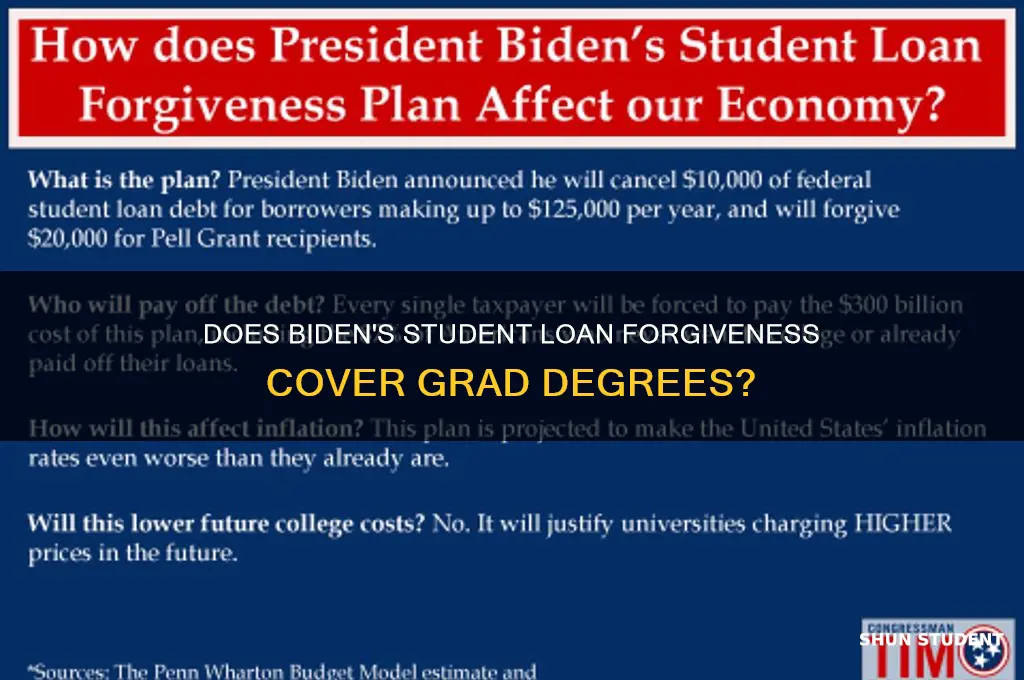

The topic of whether President Biden's student loan forgiveness plan includes graduate degrees has sparked significant debate and confusion among borrowers. While the Biden administration has announced various initiatives to alleviate student debt, the specifics of eligibility, particularly for graduate degree holders, remain a point of contention. Many are questioning whether advanced degrees, such as master's or doctoral programs, qualify for forgiveness under the current proposals. Clarifying these details is crucial, as graduate students often carry substantial debt burdens, and understanding the scope of relief could impact millions of borrowers seeking financial reprieve.

| Characteristics | Values |

|---|---|

| Eligibility for Grad Degrees | Yes, Biden's student loan forgiveness includes graduate and professional degrees. |

| Income Eligibility Threshold | $125,000 for individuals, $250,000 for married couples (based on 2020-2021 tax returns). |

| Forgiveness Amount | Up to $10,000 in forgiveness for non-Pell Grant recipients; up to $20,000 for Pell Grant recipients. |

| Loan Types Covered | Federal student loans held by the Department of Education, including Direct Loans, FFELP Loans (if consolidated into Direct Loans), and Perkins Loans. |

| Private Loans Eligibility | No, private student loans are not eligible for forgiveness under this program. |

| Application Process | Borrowers must apply through the Department of Education's online portal (application expected to open in October 2023). |

| Tax Implications | Forgiveness is tax-free at the federal level, though some states may tax it. |

| Impact on Credit Score | Forgiveness does not negatively impact credit scores. |

| Repayment Restart Date | Student loan payments resumed in October 2023 after a pandemic-related pause. |

| Legal Challenges | The program faced legal challenges, but the Supreme Court ruled against it in June 2023, halting its implementation. |

| Current Status | As of October 2023, the program is on hold due to the Supreme Court ruling, but the Biden administration is exploring alternative paths to provide relief. |

Explore related products

What You'll Learn

![]()

Eligibility Criteria for Grad Degrees

Biden's student loan forgiveness plan has sparked considerable debate, particularly regarding its inclusivity of graduate degrees. While the plan aims to alleviate financial burdens for millions, understanding the eligibility criteria for grad degrees is crucial for borrowers navigating this complex landscape.

