The principles of accounting provide students with a foundational understanding of financial reporting, analysis, and decision-making. These principles teach students how to record, summarize, and interpret financial transactions, ensuring accuracy and compliance with established standards such as GAAP (Generally Accepted Accounting Principles) or IFRS (International Financial Reporting Standards). Students learn to prepare financial statements, including the balance sheet, income statement, and cash flow statement, which are essential for assessing a company’s financial health. Additionally, the principles of accounting emphasize ethical practices, internal controls, and the importance of transparency in financial reporting. By mastering these concepts, students develop critical skills for careers in accounting, finance, and business management, enabling them to contribute to informed decision-making and organizational success.

Explore related products

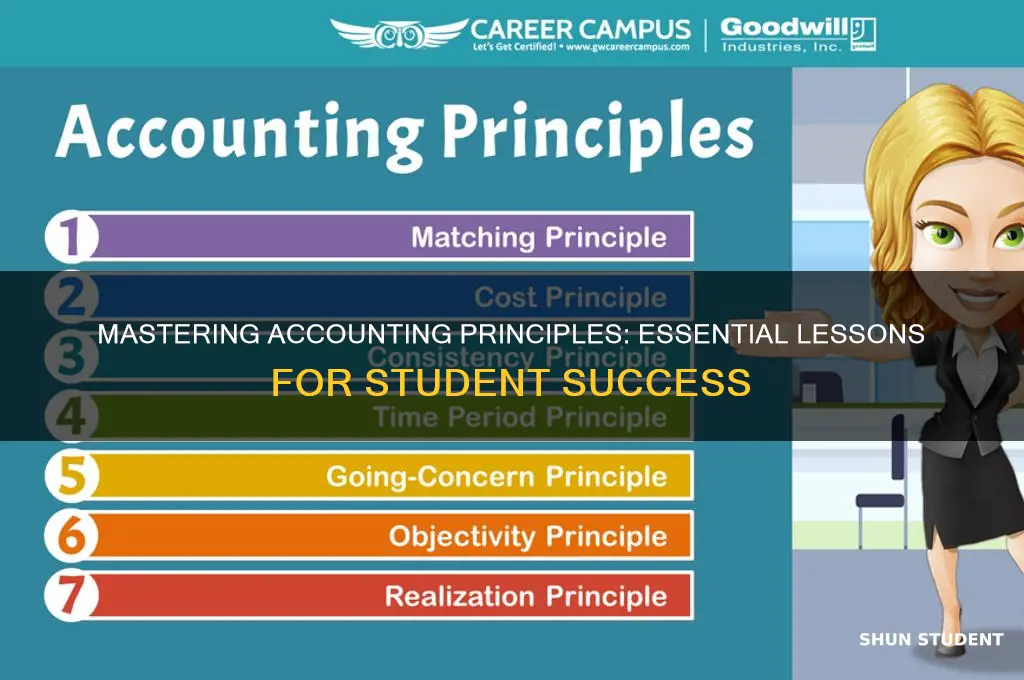

What You'll Learn

- Financial Statement Preparation: Learn to create income statements, balance sheets, and cash flow statements accurately

- Double-Entry Bookkeeping: Understand debit and credit rules for recording transactions systematically

- GAAP Compliance: Study Generally Accepted Accounting Principles for consistent financial reporting

- Cost Behavior Analysis: Analyze how costs change with business activity levels

- Ethical Accounting Practices: Develop integrity and transparency in financial decision-making and reporting

![]()

Financial Statement Preparation: Learn to create income statements, balance sheets, and cash flow statements accurately

Mastering financial statement preparation is a cornerstone of accounting education, equipping students with the skills to transform raw financial data into actionable insights. This process involves crafting three critical documents: the income statement, balance sheet, and cash flow statement. Each serves a distinct purpose, yet together they paint a comprehensive picture of an entity’s financial health. The income statement reveals profitability over a period, the balance sheet snapshots assets, liabilities, and equity at a moment in time, and the cash flow statement tracks liquidity movements. Without this knowledge, financial decision-making becomes guesswork, leaving businesses vulnerable to missteps.

