The question of whether the president has the authority to forgive student debt has sparked intense debate and legal scrutiny in recent years, particularly as the burden of student loans continues to weigh heavily on millions of Americans. Advocates argue that executive action under the Higher Education Act could allow the president to cancel debt without congressional approval, citing the Department of Education’s authority to modify or waive federal loans. However, opponents contend that such a move would overstep constitutional limits, require legislative action, and raise concerns about fairness, economic impact, and the long-term sustainability of higher education financing. As the issue remains unresolved, it continues to intersect with broader discussions about income inequality, racial disparities, and the role of government in addressing systemic financial challenges.

| Characteristics | Values |

|---|---|

| Legal Authority | The president's authority to forgive student debt is debated. Some argue it falls under the Higher Education Act's executive powers, while others believe it requires congressional approval. |

| Current Status | As of October 2023, President Biden's student debt relief plan (up to $20,000 per borrower) is blocked by the Supreme Court's June 2023 ruling in Biden v. Nebraska, which deemed the plan unconstitutional. |

| Alternative Actions | The Biden administration has pursued other debt relief measures, such as: - Income-Driven Repayment (IDR) Account Adjustment (fixing past errors in IDR counts). - Public Service Loan Forgiveness (PSLF) reforms (expanding eligibility and streamlining the process). - Targeted loan cancellations for specific groups (e.g., defrauded borrowers under the Borrower Defense rule). |

| Congressional Role | Congress retains primary authority over student loan policy. Legislation like the Student Loan Forgiveness for Frontline Health Workers Act or broader forgiveness bills would require congressional approval. |

| Political Debate | Forgiveness is highly polarized, with supporters citing economic relief and opponents raising concerns about cost, fairness, and inflation. |

| Economic Impact | Estimates vary; widespread forgiveness could stimulate the economy but also increase federal debt. Targeted relief is seen as more fiscally manageable. |

| Public Opinion | Polls show divided support, with younger and lower-income Americans generally favoring forgiveness, while older and higher-income groups are more skeptical. |

| Legal Challenges | Future executive actions on debt relief are likely to face legal challenges, as seen with the Supreme Court's rejection of Biden's 2022 plan. |

Explore related products

What You'll Learn

- Legal Authority: Does the president have the power to cancel student debt without Congress

- Executive Order Limits: Can debt forgiveness be achieved through executive action alone

- Economic Impact: How would widespread student debt cancellation affect the economy

- Political Implications: What are the potential political consequences of such a decision

- Moral and Ethical Debate: Is forgiving student debt fair to those who paid their loans

![]()

Legal Authority: Does the president have the power to cancel student debt without Congress?

The question of whether the president can unilaterally cancel student debt hinges on the interpretation of existing laws, particularly the Higher Education Act of 1965. Section 432(a) of this act grants the Secretary of Education the authority to "enforce, pay, compromise, waive, or release any right, title, claim, lien, or demand" related to federal student loans. Proponents of executive action argue that this provision provides a legal basis for broad debt cancellation, as it allows for the modification of loan terms under certain circumstances. However, critics contend that this authority is limited to individual cases or specific programs, not mass forgiveness without congressional approval.

Analyzing the legal landscape reveals a complex interplay between executive power and legislative intent. The Supreme Court’s 2023 ruling in *Biden v. Nebraska* struck down the Biden administration’s attempt to cancel up to $20,000 in student debt per borrower under the HEROES Act, citing the "major questions doctrine," which requires explicit congressional authorization for actions of significant economic or political importance. This decision underscores the judiciary’s skepticism toward expansive interpretations of executive authority in this area. While the president may have limited discretion to modify loan terms for specific groups (e.g., public service workers or defrauded students), widespread cancellation remains legally contentious without congressional involvement.

