To introduce the topic 'what are the requirements to take out a student loan', you could start with:

Navigating the world of student loans can be a daunting task for many aspiring students. Understanding the requirements to take out a student loan is crucial for those seeking financial assistance to pursue their higher education goals. From citizenship status to credit history, and from income levels to the type of institution you plan to attend, various factors come into play when determining your eligibility for a student loan. This guide aims to demystify the process by outlining the key requirements you need to meet in order to secure the financial support you need for your academic journey.

Explore related products

What You'll Learn

- Eligibility Criteria: Citizenship, residency, academic enrollment, and financial need

- Application Process: FAFSA submission, school certification, and loan agreement signing

- Types of Loans: Federal (Direct, Perkins) vs. private loans, interest rates, and repayment terms

- Repayment Options: Income-driven plans, standard repayment, deferment, and forbearance

- Credit Checks: Impact of credit history on loan approval and interest rates

![]()

Eligibility Criteria: Citizenship, residency, academic enrollment, and financial need

To be eligible for a student loan, you must meet specific criteria related to your citizenship, residency, academic enrollment, and financial need. Each of these factors plays a crucial role in determining whether you qualify for financial assistance to pursue your education.

Citizenship is often the first criterion that lenders consider. In many countries, student loans are only available to citizens or permanent residents. This means that if you are an international student, you may not be eligible for certain types of loans unless you have a valid visa or residency permit. Some lenders may also require that you have lived in the country for a certain period of time before applying for a loan.

Residency is another important factor, as it can affect the interest rates and repayment terms of your loan. If you are a resident of a particular state or region, you may be eligible for lower interest rates or more favorable repayment terms. Additionally, some lenders may require that you maintain a certain level of residency throughout the loan period, which could impact your eligibility if you plan to move or study abroad.

Academic enrollment is also a key criterion, as lenders typically require that you be enrolled in an accredited institution and pursuing a degree or certificate. The type of institution and program you are enrolled in may also affect your eligibility, as some lenders may only offer loans for certain fields of study or types of degrees. Furthermore, your enrollment status (e.g., full-time or part-time) can impact the amount of loan you are eligible for.

Finally, financial need is a critical factor in determining your eligibility for a student loan. Lenders will assess your financial situation, including your income, assets, and expenses, to determine whether you require financial assistance to cover your educational costs. This may involve submitting documentation such as tax returns, pay stubs, and bank statements. The amount of loan you are eligible for will depend on your demonstrated financial need, as well as the lender's policies and available funds.

In summary, to be eligible for a student loan, you must meet specific criteria related to your citizenship, residency, academic enrollment, and financial need. Each of these factors plays a crucial role in determining whether you qualify for financial assistance to pursue your education. By understanding these criteria and providing the necessary documentation, you can increase your chances of securing a student loan to help cover your educational expenses.

Cultivating Culinary Skills: The Case for Cooking Classes in Schools

You may want to see also

Explore related products

![]()

Application Process: FAFSA submission, school certification, and loan agreement signing

To initiate the process of securing a student loan, prospective borrowers must first complete and submit the Free Application for Federal Student Aid (FAFSA). This form is crucial as it determines the student's eligibility for federal aid, including loans, grants, and work-study programs. The FAFSA requires detailed financial information about the student and their family, such as income, assets, and the number of family members attending college. It's essential to fill out the form accurately and submit it as early as possible, as some types of aid are awarded on a first-come, first-served basis.

Once the FAFSA is submitted, the student's chosen school will receive the results and use them to determine the amount of aid the student is eligible for. This process, known as school certification, involves the school's financial aid office verifying the information provided on the FAFSA and ensuring that the student meets all the necessary criteria for federal aid. The school will then send the student an award letter outlining the types and amounts of aid they are eligible for, including any student loans.

After receiving the award letter, the student must carefully review the terms and conditions of the loan and decide whether to accept or decline it. If the student chooses to accept the loan, they will need to sign a loan agreement, which is a legally binding document that outlines the terms of the loan, including the interest rate, repayment schedule, and any fees associated with the loan. It's important for the student to read the agreement thoroughly and ask any questions they may have before signing, as the terms of the loan will have a significant impact on their financial future.

In addition to the FAFSA and loan agreement, there may be other requirements that the student needs to fulfill in order to receive the loan funds. For example, some schools may require the student to complete a separate application for institutional aid or to provide additional documentation, such as proof of enrollment or a valid Social Security number. It's essential for the student to stay in touch with their school's financial aid office and to respond promptly to any requests for additional information or documentation.