Graduate degree holders often carry significantly higher debt burdens compared to undergraduate borrowers. The average graduate student loan debt exceeds $70,000, highlighting the urgent need for targeted relief.

Income-Driven Repayment Plans: A Key Gateway

A central pillar of Biden's plan is the expansion of income-driven repayment (IDR) plans. These plans cap monthly payments based on income and family size, offering a lifeline to borrowers struggling with high debt-to-income ratios. Crucially, IDR plans are open to borrowers with both undergraduate and graduate loans, making them a vital pathway to forgiveness for grad degree holders.

Under the revised IDR plans, borrowers earning under $150,000 annually (or $300,000 for married couples filing jointly) may qualify for reduced payments. After 20 years of consistent payments under an IDR plan, any remaining balance is forgiven. This extended timeline acknowledges the higher earning potential often associated with graduate degrees while still providing a path to debt relief.

Public Service Loan Forgiveness: A Faster Track for Some

For grad degree holders working in public service, the Public Service Loan Forgiveness (PSLF) program offers a potentially faster route to forgiveness. This program forgives the remaining balance on Direct Loans after 120 qualifying payments (10 years) while working full-time for a qualifying employer, such as government agencies, non-profit organizations, or certain educational institutions.

Targeted Relief for Specific Fields

While the broad forgiveness plan doesn't explicitly target specific graduate degrees, certain professions may benefit from existing or proposed initiatives. For example, programs aimed at encouraging careers in healthcare, education, or STEM fields might offer loan forgiveness or repayment assistance for individuals with relevant graduate degrees.

Navigating the Nuances: A Call for Vigilance

Understanding the intricacies of eligibility criteria is paramount. Borrowers should carefully review the specific requirements for IDR plans, PSLF, and any field-specific programs. Consulting with a qualified financial advisor or student loan counselor can provide personalized guidance and ensure borrowers maximize their chances of qualifying for forgiveness.

Capitalized Student Loan Interest Forgiveness Under PSLF: What You Need to Know

You may want to see also

Explore related products

$8.34 $17.99

$17.99 $18.99

![]()

Loan Limits and Grad Programs

Biden's student loan forgiveness plan has sparked debates about its scope, particularly regarding graduate degrees. While the plan aims to alleviate the burden of student debt, the inclusion of graduate programs is not as straightforward as it might seem. The loan limits for graduate students are a critical factor in determining eligibility and the extent of relief.

Understanding Loan Limits

Graduate students often face higher loan limits compared to their undergraduate counterparts. For instance, the annual loan limit for graduate and professional students is $20,500, with an aggregate limit of $138,500. This is significantly higher than the $31,000 aggregate limit for dependent undergraduate students. As a result, graduate students may accumulate substantial debt, making loan forgiveness a crucial aspect of their financial planning.

Eligibility Criteria and Grad Programs

The eligibility criteria for Biden's student loan forgiveness plan are based on income and loan type, rather than the degree level. Borrowers earning less than $125,000 (individuals) or $250,000 (married couples) are eligible for up to $10,000 in forgiveness, with an additional $10,000 for Pell Grant recipients. This means that graduate students, regardless of their degree program, may qualify for forgiveness if they meet the income requirements. However, the loan limits for graduate programs can impact the overall amount of forgiveness.

Implications for Grad Students

For graduate students with loans exceeding the undergraduate aggregate limit, the forgiveness plan may provide partial relief. Suppose a graduate student has accumulated $150,000 in debt, exceeding the $138,500 aggregate limit. In that case, they may still be eligible for $10,000 in forgiveness, but the remaining balance will not be covered. This highlights the need for graduate students to carefully consider their loan amounts and explore alternative repayment options, such as income-driven repayment plans.

Strategies for Grad Students

To maximize the benefits of the loan forgiveness plan, graduate students should:

- Review their loan portfolio: Identify the types of loans held (e.g., Direct Loans, FFEL Loans) and their current balances.

- Assess income eligibility: Determine if their income falls within the specified thresholds to qualify for forgiveness.

- Explore repayment options: Consider income-driven repayment plans, which can lower monthly payments and potentially lead to loan forgiveness after a certain period.

- Stay informed: Keep track of updates and changes to the loan forgiveness plan, as well as any new initiatives targeting graduate student debt.