A comparative analysis of past executive actions offers insight into the boundaries of presidential power. For instance, the Trump administration used the HEROES Act to pause student loan payments during the COVID-19 pandemic, a move widely accepted as within the president’s authority. However, this action was temporary and did not involve debt cancellation. In contrast, the Biden administration’s attempt at broad forgiveness was framed as a permanent solution, crossing into territory traditionally reserved for legislative action. This distinction highlights the importance of scale and permanence in determining the legality of such actions.

Practically, borrowers seeking relief should focus on existing programs rather than relying on potential executive action. Income-Driven Repayment (IDR) plans, Public Service Loan Forgiveness (PSLF), and borrower defense to repayment are established pathways for reducing or eliminating debt. For example, IDR plans cap monthly payments at 10-20% of discretionary income, with forgiveness after 20-25 years. PSLF offers tax-free forgiveness after 120 qualifying payments for those in eligible public service jobs. Borrowers should also monitor legislative developments, as Congress remains the most direct route for comprehensive student debt reform.

In conclusion, while the president possesses some authority to modify student loan terms, the power to cancel debt on a large scale without Congress is legally uncertain and politically fraught. Borrowers should prioritize leveraging existing programs and advocating for legislative solutions rather than banking on executive action. The debate over presidential authority in this area is likely to persist, but for now, the law favors a more constrained interpretation of executive power.

Biden Student Loan Forgiveness: Step-by-Step Application Guide for Borrowers

You may want to see also

Explore related products

![]()

Executive Order Limits: Can debt forgiveness be achieved through executive action alone?

The authority to forgive student debt through executive action alone is a contentious issue, hinging on the interpretation of the Higher Education Act of 1965. Section 432(a) of this act grants the Secretary of Education the power to "enforce, pay, compromise, waive, or release any right, title, claim, lien, or demand" related to federal student loans. Proponents argue this language provides a legal basis for broad executive action, while critics contend it was intended for administrative adjustments, not mass forgiveness. This debate underscores the limits of executive power in reshaping policy without congressional approval.

Consider the practical implications of relying solely on executive action. An executive order forgiving student debt could face immediate legal challenges, potentially delaying implementation for years. For instance, the Biden administration’s 2022 attempt to forgive up to $20,000 in student debt was blocked by the Supreme Court in *Biden v. Nebraska* (2023), which ruled the administration exceeded its authority under the HEROES Act. This case highlights the risk of relying on executive action without a clear statutory mandate, as courts may interpret such actions as overreach.

From a strategic perspective, pursuing debt forgiveness through executive action alone ignores the broader political and economic context. Congress holds the power of the purse and could undermine an executive order by refusing to fund its implementation or passing legislation to reverse it. Additionally, executive actions are inherently fragile, as they can be rescinded by future administrations. For example, President Trump rolled back several Obama-era executive actions, demonstrating the transient nature of such policies. This instability makes executive action a risky foundation for long-term policy change.

A more effective approach might involve a combination of executive action and legislative efforts. The president could use executive authority to provide temporary relief, such as pausing loan payments or reducing interest rates, while simultaneously pushing Congress to pass comprehensive student debt reform. This dual strategy leverages the immediacy of executive action while seeking the durability of legislative solutions. For instance, the CARES Act of 2020 included a provision pausing federal student loan payments, a measure later extended through executive action, showcasing how these tools can complement each other.

In conclusion, while executive action offers a tempting shortcut for achieving student debt forgiveness, its limitations are significant. Legal challenges, political pushback, and the risk of reversal all undermine its effectiveness as a standalone solution. Policymakers must balance the urgency of the student debt crisis with the need for sustainable, legally sound reforms. Relying exclusively on executive action may provide short-term relief but risks long-term instability, making it a flawed strategy for addressing a systemic issue.

Do Student Loans Disappear When You Die? What You Need to Know

You may want to see also

Explore related products

![]()

Economic Impact: How would widespread student debt cancellation affect the economy?

