When deciding whether to pay the interest first on a student loan, it’s essential to consider your financial goals and the loan’s structure. Paying interest early can prevent it from capitalizing, which occurs when unpaid interest is added to the principal balance, increasing the total amount owed over time. This approach is particularly beneficial for unsubsidized loans, where interest accrues while you’re in school or during grace periods. However, if you’re in a tight financial situation, prioritizing minimum payments or focusing on higher-interest debt might be more practical. Ultimately, paying interest first can save you money in the long run, but it’s crucial to weigh this against your current financial stability and other financial priorities.

| Characteristics | Values |

|---|---|

| Reduces Loan Principal Faster | Paying interest first prevents it from capitalizing, lowering overall debt. |

| Saves Money on Total Interest | Early interest payments reduce the total interest paid over the loan term. |

| Prevents Capitalization | Unpaid interest doesn’t get added to the principal, avoiding higher costs. |

| Best for High-Interest Loans | More effective for loans with higher interest rates (e.g., private loans). |

| Requires Extra Payments | Requires paying more than the minimum monthly payment to target interest. |

| May Not Be Feasible for All | Budget constraints may limit ability to pay extra toward interest. |

| Depends on Loan Type | Federal loans may have subsidies or grace periods affecting strategy. |

| Long-Term Financial Benefit | Reduces long-term debt burden and improves financial health. |

| Requires Discipline | Consistent extra payments are needed to maximize benefits. |

| Alternative Strategies Exist | Other options include refinancing or income-driven repayment plans. |

Explore related products

What You'll Learn

![]()

Pros of paying interest first

Paying interest first on your student loan can be a strategic financial move, particularly during periods of deferment or forbearance. One of the primary pros of paying interest first is that it prevents interest capitalization, which occurs when unpaid interest is added to the principal balance of your loan. By paying the interest as it accrues, you keep the principal amount from growing, ultimately saving money over the life of the loan. This is especially beneficial for unsubsidized loans, where interest begins accruing immediately after disbursement.

Another advantage of paying interest first is that it reduces the overall cost of the loan. When interest capitalizes, you end up paying interest on a larger principal balance, which increases the total amount you owe. By addressing the interest early, you minimize the compounding effect, making your future payments more manageable. This approach is particularly useful if you anticipate a long repayment period or if you’re in a financial situation where you cannot yet afford full monthly payments.

Paying interest first also helps maintain a lower loan balance, which can improve your debt-to-income ratio. A lower loan balance can positively impact your credit score and financial health, as it demonstrates responsible financial management. This can be advantageous if you plan to apply for other forms of credit, such as a mortgage or car loan, in the future. Keeping your loan balance in check by paying interest first ensures you’re not burdened with unnecessary debt.

Additionally, paying interest first provides flexibility and peace of mind. If you’re in a deferment or forbearance period, paying the interest allows you to avoid a financial shock once repayment begins. You won’t be faced with a significantly higher balance or larger monthly payments due to capitalized interest. This proactive approach can reduce stress and make it easier to transition into full repayment mode when the time comes.

Lastly, paying interest first is a cost-effective strategy for borrowers who have extra funds but are not yet ready to make full payments. Even small interest payments can make a substantial difference over time. It’s a way to stay ahead of your debt without committing to a full repayment plan, making it an ideal option for recent graduates or those in low-income periods. By focusing on interest first, you’re investing in your long-term financial stability and reducing the burden of student loans.

Employers' Guide to Supporting Employees' Student Debt

You may want to see also

Explore related products

![]()

Cons of delaying interest payments

Delaying interest payments on your student loan might seem like a way to free up cash in the short term, but it comes with significant drawbacks that can impact your financial health in the long run. One of the primary cons is the accumulation of interest over time. When you postpone paying interest, it continues to accrue and is often capitalized, meaning it is added to the principal balance of your loan. This results in a larger overall debt, as you end up paying interest on a higher amount than you originally borrowed. Over time, this can substantially increase the total cost of your loan, making it more expensive to repay.