By understanding the loan limits and eligibility criteria, graduate students can make informed decisions about their debt management and take advantage of available relief options. While the forgiveness plan may not cover the entirety of their debt, it can provide a significant financial boost, enabling them to focus on their careers and long-term financial goals.

Navigating the Path to Student Loan Forgiveness: A Comprehensive Guide

You may want to see also

Explore related products

$13.97 $22.95

![]()

Public vs. Private Grad Loans

Biden's student loan forgiveness plan has sparked debates about its scope, particularly whether it covers graduate degrees. While the plan primarily targets federal student loans, the distinction between public and private grad loans becomes crucial for borrowers navigating potential relief.

Understanding the Divide: Public grad loans, also known as federal loans, are issued by the government and offer fixed interest rates, income-driven repayment plans, and potential loan forgiveness options. These loans are often more borrower-friendly, with protections like deferment and forbearance. In contrast, private grad loans are provided by banks, credit unions, or other financial institutions, typically with variable interest rates and less flexible repayment terms. Private loans rarely offer forgiveness programs, making them a riskier choice for graduate students.

Forgiveness Implications: Here's where the distinction matters. Biden's plan focuses on federal student loans, which includes grad school debt. Eligible borrowers with federal loans can receive up to $20,000 in forgiveness if they received a Pell Grant, and up to $10,000 without one. This relief extends to graduate-level loans, such as Direct Unsubsidized Loans and Grad PLUS Loans. However, private grad loans are excluded from this forgiveness program, leaving borrowers with these loans without direct relief.

Strategic Considerations: For graduate students, the choice between public and private loans should be strategic. Opting for federal loans provides access to potential forgiveness programs and more flexible repayment options. It's essential to exhaust federal loan options before considering private lenders. If private loans are necessary, borrowers should carefully review the terms, interest rates, and repayment conditions. Refinancing private loans to secure better rates or terms might be a viable strategy, but it won't make them eligible for federal forgiveness programs.

Long-Term Impact: The decision between public and private grad loans has long-lasting consequences. Federal loans offer a safety net with various repayment plans and forgiveness opportunities, which can be crucial for graduates entering fields with varying income potential. Private loans, while sometimes necessary, require a thorough understanding of the risks involved. Borrowers should consider their future earning potential, the loan's interest rate, and the likelihood of qualifying for private loan forgiveness programs, which are often limited and specific.

In the context of Biden's student loan forgiveness, the public vs. private grad loan debate highlights the importance of informed borrowing decisions. Graduate students must weigh their options, considering both immediate financial needs and long-term repayment strategies to ensure a manageable debt burden.

Understanding Loan Forgiveness: What Current Students Need to Know

You may want to see also

Explore related products

![]()

Income Caps for Grad Borrowers

Biden's student loan forgiveness plan has sparked intense debate, particularly regarding its inclusivity of graduate degree borrowers. While the plan offers relief to millions, the income caps for grad borrowers have emerged as a critical point of contention. These caps, set at $125,000 for individuals and $250,000 for married couples, determine eligibility for up to $20,000 in loan forgiveness. For graduate borrowers, who often carry higher debt loads due to advanced degrees, these thresholds can feel restrictive. Many argue that these caps fail to account for the higher earning potential and cost of living associated with graduate-level professions, leaving some high-debt borrowers ineligible despite their financial strain.

Consider the case of a recent law school graduate with $150,000 in student loans, earning $130,000 annually. Despite their substantial debt, they exceed the income cap by just $5,000, disqualifying them from any forgiveness. This scenario highlights a gap in the policy: while intended to target lower-income borrowers, the caps may inadvertently exclude graduate borrowers who are still struggling under significant debt. Critics suggest that a more nuanced approach, such as adjusting caps based on debt-to-income ratios or degree type, could better address the unique financial realities of grad borrowers.

From a practical standpoint, graduate borrowers navigating this policy should first assess their eligibility by comparing their annual income to the caps. Tools like the Federal Student Aid website can provide clarity on whether they qualify. For those just above the threshold, exploring income-driven repayment plans or refinancing options may offer temporary relief. Additionally, staying informed about potential policy updates is crucial, as advocacy groups continue to push for adjustments that could expand eligibility for grad borrowers.