Throughout the application process, it's important for the student to be aware of the potential risks and consequences of taking out a student loan. Student loans can be a significant financial burden, and it's essential for the student to borrow only what they need and to have a plan in place for repaying the loan after graduation. By carefully considering the terms of the loan and seeking guidance from financial aid professionals, students can make informed decisions about their financial future and minimize the risks associated with student loan debt.

Navigating College Admissions: The ACT Dilemma for Transfer Students

You may want to see also

Explore related products

![]()

Types of Loans: Federal (Direct, Perkins) vs. private loans, interest rates, and repayment terms

Federal loans, such as Direct and Perkins loans, are funded by the government and typically offer lower interest rates and more flexible repayment terms compared to private loans. Direct loans are the most common type of federal loan and are available to both undergraduate and graduate students. Perkins loans are need-based and have a fixed interest rate of 5%. Private loans, on the other hand, are offered by banks and other financial institutions and often have higher interest rates and stricter repayment terms.

When considering taking out a student loan, it's important to understand the differences between federal and private loans. Federal loans generally have a fixed interest rate, while private loans may have variable interest rates that can change over time. Additionally, federal loans often offer income-driven repayment plans, which can help make monthly payments more manageable for borrowers with lower incomes. Private loans may not offer these same repayment options.

Another key difference between federal and private loans is the application process. Federal loans require borrowers to fill out the Free Application for Federal Student Aid (FAFSA), while private loans typically require a separate application through the lender. Additionally, federal loans may have additional eligibility requirements, such as maintaining a certain GPA or enrolling in a specific program of study.

When comparing interest rates and repayment terms, it's important to consider the long-term cost of the loan. While federal loans may have lower interest rates, they may also have longer repayment terms, which can result in paying more interest over the life of the loan. Private loans, on the other hand, may have higher interest rates but shorter repayment terms, which can result in paying less interest overall.

Ultimately, the choice between federal and private loans will depend on individual circumstances and financial needs. Borrowers should carefully consider the interest rates, repayment terms, and eligibility requirements of each type of loan before making a decision. It's also important to remember that taking out a student loan is a significant financial commitment and should be approached with caution and careful consideration.

Balancing Act: Sports Participation vs. Mandatory Gym Classes

You may want to see also

Explore related products

$19.99 $8.99

![]()

Repayment Options: Income-driven plans, standard repayment, deferment, and forbearance

Navigating the repayment of student loans can be as complex as securing them in the first place. Borrowers are often faced with a variety of repayment options, each with its own set of criteria and benefits. Income-driven repayment plans, for instance, adjust monthly payments based on income and family size, potentially offering lower payments for those with lower earnings. These plans include the Revised Pay As You Earn (REPAYE), Pay As You Earn (PAYE), Income-Based Repayment (IBR), and Income-Contingent Repayment (ICR) options. Each has specific eligibility requirements, such as income thresholds and loan types, which borrowers must meet to qualify.

Standard repayment, on the other hand, is the default plan for most federal student loans, featuring a fixed monthly payment over a 10-year period. While this plan does not offer the flexibility of income-driven options, it can be a straightforward choice for borrowers with stable incomes who prefer a predictable repayment schedule. However, it's important to note that standard repayment may not be the most cost-effective option in the long run, as it does not account for changes in income or financial circumstances.

Deferment and forbearance are temporary measures that allow borrowers to postpone or reduce their loan payments. Deferment is typically granted for specific situations, such as returning to school, unemployment, or military service, and interest does not accrue on subsidized loans during this period. Forbearance, while similar, is granted at the discretion of the lender and may be used for a wider range of financial hardships. Interest continues to accrue during forbearance, which can increase the total cost of the loan over time.

Choosing the right repayment option requires careful consideration of one's financial situation, career prospects, and personal goals. Borrowers should regularly review their repayment plans and adjust as necessary to ensure they are on track to meet their financial obligations while also taking advantage of any available benefits or protections. It's also advisable to consult with a financial advisor or student loan expert to explore all available options and make informed decisions about managing student loan debt.

Decoding the Risks: Pills Popular Among College Students

You may want to see also

Explore related products

![]()

Credit Checks: Impact of credit history on loan approval and interest rates

Credit history plays a pivotal role in the loan approval process, particularly for student loans. Lenders use credit checks to assess the borrower's creditworthiness, which is a measure of their ability and willingness to repay debts. A positive credit history can significantly enhance the chances of loan approval and may result in more favorable interest rates. Conversely, a negative credit history can lead to loan denial or higher interest rates, making the loan more expensive over time.