Consider the income statement, often the first financial document students learn to prepare. It begins with revenue, subtracts expenses, and culminates in net income or loss. A common pitfall is misclassifying expenses—for instance, treating a capital expenditure as an operating expense. To avoid this, students must understand the difference: operating expenses (e.g., rent, salaries) impact day-to-day operations, while capital expenditures (e.g., equipment purchases) are long-term investments. A practical tip: use depreciation schedules to allocate capital costs over time, ensuring accuracy in expense reporting.

The balance sheet, on the other hand, demands precision in aligning assets, liabilities, and equity. Students often struggle with the equation: Assets = Liabilities + Equity. A real-world example illustrates its importance: a company overstates inventory (an asset) without adjusting cost of goods sold (an expense), inflating both the balance sheet and income statement. To prevent such errors, reconcile accounts regularly—for instance, compare physical inventory counts to recorded values monthly. This practice ensures the balance sheet remains a reliable reflection of financial position.

Cash flow statements bridge the gap between accrual accounting and actual cash movements, categorizing flows into operating, investing, and financing activities. A common challenge is reconciling net income to cash from operations. Students should focus on adjusting for non-cash items like depreciation and changes in working capital. For example, an increase in accounts receivable reduces cash flow, even if sales revenue rises. A useful strategy: prepare a T-account for each working capital component to track changes systematically.

In conclusion, financial statement preparation is both an art and a science, requiring meticulous attention to detail and a strategic mindset. By mastering these documents, students not only ensure compliance with accounting standards but also empower stakeholders to make informed decisions. Whether analyzing profitability, assessing solvency, or evaluating liquidity, the ability to prepare accurate financial statements is indispensable in the accounting profession. Practice, paired with a deep understanding of underlying principles, transforms this skill from theoretical knowledge into a powerful tool for financial storytelling.

Should You Drop Student Teaching? Weighing Pros, Cons, and Alternatives

You may want to see also

Explore related products

![]()

Double-Entry Bookkeeping: Understand debit and credit rules for recording transactions systematically

Double-entry bookkeeping is the cornerstone of modern accounting, ensuring every financial transaction is recorded accurately and systematically. At its core, this method relies on the fundamental principle that every debit must have a corresponding credit, maintaining the balance of a company’s books. Students learning the principles of accounting quickly discover that mastering this system is essential for tracking assets, liabilities, equity, revenue, and expenses with precision. Without it, financial statements would lack reliability, undermining decision-making for businesses and stakeholders alike.

To understand double-entry bookkeeping, one must first grasp the rules governing debits and credits. Contrary to common intuition, debits do not inherently signify losses, nor do credits represent gains. Instead, their application depends on the account type. For instance, debiting an asset account increases its balance, while debiting a liability account decreases it. Conversely, crediting an equity account increases owner’s equity, whereas crediting an expense account reduces it. A practical example: purchasing office supplies for $500 involves debiting the Supplies account (an asset) and crediting the Cash account (another asset), reflecting the transfer of value within asset categories.

The systematic nature of double-entry bookkeeping ensures errors are easily identifiable. If a transaction is recorded incorrectly, the trial balance—a summary of all debits and credits—will not reconcile. For instance, failing to credit Cash when recording a $1,000 sale would result in a $1,000 discrepancy. This built-in check mechanism underscores the method’s reliability, making it indispensable for auditors and accountants. Students practicing this system learn to approach transactions methodically, reducing the likelihood of mistakes in real-world applications.

A key takeaway for students is that double-entry bookkeeping is not merely a mechanical process but a foundational skill for financial analysis. By understanding how transactions affect multiple accounts simultaneously, learners can interpret financial statements more effectively. For example, recognizing that a loan repayment involves debiting the Loan Payable account (a liability) and crediting Cash (an asset) highlights the interplay between different financial elements. This insight prepares students to analyze cash flow, profitability, and solvency with greater clarity and confidence.