Another major disadvantage is the long-term financial burden that delaying interest payments creates. By not addressing the interest early on, you extend the life of your loan and increase the total amount you owe. This can limit your financial flexibility, making it harder to save for other goals like buying a home, investing, or building an emergency fund. Additionally, a higher loan balance can negatively impact your debt-to-income ratio, potentially affecting your ability to qualify for other types of credit, such as mortgages or car loans.

Delaying interest payments can also hinder your progress toward financial freedom. Instead of chipping away at your debt, you’re allowing it to grow, which can feel demoralizing and overwhelming. This can lead to a cycle of perpetual debt, where you’re constantly paying more than you initially borrowed without making significant headway. Paying interest first, on the other hand, helps reduce the principal balance faster, allowing you to become debt-free sooner and save money in the process.

Furthermore, delaying interest payments can limit your options for loan forgiveness or repayment plans. Many income-driven repayment plans or loan forgiveness programs require consistent payments, including interest, to qualify. By falling behind on interest, you may lose eligibility for these programs, which could have otherwise provided relief or reduced your overall debt burden. This lack of flexibility can leave you with fewer tools to manage your student loans effectively.

Lastly, delaying interest payments can have a negative impact on your credit score. Accumulated interest and a growing loan balance can increase your credit utilization ratio, which is a key factor in determining your credit score. A higher credit utilization ratio can lower your score, making it harder to secure favorable terms on future loans or credit cards. Paying interest on time, however, demonstrates financial responsibility and helps maintain a healthy credit profile. In summary, while delaying interest payments might provide temporary relief, the long-term consequences far outweigh the short-term benefits.

Student Accounts: Paying for Permits at Montclair

You may want to see also

Explore related products

![]()

Impact on loan principal balance

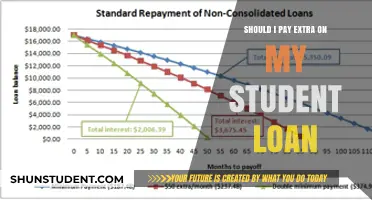

When deciding whether to pay interest first on a student loan, it’s crucial to understand how this choice directly impacts the loan principal balance. The principal is the original amount borrowed, and reducing it faster can save you money in the long run. If you pay interest first, especially during periods like the grace period after graduation or while in school, you prevent interest from capitalizing and being added to the principal. This means the principal remains unchanged, and future interest calculations are based on the original loan amount, not an inflated one. By addressing interest early, you avoid the compounding effect, which can significantly increase the total cost of the loan over time.

Conversely, if you allow interest to accrue without paying it, it will eventually capitalize and become part of the principal balance. This increases the total amount you owe, and subsequent interest charges will be calculated on this higher principal. For example, if you have a $10,000 loan with 5% annual interest and let $500 in interest accrue, your principal will grow to $10,500. Future interest will then be calculated on $10,500 instead of $10,000, leading to higher overall repayment costs. Paying interest first prevents this increase in the principal, keeping the loan balance as low as possible.

Another key impact on the principal balance is the speed at which you can pay down the loan. When you prioritize interest payments, you ensure that any extra payments you make later go directly toward reducing the principal. This accelerates the repayment process because more of your money is applied to the core debt rather than accumulating interest. For instance, if you pay off $500 in interest early, your future payments can immediately target the $10,000 principal instead of chipping away at a growing balance due to unpaid interest.

Additionally, paying interest first can provide psychological and financial clarity. By keeping the principal stable, you have a clear target for repayment and can better plan your budget. It also reduces the risk of payment shock later, as the loan balance remains predictable. This approach is particularly beneficial for long-term loans, where the effects of compounding interest can be most pronounced.