The impact of credit history on loan approval is multifaceted. Lenders look at various factors, including the borrower's payment history, credit utilization ratio, length of credit history, and any derogatory marks such as bankruptcies or foreclosures. A consistent history of on-time payments and responsible credit usage can demonstrate to lenders that the borrower is a low-risk candidate, thereby increasing the likelihood of loan approval. On the other hand, missed payments, high credit card balances, or other negative entries on the credit report can raise red flags and suggest to lenders that the borrower may struggle to repay the loan.

Interest rates are also closely tied to credit history. Borrowers with excellent credit scores typically qualify for lower interest rates, which can lead to substantial savings over the life of the loan. For example, a student loan with a lower interest rate may result in lower monthly payments and less overall interest paid. In contrast, borrowers with poor credit scores may be offered higher interest rates, increasing the cost of borrowing and potentially making it more difficult to manage the loan repayments.

It's important for students to understand the significance of credit history when applying for loans. Building a strong credit profile takes time and effort, but it can pay off in the long run by improving access to credit and reducing borrowing costs. Students can start by making timely payments on any existing debts, keeping credit card balances low, and avoiding unnecessary credit inquiries. Additionally, regularly monitoring credit reports for errors and disputing any inaccuracies can help maintain a healthy credit score.

In conclusion, credit checks are a critical component of the student loan application process. A good credit history can open doors to loan approval and lower interest rates, while a poor credit history can create barriers and increase borrowing costs. By being proactive about managing their credit, students can position themselves for better financial outcomes when seeking loans to fund their education.

Exploring the Benefits: Should Students Take Art and Music Classes?

You may want to see also

Frequently asked questions

To be eligible for a student loan, you typically need to be a U.S. citizen or permanent resident, have a valid Social Security number, and be enrolled at least part-time in an eligible program at an accredited school.

For federal student loans, there is no credit score requirement. However, for private student loans, lenders usually check your credit score and may require a cosigner if you have poor credit.

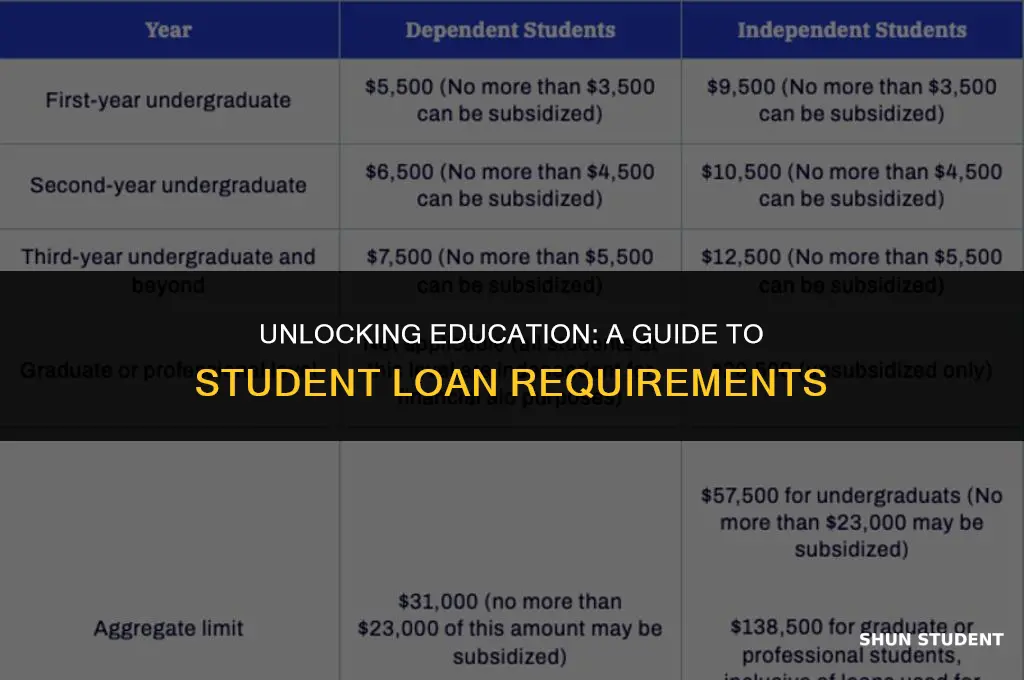

The maximum amount you can borrow with a student loan varies depending on the type of loan and your level of education. For federal loans, the limits range from $5,500 to $13,500 per year for undergraduate students, and up to $16,500 per year for graduate and professional students. Private loans can offer higher limits but depend on the lender and your creditworthiness.

To apply for a federal student loan, you need to fill out the Free Application for Federal Student Aid (FAFSA) online. For private student loans, you'll need to apply directly with the lender, which usually involves providing personal and financial information, as well as details about your school and program.