Deciding whether to let student loans collect interest until forgiveness is a complex financial decision that hinges on several factors, including the type of loan, repayment plan, and individual financial circumstances. For borrowers with federal loans eligible for income-driven repayment (IDR) plans or Public Service Loan Forgiveness (PSLF), allowing interest to accrue might be a strategic move, as forgiveness programs can discharge remaining balances after a set period. However, this approach can significantly increase the total cost of the loan, especially for those with high balances or long repayment terms. Conversely, paying down interest or making extra payments can reduce the overall debt burden but may not align with long-term forgiveness goals. Ultimately, the decision requires careful consideration of one’s career trajectory, income stability, and tolerance for debt, often necessitating professional financial advice to weigh the pros and cons effectively.

| Characteristics | Values |

|---|---|

| Interest Accrual | Interest continues to accrue on most federal student loans (e.g., Direct Loans) even if payments are paused. |

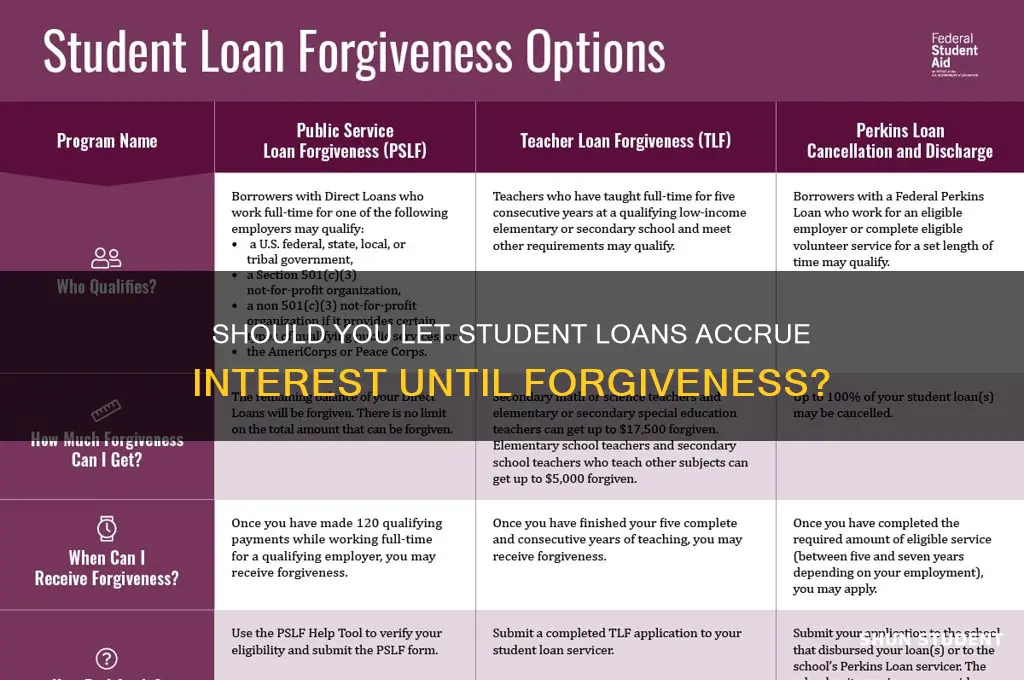

| Loan Forgiveness Programs | Programs like Public Service Loan Forgiveness (PSLF) and Income-Driven Repayment (IDR) plans forgive remaining balances after 10–25 years of qualifying payments. |

| Capitalization of Interest | Unpaid interest may capitalize (added to the principal balance), increasing the total loan amount and future interest costs. |

| Loan Type Impact | Subsidized loans do not accrue interest while in school, deferment, or grace periods; unsubsidized loans do. |

| Repayment Strategy | Paying interest during deferment or forbearance prevents balance growth but may not be feasible for all borrowers. |

| Tax Implications | Forgiven amounts may be taxable as income (except for PSLF and IDR forgiveness under current law). |