In summary, paying interest first on a student loan directly protects the principal balance from increasing due to capitalization. It prevents compounding interest from inflating the total debt, ensures that future payments are more effective in reducing the principal, and provides a clearer path to repayment. While it may require more immediate financial discipline, the long-term savings and reduced loan balance make it a strategic choice for managing student loan debt effectively.

Student Loan Payment Strategies: What If I've Been Paying?

You may want to see also

Explore related products

![]()

Strategies for minimizing total interest

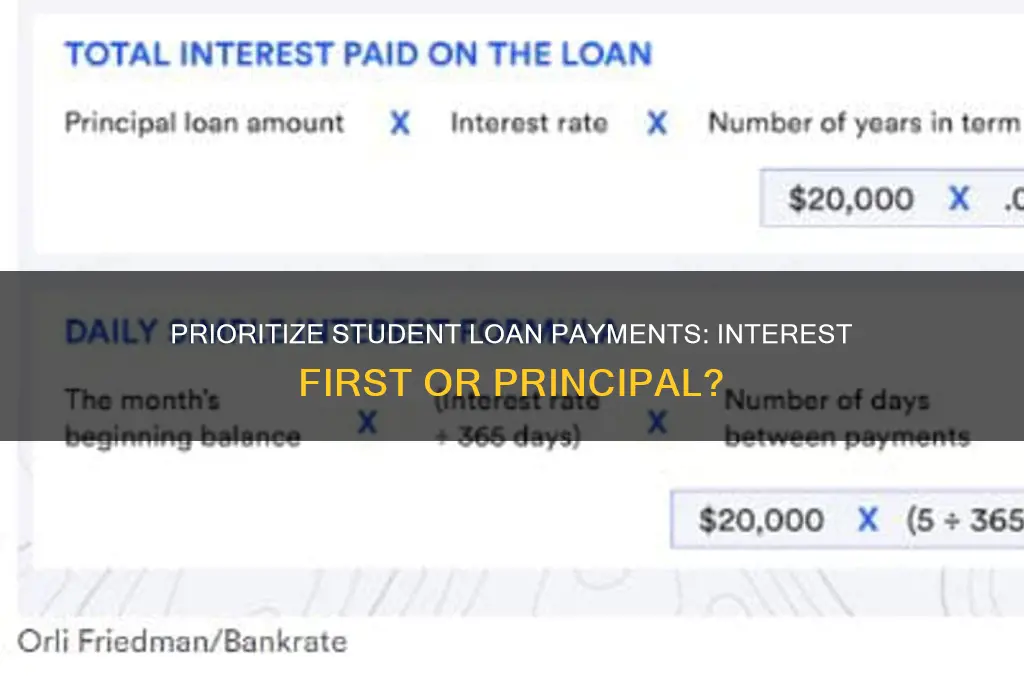

When it comes to minimizing the total interest on your student loan, paying interest first can be a strategic move, especially during the grace period or while the loan is in deferment. By making interest payments early, you prevent the interest from capitalizing, which means it won't be added to the principal balance. This is crucial because once interest capitalizes, you end up paying interest on the interest, significantly increasing the total cost of the loan. For example, if you have a $30,000 loan with a 6% interest rate, paying the accruing interest during the grace period can save you hundreds or even thousands of dollars over the life of the loan.

One effective strategy is to make interest-only payments during periods when full payments are not required. This is particularly beneficial if your loan is unsubsidized, as interest accrues even while you’re in school or during grace periods. By paying the interest as it accrues, you keep the loan balance from growing. For instance, if your monthly accruing interest is $150, paying this amount regularly ensures that the principal remains unchanged, making it easier to manage once repayment begins. This approach requires discipline but can yield substantial long-term savings.

Another strategy is to pay more than the accruing interest whenever possible. Even small additional payments can reduce the principal balance faster, which in turn reduces the amount of interest that accrues over time. For example, if your monthly interest is $100, consider paying $150 or $200. This not only covers the interest but also chips away at the principal. Over time, this method can shorten the loan term and save you a significant amount in interest. Use any extra income, such as bonuses or tax refunds, to make these additional payments.

