recipients, faced legal challenges and was blocked by the Supreme Court in 2023. This highlights the importance of focusing on existing programs with clear eligibility criteria. Borrowers should prioritize understanding the requirements for PSLF, TPD discharge, and IDR forgiveness, as these programs remain active and accessible. For instance, consolidating FFEL loans into Direct Loans can open up PSLF eligibility, a practical step for many borrowers.

Finally, staying informed about updates to eligibility criteria is essential. The Department of Education frequently announces changes, such as time-limited waivers or expansions of qualifying employment for PSLF. Subscribing to federal student aid newsletters or consulting with a loan servicer can provide timely information. Borrowers should also maintain detailed records of their payments and employment, as these documents are often required to prove eligibility. By proactively meeting these criteria, borrowers can maximize their chances of securing loan forgiveness under the Biden administration’s initiatives.

Defrauded Student Loan Forgiveness: A Step-by-Step Application Guide

You may want to see also

Explore related products

![]()

Impact on Borrowers' Credit Scores

Student loan forgiveness under Biden’s initiatives has sparked debates about its impact on borrowers’ credit scores, a critical factor in financial health. While forgiveness removes debt, its effect on credit isn’t uniform. For instance, discharged loans are typically reported as "paid in full" or "settled," which can neutralize their negative impact if they were previously in default or delinquency. However, this outcome depends on accurate reporting by servicers, a process that has historically been prone to errors. Borrowers must monitor their credit reports post-forgiveness to ensure updates reflect the discharge correctly, as discrepancies can linger and harm scores unnecessarily.

Analyzing the mechanics reveals a nuanced relationship between forgiveness and credit scoring. FICO and VantageScore models consider factors like payment history, credit utilization, and debt levels. Forgiveness reduces overall debt, potentially improving the debt-to-credit ratio, a key metric. Yet, if forgiven loans were in good standing, their removal might shorten the borrower’s credit history, a factor that constitutes 15% of a FICO score. For younger borrowers with limited credit accounts, this could temporarily lower scores. Conversely, older borrowers with diverse credit profiles may see minimal impact, as the benefit of reduced debt outweighs the loss of a positive payment history.

A persuasive argument for proactive credit management emerges when considering long-term implications. Borrowers should not assume forgiveness automatically boosts their score. Instead, they should focus on maintaining healthy credit habits: paying bills on time, keeping credit card balances low, and avoiding new debt. For those with multiple loans, prioritizing high-interest debt repayment while awaiting forgiveness can mitigate risks. Additionally, leveraging tools like credit monitoring services or free annual credit reports can help identify and dispute inaccuracies, ensuring forgiveness translates to a stronger credit profile.

Comparatively, the impact of Biden’s forgiveness programs differs from other debt relief methods, such as bankruptcy or debt settlement. Bankruptcy, for example, can drop credit scores by 160–220 points and remain on reports for up to 10 years. In contrast, forgiven student loans, when reported accurately, carry less stigma. However, borrowers must distinguish between forgiveness and forbearance or deferment, which pause payments but don’t erase debt. Misunderstanding these terms can lead to missed opportunities or unintended credit damage, underscoring the need for financial literacy in navigating these programs.

Finally, a descriptive snapshot of real-world outcomes highlights the variability in borrower experiences. Take Sarah, a 32-year-old teacher whose $40,000 loan was forgiven under the Public Service Loan Forgiveness program. Her credit score initially dipped by 15 points due to reduced credit history length but rebounded within six months as her low credit utilization ratio improved. Conversely, John, a 28-year-old with defaulted loans, saw a 30-point increase after forgiveness, as the removal of derogatory marks outweighed other factors. These examples illustrate that while forgiveness can reshape credit landscapes, individual outcomes hinge on pre-existing financial behaviors and reporting accuracy.

Student Loan Relief: Is $5,000 Debt Forgiveness Enough?

You may want to see also

Explore related products

![]()

Public Service Loan Forgiveness Updates

The Public Service Loan Forgiveness (PSLF) program has seen significant updates under the Biden administration, offering new hope to borrowers in public service roles. One of the most notable changes is the Limited PSLF Waiver, which temporarily expanded eligibility criteria until October 31, 2022. This waiver allowed past payments on any federal loan type, including those previously ineligible, to count toward forgiveness. For example, borrowers with Federal Family Education Loans (FFEL) or Perkins Loans could consolidate into Direct Loans and retroactively qualify for PSLF. This move addressed long-standing frustrations with the program’s strict requirements, providing a lifeline to thousands of public servants.