| Financial Trade-Off | Allowing interest to accrue increases total debt but may be offset by eventual forgiveness, depending on the program. |

| Eligibility Requirements | Forgiveness programs require consistent payments, specific employment (e.g., PSLF), or income-driven plans. |

| Time Horizon | Forgiveness typically takes 10–25 years, during which interest accrual can significantly impact total debt. |

| Risk of Non-Forgiveness | If forgiveness criteria are not met, borrowers are responsible for the full balance, including accrued interest. |

| Current Policy Landscape | Recent changes (e.g., IDR Account Adjustment) may reduce interest burdens for some borrowers. |

| Opportunity Cost | Paying interest reduces disposable income but avoids long-term debt growth. |

| Loan Servicer Guidance | Borrowers should consult servicers to understand interest accrual and forgiveness eligibility. |

Explore related products

What You'll Learn

- Pros of Delaying Payments: Allows cash flow flexibility, potential for forgiveness, but risks higher balances

- Cons of Accrued Interest: Increases total debt, prolongs repayment, limits financial freedom post-forgiveness

- Income-Driven Repayment Plans: Caps payments based on income, reduces monthly burden, extends forgiveness timeline

- Public Service Loan Forgiveness: Requires 120 qualifying payments, forgives remaining balance tax-free, interest accrues

- Strategic Financial Planning: Invest extra funds, prioritize high-interest debt, balance savings vs. loan repayment

![]()

Pros of Delaying Payments: Allows cash flow flexibility, potential for forgiveness, but risks higher balances

Delaying student loan payments can free up immediate cash flow, a lifeline for recent graduates navigating entry-level salaries or unpredictable freelance income. By opting for forbearance or income-driven repayment plans, borrowers can redirect funds toward essentials like rent, groceries, or emergency savings. This financial breathing room allows individuals to stabilize their budgets, avoid high-interest debt like credit cards, and even invest in career-boosting certifications or tools. For instance, a borrower with $30,000 in loans at 6% interest might save $200–$300 monthly by delaying payments, funds that could instead cover professional development courses or a reliable vehicle for commuting.

However, the allure of forgiveness programs like Public Service Loan Forgiveness (PSLF) or income-driven repayment forgiveness complicates this strategy. Borrowers in qualifying public service roles or those with low incomes relative to their debt may eventually have their balances forgiven after 10–25 years. Delaying payments while working toward these milestones can maximize the forgiven amount, effectively shifting the burden of interest accumulation onto the government. For example, a teacher earning $45,000 annually with $50,000 in loans might pay only $100/month under an income-driven plan, accruing interest but positioning themselves for full forgiveness after 10 years of service.

Yet, this approach carries significant risks. Interest capitalization—when unpaid interest is added to the principal balance—can inflate the total debt by thousands of dollars. A borrower with $40,000 in loans at 7% interest who delays payments for 5 years could see their balance grow to $54,000, even without making a single payment. This higher balance not only increases the eventual forgiveness amount but also prolongs repayment terms if the borrower switches to a standard plan later.

To mitigate these risks, borrowers should adopt a strategic mindset. First, calculate the break-even point where delayed payments and potential forgiveness outweigh the cost of immediate repayment. Tools like the Department of Education’s Loan Simulator can model scenarios based on income, family size, and loan type. Second, prioritize forgiveness-eligible plans like PSLF or income-driven repayment, ensuring all payments (even $0 ones) count toward the required 120 or 300 months. Finally, consider partial payments during deferment periods to curb interest growth without sacrificing cash flow entirely. For instance, paying $50–$100 monthly toward accruing interest can prevent balance bloat while maintaining flexibility.

In essence, delaying payments offers a tactical advantage for those confident in their eligibility for forgiveness programs or facing short-term financial strain. However, it demands vigilance against interest capitalization and a long-term commitment to program requirements. Borrowers must weigh their current liquidity needs against future debt obligations, treating this strategy as a calculated risk rather than a passive solution.