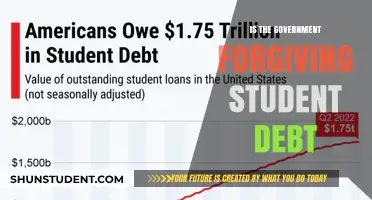

Widespread student debt cancellation would inject billions of dollars into the economy by freeing up disposable income for millions of borrowers. Currently, over 43 million Americans hold a combined $1.7 trillion in student debt, with average monthly payments ranging from $200 to $300. Eliminating this financial burden would allow individuals to redirect funds toward consumer spending, savings, or investments. For instance, a borrower with a $30,000 debt at 6% interest could save approximately $300 per month, potentially boosting retail sales, housing markets, or retirement accounts. This increased spending power could stimulate economic growth, particularly in sectors like automotive, travel, and small businesses, which rely heavily on consumer demand.

However, the economic impact isn’t uniformly positive. Critics argue that debt cancellation could lead to inflationary pressures if spending surges without a corresponding increase in supply. Additionally, the policy’s cost—estimated at $1 trillion or more—would likely be funded through deficit spending or tax increases, which could dampen economic activity in other areas. For example, higher taxes on high-income earners or corporations might reduce investment or hiring, offsetting some of the stimulus from debt relief. Policymakers would need to carefully balance these trade-offs to avoid unintended consequences, such as rising prices or reduced business confidence.

Another consideration is the distributional impact of debt cancellation. While it would benefit individual borrowers, the policy disproportionately favors higher-income households, as they hold a larger share of student debt due to advanced degrees. For instance, the top 25% of earners hold nearly 50% of all student debt. To maximize economic equity, targeted relief—such as capping cancellation at $10,000 or $50,000 per borrower—could be paired with reforms like income-driven repayment plans or increased funding for public colleges. This approach would ensure that relief reaches those most in need while minimizing moral hazard and fiscal strain.

Finally, the long-term economic effects depend on how borrowers use their newfound financial freedom. If individuals invest in education, entrepreneurship, or homeownership, debt cancellation could enhance productivity and wealth accumulation. For example, a borrower relieved of $50,000 in debt might start a business, creating jobs and contributing to GDP growth. Conversely, if funds are spent on non-essential goods or services, the economic benefits may be short-lived. Pairing debt relief with financial literacy programs or incentives for savings could amplify its positive impact, ensuring that borrowers make choices that strengthen both their own financial health and the broader economy.

Student Loan Forgiveness: Which Loans Qualify for Debt Relief?

You may want to see also

Explore related products

$14.95 $14.95

![]()

Political Implications: What are the potential political consequences of such a decision?

The decision to forgive student debt carries profound political implications, reshaping public perception, electoral dynamics, and policy debates. At its core, such a move would signal a bold assertion of executive power, potentially redefining the role of the presidency in addressing systemic economic issues. This act could galvanize support among younger, debt-burdened voters while alienating fiscal conservatives, creating a polarized landscape that reverberates across party lines.

Consider the immediate electoral consequences. For Democrats, forgiving student debt could solidify loyalty among progressive and youth demographics, groups critical to their coalition. However, it risks alienating moderate voters wary of perceived government overreach or concerned about the cost. Republicans, meanwhile, could exploit the decision to paint the administration as fiscally irresponsible, leveraging it to rally their base around themes of limited government and personal accountability. The political calculus here is delicate: the short-term gain in voter enthusiasm must be weighed against the long-term risk of backlash.

Beyond elections, the decision would reshape policy discourse, setting a precedent for executive action on economic inequality. Advocates would hail it as a transformative step toward addressing the student debt crisis, while critics would decry it as an unconstitutional overstep. This polarization would likely spill into other policy areas, with future administrations potentially emulating or rejecting this model based on their ideological leanings. The ripple effect could extend to debates on healthcare, taxation, and social welfare, fundamentally altering the boundaries of federal intervention.

Practically, the decision’s implementation would require strategic communication to mitigate political fallout. Framing forgiveness as targeted relief for low- and middle-income borrowers, rather than a blanket handout, could soften opposition. Pairing it with reforms to prevent future debt accumulation—such as capping interest rates or expanding Pell Grants—would demonstrate a commitment to long-term solutions. Without such nuance, the policy risks being perceived as a political gambit rather than a principled reform.