To maximize the benefits of these updates, borrowers should take specific steps. First, consolidate non-Direct Loans into the Direct Loan program if you haven’t already—this is a prerequisite for PSLF eligibility. Second, submit the PSLF form to ensure your qualifying payments are counted, especially if you’ve made payments under a non-qualifying plan. Third, review your employment certification to confirm your employer qualifies under PSLF guidelines. For instance, non-profit organizations, government agencies, and certain public schools meet the criteria. These actions, combined with the waiver’s flexibility, can significantly reduce the time to forgiveness.

A critical analysis of the PSLF updates reveals both progress and lingering challenges. While the waiver addressed historical barriers, such as payment plan ineligibility, it also highlighted the program’s complexity. Many borrowers reported confusion about the consolidation process or uncertainty about whether their payments qualified. Additionally, the October 2022 deadline created a rush, leaving some borrowers scrambling to meet requirements. Moving forward, advocates argue for permanent reforms, such as simplifying eligibility rules and improving borrower support, to ensure the program’s long-term effectiveness.

For public servants navigating these updates, practical tips can make a difference. Keep detailed records of your payments and employment certifications, as documentation is key to proving eligibility. If you’re unsure about your status, contact your loan servicer or use the Department of Education’s PSLF Help Tool for guidance. Finally, stay informed about potential future changes, as the Biden administration continues to explore student loan relief measures. By leveraging these updates and staying proactive, public servants can turn the PSLF program into a tangible path to debt freedom.

Unlocking Student Loan Forgiveness: Strategies to Erase $20,000 in Debt

You may want to see also

Explore related products

![]()

Criticisms of Biden's Forgiveness Policy

President Biden's student loan forgiveness policy, which aimed to alleviate the financial burden on millions of Americans, has faced significant criticism from various quarters. One of the primary concerns is the perceived inequity of the policy. Critics argue that forgiving student loans disproportionately benefits higher-income individuals who are more likely to hold advanced degrees and larger loan balances. For instance, a borrower with a law degree and $200,000 in debt stands to gain more than someone with an associate degree and $10,000 in loans. This disparity raises questions about whether the policy effectively targets those most in need.

Another point of contention is the economic impact of widespread loan forgiveness. Opponents claim that canceling billions in student debt could exacerbate inflation, as it injects additional spending power into the economy without addressing underlying supply constraints. While the Biden administration has capped individual forgiveness at $10,000 (or $20,000 for Pell Grant recipients), the aggregate cost of the program remains substantial. Critics suggest that this money could be better spent on broader economic initiatives, such as infrastructure or healthcare, which might yield more widespread benefits.

Legal challenges have also plagued the policy, with critics questioning its constitutionality. Several lawsuits argue that the administration overstepped its authority by implementing loan forgiveness through executive action rather than congressional legislation. This debate highlights a deeper divide over the role of the executive branch in shaping fiscal policy. If the courts rule against the administration, it could set a precedent limiting future presidential actions on similar issues, leaving borrowers in limbo.

Lastly, there is a moral hazard argument against blanket forgiveness. Detractors contend that canceling debt without addressing the root causes of rising tuition costs could encourage colleges to continue increasing prices, knowing that future loans might be forgiven. This cycle could perpetuate the very problem the policy aims to solve. Critics advocate for structural reforms, such as capping interest rates or increasing funding for public institutions, as more sustainable solutions to the student debt crisis.

In summary, while Biden's student loan forgiveness policy has been hailed as a lifeline for many borrowers, it has also sparked intense criticism. Concerns about equity, economic impact, legal authority, and long-term consequences underscore the complexity of addressing student debt. As the debate continues, it is clear that any solution must balance immediate relief with systemic change to avoid repeating the mistakes of the past.

Mastering Student Loan Forgiveness: A Step-by-Step Application Guide

You may want to see also

Frequently asked questions

Yes, President Biden has forgiven student loans for specific groups, including borrowers who attended predatory for-profit schools, disabled borrowers, and those eligible under the Public Service Loan Forgiveness (PSLF) program. Additionally, his administration has implemented targeted debt cancellation for certain borrowers.

As of October 2023, the Biden administration has forgiven over $127 billion in student loan debt for approximately 3.6 million borrowers through various programs and initiatives, including targeted cancellations and PSLF reforms.

No, Biden has not forgiven all student loans for everyone. His administration has focused on targeted relief for specific groups, such as low-income borrowers, defrauded students, and public service workers, rather than broad, universal forgiveness.