Can Private Student Loans Be Forgiven? Exploring Your Options

You may want to see also

Explore related products

![]()

Cons of Accrued Interest: Increases total debt, prolongs repayment, limits financial freedom post-forgiveness

Accrued interest on student loans is a silent adversary, compounding over time to inflate the total debt burden. For instance, a $30,000 loan at a 6% interest rate, left unpaid for 10 years, can balloon to nearly $51,000 due to compounding. This isn’t just a number—it’s a financial anchor that drags down borrowers, making the original principal seem like a distant memory. Every dollar added to the principal through interest is a dollar that wasn’t spent on building wealth, investing, or achieving financial milestones.

Prolonged repayment periods are another consequence of letting interest accrue unchecked. Consider a borrower on an income-driven repayment plan, where monthly payments are capped at a percentage of discretionary income. If interest outpaces these payments, the loan balance grows, potentially resetting the repayment clock. For example, a borrower on a 20-year forgiveness plan might find themselves still in debt after two decades if accrued interest keeps the balance above the original principal. This delays the day when they can finally be debt-free, trapping them in a cycle of repayment long after their peers have moved on.

The third casualty of accrued interest is financial freedom post-forgiveness. Even if a borrower qualifies for loan forgiveness after 20 or 25 years, the forgiven amount may be treated as taxable income. A larger balance due to accrued interest means a larger tax liability, which can be a five-figure bill for some. For example, a $70,000 forgiven loan could result in a $15,000 tax obligation, depending on the borrower’s tax bracket. This unexpected expense can derail financial plans, forcing borrowers to dip into savings or take on new debt just as they thought they were free.

To mitigate these risks, borrowers should prioritize strategies to minimize interest accrual. Making interest-only payments during deferment or forbearance periods can prevent capitalization, keeping the balance in check. For those in income-driven plans, submitting annual recertification paperwork on time ensures payments are accurately adjusted to income, reducing the gap between payments and interest. Additionally, exploring refinancing options with lower interest rates can be a proactive step, though it’s crucial to weigh the loss of federal benefits like forgiveness programs. Ignoring accrued interest may seem painless in the short term, but its long-term consequences are anything but.

Michigan's Tax Treatment of Student Loan Forgiveness: What You Need to Know

You may want to see also

Explore related products

![]()

Income-Driven Repayment Plans: Caps payments based on income, reduces monthly burden, extends forgiveness timeline

Income-driven repayment (IDR) plans are a lifeline for borrowers juggling student loans and tight budgets. By capping monthly payments at a percentage of discretionary income (typically 10-20%), these plans offer immediate relief. For instance, a borrower earning $40,000 annually with $50,000 in loans might see payments drop from $500 to $200 under an IDR plan. This reduction frees up cash for essentials like rent, groceries, or emergencies, making loan management more sustainable. However, this benefit comes with a trade-off: lower payments mean more interest accrues over time, potentially increasing the total cost of the loan.

Consider the mechanics of IDR plans to understand their long-term implications. Under these plans, any unpaid interest may capitalize, adding to the principal balance. For example, if a borrower’s monthly payment doesn’t cover the accruing interest, the difference is added to the loan, causing the balance to grow. This can create a snowball effect, especially for borrowers with high-interest rates or large loan amounts. Yet, IDR plans also offer a safety net: after 20-25 years of qualifying payments, any remaining balance is forgiven, though the forgiven amount may be taxable as income.

The decision to enroll in an IDR plan hinges on individual financial goals and circumstances. For borrowers pursuing Public Service Loan Forgiveness (PSLF), IDR plans are often the best route, as they minimize payments while maximizing forgiveness eligibility. For others, the extended repayment timeline and potential tax liability on forgiven debt may outweigh the benefits. A borrower with a stable, high-income career might opt for a standard repayment plan to avoid interest accumulation, while someone in a low-paying field could benefit from the lower payments and eventual forgiveness.