In practice, mastering double-entry bookkeeping requires repetition and attention to detail. Students should start by categorizing accounts into assets, liabilities, equity, revenue, and expenses, then practice recording transactions in pairs. Tools like T-accounts can simplify the learning process, visually representing debits on the left and credits on the right. Over time, this practice becomes second nature, enabling accountants to maintain accurate records even in complex scenarios. Ultimately, double-entry bookkeeping is more than a principle—it’s a discipline that transforms raw data into meaningful financial insights.

Florida Teachers' Training: Are They Equipped for Disabled Students?

You may want to see also

Explore related products

![]()

GAAP Compliance: Study Generally Accepted Accounting Principles for consistent financial reporting

GAAP compliance is the cornerstone of reliable financial reporting, ensuring that businesses present their financial health in a standardized, comparable manner. Students of accounting must grasp the Generally Accepted Accounting Principles (GAAP) not merely as rules but as a framework for transparency and trust in financial markets. These principles dictate how transactions are recorded, assets valued, and financial statements prepared, providing a common language for investors, creditors, and regulators. Without GAAP, financial statements would be as chaotic as a library without a cataloging system, rendering them nearly useless for decision-making.

To achieve GAAP compliance, students should begin by studying the ten core principles outlined in the framework. These include the principles of regularity, consistency, sincerity, permanence of methods, non-compensation, prudence, continuity, periodicity, materiality, and utmost good faith. For instance, the principle of materiality teaches students to recognize that not all financial information is equally significant; only items that could influence economic decisions need detailed reporting. Practical application involves analyzing real-world financial statements to identify GAAP adherence, such as verifying if revenue recognition aligns with the matching principle.

One critical aspect of GAAP compliance is the consistent application of accounting methods over time. Students must understand that switching methods—say, from FIFO to LIFO inventory valuation—without proper disclosure can distort financial comparisons. A cautionary tale is the 2001 Enron scandal, where non-compliance with GAAP led to fraudulent financial reporting, resulting in bankruptcy and regulatory reforms. To avoid such pitfalls, students should practice reconciling financial statements using GAAP guidelines, ensuring that every entry is justified and every method is consistently applied.

Finally, GAAP compliance is not just about following rules; it’s about fostering accountability and integrity in financial reporting. Students should engage in case studies that highlight the consequences of non-compliance, such as fines, loss of investor confidence, or legal action. For example, a company failing to disclose contingent liabilities in accordance with GAAP could face penalties from the SEC. By internalizing these principles, students not only prepare for professional exams like the CPA but also develop the ethical mindset required to uphold the credibility of the accounting profession. GAAP compliance is thus both a technical skill and a moral imperative.

Obama's Take on Student-Teacher Respect: When Students Talk Back

You may want to see also

Explore related products

$13.37 $14.99

$19.2 $35

![]()

Cost Behavior Analysis: Analyze how costs change with business activity levels

Understanding cost behavior is a cornerstone of managerial accounting, teaching students how costs respond to changes in business activity. This analysis categorizes costs into fixed, variable, and mixed, each with distinct patterns. Fixed costs, like rent or salaries, remain constant regardless of output, providing stability in budgeting. Variable costs, such as raw materials or sales commissions, fluctuate directly with production or sales volume, offering scalability. Mixed costs, a blend of both, include elements like utilities, where a base charge is fixed, but usage-based fees vary. By mastering these classifications, students learn to predict financial outcomes under different scenarios, a critical skill for decision-making.

To illustrate, consider a bakery producing artisanal bread. The monthly rent of $2,000 is a fixed cost, unchanged whether the bakery sells 100 loaves or 1,000. Flour, a variable cost, increases proportionally with production—if 100 loaves require $200 in flour, 1,000 loaves would cost $2,000. Electricity, a mixed cost, includes a $100 base charge plus $0.10 per kilowatt-hour used. During peak production, electricity costs might rise to $300, reflecting higher usage. This example highlights how cost behavior analysis enables precise forecasting and cost control, essential for profitability.

A practical approach to cost behavior analysis involves three steps. First, identify cost drivers, such as machine hours or units produced, that influence cost variability. Second, collect historical data to plot cost patterns against activity levels. Third, use regression analysis or the high-low method to separate fixed and variable components in mixed costs. For instance, the high-low method calculates variable cost per unit by dividing the difference in costs between high and low activity periods by the corresponding change in activity. This method, while simple, provides valuable insights for short-term decision-making.