Ultimately, the political consequences of forgiving student debt hinge on execution and context. A well-crafted, equitable plan could redefine the president’s legacy, while a haphazard approach could become a liability. The decision is not merely about debt relief; it’s a test of leadership, a referendum on the government’s role in addressing generational inequities, and a catalyst for broader political realignment.

Marriott's Student Loan Forgiveness: What Employees Need to Know

You may want to see also

Explore related products

![]()

Moral and Ethical Debate: Is forgiving student debt fair to those who paid their loans?

The debate over student debt forgiveness often hinges on a central question: Is it fair to those who have already repaid their loans? This moral and ethical dilemma pits the principle of individual responsibility against the broader societal goal of economic equity. For those who sacrificed to pay off their debts, the idea of forgiving others’ obligations can feel like a betrayal of their hard work. Yet, proponents argue that systemic issues in higher education financing justify a collective solution, even if it means unsettling those who played by the rules.

Consider the case of Sarah, a 45-year-old nurse who worked multiple jobs for a decade to repay $80,000 in student loans. For her, forgiveness feels like a slap in the face—a reward for those who didn’t prioritize repayment as she did. This perspective highlights the tension between fairness as equity (ensuring equal outcomes) and fairness as justice (rewarding effort and sacrifice). Critics argue that forgiving debt without addressing the root causes of rising tuition costs merely shifts the burden, leaving future generations vulnerable to the same cycle.

However, the argument for forgiveness isn’t solely about individual relief but about correcting systemic failures. Since the 1980s, tuition costs have risen over 200%, far outpacing inflation and wage growth. Many borrowers, particularly those from low-income backgrounds, were sold the idea that a degree guaranteed financial stability, only to graduate into a recession or stagnant job market. From this view, forgiveness isn’t about penalizing responsible payers but about acknowledging a broken system that trapped millions in unmanageable debt.

A middle ground might involve targeted relief rather than blanket forgiveness. For instance, capping monthly payments at 8–10% of discretionary income, as proposed in income-driven repayment plans, could ease the burden without erasing debts entirely. Additionally, refunding payments made by those who have already repaid their loans could address feelings of inequity. Such measures would balance accountability with compassion, recognizing both the sacrifices of past borrowers and the struggles of current ones.

Ultimately, the fairness debate isn’t just about dollars and cents but about values. Do we prioritize rewarding individual effort, or do we seek to rectify systemic injustices? There’s no one-size-fits-all answer, but any solution must grapple with these competing principles. Forgiving student debt could be a step toward a more equitable future, but it must be paired with reforms to prevent history from repeating itself. Otherwise, the cycle of debt—and the moral dilemmas it creates—will persist.

County Jobs and Student Loan Forgiveness: What You Need to Know

You may want to see also

Frequently asked questions

The President's authority to forgive student debt unilaterally is a subject of debate. While the Higher Education Act grants the Secretary of Education the power to modify or waive federal student loans, the extent of this authority for broad-scale forgiveness is unclear and has been challenged in court.

Yes, President Biden announced a student debt relief plan in 2022, aiming to forgive up to $20,000 for eligible borrowers. However, the plan was blocked by the Supreme Court in 2023, which ruled that the administration overstepped its authority.

Legal challenges often center on whether the President or the Department of Education has the statutory authority to forgive debt on a large scale. Critics argue that such actions require congressional approval, while supporters point to existing laws like the Higher Education Act.

No, the President does not have the authority to forgive private student loans, as these are not federally held. Only federal student loans are subject to potential executive action or legislative forgiveness.

Alternatives include congressional legislation to forgive debt, expanding income-driven repayment plans, improving loan forgiveness programs like Public Service Loan Forgiveness (PSLF), and addressing the root causes of rising tuition costs.