Practical tips can help borrowers navigate IDR plans effectively. First, recertify income annually to ensure payments remain aligned with earnings. Missing recertification can lead to payment spikes. Second, explore tax strategies to minimize the impact of forgiven debt, such as planning for a lower income year when forgiveness occurs. Third, track payments meticulously, as errors in counting qualifying payments can delay forgiveness. Finally, consider refinancing if income increases significantly, as IDR plans may no longer be the most cost-effective option.

In conclusion, income-driven repayment plans are a double-edged sword. They provide immediate financial relief by capping payments based on income but extend the repayment timeline and allow interest to accrue. Borrowers must weigh their current financial needs against long-term costs, considering factors like career stability, tax implications, and forgiveness eligibility. With careful planning and strategic decision-making, IDR plans can be a powerful tool for managing student debt sustainably.

Biden's Student Loan Forgiveness: A Step-by-Step Application Guide

You may want to see also

Explore related products

![]()

Public Service Loan Forgiveness: Requires 120 qualifying payments, forgives remaining balance tax-free, interest accrues

The Public Service Loan Forgiveness (PSLF) program offers a lifeline to borrowers committed to public service careers, but its 120-payment requirement demands strategic planning. Unlike standard repayment plans, PSLF forgives the remaining balance tax-free after 120 qualifying payments, making it a powerful tool for debt elimination. However, interest continues to accrue during this period, raising the question: should you prioritize paying down principal or let interest grow until forgiveness?

Analyzing the Interest Dilemma:

Imagine two borrowers, both with $100,000 in student loans at 6% interest. Borrower A aggressively pays down principal, aiming to minimize interest accrual. Borrower B makes only the minimum payments required for PSLF, allowing interest to compound. After 10 years, Borrower A might have paid off a significant portion of the principal, reducing the forgiven amount. Borrower B, while facing a larger balance due to accrued interest, will have the entire remaining balance forgiven tax-free.

Crucially, the tax-free forgiveness under PSLF can offset the higher balance. For example, if Borrower B's balance grows to $130,000 due to interest, the entire $130,000 is forgiven without tax consequences, potentially saving tens of thousands compared to Borrower A who paid down principal but faces taxable income on forgiven debt under other programs.

Strategic Considerations:

- Income-Driven Repayment Plans: PSLF requires enrollment in an income-driven repayment plan. These plans cap monthly payments based on income and family size, often resulting in lower payments than standard plans. This lower payment structure can make it more feasible to let interest accrue while still meeting the 120-payment requirement.

- Career Stability: PSLF requires 10 years of qualifying employment in public service. If you're confident in your long-term commitment to a qualifying employer, the potential benefits of tax-free forgiveness may outweigh the temporary increase in balance due to interest.

- Opportunity Cost: Consider the opportunity cost of aggressively paying down principal. Could those extra funds be better invested elsewhere, potentially generating returns that exceed the student loan interest rate?

Practical Tips:

- Track Your Payments: Meticulously document each qualifying payment to ensure you reach the 120-payment threshold. The Department of Education provides tools to help track your progress.

- Recertify Annually: Income-driven repayment plans require annual recertification of income and family size. Missing a recertification deadline can disrupt your PSLF eligibility.

- Consult a Professional: Given the complexities of PSLF and tax implications, consulting a financial advisor or student loan specialist can provide personalized guidance.

Letting interest accrue under PSLF can be a strategic decision, particularly for borrowers with stable public service careers and a long-term commitment to the program. The tax-free forgiveness benefit can outweigh the temporary increase in balance, making it a powerful tool for achieving debt freedom. However, careful planning, diligent documentation, and a clear understanding of the program's requirements are essential for success.