However, students must be cautious of assumptions in cost behavior analysis. Costs classified as variable may become fixed at certain thresholds, such as when a company reaches capacity and must invest in additional machinery. Similarly, fixed costs can vary over time due to renegotiated contracts or inflation. For example, a long-term lease might include escalation clauses, turning a seemingly fixed cost into a mixed one. Recognizing these nuances ensures more accurate analysis and strategic planning.

In conclusion, cost behavior analysis equips students with the tools to dissect cost structures, forecast financial impacts, and optimize resource allocation. By understanding how costs evolve with business activity, they can support informed decisions, from pricing strategies to production scaling. This analytical skill is not just theoretical but directly applicable in real-world scenarios, making it a vital component of accounting education. Mastery of cost behavior transforms raw data into actionable insights, bridging the gap between financial theory and practical management.

Understanding Student Teaching Duration in National Law Universities

You may want to see also

Explore related products

![]()

Ethical Accounting Practices: Develop integrity and transparency in financial decision-making and reporting

Accounting principles are not merely about numbers and spreadsheets; they are the bedrock of ethical financial practices that shape the integrity of businesses and economies. Among these principles, ethical accounting practices stand out as a critical lesson for students, emphasizing the importance of integrity and transparency in financial decision-making and reporting. These values are not just theoretical ideals but practical tools that ensure trust, accountability, and long-term sustainability in any organization.

Consider the collapse of Enron in 2001, a stark example of what happens when ethical accounting practices are ignored. The company’s fraudulent financial reporting led to billions in losses and eroded public trust in corporate governance. This case underscores the necessity of teaching students not just *how* to account for transactions, but *why* ethical practices matter. Integrity in accounting means adhering to standards like GAAP (Generally Accepted Accounting Principles) or IFRS (International Financial Reporting Standards), even when it’s tempting to manipulate figures for short-term gains. Transparency, on the other hand, involves clear, accurate, and accessible financial disclosures that allow stakeholders to make informed decisions.

To develop these qualities, students must be taught to think critically about the ethical implications of their decisions. For instance, when faced with a scenario where revenue recognition could be accelerated to meet quarterly targets, they should weigh the immediate benefits against the long-term risks of misrepresentation. Practical exercises, such as case studies or role-playing ethical dilemmas, can reinforce these lessons. Additionally, integrating real-world examples like the Wells Fargo scandal or the Volkswagen emissions scandal can illustrate the consequences of ethical lapses and the importance of whistleblowing mechanisms.

A key takeaway for students is that ethical accounting is not just about avoiding legal penalties; it’s about building a reputation for trustworthiness. Companies like Patagonia and Unilever are often cited as examples of organizations that prioritize transparency and ethical practices, which has bolstered their brand value and customer loyalty. By embedding these principles early in their education, students learn that ethical accounting is a competitive advantage, not a bureaucratic burden.

In conclusion, teaching ethical accounting practices goes beyond technical skills—it cultivates a mindset of responsibility and honesty. Students who grasp the importance of integrity and transparency are better equipped to navigate complex financial landscapes, ensuring they contribute to a more accountable and sustainable business environment. This is not just a lesson in accounting; it’s a lesson in leadership.

Empowering Math Learning: Strategies for Students with Disabilities

You may want to see also

Frequently asked questions

The principles of accounting teach students the fundamental concepts, rules, and standards for recording, analyzing, and reporting financial transactions to ensure accuracy, consistency, and transparency in financial statements.

The principles of accounting provide students with the tools to interpret financial data, enabling them to make informed decisions by understanding a company’s financial health, profitability, and liquidity.

Students learn essential skills such as bookkeeping, financial statement preparation, auditing, and compliance with accounting standards, which are critical for careers in finance, business, and related fields.

Understanding accounting principles helps non-accounting professionals grasp financial concepts, communicate effectively with financial teams, and make strategic decisions that align with organizational goals.