Refinancing your student loan is another powerful strategy to minimize total interest, especially if you have a high interest rate. Refinancing involves taking out a new loan with a lower interest rate to pay off the existing loan. This can reduce your monthly payments and the total interest paid over the life of the loan. However, refinancing federal loans means losing access to federal benefits like income-driven repayment plans and loan forgiveness programs, so weigh the pros and cons carefully. If you have a stable income and good credit score, refinancing could be a smart financial move.

Lastly, enroll in autopay to ensure timely payments and take advantage of any interest rate reductions offered by lenders. Many loan servicers offer a small interest rate discount (usually 0.25%) for setting up automatic payments. While this may seem minor, it can add up over time and reduce the total interest paid. Additionally, autopay eliminates the risk of late payments, which can harm your credit score and result in additional fees. Combining autopay with other strategies like paying extra toward the principal can maximize your interest savings.

By implementing these strategies—paying interest first, making extra payments, refinancing when beneficial, and using autopay—you can effectively minimize the total interest on your student loan. Each approach requires careful planning and discipline, but the long-term savings make the effort worthwhile. Start early and stay consistent to achieve the best results.

Dental Care: Who Pays at University?

You may want to see also

Explore related products

![]()

When to prioritize other debts instead

When deciding whether to prioritize other debts over paying the interest first on your student loans, it’s essential to consider the interest rates and terms of your other financial obligations. If you have high-interest debts, such as credit card balances with APRs of 18% or more, these should often take precedence. Paying off high-interest debt first can save you significant money in the long run, as the compounding interest on these accounts grows much faster than the relatively lower rates on most student loans. Focus on eliminating these debts aggressively while making minimum payments on your student loans to avoid default.

Another scenario where prioritizing other debts makes sense is when you have outstanding medical bills or personal loans with strict repayment terms. Medical debt, for example, can often be sent to collections quickly, damaging your credit score and leading to additional fees. Similarly, personal loans with high monthly payments or short repayment periods can strain your budget. Addressing these debts first ensures you avoid penalties, maintain your creditworthiness, and free up cash flow for other financial goals, including eventually tackling your student loans more aggressively.

If you have debts with variable interest rates, such as certain credit cards or private loans, it’s wise to prioritize them, especially in a rising interest rate environment. Variable rates can increase unexpectedly, making these debts more expensive over time. By paying them down first, you reduce the risk of being caught off guard by higher monthly payments. Meanwhile, most federal student loans have fixed interest rates, providing more predictability and flexibility in your repayment strategy.

Prioritizing other debts also becomes crucial when you’re working toward specific financial milestones, such as saving for an emergency fund or a down payment on a home. While paying student loan interest is important, having a safety net or achieving homeownership can provide greater long-term stability and financial security. Allocate your resources to these goals first, ensuring you’re prepared for unexpected expenses or major life events before directing extra funds toward student loans.

Finally, if you’re enrolled in an income-driven repayment plan or pursuing student loan forgiveness, it may make sense to prioritize other debts. These programs often cap your monthly payments based on your income and forgive remaining balances after a certain period. In such cases, paying extra toward student loans may not yield significant benefits, as the forgiven amount could be taxable. Instead, focus on clearing higher-priority debts while staying current on your student loan payments to maximize your overall financial health.

Student Loans for Car Insurance: Is It Possible?

You may want to see also

Frequently asked questions

Yes, paying the interest first can prevent it from capitalizing and increasing the overall balance of your loan, saving you money in the long run.

Unpaid interest on unsubsidized loans will capitalize, meaning it’s added to the principal balance, causing you to pay interest on a larger amount later.

Paying extra toward the principal reduces the overall loan balance faster, but paying interest first prevents capitalization and can be more beneficial if your loan is in deferment or forbearance.

Make interest payments while in school (if possible), pay more than the minimum amount due, and consider refinancing for a lower interest rate if eligible.