Persuasively, the income caps for grad borrowers underscore a broader issue: the one-size-fits-all approach to student loan forgiveness may not adequately address the diverse financial landscapes of borrowers. Graduate degrees, while often linked to higher earnings, also come with higher debt and longer repayment periods. By failing to account for these differences, the current policy risks leaving a significant portion of grad borrowers in financial limbo. A more tailored approach, one that considers both income and debt levels, could ensure that relief reaches those who need it most, regardless of their degree level.

In conclusion, while Biden's student loan forgiveness plan represents a significant step toward alleviating educational debt, its income caps for grad borrowers warrant reevaluation. By addressing these limitations, policymakers can create a more equitable system that acknowledges the unique challenges faced by graduate degree holders. For now, grad borrowers must carefully navigate the existing framework, leveraging available resources and staying vigilant for potential changes that could expand their eligibility for much-needed relief.

VA Disability Benefits: Student Loan Deferment Options for 50% Rating

You may want to see also

Explore related products

![]()

Impact on Grad School Enrollment

Biden's student loan forgiveness plan, which includes provisions for graduate degrees, has sparked a wave of speculation about its potential impact on grad school enrollment. While the plan aims to alleviate the burden of student debt, its effects on enrollment trends are multifaceted and depend on various factors.

Analyzing the Incentives

The inclusion of graduate degrees in the forgiveness plan may incentivize individuals to pursue advanced studies, particularly those from low-income backgrounds. With the prospect of reduced debt, prospective students might be more inclined to take the financial risk associated with grad school. For instance, a recent survey by the National Association of Graduate Admissions Professionals (NAGAP) revealed that 42% of respondents would be more likely to enroll in a graduate program if they knew their loans would be partially or fully forgiven. This suggests that the forgiveness plan could lead to a surge in applications, especially in fields with high earning potential, such as STEM, business, and healthcare.

A Comparative Perspective

To understand the potential impact, it's essential to compare the current situation with historical trends. During the 2008 recession, grad school enrollment increased by 14% as individuals sought to enhance their skills and competitiveness in a tough job market. Similarly, the COVID-19 pandemic led to a 5% rise in graduate applications, as many professionals opted to upskill during the economic downturn. The student loan forgiveness plan, combined with the ongoing economic recovery, could create a similar environment, driving more individuals to pursue graduate degrees. However, it's crucial to note that the plan's eligibility criteria, which include income limits and loan types, may exclude some prospective students, potentially mitigating the overall impact on enrollment.

Practical Considerations for Prospective Students

For individuals considering grad school, it's vital to weigh the benefits of the forgiveness plan against the potential risks. Firstly, calculate the expected debt relief based on your loan type, balance, and income. The plan forgives up to $20,000 for Pell Grant recipients and $10,000 for non-recipients, but only for federal loans. Private loans are not eligible. Secondly, research the job prospects and earning potential in your desired field to ensure that the investment in grad school aligns with your long-term career goals. Lastly, consider alternative funding options, such as scholarships, grants, and employer-sponsored programs, to minimize reliance on loans.

Long-term Implications for Grad School Landscape

The student loan forgiveness plan may also have long-term implications for the grad school landscape. As more individuals pursue advanced degrees, institutions may need to adapt their programs to meet the changing demands of the workforce. This could lead to the development of more specialized, industry-focused curricula, as well as increased emphasis on experiential learning and career services. Furthermore, the plan might encourage grad schools to reevaluate their tuition structures, potentially leading to more affordable options or income-share agreements. However, it's essential for institutions to balance accessibility with academic rigor, ensuring that the quality of education remains high despite the influx of new students. By carefully navigating these challenges, grad schools can capitalize on the opportunities presented by the forgiveness plan, ultimately fostering a more educated and skilled workforce.

Unlock NP Student Loan Forgiveness: Working in HPSA Areas Guide

You may want to see also

Frequently asked questions

Yes, Biden's student loan forgiveness plan includes borrowers with federal student loans for both undergraduate and graduate degrees, as long as they meet the income eligibility criteria.

Yes, federal student loans for graduate degrees, such as Master’s and PhD programs, are eligible for forgiveness under Biden’s plan, provided the borrower’s income falls within the specified limits.

No, the amount of forgiveness does not differ based on the degree type. Eligible borrowers can receive up to $10,000 in forgiveness, or up to $20,000 if they received a Pell Grant, regardless of whether the loans were for undergraduate or graduate studies.