Public Student Loan Forgiveness: Eligible Loans and Program Requirements

You may want to see also

Explore related products

$12.95 $22.99

$18.09 $19.95

![]()

Strategic Financial Planning: Invest extra funds, prioritize high-interest debt, balance savings vs. loan repayment

Student loan forgiveness programs can seem like a distant light at the end of a long tunnel, tempting borrowers to let interest accrue while they wait. However, this passive approach often leads to a larger financial burden. Strategic financial planning offers a more proactive path, balancing the need to invest, tackle high-interest debt, and maintain savings. Here’s how to navigate this complex terrain effectively.

Step 1: Invest Extra Funds Wisely

If your student loans carry a low interest rate (e.g., below 5%), consider allocating extra funds to investments with higher potential returns. For instance, contributing to a 401(k) with employer matching or investing in a diversified index fund can yield 7–10% annual returns over time. A 30-year-old investing $200 monthly at 8% interest could accumulate over $300,000 by age 65, far outpacing the cost of low-interest loan accrual. However, ensure your emergency fund is intact before diverting funds to investments.

Step 2: Prioritize High-Interest Debt

Not all debt is created equal. If you have credit card debt at 18–24% APR or private student loans above 6%, focus on paying these off first. For example, paying off a $5,000 credit card balance at 20% interest saves $1,000 annually—money better kept in your pocket than a lender’s. Use the avalanche method, targeting debts with the highest interest rates while making minimum payments on others.

Caution: Avoid Common Pitfalls

While investing can be lucrative, it’s not risk-free. Avoid tying up all extra funds in volatile assets, especially if your job security is uncertain. Similarly, don’t neglect savings entirely. Aim for 3–6 months’ worth of living expenses in an emergency fund to avoid relying on high-interest debt during unexpected crises. Additionally, monitor loan forgiveness eligibility requirements; some programs mandate consistent payments, which could disqualify you if you pause repayment.

Balancing Act: Savings vs. Loan Repayment

Deciding between saving and repaying loans requires a nuanced approach. If your loans are subsidized (no interest accrual), focus on building savings and investments. For unsubsidized loans, calculate the break-even point: compare the interest cost of delaying repayment with the potential investment gains. For instance, if your loans accrue $500 annually in interest but investments yield $800, investing makes sense. However, if you’re risk-averse or nearing forgiveness, prioritize repayment to minimize long-term costs.

Strategic financial planning isn’t one-size-fits-all. Assess your interest rates, investment opportunities, and risk tolerance to craft a personalized plan. Tools like loan calculators and financial advisors can provide clarity. By investing wisely, tackling high-interest debt, and balancing savings with repayment, you can minimize student loan costs while building wealth for the future. Remember, the goal isn’t just to wait for forgiveness—it’s to optimize your financial health every step of the way.

Is Biden's Student Loan Forgiveness Legal? Analyzing the Debate

You may want to see also

Frequently asked questions

It depends on your financial situation and the type of loan forgiveness program you’re eligible for. If you’re enrolled in an income-driven repayment (IDR) plan and qualify for Public Service Loan Forgiveness (PSLF), letting interest accrue may be manageable since the remaining balance is forgiven after meeting program requirements. However, if you’re not on track for forgiveness, paying interest could significantly increase your total debt.

No, letting interest accrue on student loans does not directly impact your credit score, as long as you continue making required payments on time. Your credit score is primarily affected by payment history, credit utilization, and other factors, not by the accrual of interest.

If you’re pursuing loan forgiveness through programs like PSLF or IDR, waiting for forgiveness while making minimum payments may be more beneficial, especially if the forgiven amount outweighs the accrued interest. However, if you’re not eligible for forgiveness or can afford to pay off the loans early, doing so can save you money on interest in the long run.

Yes, under most loan forgiveness programs, such as PSLF or IDR forgiveness, both the principal balance and any accrued interest are forgiven after meeting the program’s requirements. However, it’s important to stay in compliance with the program’s rules to ensure eligibility for forgiveness.